Gemfields has now released its interim results for the year ending 2016.

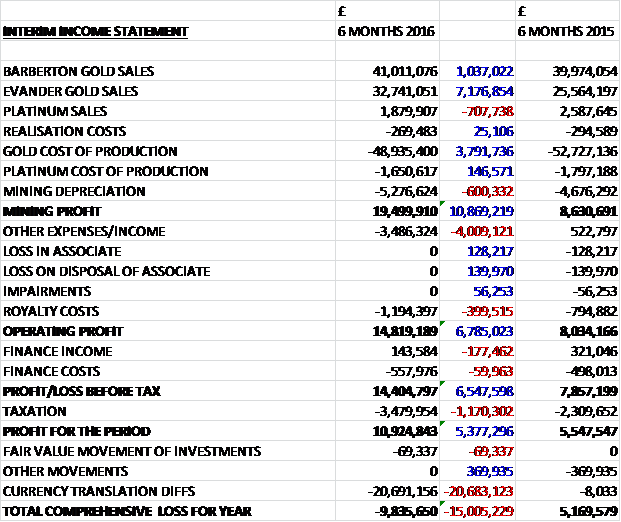

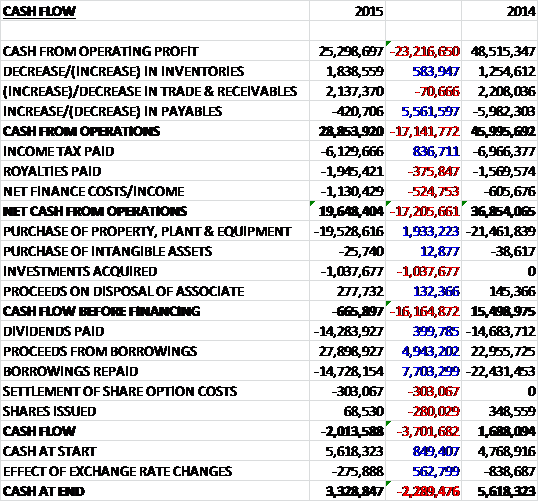

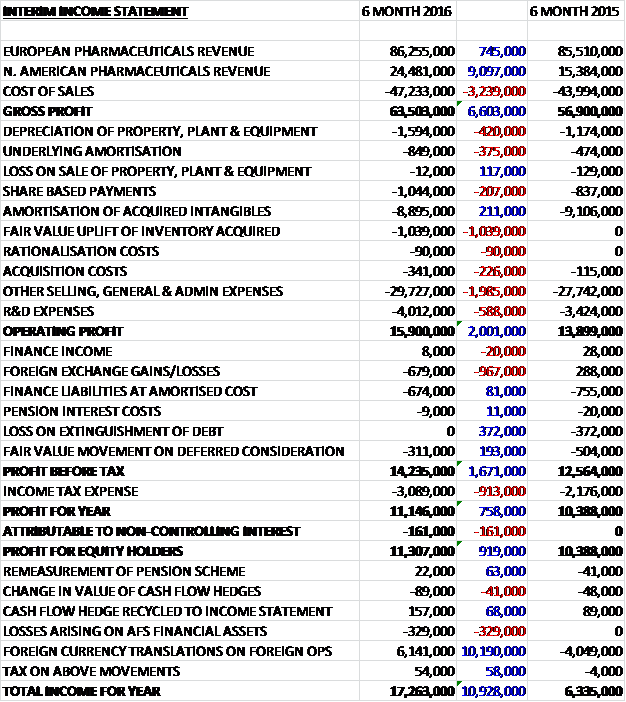

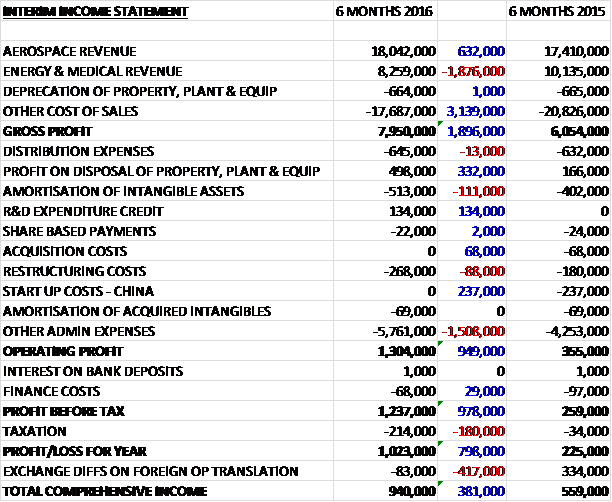

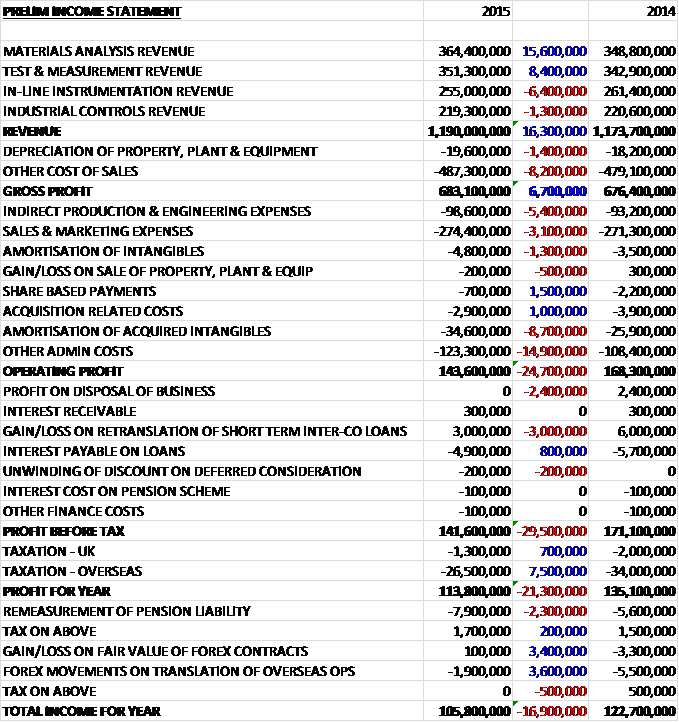

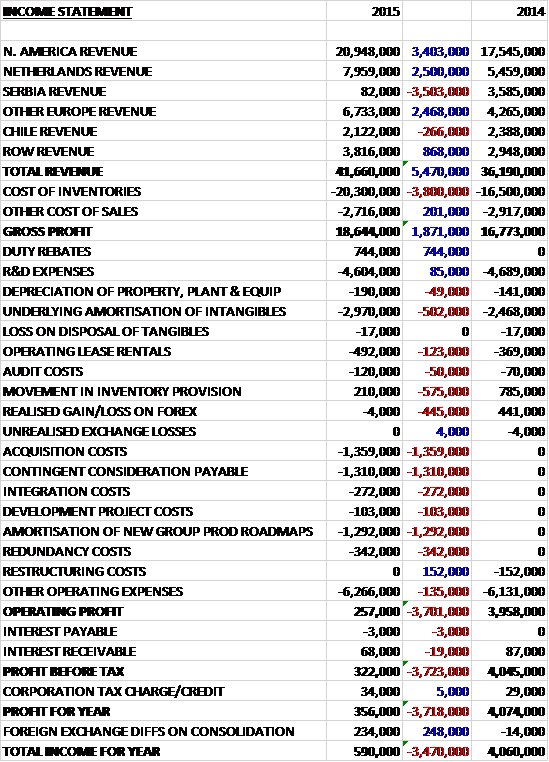

Revenues declined by $9.4M when compared to the first half of last year. We also see an increase in costs as a $1.9M decline in depreciation & amortisation, a $749K fall in mineral royalties and a $735M decrease in fuels costs were more than offset by a $1.4M growth in labour costs, a $1.2M increase in security costs, a $764K growth in repairs & maintenance and a $1.2M increase in other mining and processing costs. We also see a $10.2M adverse change in inventory and purchases to give a gross profit some $21.4M below that of the first half of 2015. Rent & rates were up $999K and professional services increased by $745K which drove the operating profit down by $24.3M. The group did benefit from over $3M of positive exchange differences and a $6.7M reduction in income tax costs, however, which meant that the profit for the half year came in at just $3.4M, a decline of $12.8M year on year.

