Braemar Shipping has now released their final results for the year ended 2018.

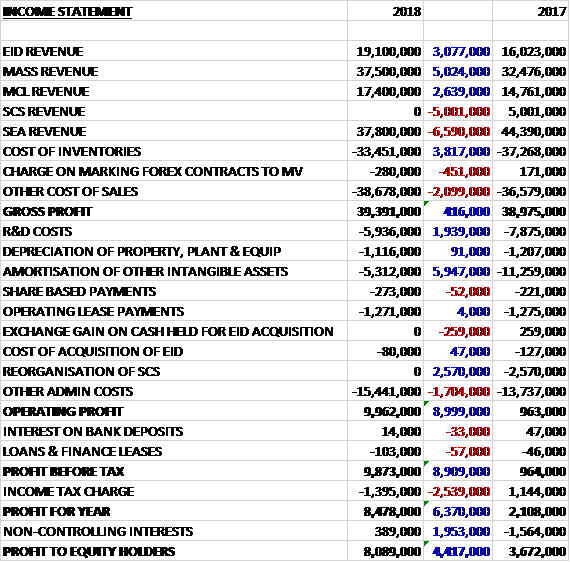

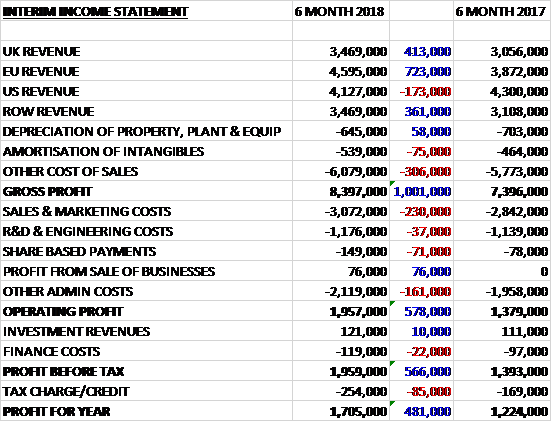

Revenues declined by £2.5M when compared to last year as the maiden £3.7M contribution from the financial business was offset by a £4.4M decline in technical revenue, a £1.3M decrease in shipbroking revenue and a £613K reduction in logistics revenue. Cost of sales also reduced to give a gross profit £125K lower. Amortisation of acquired intangibles increased by £1.9M, there was no gain on the disposal of an investment (£1.7M last time), there were £5M of costs relating to the Naves acquisition and £594K for the Atlantic Brokers acquisition. Other restructuring costs fell by £2.9M, however, and other operating costs fell by £3.4M. All of this meant that the operating loss represented a £1.4M detrimental swing. Finance costs increased by £349K and tax charges were up £857K to give an annual loss of £2.9M, an increase of £2.4M year on year.

