Serabi Gold has now released its final results for the year ended 2015.

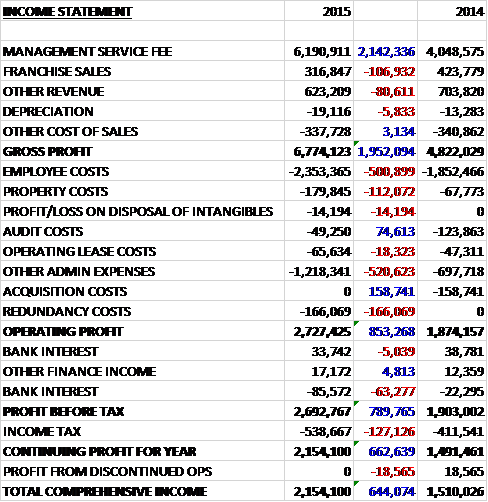

Revenues increased when compared to last year with a full year contribution of production from the Palito mine. Gold Bullion revenues increased by $8M and concentrate revenue was up $14.4M. Cost of sales increased by $13.9M, depreciation was up $1M and amortisation grew by $2.2M reflecting the fact that there was a whole year of commercial production at Palito this year to give a gross profit $5.4M above that of 2014. Admin expenses were up modestly, and share based payments increased by $145K but we also see the lack of provision write-backs which gave an income of $2.9M last year which meant that there was a $2.2M swing to an operating profit this year. This was entirely wiped out by $951K of loan interest and $527K of finance costs on the Sprott loan. In addition there was a £638K increase in the gains on financial instruments relating to the warrants and after $525K of income tax costs due to unrecognised tax losses being carried forward, the loss for the year came in at $49K, an improvement of $126K year on year.

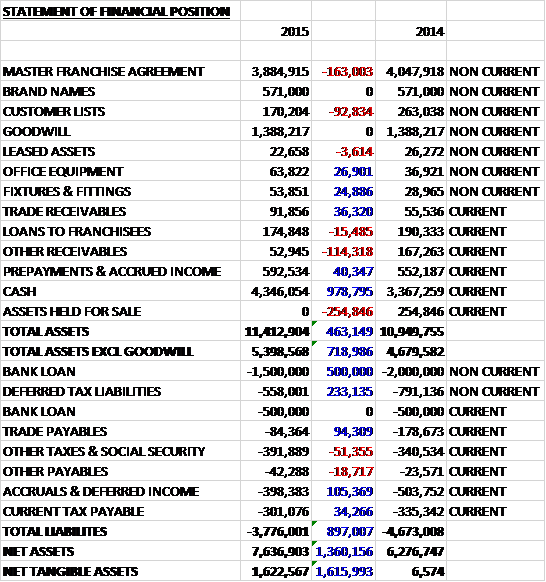

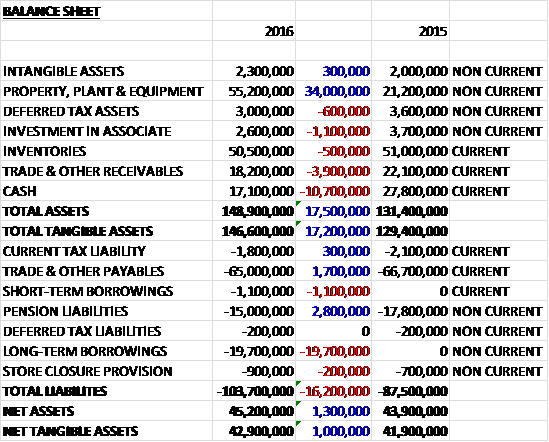

When compared to the end point of last year, total assets declined by $26.6M driven by a $12.1M fall in the value of mining property due to the depreciation of the Brazilian Real, a $7.6M reduction in cash, a $1.9M decrease in projects in construction, a $3.1M fall in development and deferred exploration costs, also due to the depreciation of the Real, and a $1.2M fall in inventories, mainly as a result of a fall in the stockpile of flotation tails. Total liabilities also decreased during the year due to a $4.9M fall in other loans and borrowings and a $919K decrease in the environmental rehab provision, also due to the depreciating currency. The end result was a net tangible asset level of $38.1M, a decline of $17M year on year.

