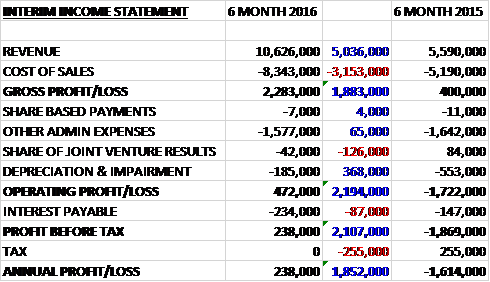

Newmark Security has now released its interim results for the year ending 2016.

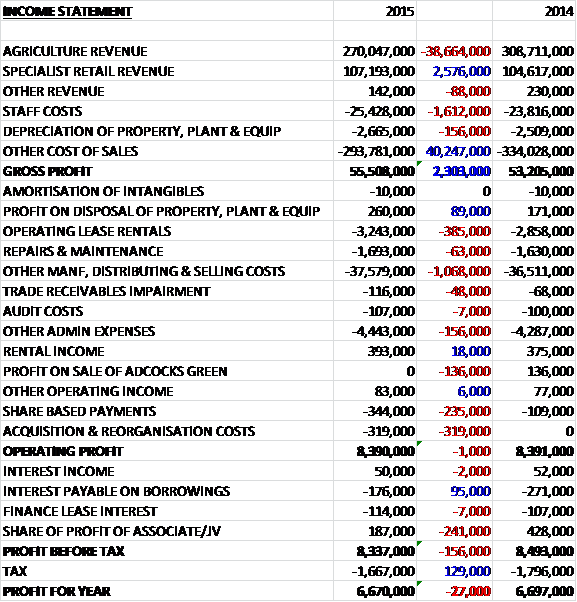

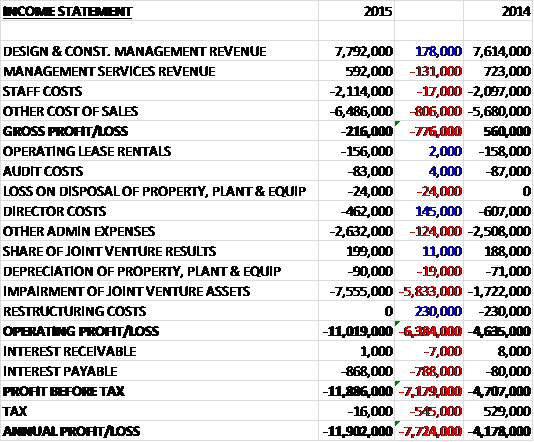

Revenues declined when compared to the first half of last year with a £532K fall in electronics revenue and a £212K decrease in asset protection revenue. Depreciation & amortisation increased by £42K but this was offset by a £307K decline in other cost of sales to give a gross profit £479K lower than last time. Admin expenses increased which meant that the operating profit was down £803K but a lower tax charge gave a profit for the half year period of £679K, a decline of £721K year on year.

