James Halstead have now released their final results for the year ended 2018.

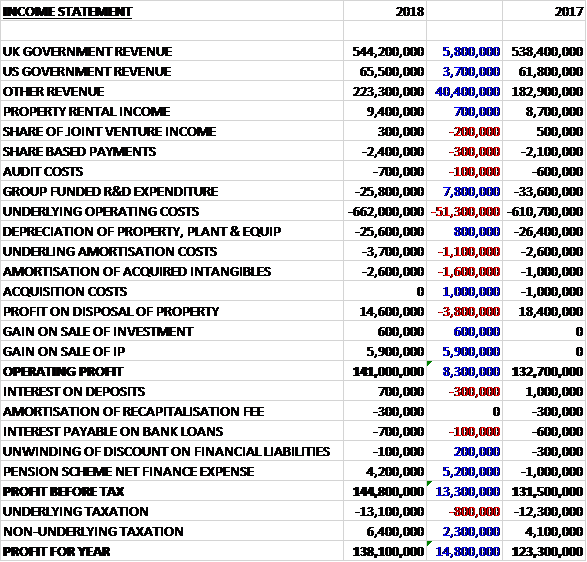

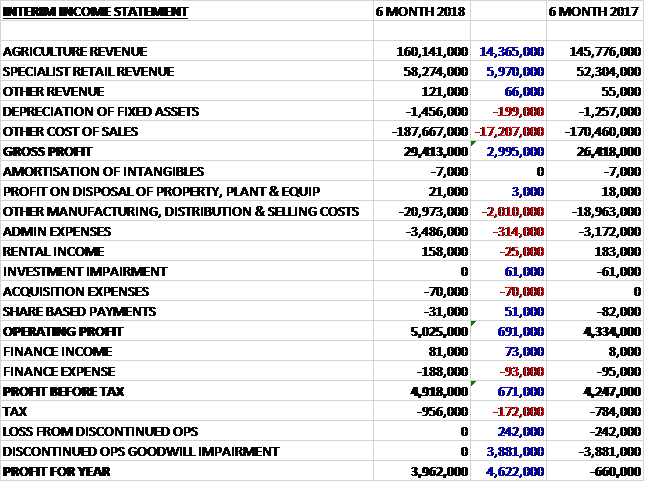

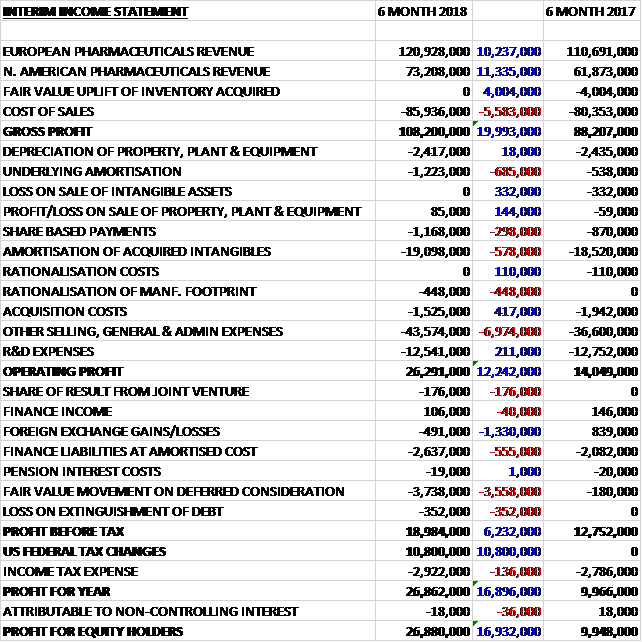

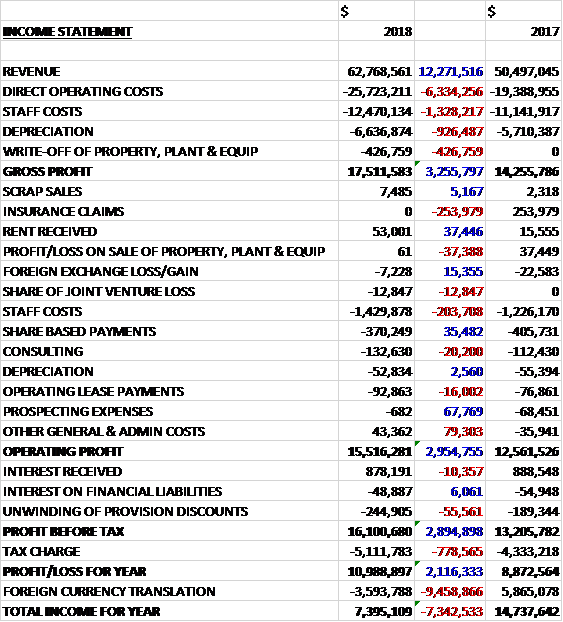

Revenues increased when compared to last year as a £2.1M decline in Asian revenue was more than offset by a £6M growth in European revenue, a £2.4M increase in UK revenue and a £2.3M growth in ROW revenue. Staff costs increased by £1.1M, R&D costs were up £474K and other cost of sales increased by £7.2M to give a gross profit £293K lower than last year. Operating lease rentals increased somewhat, selling and distribution costs were up £291K, depreciation grew by £225K but other admin expenses declined by £832K which meant that the operating profit was £136K lower. The pension interest cost fell by £209K, however, which meant that after tax expenses declined by £112K the profit for the year was £36.7M, a growth of £198K year on year.