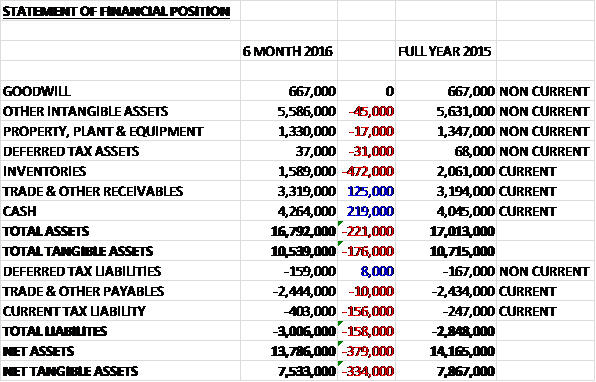

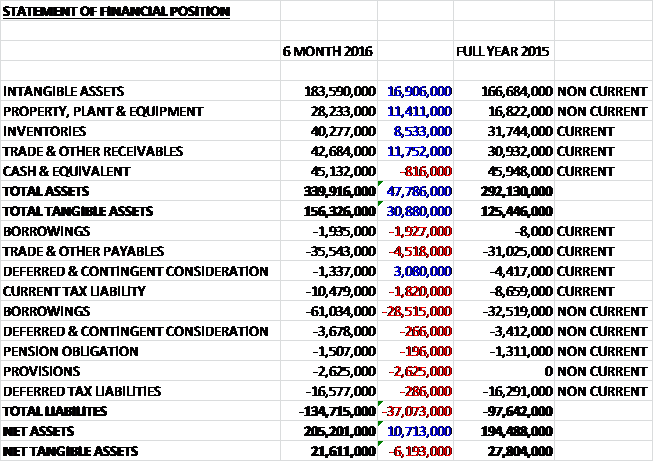

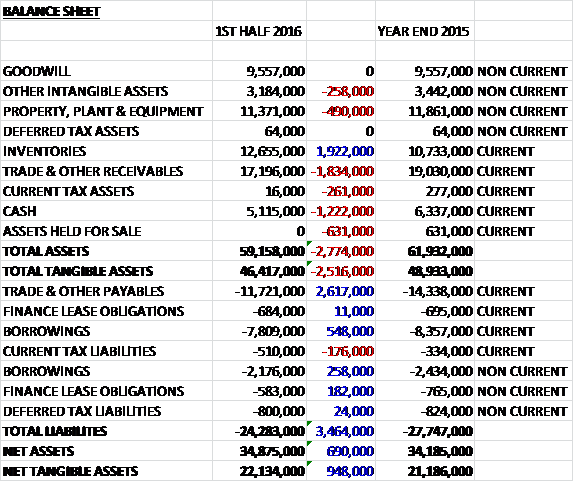

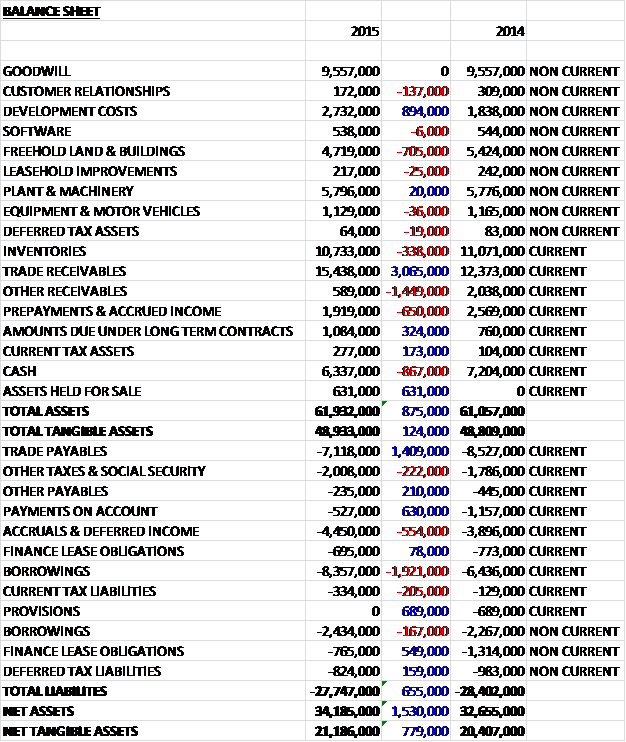

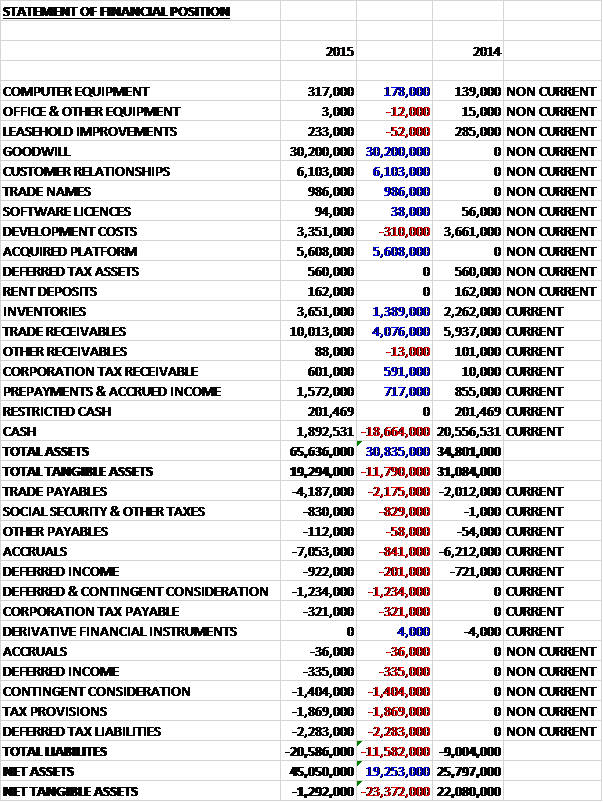

When compared to the end point of last year, total assets increased by $5.4M, driven by a $7.8M growth in receivables, a $4.8M increase in the Faberge inventory, a $2M growth in freehold land & buildings, and a $1M increase in gemstone inventory, partially offset by a $3.1M reduction in cash, a $2.8M fall in the value of evaluated mining properties, a $2.5M decrease in deferred stripping costs and a $2.4M decline in plant, machinery & vehicles. Total liabilities declined during the year as a $10M growth in borrowings was more than offset by a $6.4M decrease in payables, a $2.1M fall in deferred tax liabilities and a $1.9M decline in current tax payables. The end result is a net tangible asset level of $259.7M, a growth of $5.4M year on year.