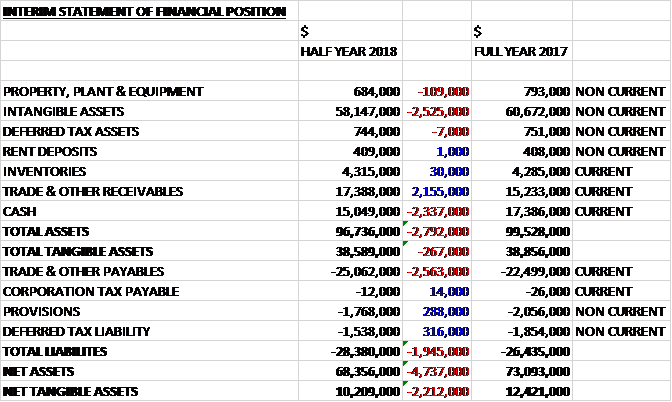

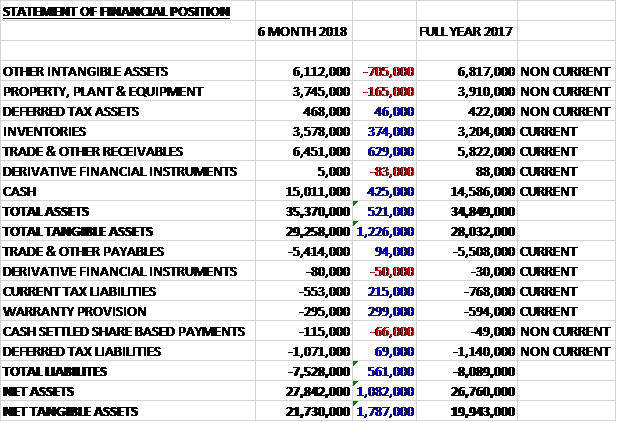

When compared to the end point of last year, total assets increased by £6.7M driven by an £11.2M growth in goodwill, a £2.9M increase in assets held for sale, and a £2.7M growth in other receivables, partially offset by a £6M decline in trade receivables and a £1.4M decrease in cash. Total assets also increased during the year as a £1.7M fall in trade payables and a £2.4M decline in other accruals and deferred income was more than offset by a £7.3M growth in short term borrowings and a £10.3M increase in deferred consideration. The end result was a net tangible asset level of just £1.3M, a decline of £18.8M year on year.

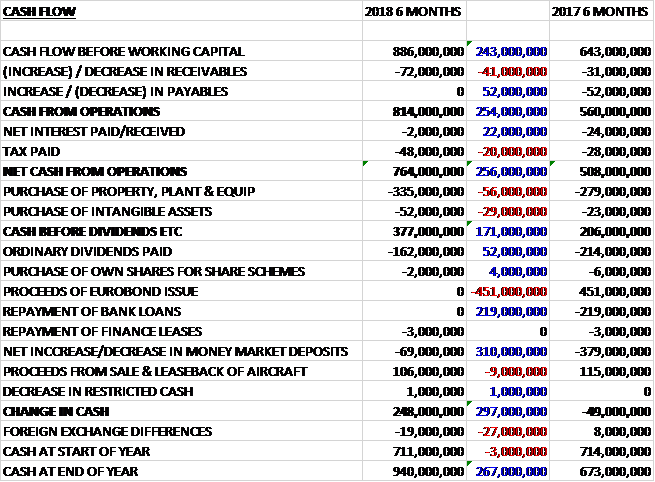

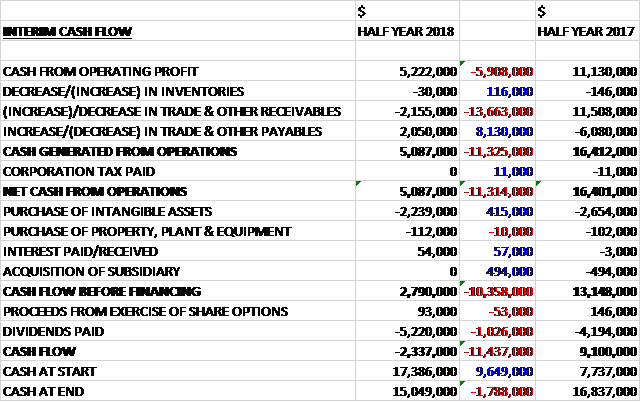

Before movements in working capital, cash profits declined by £663K to £2.9M. There was a cash inflow from working capital, but this was lower than last year and after tax payments reduced by £1.5M the net cash from operations was £3.1M, a decline of £1.6M year on year. The group spent £995K on capex and £5.9M on acquisitions which meant that there was a cash outflow of £3.8M before financing. They then took out a net £7.3M of new borrowings, paid out £3M in dividends and spent £1.1M on their own shares to give a cash outflow of £552K for the year and a cash level of £5.4M at the year-end.

The Shipbroking results were £7.7M, a decline of £140K year on year. The markets were characterised by a weakening of tanker rates and the offshore rates remained low. The dry cargo market was stronger, however, which contributed to firm activity in sale and purchase. Transaction volumes increased in virtually all sectors and the total forward order book at the year-end had grown by $5M to $44M. During the year they sought to build their presence in the dry cargo sector by hiring several dry cargo brokers in London, Singapore, Australia and Brazil.

The deep sea tanker market weakened further towards the end of the year. Fleet size in the crude tanker market grew at a faster rate than demand. Deliveries of new tonnage rose and whilst demolition values experienced some improvement, the growing disparity between vessel supply and demand put downward pressure on rates and income. Fleet size growth in the products tanker tankers slowed down but the historic oversupply coupled with high product stocks and reduced vessel demand drove a decline in earnings.

Next year both crude and product tanker fleet growth is expected to fall with an expected reduction in deliveries of new tonnage and an increase in the level of ship demolition. Growth in demand for crude oil is expected from the key importing regions of China and India which are seeking crude oil supply from non-OPEC producers in the Atlantic basin. Improvements to inland and portside infrastructure in the US are expected to make their growing supply of these products available for export. US exports are expected to require larger vessels with the result that projected tonne-mile demand growth will exceed projected supply growth. Although fleet utilisation may only be marginally better, the board feel an improved trading environment could lead to an improvement in earnings, although the overall view is that 2019 will continue to be challenging for tanker markets.