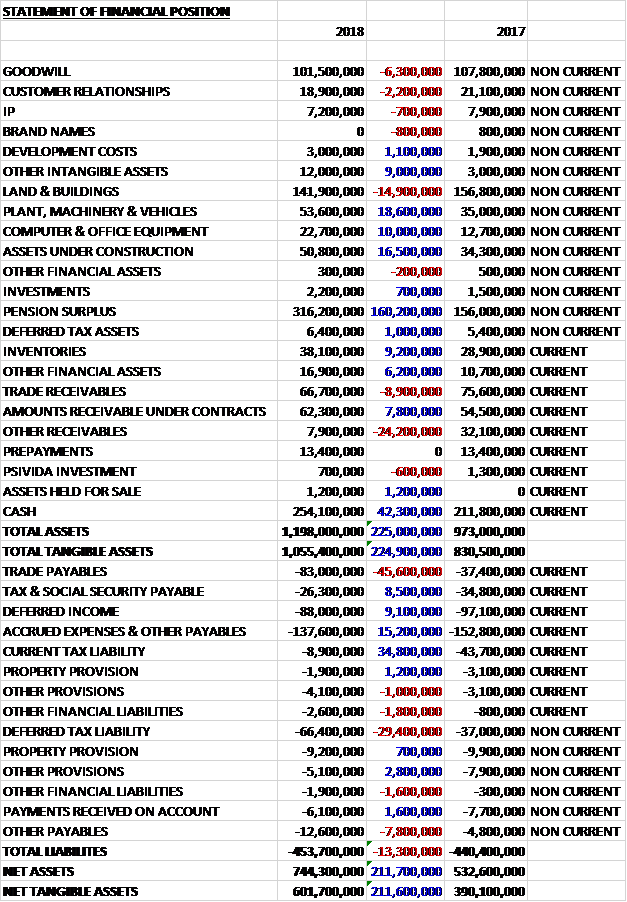

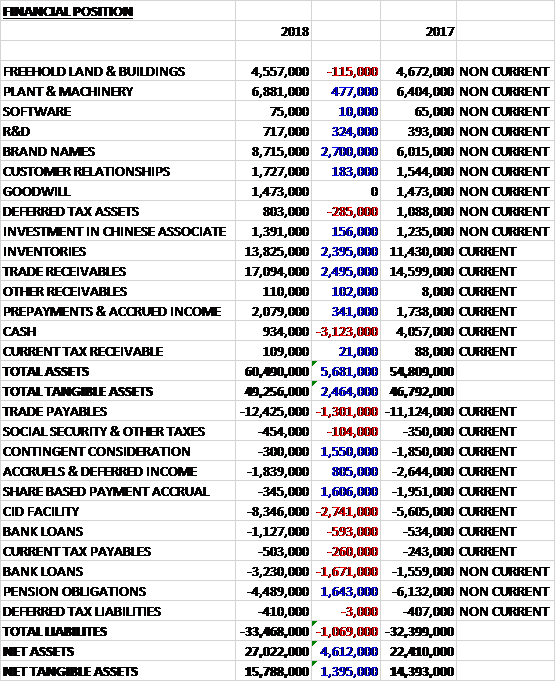

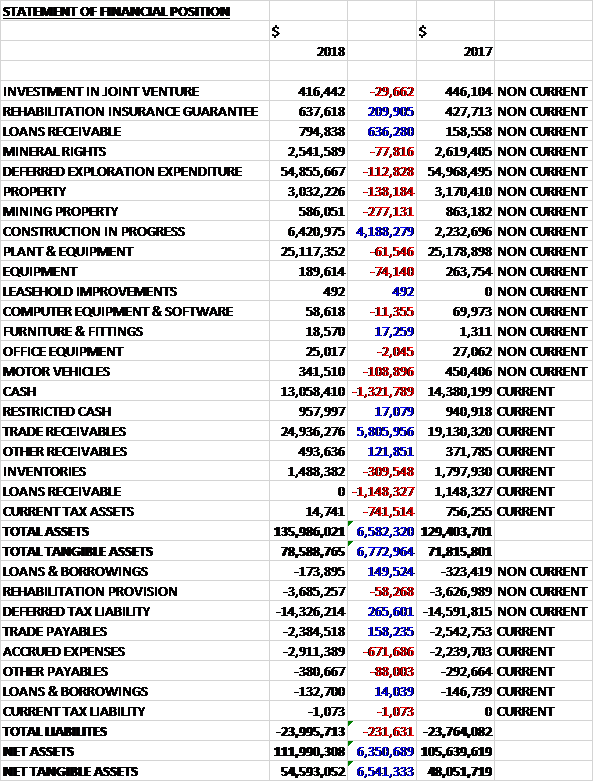

When compared to the end point of last year, total assets decreased by £3.5M driven by a £1.9M decline in cash, a £1.8M fall in inventories and a £1.5M decrease in deferred tax assets, partially offset by a £913K growth in prepayments and accrued income. Total labilities also declined during the year due to an £8.7M decline in trade payables, a £6.4M fall in pension obligations, a £1.7M decrease in accruals and a £1.2M fall in derivative financial liabilities. The end result was a net tangible asset level of £125.6M, a growth of £14.8M year on year.