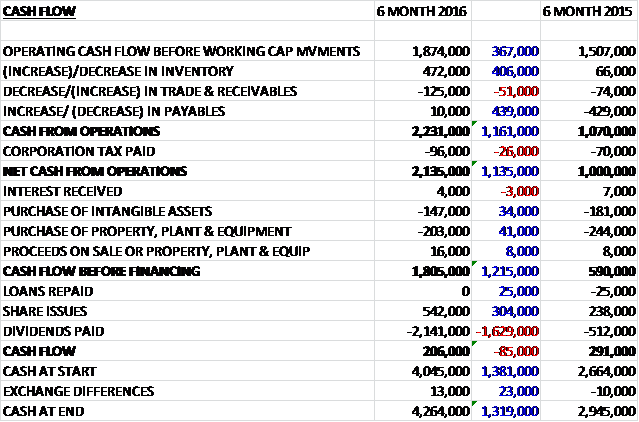

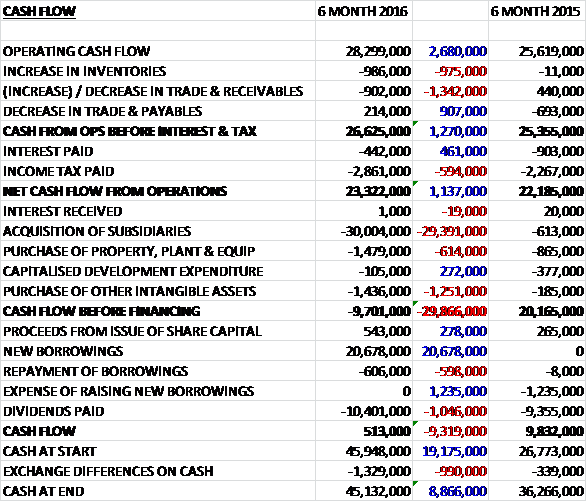

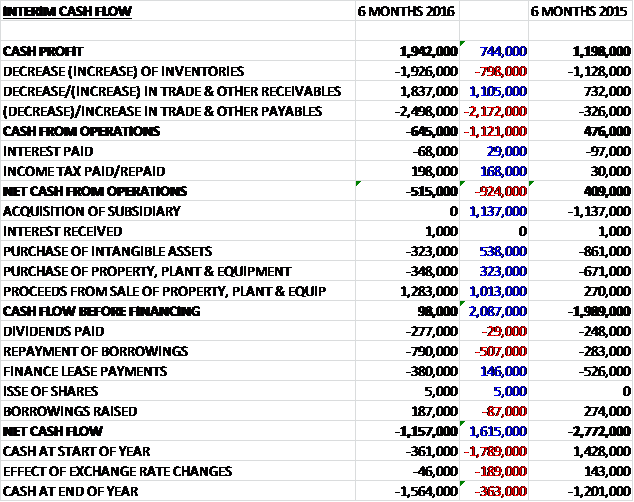

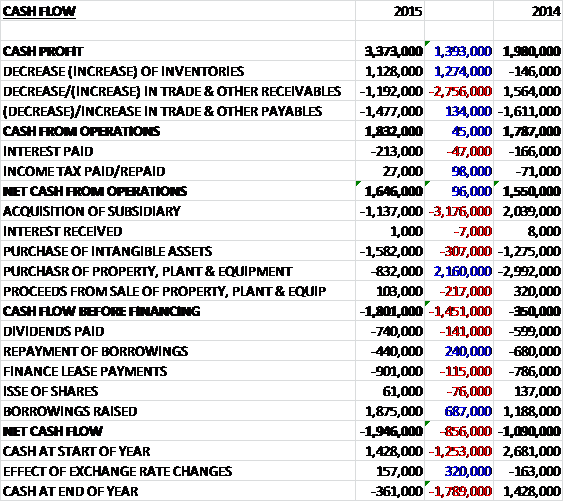

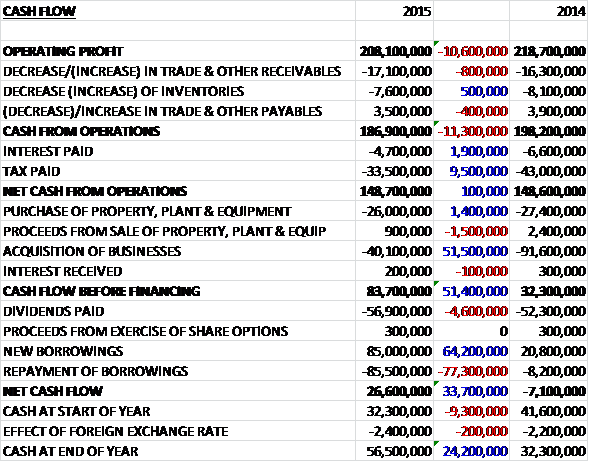

Before movements in working capital, cash profits declined by $24.2M. There was also a large cash outflow through working capital with a $20.1M growth in receivables, to give a net cash from operations of $8.1M, a collapse of $27M year on year. The group then spent $6.8M on property, plant & equipment along with $6.7M on stripping costs to give a cash outflow of $5.7M before finances. We then see $5.5M of dividends paid to non-controlling interests and a net $10M of new borrowings to give a cash outflow of $1.5M for the period and a $24.9M cash level at the end of the half.

The coloured gemstone market continued to expand throughout the period with demand for the more commercial medium to lower quality gemstones being particularly strong. This is indicative of a resurgence within the US consumer market. There is also evidence of the resurgence of coloured gemstones within the luxury sector and the inherent potential for added value drivers.

Production at Kagem was up 30% to 15.7M carats of emerald when compared to the same period of last year. This increase in production is due to an increase in the average grade of ore being mined and the continued increase in available ore reserves as a result of the earlier waste stripping projects and the ongoing improvements in mining efficiencies.

The fourth high wall pushback was completed in September leaving about 15 months of exposed ore available for mining. Continued waste stripping of the Chama pit will be done by the in-house team, which will provide for about two to three years of ore available for mining at any given point in time. Increasing the overall strike length at the Chama pit operation and optimising the blasting and scheduling techniques assisted in further improving the mining efficiency and productivity. The operations yielded 15.7M carats during the period at a grade of 254 carats per tonne compared to 12.1M carats at a grade of 202 carats per tonne in the first half of last year.

The total operating costs were $22.4M while the cost per carat decreased by 21% to $1.43 per carat reflecting the increase in production while overall costs were largely maintained at the same level. Cash rock handling unit costs were $2.38 per tonne, down from $2.92 per tonne, with the reduced costs of mining operations being a result of improved operating efficiencies, lower fuel prices and the short term positive impact of forex fluctuations.

In September the group published its updated CJORC resource and ore reserves statement for the mine with measured, indicated and inferred mineral resource of 1.8BN carats at an in-situ grade of 281 carats per tonne and proven and probable ore reserves of 1.1BN carats at an ore grade of 291 carats per tonne. The projected life of mine is 25 years with projected undiscounted real cash flow over its life of about $1.59BN. The independent technical economic model shows a post-tax net present value of $520M based on a 10% base case discount rate.