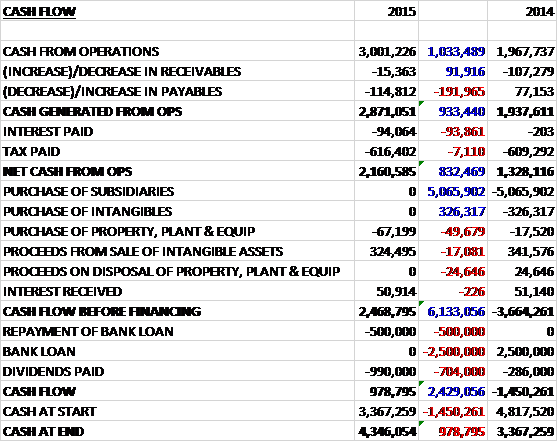

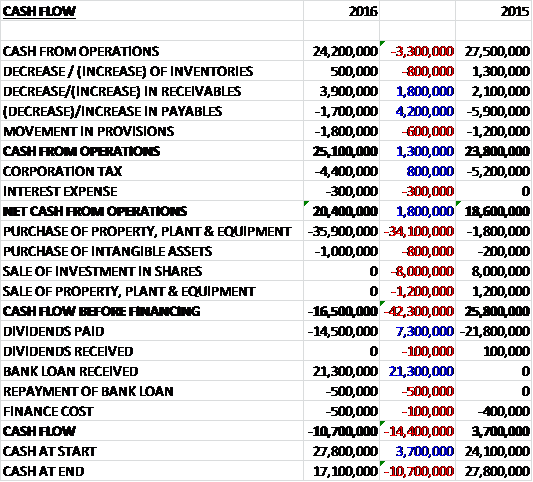

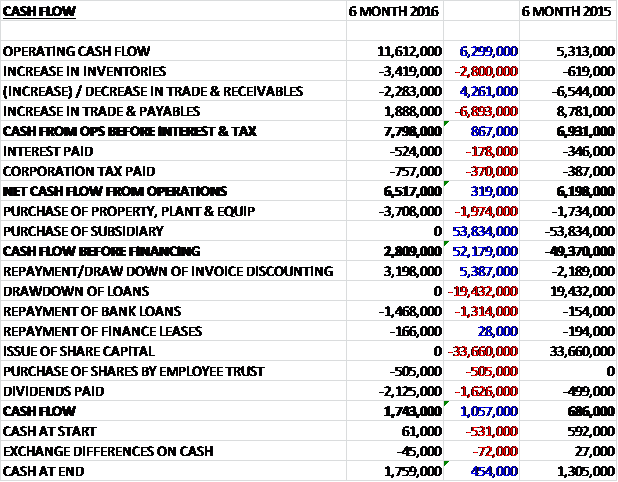

Before movements in working capital, cash profits increased by $5.9M to $4.5M. There was a broadly neutral movement in working capital compared to a large increase in receivables last year so that the cash from operations was $4.4M, a positive swing of $17.1M year on year. The Sao Chico mine contributed a net cash loss of $2.1M and the group also spent $3M on property, plant and equipment, along with $1.5M on exploration and development to give a cash outflow of $1.5M before financing. The group paid $758K in finance leases and paid back $4M of the Sprott loan and after a $1.1M cash outflow on the short term trade finance arrangement the cash outflow for the year came in at $7.4M to give a cash level of $2.2M at the year-end.

All in all, the gold produced during the year was as follows:

Q1 7,389 ounces

Q2 8,237 ounces

Q3 9,078 ounces

Q4 7,925 ounces.