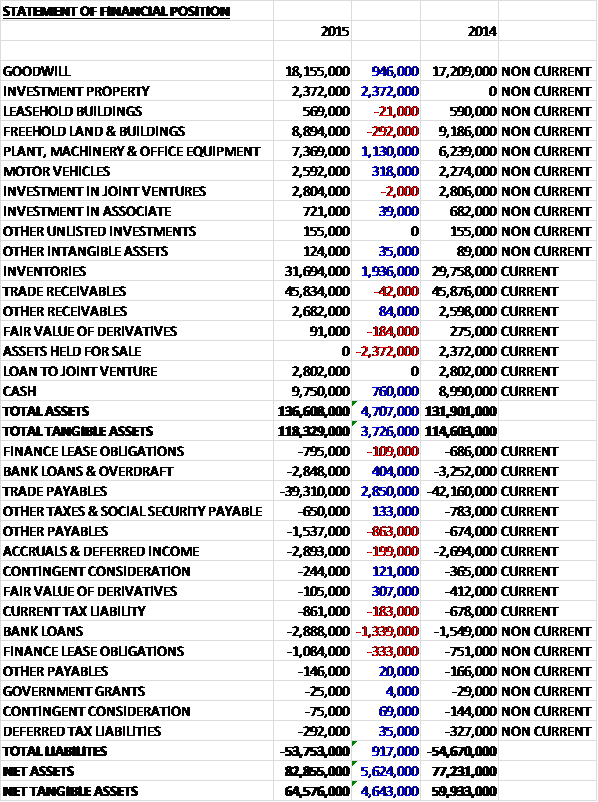

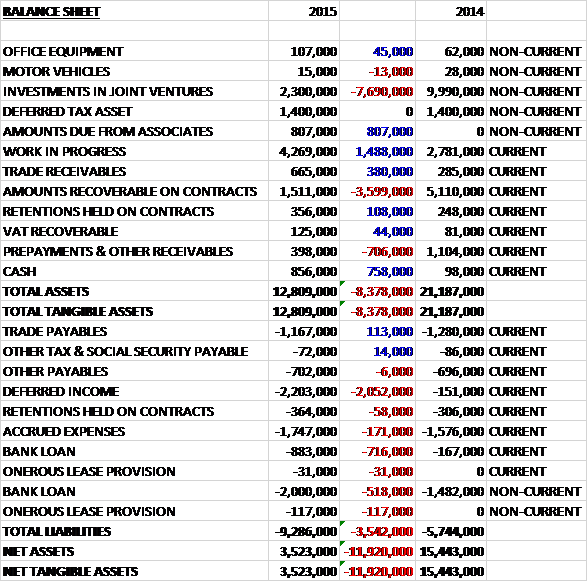

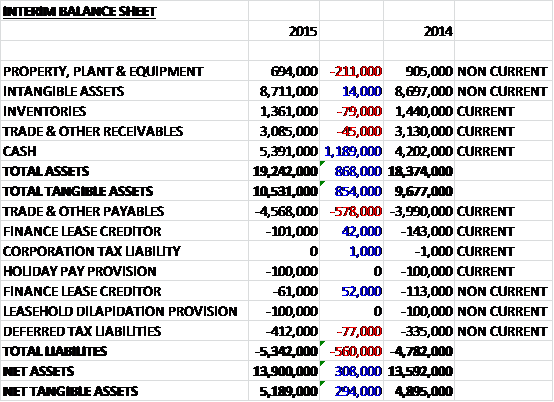

When compared to the end point of last year, total assets grew by £854K driven by a £1.2M increase in cash, partially offset by a £211K decline in property, plant and equipment. Total liabilities also grew during the period, mainly due to a £578K increase in payables. The end result is a net tangible asset level of £5.2M, an increase of £294K over the past six months.