Kagem increased its processing efficiencies and capacity following an upgrade and extension to the existing washing plant and the installation of upgraded digital security and surveillance infrastructure. A better climate-controlled environment has been established with the enclosed picking facility, resulting in an improved working environment and more rigorous operating controls. These improvements have further contributed to the efficiency drives which are being implemented at the mine with fewer breakdowns, reduced maintenance costs, improved gemstone recoveries and enhanced overall security.

Diamond core drilling continued in the Chama pit area, establishing depth continuity of the TMS up to a vertical depth of 350 metres. In the Fibolele sector, drilling resulted in the proving of steeper dipping TMS of an average drilled thickness of 25 metres. The Fibolele pit has emerged as a potentially significant production target and is presently in active operation over a strike length of 600 metres. During the period, additional production contacts were also delineated. The prime production points continued to yield good volumes, producing 2.2M carats with an average grade of 191 carats per tonne. At one of the important prospects within the Libwente sector, two bulk sampling programmes continued to test the prospective ground and a total of 56,850 crats of emerald was produced by the pit during the period.

Two auctions of rough emeralds were held during the period. In September, an auction of higher quality stones was held in Singapore, generating revenues of $34.7M at a price of $58.42 per carat. An auction of lower quality emeralds was held in November in India, generating revenues of $19.2M at a price of $4.32 per carat, which is a new record for the lower quality stones. Two further auctions of emeralds are planned for the second half of the year.

In August, Kagem entered into a $10M revolving credit facility with Barclays, supplementing an existing $20M facility, bringing the total with Barclays to $30M. Funds drawn under the facility bear interest at a rate of US LIBOR plus 4.5%. The mine also entered into a $10M short term financing facility with Pallinghurst Resources. This facility had a maturity date of 15th December and was repaid during the month. The mine therefore has an outstanding debt balance of $30M.

At Montepuez, 2.1M carats of ruby were produced compared to 6.3M last time. This variance is due to the deliberate decision to focus on lower grade, but significantly higher quality, alluvial areas in the short term which will be supplemented by a planned shift to some of the already exposed higher grade, lower value areas in the coming months.

The bulk sampling programme at Montepuez continues to increase in scale and has delivered encouraging results. During the period, bulk sampling activities have focussed primarily on alluvial deposits in Maninge Nice and Mugloto blocks, located about 9km apart. The data from the drilling provides an indication of the significant possibility to further increase the resource base.