During the year the group produced 32,629 ounces of gold having mined 135,827 tonnes at a grade of 9.8g/t. The average gold price achieved was $1,151 per ounce, although the price at the end of Q4 was $1,063 per ounce, and the all-in sustaining costs were $892 per tonne. The year was dominated by a falling gold price but a mitigating effect of local currency weakness. So far this year, the average LMBA price has been $1,178 per ounce although there has been a tendency in recent years for prices in Q1 to be strong with a decline over the remainder of the year. There are some commentators who expect gold prices to make a gradual recovery in 2016, driven in part by contraction on global mine production and increasing demand from Asia.

The production in Q4 was adversely affected by power generation problems at the Sao Chico mine which delayed mining activities. The shortfall in what was supposed to be high grade Sao Chico development ore feed was replaced by surface stockpiled ore from the Palito mine at a lower grade. By December the problems were resolved and the Sao Chico mine turned in its best month of the year with over 4,000 tonnes mined at grades in excess of 11.5g/t.

About 33,959 tonnes were produced in Q4 in total which represents an increase of 34% compared with Q4 2014 with 7,000 tonnes of this increase coming from Sao Chico, which was not in production this time last year, and 1,600 tonnes of this increase representing a growth in Palito production. Going forward, Palito is expected to produce about 27,000 tonnes a quarter, so at a similar level.

The Palito mine has continued to perform well with the level of mine output exceeding the group’s internal plans. Tonnage of Palito ore processed through the gold recovery plant exceeded internal plans by 9% and the total contained gold processed exceeded plans by 14% with the Gold production from the run of mine ore exceeding the plan by 10%. This increase in the level of ROM processed did, however, reduce the ability of the group to process stockpiled material and the stockpile of coarse ore that the group had hoped to run down during the year remained at approximately 10,000 tonnes at the year-end whilst only about 18,500 tonnes of flotation tailings were processed out of the total volume of 56,000 tonne as the start of the year.

The Palito mine generated about 111,751 tonnes of ore at a grade of 10.05g/t during the year and management expect that mine output for 2016 will be between 105,000 tonnes and 110,000 tonnes at an average grade of between 8.5g/t and 8.9g/t of gold. The gold production in 2016 will be supplemented by the processing of surface stockpiles of ROM ore and about 37,500 tonnes of flotation tailings generated in 2014.

Labour costs increased from $9.75M to $10M due to an increase in the staff numbers and pay increases for staff – the relatively modest increase was due to the depreciation of the local currency. The cost of mining consumables of $3.78M increased by 3% in dollar terms and 47% on a local currency basis as a result of increased activity. Maintenance costs of $1.23M decreased by 14% due to the favourable exchange rate movement with costs in the local currency increasing as the mining fleet grew. Plant operating costs increased by 82% to $3.38M due to an increase in productivity as the costs per tonne fell.

During the year the group completed a cross cut to the Chico da Santa zone in October and to the Senna zone in December. The opening up of these new sectors allows them to establish more ore faces and stoping areas. In the case of the Senna zone, there has never been any previous underground development on the ore zone but based on the ore grades recovered from the limited pit operations of over 3g/t, management is hopeful of the potential within the zone where they have recorded a drill intersection in hole PDD289 of 0.55 metres at a grade of just under 51g/t at about 300 metres below the surface.

The group continued mine development towards the Palito South area which has been driven some 700 metres further south than any other underground working at the mine. Having intercepted numerous high-grade pay shorts, the group are now testing the down-dip continuity of these pay shorts for future development of the mine at depth, as well as incorporating the up-dip extensions of the pay shoots in the upper levels into its future mine plans which represent an excellent potential source of additional ore.