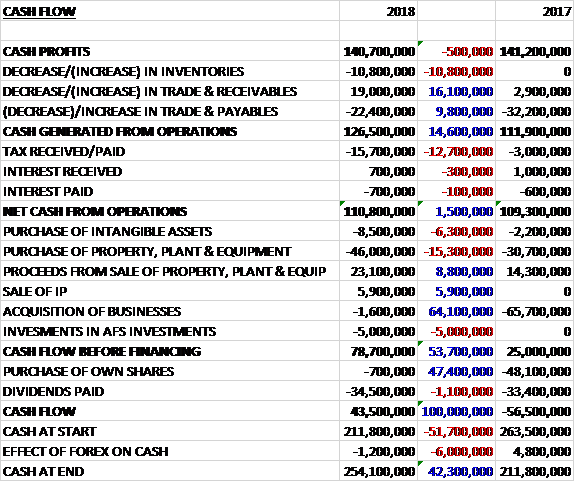

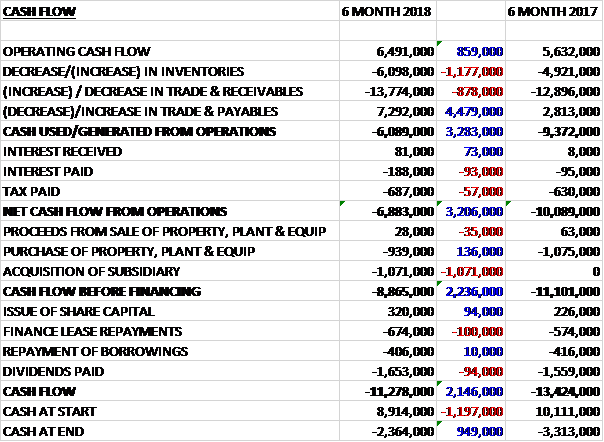

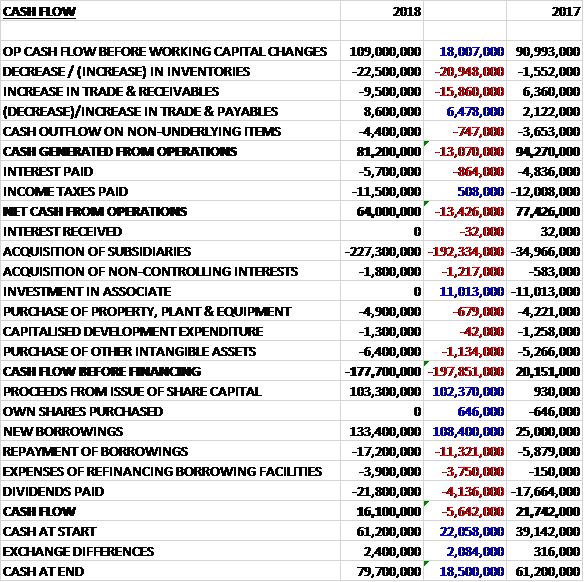

Before movements in working capital, cash profits increased by £685K to £51M. There was a cash outflow from working capital and despite tax payments reducing by £1M the net cash from operations was £28.6M, a decline of £8.3M year on year. The group spent just £3.6M on capex to give a free cash flow of £25.3M. This didn’t quite cover the dividends of £27.2M which meant there was a cash outflow of £1.7M in the year and a cash level of £50.7M at the year-end.