Rock handling capacity has increased from 310,000 tonnes per month last time to 360,000 tonnes per month during the period and total rock handling during the period was 2.2M tonnes, made up of 300K tonnes of ore and 1.9M tonnes of waste.

During the period higher quality and higher value but lower grade secondary ore deposits were mined and processed. About 144,000 tonnes of ore was processed by the washing plant producing a total of 2.1M carats of ruby compared to 171,000 tonnes of ore producing 6.3M carats in the same period last year with an average grade of 15 carats per tonne compared to 37 carats per tonne. This resulted in a 341% increase in the overall volume of higher quality rubies. Total cash operating costs increased $3M to $13M which meant that unit costs increased from $1.59 per carat to $6.19 per carat. Total capex at the mine was $5.1M with much of this being spent on improved washing plant and camp site facilities.

The second phase of the exploration programme has been carried out in and around the Maninge Nice area up to the eastern boundary of the concession involving both diamond core drilling and auger drilling through a combination of the in-house team and a third party contractor. The second phase of the auger drilling programme took place between April and December. A total of 2,026 holes were drilled and in addition a total of 76 diamond core drills were also drilled.

The auger exploration programme has delineated additional new areas of potential with a gravel bed thickness of more than one metre but these are yet to be confirmed by bulk sampling. In addition to this, some added areas of mineralised amphibolite have also been identified with the available data suggesting that the amphibolite bodies hosting the primary ruby mineralisation are oriented in an East-West direction and occur intermittently across the area. Further exploration by diamond core drilling is currently in progress.

Further diamond core drilling has also been planned to support a better understanding of the disposition of the primary mineralised zone located on the east of the Maninge Nice area. Phase three of the exploration programme will be aimed at tracing the extent of the primary ruby mineralisation within the amphibolite body while auger drilling will continue to spearhead the exploration programme to expose further greenfield areas within the license. The airborne geophysical study, covering an area of 14,560 square kilometres, has been completed during the period and results are expected to be finalised during Q1 2016.

A more durable poly panel deck screen has been installed at the wash plant, replacing the wire mesh double deck screen during the period which has enhanced the screening efficiency of the washing plant. In addition, to the conversion of dry to wet screening on the M1700 rinser, a fines master has been installed in circuit with a view to further improving overall processing and water recovery efficiencies. A new replacement log washer, with two additional dewatering screens has also been installed, with further upgrades to the plant currently underway.

To support the need for a consistent supply of clean water to the wash plant throughout the year, six additional bore wells were drilled and commissioned with higher capacity water pumps. An additional water reservoir of about 25,000 cubic metres capacity was also created in order to increase the currently available water storage capacity. The installation of a water treatment plant and dense media separation plant to replace the existing jigs is under review.

One auction of higher and medium quality rubies was held during the period which generated $28.8M, yielding an average overall value of $317.92 per carat. It is likely to take a few more years before the ruby market has access to similar levels of working capital and distribution as the emerald market but at least one auction of mixed quality ruby is expected to take place before the end of the year.

The construction of the new camp at the mine started in March 2015 with a total of 102 housing units, a recreation unit, canteen and new kitchen being built. The first set of housing units have been commissioned and allotted and completion of the project is targeted for the end of April. A new fuel storage tank with a capacity of 50,000 litres has been constructed, increasing the total storage capacity on site to 96,000 litres. It is planned to extend the existing workshop during the coming year and additional facilities such as a training room, wash-bay, scrapyard, lubricant storage and heavy earth moving machinery maintenance bays will also be constructed.

The restriction of illegal mining activity and asset loss continue to be key challenges. With the implementation of new infrastructure and improved technological interventions such as the enhancement of radio communication ranges, mobile camera lighting towers, increased numbers of CCTV cameras and mobile guard posts, however, a meaningful improvement has been noticed during the period. A dedicated training programme for security personnel incorporating human rights and soft skill development has been provided to all key personnel during the period.

At Faberge, the value of realised sales during the period increased by 70% when compared with the same period last year and losses reduced by 21%, which is progress. The total number of Faberge distribution channels increased from 20 to 25 during the period. The business’ first significant print advertising campaign since Christmas 2013 began in September and will continue through to June, focusing on timepiece collections and the “Lady Compliquee Peacock” won the ladies high mechanical category at the 2015 Grand Prix d’Horlogerie de Geneve.

At Kariba Minerals in Zambia the Curlew North, Francis West and Main Curlew pits have been actively developed and mined during the period and a new exploration programme is to be put in place to confirm the mineral resources available at the mine. Production of amethyst during the period was 485 tonnes compared to 574 tonnes last time with the grade remaining at 49kg of amethyst per tonne of ore. A total of 10.1M carats of higher quality amethyst was sold in Singapore in September for $440K with the next auction taking place in March.

Kariba is working towards a long-term cost effective solution for energy supply and has initiated an environmental project brief for a 1MW solar farm in conjunction with an Australian solar supplier and the Zambian national energy company. The project aims to supply the mine with more cost effective electricity and to offer excess capacity to the local community at a rate that will be subsidised by the government. The group will lease a portion of its land to the project in order to accommodate the solar plant and the Australian company will fund construction with Kariba signing an off-take agreement to purchase electricity. The CCTV coverage system at this mine has been extended to 25 cameras to improve security.

In Ethiopia, exploration work began in July with a preliminary ground survey, detailed mapping and the preparation of base line plans. A manual trenching exercise has been completed on a key target area within the northern part of the license, named Dogogo Hill, selected on the basis of geological indicators and artisanal activity. The block measures 1.92 square Km, covering a strike length of 2.4Km. Eight trenches were planned at 100m intervals and excavation of these trenches was completed in November. They exposed contacts between pegmatites and talcose schists, and the occurrence of beryl has been recorded. A pitting exercise has been initiated at these contact zones.

A detailed geological mapping exercise has been completed concurrently in another block to the south of the license called Karolo Kora Hill. This block measures 13.75 square km and covers a 5.5km strike length of the ultramafic belt. Steps have been started to commission a diamond core drilling programme of the license area to establish dip continuity of the ore body identified during trenching, and is expected to start in early 2016. An airborne geophysical survey of the license area is also planned for later in the year.