The performance of the Sao Chico mine was below the group’s internal plans for 2015. Whilst the group remains optimistic about the long-term potential for the mine, the orebody has, to date, been more complex than the surface drilling results has suggested. The implications for mining methodology and grade control only became apparent once access through underground development had been established at the start of Q2. The production at the mine during the year was about 3,150 ounces representing less than 40% of the initial targets. Commercial production at the mine was declared at the start of 2016 reflecting mine outputs having been achieved over a sustained period of time at levels agreed as being necessary to consider that a viable long term operation had been established.

During the year about 2,800 metres of development had been achieved and in January the ramp development intersected the principal vein about 30 metres below the portal entrance. The initial sampling confirmed a payable intersection with a true width of 3.6 metres and a gold grade of 42g/t.

The immediate priority is to evaluate and define stoping blocks on the first four levels to secure mine production for the next year and a half. Further ramp development will therefore be progressed to pursue the down-dip extension of the current areas that are in development. The rates of lateral development on existing levels will be increased when the group has greater confidence in the distribution of the high grade mineralisation within the lateral strike extensions.

As previously reported, the high grade mineralisation is dominantly hosted in a consistent alteration zone that can be anything from two to ten metres wide. The alteration zone itself is readily identifiable but the high grade gold zones within the zone are much less so, and as a result the mining operations will require on-lode development at regular vertical intervals, with regular channel sampling and in-fill drilling between these levels to best define the high grade gold mineralisation. This approach will allow the group’s mining personnel to readily identify stoping blocks and optimise mining the high grade zones.

The group is continuing to progress the conversion of the exploration license at the mine to a mining license. As the next major step in the conversion procedure, in September they submitted a form of economic assessment prepared in accordance with Brazilian legislation. With the trial mining license already in place, all mining operations can continue in parallel, however. A submission for a further extension for a period of one additional year was also submitted in September. The issuing of the mining license requires the submission of a risk assessment and management plan, safety assessments, environmental and social impact studies and these additional reports have either been submitted or are being submitted when requested to the relevant government bodies.

Reflecting the higher volumes of ore that the group expects to produce and process, a third ball mill was acquired in Q4 2015 and will become operational during Q2 2016. During the year the group also acquired and commissioned an in-line Leach Reactor for processing the high grade gravity concentrate that is produced from the processing of the Sao Chico ores. This will help improve overall gold recovery levels and increase the processing capacity of the Carbon in Pulp process circuit. The improvements should cost about $1.2M, funded from the cash flow of the current operations. The group has also been introducing further improvements to its process plant targeted to increase process capacity and overall gold recoveries which averaged 90% during 2015.

As well as the potential that exists to grow resources at Sao Chico, the Palito South , Currutela and Piaui prospects still provide excellent opportunities for identifying additional resources which could enhance current production levels and extend the mine life. At this time, no surface drilling or other surface exploration activities are currently planned on the group’s properties but once adequate cash flow is being generated, they will step up exploration activity and will be looking to add to the resource base and production potential by establishing additional satellite high grade gold mines close to the current Palito operation which would be a centralised processing facility.

The mining fleets at the mines are relatively new and in total the group operates with a fleet of seven 20 tonne trucks, five underground drilling jumbo rigs and dour underground loaders. The group also owns various other mobile equipment including four front end loaders, a bulldozer and other smaller vehicles. Whilst further equipment purchases are planned during 2016, both mining operations are now well equipped. Transportation of the ore from the Sao Chico mine to the Palito processing plant is undertaken by a contractor and began in February 2015.

The total volume of ore processed during the year was 130,299 tonnes. Milling performance at the start of Q1 was affected by power stoppages resulting from an inconsistent electricity supply from CELPA, the regional power company. The reliability of power has remained subject to fluctuations and interruption which is particularly detrimental to the performance of the gold processing plant. As a consequence, during Q2 the group took the decision to commit to the use of diesel generated power for the operation of the plant as management expects the benefits of increased plant availability will significantly outweigh the increased operational costs but the power requirements of mining operations continue to me met by CELPA except in exceptional circumstances.