High stock levels of refined product have been a major factor in the weakness of the product tanker market since 2015. Inventories in OECD countries have been drawn down to the 2012-2016 average during the year leaving the product tanker market likely to benefit from demand growth. As consumers are likely to increase their reliance on imports, this may allow increased arbitrage trade opportunities. They expect oil demand growth in many importing regions during 2019 which is expected to improve CPP trade. They expect clean tanker demand growth will be matched by fleet growth leaving the supply and demand balance broadly unchanged.

There has been a continued expansion of the fleet of gas carriers in the VLGC sector which has continued to put pressure on freight rates in the spot market and restricted demand for time charters. The group’s fixture volumes and earnings remained steady, however. The LNG shipping market experienced demand growth towards the end of 2017 and a number of new export facilities came onstream in the US, Malaysia and Australia. In 2018 it is expected that further new facilities will come on line in Australia, the US and Russia which will fulfil the demand growth in China.

Weakness in LPG freight rates continued during the year as fleet growth outpaced seaborne LPG trade, particularly in the VLGC sector. They expect a slowdown in fleet growth and increased LPG production next year, particularly in the US. This, together with increasing demand in the key markets of India and China, is expected to improve rates.

The dry bulk market performed well during the year due to increased demand and reduced fleet growth. The group continues to develop their market presence and now have a strong global team in place which has significantly increased their transaction volume. While the whole market is presently weak, they expect it to improve during the year across most dry bulk sectors. Chinese steel production will remain the key driver for dry bulk commodities trade.

The offshore desk continued to experience over-supplied markets as global oil and gas exploration and production activity remained low. They are starting to see early indications of market recovery in some regions but it will take some time for oil price increases to translate into increased exploration and production expenditure. They have maintained their core team in readiness for a cyclical recovery.

During the year the team concluded similar volumes of second-hand and demolition vessel transactions compared to the prior year with an increase in the average value of vessels sold. Most of the vessel sales were dry bulk carriers with reduced activity on tanker sales. With positive sentiment returning to the dry cargo market and weakened freight rates in the tanker market this was not unexpected. In the coming year they expect to see an increase in demolition as new ballast water treatment regulations come into effect from 2020.

The group were involved in the placing of several important tanker newbuild orders during the year which has enhanced the forward order book. They were also successful in arranging long term employment for the vessels which will benefit future years.

The Technical profits were £722K, an improvement of £2.9M when compared to last year. The key drivers in the improved performance were cost control measures that were implemented last year, combined with increased utilisation of staff. This has been achieved despite a tough environment in the upstream energy sector and the related impact this has on the insurance market. While the oil price continued to recover during the year, they have not yet seen large scale increases in offshore exploration and production, albeit there are promising signs of increased activity for 2018.

Recent announcements from the Lloyds insurance market confirmed the difficult market conditions and while the insurance market sustained significant impact from natural disasters in 2017, they did not have a significant impact on the energy, offshore and commercial hull and machinery sectors. The upstream energy sector continued to experience very low premium levels due to reduced offshore construction projects, rig activity and asset values. They sector reported a profit in the year due to the reduction in volume and size of losses sustained.

In the marine market, while lloyd’s ended up making a loss, this was largely due to compound premium pressure over previous years and the effect of hurricanes Harvey, Irma and Maria, particularly in the Yacht and cargo sectors. While there was an increase in activity associated with the hurricanes, this was tempered by reduced activity in some other areas and continued price pressure for all service providers. As such, their positive performance was despite a challenging environment. They remain optimistic that a cyclical recovery in the upstream sector and an expected hardening of marine insurance markets towards the end of this year, bode well for the future.

The marine warranty surveying and offshore consultancy business continued to be affected by project delays and low exploration and construction activity in the region. Despite a difficult start to the year, they have recorded an improving performance quarter on quarter with a positive result in Q3 and Q4 despite the seasonal downturn of activity in SE Asia in Q4. Vietnam, India, Malaysia and Indonesia continued to be their strongest performing areas and at the close of the year they are seeing an increase in tender activity and are encouraged by contract wins in several of their offices in SE Asia and the Gulf of Mexico.