In Sri Lanka the group received the necessary license to trade sapphires, completed the establishment of the required infrastructure and acquired the supporting equipment for trading in Colombo and Ratnapura. The appointment of key management personnel has also been completed and the associated supply chain mechanisms are being developed.

The group have a production target for 2016 of 25 to 30M carats for emeralds and 8M carats for rubies. The reduction in profits are apparently mostly attributable to a more equally planned auction mix between the first and second halves of the year when compared to last year when a significant part of the revenue was achieved in the first half.

During the period the group made two acquisitions in Colombia. The first project relates to the acquisition of a 70% stake in the Coscuez Emerald mine in the Boyaca province for a total consideration of $15M to be paid in tranches of a combination of cash and Gemfield shares conditional on achieving certain pre-determined milestones. The license area covers an area of 47 hectares with the mine having been in operation for over 25 years and known to have produced some fine emeralds. Exploration and mine planning activities such as drone surface topographic survey, and preliminary assessment of engineering solutions were initiated as part of the ground preparations for future operations. Further exploration activity will be carried out over the next 18 to 24 months to support the development of an expanded geological model and preliminary mine plan.

The second project relates to selected exploration prospects held by ISAM Europa via the acquisition of 75% and 70% interests in two Colombian companies holding rights in respect of mining license applications and assigned concession contracts respectively. It comprises a number of new license applications and assignments to existing concession contracts administered by the Colombian Mining Agency. Eight of the applications and assignments have been approved and issued with the remaining assignments and applications are being reviewed by the Colombian Mining Agency. The total consideration payable is $7.5M to be paid in tranches of a combination of cash and shares conditional to achieving certain milestones.

Overall then this has been a mixed period for the group. Profits were down as revenues fell and costs increased and although net assets did grow, the operating cash flow fell and there was no free cash generated. Although the coloured gemstone market is apparently strong, these results are affected by a more equal spacing of gemstone auctions with last year being first-half weighted.

The Kagem mine seems to be performing well with an increase in production due to earlier waste stripping projects and higher grade ore. The cost per carat declined due to operational gearing, forex benefits and lower fuel prices. The prices for low-quality emeralds held up well with some more softness at the higher quality end. The performance at Montepuez was more mixed. Production fell as the group concentrated temporarily on lower grade high quality areas and there was only one auction during the year.

The losses at Faberge do seem to be reducing, however, and in the second half, the production of rubies is expected to increase considerably as the mine moves to higher grade areas but it looks like the production at Kagem is expected to reduce slightly. I have to say, the lack of any cash generation is starting to concern me slightly and I don’t see anything in this update to really make me want to buy back in so I am keeping a watching brief currently.

On the 4th April the group announced the results of its auction of higher quality emeralds and amethyst which was held in Zambia. The emerald auction saw 558K carats of higher quality stones placed on offer with 470K carats being sold generating revenues of $33.1M at an average value of $70.68 per carat which was a new record for this type of auction.

The amethyst auction saw 9.4M carats of higher quality stones placed on offer with 6.6M carats being sold which generated revenues of $220K realising an average value of 3.26c per carat.

These prices look very good to me, although it should be noted that a fair amount of the gems remained unsold. I suppose the next ruby auction will be the real barometer with regards how the group is doing.

On the 4th May the group released an update covering trading in Q3. At Kagem, the group produced 23,900 tonnes of ore at a grade of 297 carats per tonne, producing 7.1M carats of emeralds. This compared to 30,100 tonnes at 272 carats per tonne producing 8.2M carats in Q2 and 27,900 tonnes at 355 carats per tonne, producing 9.9M carats in Q3 last year with the differences being attributed to the fluid nature of the mineralisation and a higher-grade zone having been encountered last year. Capex on property, plant and equipment was $2.6M and the spend on waste stripping was $1.2M. The gemstone unit cost was $1.45 per carat compared to $1.38 in Q2 and 99c in Q3 last year.

Waste stripping and ore mining of the Chama pit continued to be advanced. Total rock handling during the quarter was 2.6MT and increasing the strike length at the pit along with optimising production scheduling assisted in improving productivity. Exploration and bulk sampling activities at the Fibolele and Libwente sectors are progressing well and continue to indicate promising results. The mine has also increased its processing efficiency and capacity with commissioning of an upgrade and extension to the existing wash plant facility during the previous quarter. This is further supplemented by the installation of digital security and surveillance technology across the production infrastructure.

The April auction of higher quality emeralds held in Zambia saw 470K carats being sold, representing 84% of the total weight offered and generated revenues of $33.1M. The auction yielded an overall average value of $70.68 per carat which is a record average price achieved to date for this type of auction.

At Montepuez the group processed 67,600 tonnes of ore at a grade of 30 carats per tonne, generating 2M carats of gemstones. This compared with 71,700 tonnes at a grade of 22 carats per tonne generating 1.6M carats in Q2, and 78,600 tonnes at a grade of 18 carats per tonne generating 1.4M carats in Q3 2015. The total capex in the quarter came in at $1.6M and the unit cost per carat was $2.40, comparing favourably to the $3.31 in Q2 and $2.64 in Q3 last year.

The reduction in throughput at the processing plant was a result of delayed, unseasonably high rainfalls making the head feed difficult to process which was compensated for by a shift in focus on processing higher grade, lower value amphibolite ore.

The construction of the new camp is proceeding to plan and on track for completion by the end of June. An extensive security plan has been formulated to combat continuing asset loss at the mine and a training programme for security personnel incorporating human rights development has been provided.

Faberge saw a 26% fall in sales orders during the quarter largely due to the sale of the high value pearl egg in February 2015, boosting that period’s results, along with the timing differences on sales orders arising from the Baselworld fair. Total operating costs increased by 10%, largely due to an increase in advertising spend with the first significant print campaign since 2013 continuing in to 2016.

In Colombia, the group continued with its pre-emptive exploration and mine planning exercises which included topographical survey, mapping of underground tunnels, surface mapping, sampling, chemical analysis, testing of mining equipment and further planning of the underground engineering solutions. A project team has been created to finalise the takeover of admin and legal control of the ISAM portfolio and the group carried out field visits and preliminary geological activities in selected licenses.