To enable processing of ore from the Sao Chico mine through the Palito gold recovery plant, a separate process line was established with a dedicated feed hopper which can feed one of the two mills that have been in operation during the year with a dedicated feed of Sao Chico ore. The construction of the hopper was completed at the end of Q1 2015 and after an initial commissioning period using ore from the Palito mine, the processing of the Sao Chico ore commenced in April. In the short term the crushed and milled Sap Chico ore has passed directly to the CIP plant but during Q3, the group acquired an ILR which was commissioned during November and with this now fully operational the milled Sao Chico ore can be passed initially through a gravity concentrator with the recovered gravity concentrate containing gold passing through the ILR where in a small closed circuit it is leached with high concentrations of cyanide, dissolving the gold. The gold in solution is them recovered by conventional smelting. This use of the gravity concentrator enhances gold recovery for the Sao Chico ore and creates efficiencies in the CIP plant and the ability to increase flow rates.

The slower start-up of the Sao Chico mine which necessitated an increased level and longer period of financial support for this new operation placed pressure on the group’s ability to generate positive cash flow from operations. To compensate for falling gold prices during the year and after the year-end, the group renegotiated the repayment terms of its financial arrangements with Sprott.

At the end of the year the group entered into an agreement with the major shareholder, Fratelli Investments, in which they received an unsecured short term working capital convertible loan facility of $5M to provide additional working capital facilities and in January they drew down $2M against the facility. The balance of the facility may be drawn down at any time up to the end of June 2016 and it is to be repaid by January 2017. It comes with a hefty interest rate of 12% per annum but there is no prepayment penalty or arrangement fee. The first $2M of the loan is convertible at the election of Frateli into new shares at an exercise price of 3.6p each.

The remaining amount of the loan, if drawn down, may be repaid by the group at its option at any time before the end of June 2016 after which, Frateli will have the right to convert all or part of the remaining amount into Serabi shares at an exercise price of 3.6p.

They also have a secured loan facility with Sprott which carries an interest rate of 10% per annum and is repayable by the end of 2016 with the amount outstanding on this loan being $4M. The directors think that the group now has access to sufficient funding for its immediate projected needs and they expect to have sufficient cash flow from its forecast production to finance its ongoing operational requirements and to pay back the loan facilities along with, in part, funding exploration and development activity on its other gold properties. There are a number of undertakings that the group has provided with regards the Sprott loan including an undertaking to maintain working capital in excess of $2.5M excluding any amount due to Sprott of Fratelli, and a minimum of $1M in unrestricted cash.

The company issued 100,000,000 warrants in March 2014 which gave rise to a liability of $1.7M at the date of issue. At the end of 2015, the fair value of these warrants was assessed to be nil (compared to $332K in the prior year) and they expired in March 2016 with none having been exercised.

A significant element behind the decrease in current liabilities relates to the fair value provision for a property acquisition payment that is due to a past owner of the Sao Chico property. This is currently valued at $1.75M and the group expects that under the contractual terms the first instalment will become payable in Q2 2017, instead of the originally forecasted June 2015. As the payment terms have been deferred, all of the provision is included in non-current liabilities. There is no longer a liability for derivatives as they have all expired. The liability for derivatives was valued at $529K and all provisions have been released to the income statement during the year.

In 2016 the group is forecasting gold production of about 37,000 ounces with all-in sustaining costs of between $840 and $870 per ounce. In all, the group expects Palito to produce about 127,000 tonnes per annum and during 2016 to run down stockpiles of course ore and flotation tailings whereas Sao Chico is going to be in its first full year of production in 2016 with the mine producing between 30,000 and 33,000 tonnes per annum. The average LOM gold production from 2017 is 42,000 ounces and the production period is eight years for Palito and seven years for Sao Chico. These plans assume a gold price of $1,150 per ounce. As of the 1st January 2016, the Sao Chico mine entered into commercial production. Going forward, the board is confident that the group will meet or even exceed their targets for the next year.