The consulting engineering business was impacted heavily at the end of the prior year by the reduced activity in the LNG tanker newbuild market and the ongoing delays associate with LNG import/export projects in general. The business returned to profitability in the second half of the year, however.

The team concluded its work to obtain general design approval for the FSP Type B LNG containment system in conjunction with their joint venture partners Honghua Offshore and Jamestown Metal Marine Services. This has resulted in their appointment for additional development work for individual tank designs and moved the project to the next development phase in relation to an export terminal project located in the Gulf of Mexico. They are also currently working on several new build and modification proposals and are encouraged by an improved pipeline of business compared with the same time last year.

The energy loss adjusting business reported a profitable performance in the year. The ongoing low level of upstream activity has had an impact on staff utilisation which averaged just 57%. The office in the Middle East continued to perform well and in the Far East the performance continued to improve throughout the year, augmented by the addition of a number of senior personnel resulting in a significant increase in activity. Upstream activity in Europe and North America has been slower to respond to the improving oil price and so they have experienced lower activity in these locations. They have widened their adjusting services and received numerous instructions in the downstream, mining and power sectors.

The marine hull and machinery surveyor and consultancy had a much better year. This was driven by repositioning the business to access other markets as well as managing cost reductions. In particular they have seen increased work on P&I claims, technical due diligence and ports & harbours consultancy. Utilisation has averaged 60%, a slight fall from last year, but they have been able to raise revenue through the increase of higher value consultancy work.

The Logistics profits were £777K, a decrease of £477K when compared to 2017. In the port and hub agency, following the business development seen last year they have consolidated that position and delivered a solid performance across the global network. Their international hub business continues to develop and win new clients. The UK operations saw a market driven dip in activity in Q3 but by Q4 revenues returned to normal levels. The US business suffered in the first half of the year due to low market activity but they had a strong finish to the year as they won new customers.

Despite competitive pressures the liner agency and freight forwarding business maintained a steady performance. In freight forwarding they continued to experience challenging market conditions in the imports and exports business and an increasingly competitive environment. An adverse mix of activity diluted margins, however. There was a one-off charge during the year of £500K for the conclusion and settlement of an historic claim relating to activity in the early 2000s. This followed £250K paid out last year.

The Financial business made a maiden profit of £1.8M this year. During the year they supported more than 20 restructuring mandates. This was driven by the ongoing structural weakness in shipping sectors such as tankers, MPP/heavy lift and smaller container vessels without long term employment. The pre and post insolvency and management business benefited from the time lagged impact of cyclical lows in the container market and in the dry bulk market seen in 2016. Increasing charter rates indicate decreasing insolvency filing activity with lenders and owners moving to sell off or refinance assets. Where this may limit insolvency advisory services, it provides opportunities to strengthen their refinancing service portfolio.

Deal flow from restructuring related sale and purchase activity remained strong with more than 20 vessels being sold during the period. Lenders are using increasing asset price in containers and dry bulkers to exit from loans and vessels.

European banks are downsizing their portfolios and shrinking new business volumes so an increasing number of shipowners are facing the need to develop new funding sources. The business is supporting clients to attract both debt and equity financing in an increasingly complex environment. They have worked with more than fifty finance providers for many years and are able to broaden shipowners’ relationships with new banks.

The group expect their activities around loan acquisition support services and loan servicing to increase in the short and medium term. They have received enquiries concerning the disposal of loan portfolios.

The German market represents the historic core of the NAVES business. They have expanded to support the Greek and Cypriot markets and have established a presence in London. They continue to review geographic expansion opportunities to strengthen their links to institutional investors as well as integrate their services with the wider Braemar group.

During the year the group resolved to dispose of their response operations under the technical division. The business has net assets of £2.1M and made a loss of £595K in the year. They expect to sell the business within the year.

In September the group acquired NAVES Corporate Finance, headquartered in Hamburg. They advise clients on corporate finance related to the maritime industry including restructuring advisory, corporate finance advisory, M&A, asset brokerage and financial asset management. The agreement provides for a minimum consideration of €24M and a maximum of €35M (generating goodwill of £12.5M). The initial consideration was €14.8M, of which half was paid in cash and the other half by the issue of convertible loan notes; and €1.5M to be satisfied by the issue of 458,166 shares to the sellers. Three annual instalments of €1.4M will be payable to the sellers, 50% in cash and 50% by the issue of loan notes and five annual instalments of €700K will be payable to sellers by the issue of loan notes. An additional amount of up to €11M may be payable over the three years following completion in loan notes. The business generated an operating profit of €3M in 2016. To be honest, this seems like a rather expensive and complicated transaction.