In Sri Lanka the group has initiated early stage market evaluation and the appraisal of suitable partners for the supply of gemstones. They will continue its evaluation of some of the exploration licenses, covering diverse minerals, throughout the remainder of the year.

In Ethiopia, following completion of a trenching exercise within the northern part of the license named Dogogo Hill, exploratory pits have been excavated in potential contact zones that were exposed within the trenches. Samples of Beryl and other indicator minerals were recovered from some of the pits and preliminary ground work, including contractor selection, has been completed with a view to starting exploratory drilling in this block in due course. A detailed geological mapping exercise has been initiated on the Funkoftu block, located to the south of Dogogo. This measures 2.5 square km and covers 2.25km of prospective strike length for emerald mineralisation.

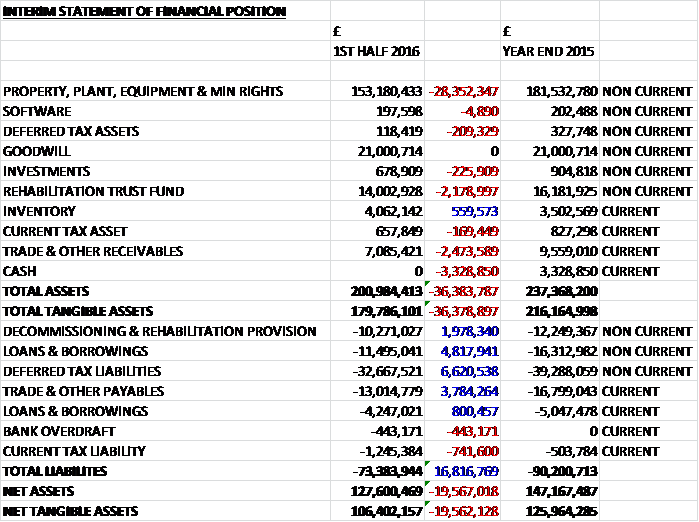

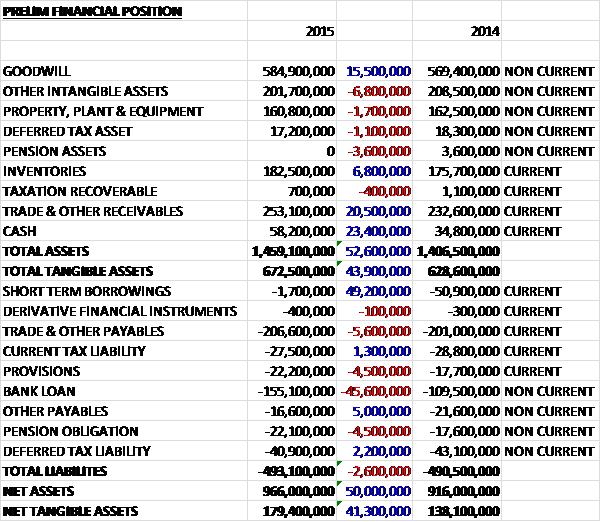

At the period-end, the group had cash of $5.6M with a further $33.1M of auction revenue due shortly. The total debt outstanding was $49M so net debt stood at $10.3M once the auction revenues are taken into account.

Overall then, the results from Kagem were affected by lower grade ore being processed and Montepuez was affected by increased rainfall, although higher grade ore was processed which meant that carats produced increased. The emerald auction seemed to go well and the coloured gemstone market remains robust, supported by improving consumer demand from the US. The Faberge business still seems a long way off breaking even though, and there is not much here really to make me want to buy in again.

On the 17th May the group released a trading update covering Q1 2016. The group had $68.8M cash on hand at the end of the period, excluding the receipts from the third tender, although the $11.7M dividend will be paid in June. Positive actions taken by the major diamond producers have led to an overall steady sentiment in the diamond market during Q1. Although there have been some signs of improvement, the diamond market as a whole remained cautious during the period. The continued slowdown in Chinese retail demand, a strong US dollar and reports of continued high levels of polished inventory have contributed to a cautious approach being adopted in the purchasing of rough and polished diamonds.

At Letseng, the mine treated 1,624,964 tonnes of ore which was 10% below the prior quarter due to seasonal rain impacting access to ore and treatment rates (the ore treated was up 14% year on year). The grade recovered increased by 10% to 1.77cpht, however, so the number of carats recovered stood at 28,698, down by just 1%. During the period, 7.1MT of waste was mined. This is in line with the revised life of mine plan which allows for increased levels of higher grade ore from the Satellite pipe to be mined.

The two plants treated a total of 1.4MT of ore during the period, of which 36% was from the satellite pipe. The balance of the ore was treated through the Alluvial Ventures plant which was sourced from the main pipe and low grade stockpiles. The increase in grade recovered is reflective of the area mined in the Satellite pipe that has historically produced higher than reserve grades, albeit at a slightly smaller average stone size which contributed to a lower average price achieved per carat in the period. The three tenders in the period saw 45,311 carats sold, an increase of 26% year on year but the $1,938 per carat achieved was a 10% decline which meant that the total value sold was $87.8M, a growth of 13%.

At Ghaghoo, the group treated 50,514 tonnes of ore which represented a 41% decline on Q4 but a 4% growth year on year. The grade recovered also fell, down 24% quarter on quarter to 21.8cpht so the carats recovered fell by 55% to 11,029 which represented a 5% decline on Q1 last year. The reduced tonnage is in line with the strategy of downsizing and reducing the production plan for 2016 to about 300KT. The majority of the ore treated was sourced from tunnels one to five on level 1. The area of the pipe mined was close to the contact and contained more internal dilution which led to the lower grade seen.

The development of the second production block is progressing well with over 200 metres of tunnelling completed per month which will allow access to higher grade ore towards the centre of the pipe in the second half of the year. A parcel of 14,114 carats was sold for $2.3M which represents a value of just $160 per carat, although this does represent a 7% increase compated to the previous price achieved in December 2015. Although the mine will operate at a reduced rate during the year, prices for the Ghaghoo production will continue to be monitored and the option of returning it to full production regularly reviewed.