Over the year the group have benefited from exporting products in an environment of a weaker sterling, but against this raw material prices have continued to rise. The adverse raw material price affect from forex movements was £1.8M. This was mitigated somewhat by higher sales prices outside the UK but it did affect profitability within the UK where they took the decision to hold back on price increases. A favourable mix of sales largely offset the bottom line effect of these raw material costs.

The launch in May of Palettone was costly but worthwhile for the longer term. The costs of development trials, sampling, marketing material and related expenditure were around £2M and the product has just been launched into the global market place. The timing was important due to the closure of one of the group’s competitor’s factories.

Within Europe, the Karndean ranges aimed at the wholesale market were launched at the beginning of the year and the Expona Domestic range was launched in January with the Palettone in May. The gestation period for a new launch is generally a number of months so the impact from such major product changes has only been partly felt this year. Sales increased by 2% across the business but profitability was negatively affected by changes in forex rates and price increases from suppliers. All the key markets grew with the exception of Benelux with France in particular showing good growth.

The Australian business had a record year in both terms of turnover and profits. The ongoing projects that the business continues to win and supply include the Howard Soloman Aged Care Facility in Western Australia and the Australian Embassy in Port Moresby. Another installation is the Pier 33 Yacht Club in Queensland. Given that the group are the only manufacturer with warehousing in every state and with the sales reps local to each major city, the business is soundly based for continued growth. During the year they added warehousing in South Australia and this has enhanced their offering with the Angaston, Strathalbyn, Goolwa and Barossa hospitals all examples of penetration in this region.

New Zealand had another year of modest (1%) growth which showed good growth on the North Island offset by contraction on the South Island which continues to be slow. Product mix has had some negative impact on margin locally for bought in products as one key supplier had some supply interruptions and the shortfalls in this product were made up with greater sales of lower margin products. The UK manufactured products continue to have a dominating market share and the New Zealand social housing contract referred to last year continues to be an important component of this.

The group have changed the management structure of the Asian business to align it with the larger Australian business. Plans are in place to extend the footprint of the Hong Kong operation both in China and in other Key Asian markets. The presence of Chinese manufactured products makes many of these markets very price sensitive and the restructuring of this part of the business continues to ensure their response to these market pressures is robust. Projects such as the HPA Electronics Factory in Malaysia, Hamazushi Chain stores across Japan, the Water Market in Macau and Chengdu Woman and Children’s Hospital in China are some of the new installations they have been involved with.

In the UK there was a dearth of large government funded projects as spending cuts are applied across the board. Nevertheless sales into the refurbishment sector remained strong and Polyflor was able to make the most out of a weak market. Their UK sales were 3% ahead of the prior year. New products such as the barefoot safety flooring, Polysafe Quattro and Palletone collection helped sales.

During the year research was undertaken into the development of a totally new format of manufacturing flooring, the results of which are now under board consideration. They plant to acquire a new production plant and their technical teams are working with suppliers on a final specification. To pave the way for this, they have spent many months removing old and surplus equipment to create space for this facility on the Radcliffe site.

In the early part of the year they upgraded the chilling units at the Radcliffe site which reduced energy consumption. Their non-directional sheet vinyl plant was modified with increased automation allowing them to achieve 96% utilisation. Over the coming year this should ensure 25% higher output for the same man-hours. Their high voltage and low voltage equipment was completely revamped which will again reduce downtime and improve quality control. At the same time they installed new LED lighting across the site which improves visibility at a reduced cost and negated the energy cost increases.

Investment at Teesside has continued. They have completed the upgrade to allow in-line register emboss on their sheet as well as upgrading their inspection to an in-line facility. The former offers payback with improved designs and the latter with reduced manpower. In addition they have increased the number of racks in the warehouse at Teesside to give them greater capacity and flexibility in their distribution and have also replaced their chilled water system for cooling rolls on the finishing line.

Notable projects in the year included the new Kellogg HQ in Manchester, the S4C HQ in Carmarthen which used the new Palettone, Adidas UK HQ in Stockport and Alexander McQueen Head Office in London.