In February 2018 the group acquired Atlantic Brokers, an introducing broker of physical and financial coal products in the Atlantic and Pacific basins. There was a total consideration of £4.8M. £2.7M was in cash and £2.1M will be satisfied by the issue of 804,426 shares at a price of £2.61 per share, generating goodwill of just £12K. The business made a pre-tax profit of £600K last year which seems a good deal to me.

There were a number of “non-recurring” items during the year. The group charged amortisation of £2.4M in relation to acquired intangibles. Acquisition related expenditure included £600K incurred in relation to the restricted share plan implemented to retain key staff following the merger with ACM Shipping. The incurred expenditure of £5.1M directly linked to the acquisition of NAVES. This included £2.1M of acquisition fees and £3M of post-acquisition remuneration payable. Finally they incurred £600K of expenditure directly linked to the acquisition of Atlantic Brokers including £400K of acquisition fees and £200K of post- acquisition remuneration.

At this point in the cycle, tanker freight rates are relatively low and with the growth in the fleet, they are unlikely to see a recovery before next year. The dry bulk market has been recovering and the board expect this to continue through the year. In the medium term it is likely that they will see an increase in demolition as new environmental legislation takes effect by 2020. The financial division is expected to increase its contribution to the group’s profits due to the full year of ownership and they expect the technical and logistics divisions to continue their recent recovery trends. The impact of Brexit on the logistics business is as of yet hard to quantify.

The forward order book has increased by 13% to $44M compared to the start of the year.

As the group was loss making during the year the current PE ratio is rather meaningless but going on the consensus forecast for next year they are trading on a forward PE ratio of 10.2. After an increase in the dividend the shares are yielding 6%, increasing to 6.5% on next year’s forecast. At the year-end the group had a net debt position of £2.4M compared to a net cash position of £7.1M at the same point of last year.

On the 22nd June the group released a trading update covering Q1 2019 which was in line with board expectations. The shipping markets are largely unchanged since the results announcement. Strong commodities demand continues to drive the dry bulk market while the tanker freight market remains below average levels. The group’s sale and purchase activity was supported by fleet transactions in more than one sector and has contributed to the strong forward order book.

NAVES had a strong Q1, concluding several refinancing transactions as well as providing advisory services to purchasers of shipping debt portfolios, and has traded ahead of board expectations. In the Technical business, trading activity remains relatively subdued, especially in offshore, but the level of new enquiries is providing encouragement.

The group’s port agency and hub management business has had a strong Q1 assisted by improved performances from overseas operations which are being developed. These are offset somewhat by lower freight forwarding activity. The group also announced that James Hayward has been appointed as interim CFO.

Going forward the board’s expectations for the year remain unchanged and the group as a whole is trading in line with expectations.

Overall then this has been a rather mixed year for the group. The losses worsened, not helped by the rather large acquisition costs. Even without these, however, the underlying organic profit declined. The net tangible asset level declined too, and is now precariously close to zero. The operating cash flow also fell and no free cash was generated after the acquisition. There was some prior to that but not enough to cover the dividends.

The broker business declined somewhat due to a weaker tanker market and continued low levels of offshore activity. There are some signs of improvement with a stronger order book but 2019 is expected to continue to be challenging for the tanker market. The dry bulk market is much better, mainly driven by Chinese steelmaking requirements. The technical division saw an improvement in performance due to cost control measures. The upstream energy market continued to be tough, however.

The logistics business saw profits dive, apparently due to a poor Q1 in the UK port division and a poor first half of the year in the US. Both divisions have shown improved performances by the end of the year. The financial division is contributing well and should offer a good counter-cyclical revenue stream. The acquisition does seem to be needlessly complex and rather costly, however. The shares are not very expensive, trading on a forward PE of 10.2 and yield of 6.5%. This is a tricky one – Q1 trading is not very different from the full year and the group seems to have stabilised but on the other hand I am getting concerned they are over-reaching on acquisitions.

On the 10th October the group announced the disposal of Braemar Response to Group Ambipar for £774K. This comprises an initial cash payment of £400K with a further £374K payable within a year of completion. The group purchased the business in 2006 for £900K. It made a loss of £595K last year.