On the 23rd May the group released the results of the lower quality rough emerald auction held in India. Of the 3.67M carats offered, only 2.78M were sold, representing about 76% of the total. This sale brought in $14.3M which represents an average of $5.15 per carat which is a record price, although the overall amount sold was disappointing.

A few of the lots, in which there was a slightly higher degree of uncertainty with respect to final recovery from rough to finished goods did not achieve their reserve price so were held back. The company believes that these goods offer considerable opportunity to further build demand in other areas and is confident in the quality and longer term value of these lots and is supported by evidence of the US market continuing to come back on stream.

On the 20th June the group announced the results of its mixed high and commercial quality rough ruby auction in Singapore. It recorded revenues of $44.3M with an average realised price of $29.21 per carat as a total of 95% of stones were sold. It is difficult to compared to other auctions given the mix of different qualities but apparently the prices achieved were indicative of improved overall global demand.

On the 4th July the group announced details of new debt facilities. This includes a $15M unsecured overdraft with Barclays at an interest rate of LIBOR+4%; a $15M overdraft facility with Banco Commercial De Investimentos with an interest rate of LIBOR+3.75; and a $15M finance leasing facility with BCI at an interest rate of LIBOR+3.75%, all for Montepuez. In addition, they announced a $20M financing facility with Macquarie with an interest rate of LIBOR+4.5%. This loan replaces the $25M debt facility and the proceeds of the new Montepuez loans will enable them to finance their capex requirements at the mine and provide additional working capital.

On the 1st August the group gave a market update covering trading in Q4.

At Kagem, the group produced 7.2M carats of emeralds, a reduction of 900K carats year on year due to the varied nature of mineralisation and a higher grade zone having been encountered during Q4 2015 as the average grade fell from 222 carats per tonne to 185 carats per tonne. Unit operating costs increased from $1.58 to $1.75 per carat, mainly as a result of the lower grade area being mined.

An auction of commercial quality stones held in India generated revenues of $14.3M at an average value of $5.15 per carat, a record average price for commercial emeralds. The amount sold represented 79% of the value being offered compared to 95% at the last commercial emerald auction.

An increase in the strike length at the Chama pit and optimising production scheduling has assisted in further improved mining efficiencies. Exploration and bulk sampling activities at the Fibolele and Libwente sectors are progressing well and continue to deliver promising early stage results.

A GPS based radio controlled fleet monitoring and management system was made fully operational during the quarter. The system improve the real time tracking and allocation of fleet. The utilisation of bulk emulsion explosives has further improved blasting performance and resulted in optimised rock fragmentation leading to less wear and tear of fleet buckets and improved cost of production. Security infrastructure has been further improved by the installation of digital security and surveillance technology across the mine infrastructure.

At Montepuez, the group produced 6.2M carats of ruby, an increase of 5.5M carats year on year, supported by processing of the higher grade but lower value amphibolite resources as the average grade increased from 9 carats per tonne to 75 carats. Unit operating costs reduced from $10 to $1.19 per carat but cash rock handling unit costs increased from $6.13 to $7.14 per tonne as a result of an increase in headcount and fleet size in anticipation of a continued increase in the scale of operations and a reduction of rock handling volumes due to the prolonged rainy season and focus on ore mining rather than waste mining.

During the quarter, the wash plant saw a 10% increase in tonnes processed due to improved production planning and processing availability. The construction of the new camp is proceeding according to plan and will be fully completed by December. In order to facilitate DUAT, a technical team from the government completed a site audit in April and the application is currently being reviewed by the Land Minister’s office and will be presented to the council of Ministers. The comprehensive resettlement action plan has also been completed and submitted and is also being reviewed by the government. Both submissions are expected to be approved by December. Construction of a new security base was started in April and is progressing well.

A mixed quality auction of rubies was held in Singapore which generated revenues of $44.3M at an average value of $29.21 per carat, representing 98% of the value being offered.

At Faberge, the value of sales orders agreed in the quarter increased by 14% and the number of transactions doubled which meant that the average selling price fell by 56% as two significant pieces were sold in Q4 last year. Importantly, operating costs fell by 28% in the quarter. Sales orders agreed during the year as a whole fell by 10% due to no high value objets d’art being sold this year.

In Colombia the group continued with its pre-emptive exploration and mine planning exercises in preparation for completion of the Coscuez transaction and as part of the base level arrangements for future operations. These included rock support testing, hoisting system evaluation as well as waste dump, ventilation systems and wash plant design. The administrative control of the ISAM licenses has been largely transferred to the project team. The group also carried out field visits and prelim geological activities in selected ISAM licenses.

During the period the group conducted several meetings with the Ministry of Mines and the National Mining Agency regarding the completion of the pending issues between Esmeracol and the government. Completion of the transaction was extended by a further three months to September in view of the pending issues which sounds a bit ominous.

In Sri Lanka, necessary geological and geophysical exploration work for diverse minerals has been completed in selected areas across the exploration licenses. Following field assessment, the requisite reports have been submitted to the authorities and the process of license renewal has been completed. Initial steps to set up an in house lab and the implementation of standard operating procedures for gemstone authentification has been completed and the group intends to start trading operations in Q2 2017.

In Ethiopia, an exploratory drilling programme was initiated at the end of June in the Dogogo South lock. The drill targets are based on the inputs from the trenching and exploratory pitting exercise carried out earlier in the year. Further trenching work has been carried out in the North Block. The excavated trenches covered a total length of 2.7km and the average width is 70cm to 80cm with a depth ranging from 60cm to 150cm. Contacts have been exposed between pegmatite and talc mica schist and the occurrence of beryl and mineralised reaction zone has also been recorded.

In June the group launched a global marketing campaign to promotive Mozambique rubies. A series of three short films formed the backbone of the campaign and in just under two weeks one of the films had reached over 550,000 views and the campaign was listed in the top ten brand social videos of Q2 2016 on Luxury Daily.

After the year-end, a $65M financing facility was announced to sustain the expansion plans to increase annual production to about 20M carats of rubies at Montepuez and more than 40M carats of emeralds in Kagem within the next three years.