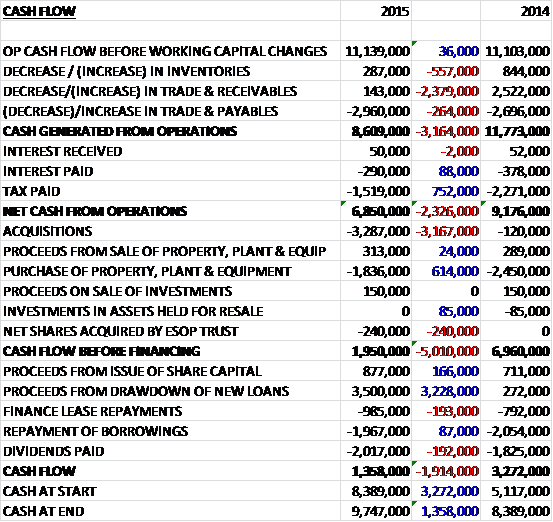

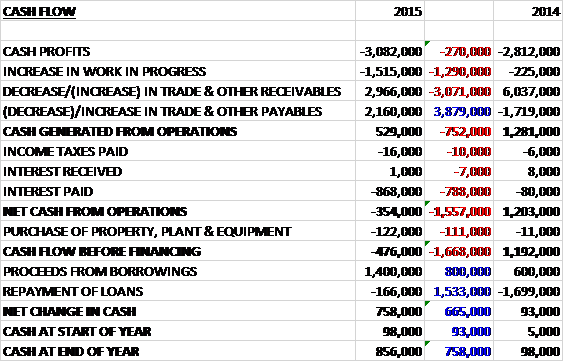

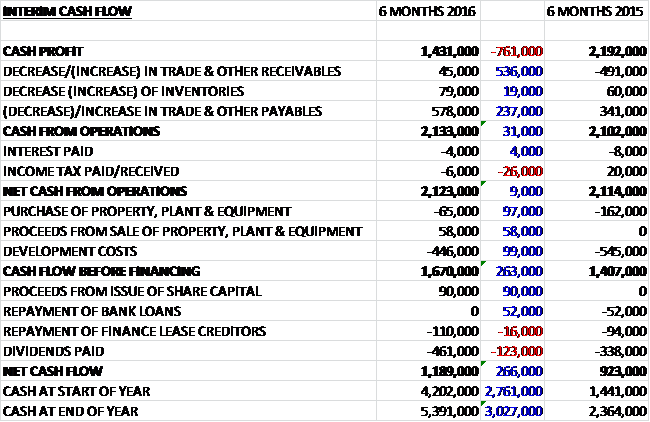

Before movements in working capital, cash profits declined by £761K to £1.4M. There was a cash inflow from working capital, however, with a sizeable growth in payables and a fall in receivables compared to a big increase last time, which meant that after a small tax bill was paid (compared to a receipt last time) the net cash from operations came in at £2.1M, broadly flat year on year. The group spent a net £7K on property, plant and equipment along with £446K in development costs to give a free cash flow of £1.7M. Some £461K went on dividends and £110K was used to pay finance leases to give a cash flow of £1.2M for the first half of the year and a cash level of £5.4M at the period-end.

Overall trading was in line with expectations. In the Asset Protection division, revenue declined from £7.8M to £7.6M. Safetell revenue was 3% lower than in the first half of last year as a result of a reduced contribution from time delay cash handing equipment to the Post Office and the completion of some major customer refurbishment programmes. Revenues from the CSI and Service divisions, however, increased by 17.4% and 21.7% respectively.

Excluding CSI product division revenue was 13.9% lower than last time. Revenue from Eclipse Rising was 35.3% lower as a result of reduced spending by one long standing financial institution client on its branch refurbishment programme. There was increased spending by another long standing financial institution customer, however, who decided to reinstall Eclipse Rising screens after their new screenless counter approach resulted in a spate or robberies. Cash handling revenue was 5.3% lower as a result of a decline in orders from the Post Office for time delay cash handling equipment as the programme enters its fourth year.

CSI division revenue increased by 17.4% as a result of increased sales from Gunnebo, which continued to promote and market CSI products after the division’s sale to Safetell in 2013. The group invoiced £307K in the period for 25 Ballistic Doors for a hotel in Iraq as part of their marketing efforts to promote their ballistic and blast resistant products in the Middle East.

During the period, Service division revenue increased by 21.7% compared to the same period last year. This was attributable to the various Eclipse Rising Screen upgrade programmes. Upgrading Eclipse Rising Screen control systems and pneumatic upgrades to the screens are expected to form a core revenue stream for the future and the service division has recently signed a contract with a top five building society to support the screens for a further three years, worth nearly £500K over that period.

In the Electronic Division, revenue fell from £4.1M to £3.6M. Revenue from workforce management in the UK based operation decreased by 27% compared to the prior year as previous major projects with a blue chip retailer and a supermarket chain reached their conclusion. As one of the world’s largest retailers, one of these customers has the potential to generate significant further revenues in the future as they look to continue integration of Grosvenor’s next-gen VFM solutions to help improve their business processes and increase efficiencies.

During the period, Grosvenor Technology secured a contract with a major global WFM partner for the development, manufacture and supply of one of the group’s next generation terminals. The development costs, partly funded by the partner, include incentives for completion of the development work and availability of the terminal in late 2016. The contract is for a period of ten years with guaranteed revenues of $6M over the first five years. The partner has exclusivity for the terminal for a period of six months from the launch of the terminal with the exception of one existing major customer.

Sales of SATEON Access Control increased by 44% following the restructuring of the sales team and expansion of the range. The product range is now ultimately scalable from entry level to enterprise level on a single platform and this proposition has proved attractive to system integrators looking to consolidate product lines, and it end users seeking seamless expansion to existing AC systems.

During the period SATEON version 2.9 was released which included integration into Salto’s wireless lock, adding to the integration already offered by Assa Abloy’s Aperio locks and further strengthening the company’s offering in the wireless locking markets. This version also included innovations such as a refined personal hub for easier user management, improved search facilities and support for Microsoft Windows 10. SATEON Faces was also incorporated into version 2.9 which enhances security by employing photo verification at the point of entry to a building, preventing the use of a lost or stolen credential.

Sales of JANUS AC declined 18% compared to the corresponding period last year due to a combination of adoptions of newer technologies and the transition of long-standing customers to SATEON. The group remain committed to supporting new and existing JANUS projects and it is expected that the product line will continue to be available as long as market demand remains.

In the Middle East a healthy sales pipeline is seen through a major systems integrator in the region with whom the group has reached an agreement to promote the SATEON range. Business development continues both in the Middle East and the US where it is expected that sales will increase in forthcoming period, as typical project gestation periods tend to be a year to a year and a half. Trading with US WFM partners decreased by 9% compared to the corresponding previous period and additional resources are planned to be deployed in this region to support and take further advantage of this large market. Grosvenor’s Hong Kong office was opened during the period, with staff based both in Hong Kong and China beginning business development in the region.