The Scandinavian business posted a 6% increase in turnover. Sweden had a record year for sales and profitability along with growth in sales of UK manufactured products. The Norwegian business had a change in management late in the year following the death of the MD. During the year the business was refocussed on the core portfolio of Polyflor vinyl sheet. One highlight was one of the first Palletone specs for Helly Hanson in Oslo. Sales in this business fell back slightly, however, as major projects were keenly contested. Nevertheless projects such as the FlipZone Trampoline park in Bergen and supplying the Swedish government controlled pharmacy Apoteket were examples of their presence.

Turnover in the Canadian business continued to grow with 15% growth in sales. The mining sector continues to be subdued and the growth comes from the sales force obtaining specs from end users. During the year they relocated to larger premises and they have added more sales reps with a team now based in British Colombia. In the year they had products installed in the Canadian Hockey Hall of Fame and in CBC’s radio studios.

In India the introduction of general sales tax in July 2017 severely disrupted the performance of the business for much of the year. As the year progressed the business community overcame the initial shock and following a reduction in the GST rates applicable to the group’s product, business activity increased considerably in the latter months of the year allowing it to break even for the year as a whole.

This level of activity has continued in the first months of the new year. The portfolio of projects continues to increase monthly as the sales extend Polyflor’s footprint across the country. Healthcare remains at the core of opportunities but the year has seen sales to the Indian Space Research Organisation, Goldman Sachs’ offices in Bangalore and the Chaitanya Bharati Institute of Technology. Although competition from both global and local players is tough throughout the market they are seeing increasing levels of specifications for their products which bodes well for the future.

In the ROW, in order to further support their activities they opened Polyflor PZE in Dubai in February 2018 as a representative office to support their trade in the region and enable them to employ local sales staff. They won the contract to supply Al Hokair Play Centres across Saudi Arabia and the UAE and they have every expectation of increased penetration of these markets.

The Palettone range is a premium homogenous sheet vinyl collection. It is the largest new range by any manufacturer in this core product area for many years and offers a collection of 50 colours optimised for the global market. In recent years a lot of competitor focus has been in the area of luxury vinyl tile but vinyl sheet continues to be a large sector of the market. The feedback received so far since the launch has apparently been very good.

As the Brexit deadline grows nearer, the board remain vigilant for issues that may arise. They believe they are well placed in that they export to far more countries outside than the EU than inside and they have attained full Authorised Economic Operator status with HMRC. It is considered, depending on the exact details of Brexit, that this will minimise the risk of any post-Brexit border delays.

Trading since the year-end continues to be solid, particularly in the UK. Given the adverse raw material price increases over the last year they have increased their prices which their trade partners have accepted. In addition, they have updated their product portfolio and to date the new products have received a very good reaction from customers. The board are therefore confident of continued progress in the coming year.

At the current share price the shares are trading on a PE ratio of 21.8 which falls to 20.1 on next year’s consensus forecast. After a 4.3% increase in the final dividend the shares are yielding 3.5% which increases to 3.6% on next year’s forecast. At the year-end the group had a net cash position of £50.7M compared to £52.5M at the end of last year.

Overall then, this has been a bit of a mixed year for the group. Profits saw a modest rise due to a reduction in pension costs, without which there would have been a modest fall. Net assets rose but the operating cash flow declined. This was due to working capital movements, however, and cash profits were higher this year. The group remains very cash generative but the free cash flow didn’t quite cover the dividends this year.

The issue seems to be due to increased costs, due to supplier price rises, adverse forex movements and the launch of the Palettone range at the end of the year. UK margins in particular have been squeezed due to the weak pound and a lack of government infrastructure spend. On the other hand, the rest of Europe, Australia and Canada all seem to be performing well. This remains a high quality company but the shares are not cheap with a forward PE of 20.1 and yield of 3.6%. It is worth noting the big pile of net cash, however. I would like to get back in to this share but think perhaps I can do so at a better valuation?

On the 7th December the group released a trading update covering the first five months of the year. Following a £2M investment in Palettone, customer interest has already exceeded their expectations and examples of installations are the Charite Universitatsmedizin in Berlin and the Theatre du Petit Saint Martin in Paris. In addition Polysafe Verona Pure Colour has been installed in a nursing home in Dublin.

Trading to date has been encouraging and they have traded ahead of last year in terms of turnover and profits. The board is confident in the prospects of the company.

On the 30th January the group released a trading update covering the first half of the year. Trading was encouraging in the first five months of the year but December was disappointing, having been impacted by the UK and relates in part to fewer trading days and year-end stock reductions by UK distributors. Trading in January is ahead of the comparative period, however. In addition they have seen margin improvement and profit for the half year will be at a record level. Confidence in full year progress continues.