As the group made a loss during the year, we can’t really gain much from looking at PE ratios in 2015 and I can’t find any forecasts for next year.

Overall then, this has been a bit of a mixed year for the group. They are nearly at the break-even level but this was only due to a gain from the expiry of the warrants and the operating profit was wiped out by financing costs. Net assets declined due to the depreciation of the Brazilian Real but there was a cash inflow from operations as opposed to last year’s outflow, although there was an outflow before financing. Gold production in Q4 was below that of Q2 and Q3 due to power generation problems at Sao Chico meaning that lower grade stockpiled ore was used. These issues have been resolved now, however.

The Palito mine performed well in it’s first full year of commercial production but the going at Sao Chico was more challenging as the ore body is proving more complex than initially expected which has meant that production is slower than expected. Despite this, the mine has entered commercial production but there remains much to be done to fully understand the ore body and get it contribution in the way that it should.

The group achieved an average gold price of $1,151 during the year and so far in Q1 the gold price has averaged $1,178 which bodes fairly well for the year, although the board have cautioned that Q1 is often strong with regards the gold price and it tends to drift as the year progresses. The all-in costs of $892 per ounce were pretty good and the group expects these to fall further to $870 per ounce going forward.

In conclusion then, the investment case here is pretty good if the gold price can be sustained at this level but it starts to look a bit shaky if it falls. There is some headroom with regards the cash position due to a supportive majority shareholder so I don’t think a placing is on the cards for the foreseeable future. A tricky one this, I am tempted to take a nibble.

On the 20th April the group released an update covering trading in Q1. The mine production totalled 37,546 tonnes which included 26,752 tonnes at a grade of 11.84g/t from Palito and 10,794 tonnes at 9g/t from Sao Chico which meant that 9,771 ounces of gold was produced compared to 7,924 ounces last quarter. At the end of the quarter, the combined surface stockpiles totalled 17,000 tonnes at a grade of 5.3g/t with the accumulation as a result of the overall limitations in the capacity of the gold processing plant.

The installation of the third ball mill is nearly complete, along with the second flotation line and enhancements in the carbon in pulp plant. The works are on schedule to be completed by the start of May. A carbon regeneration kiln is also being acquired which will assist in enhancing gold recoveries once it is operational in H2 of this year. Following the completion of the improvements, it is anticipated that plant processing capacity could be increased from the current levels of about 400 tonnes per day to over 500 tonnes. This will be in excess of production levels, allowing the stockpiles to be depleted and creating surplus capacity to catch up any lost production caused by unplanned stoppages.

The lateral expansion of the Palito mine, completed at the end of 2015, has opened up the Senna and Chico da Santa sectors. Senna especially is returning some very encouraging mineable grades to date. Underground drilling is being used to evaluate numerous known but underexplored veins and together with these two new sectors, the group hope to open up numerous new mining faces in the upper levels. These have the advantage of being in close proximity to existing mine infrastructure and will not require any new ramp development.

At Sao Chico, outside the pay shoots the vein is continuous but with low gold grades and as a result it is unavoidable that as the mine development passes between the pay shoots, lower grade ore has to be mined. The central pay shoot is the most established of the four and is some 100m long. The group are focusing on developing this part of the main vein and are now seeing some consistent higher grade development ore as a result. The other pay shoots along the strike will be developed later in the year.

The group expects to produce 28,000 ounces of gold this year from the processing of Palito ROM and stockpiles. With the Sao Chico mine now under development, they also expect production of 9,000 ounces of gold from ore mined there and as a result, the board remain confident of achieving their production forecast of 37,000 ounces for the year with an all-in sustaining costs of between $840 and $870 per ounce, which looks impressive to me.

I do think this company would probably make a good investment but I have heard rumours of an acquisition on the way. If this is true, I would prefer to wait to see where the funding is coming from for that before buying the shares.