Going forward, profit for the year is forecast to be in line with market expectations. Group profits for the current year were expected to be lower than in the previous year with new market and product development, including the opening of the new office in Hong Kong, the benefits of which are expected to be seen in the future.

No interim dividend is proposed, as with last year so the dividend yield remains 3.3% for the year and the forward PE ratio stands at 13.6 at the current share price.

Overall then this was a fairly difficult period for the group, but one that was predicted with trading in line with expectations. Profits were down, but net assets were up and operating cash flow was flat, although this was due to a cash inflow from working capital and cash profits were down but nonetheless, plenty of free cash was still generated.

Profits in both the asset protection and electronics divisions fell with the decline in the former due to the well-publicised slow-down in the Post office contract and one financial institution client spending less on refurbishments, although the decision by one client to re-install the group’s products after a spate of robberies is a good sign. In the electronics division, the problem was with a reduction in workforce management sales due to two major projects coming to an end. Here the new terminal development sounds like a promising development.

Trading for the full year is expected to be as predicted so the investment case here really hinges on whether the actions and developments taking place this year can boost sales in the coming years to the degree that is expected. If so, a forward PE of 13.6 and dividend yield of 3.3% seems like a fairly decent entry point. I am considering a purchase here but it is not without its risks.

On the 19th May the group released a trading update covering 2016. The group’s financial performance in the second half of the year was broadly similar to that of the first half with revenues expected to be at least £22M and profit in line with market expectations at around £1.2M.

The strategy in the Middle East is proving successful with increasing traction bring gained in the region with the recent signing of Abu Dhabi National Oil Company as a client. Beyond the Middle East, Grosvenor has also achieved a number of new client wins including the Bank of Tokyo Mitsubishi and the Royal Albert Hall.

Three major product developments from Grosvenor include a combined hardware and software access control range in addition to a completely new workforce management terminal built on the Android platform. The business has also announced an opportunity to upgrade existing customers from its JANUS to its Sateon platforms.

Sateon’s new advanced range will provide customers with a seamless access control solution. It combines hardware and software in one package, and helps deliver low energy environments. Customer benefits include easier installation, enhanced reliability, lower cost per door and future proofing along with quicker installation times. The group are expecting to launch this new product this summer.

The workforce management business is launching its first Android based terminal. The new terminals will enable customers to expand their use of work force management by providing staff training and work scheduling with advanced end user features like delegating holiday booking to staff and central management of an organisation’s entire terminal estate. The system also offers biometric fingerprint readers.

Overall then, this is a decent enough update and I think the shares are looking rather cheap at the moment.

On the 6th July the group announced that trading conditions had become increasingly difficult and that the budgeted operating profit for the year is expected to be significantly lower than expected, although they will maintain the dividend.

During the year there was a clear divergence of revenue between the JANUS and SATEON product lines. Sales of JANUS declined more quickly than anticipated due in part to the retirement of older Microsoft platforms. SATEON revenues increased significantly overall, although revenue from the mid-tier customers has not grown as quickly as expected. The overall increase in SATEON sales has been partly attributable to the adoption of the product by new clients, but also to the migration of existing clients from JANUS.

Also a new sales office was opened in Hong Kong last year and the staff were hired locally to support sales in the Asia Pacific region. Whilst the pipeline of opportunities in these countries has grown, meaningful revenues are yet to be generated. Sales in the US have also not matched expectations.

Owing to a decline in sales of the legacy RS series of products and a slowdown of the rollout across the estate of a large apparel retailer, revenues in the UK Workforce Management business softened during the year. In addition, sales in support of a workforce management contract worth $6M over five years have been deferred due to the customer experiencing internal resource constraints. This will delay the delivery of the planned rollout and means that Grosvenor Technology will, in the short term, bare an increased proportion of the cost of developing its next generation workforce management product portfolio.

The revenue stream within the asset protection division during the last few years has included substantial sales of cash handling equipment to the Post Office as part of their network transformation programme. As previously announced, this revenue stream was expected to reduce during the year. The group have been seeking to replace this revenue stream by broadening their product range and have just been appointed as UK distributor of an industry leading manufacturer’s doors and partitions range. Safetell has also been expanding its market presence in new geographies, particularly in the Middle East following the large sales of ballistic doors in the first half of 2016.

Overall then, this is a pretty dire profit warning and I am steering clear until it can be seen whether the group can improve going forward.