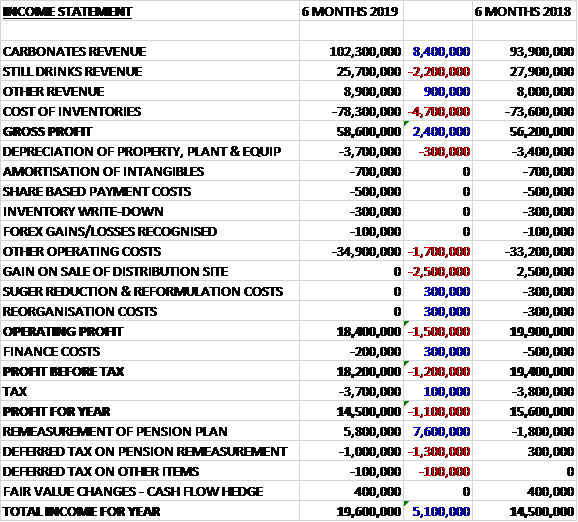

AG Barr have now released their interim results for the year ending 2019.

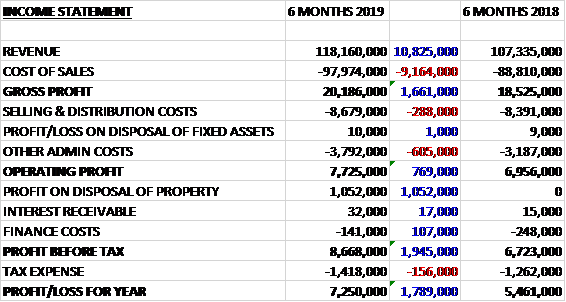

Revenues increased when compared to the first half of last year as a £2.2M decline in still drinks revenue was more than offset by an £8.4M increase in carbonates revenue and a £900K growth in other revenue. Cost of sales also increased to give a gross profit £2.4M higher. Operating costs increased by £2M and there was no sale of buildings, which brought in £2.5M last time. There was also no reformulation costs or reorganisation costs, which were both £300K last time which meant the operating profit declined by £1.5M. Finance costs were down £300K and tax charges fell by £100K to give a profit for the period of £14.5M, a decline of £1.1M year on year.

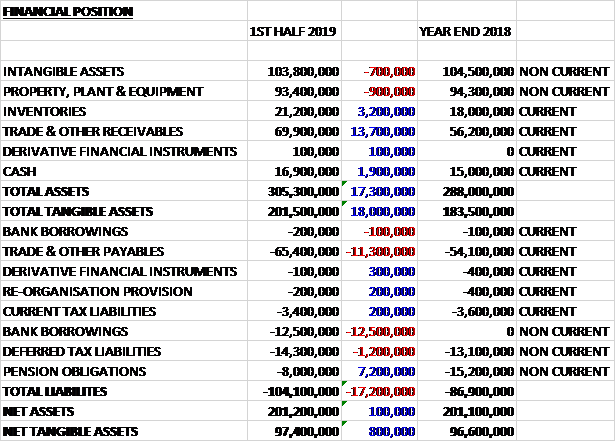

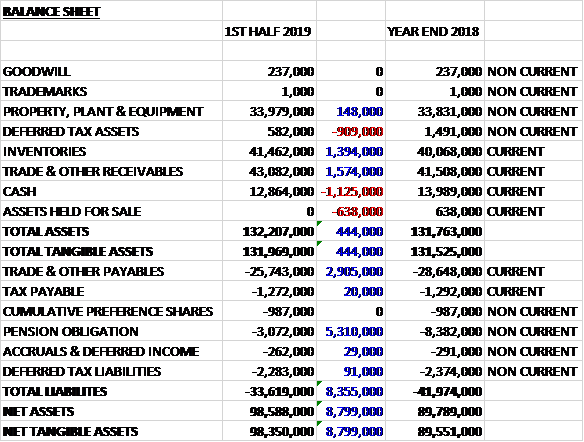

When compared to the end point of last year, total assets increased by £17.3M driven by a £13.7M growth in receivables, a £3.2M increase in inventories and a £1.9M growth in cash. Total liabilities also increased during the period as a £7.2M decline in pension obligations was more than offset by a £12.6M increase in bank borrowings and an £11.3M increase in payables. The end result was a net tangible asset level of £97.4M, a growth of £800K over the past six months.

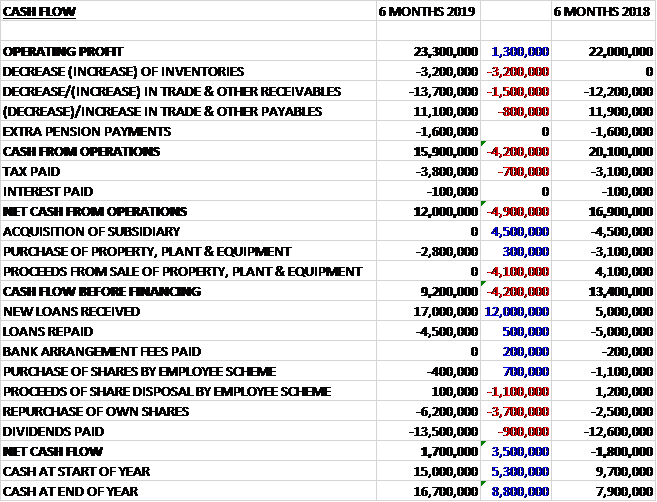

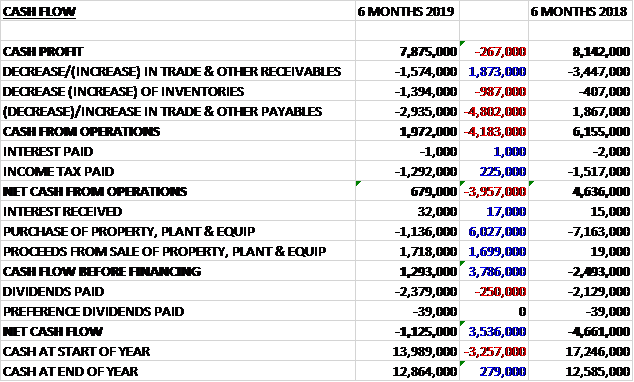

Before movements in working capital, cash profits increased

by £1.3M to £23.3M. There was a cash

outflow from working capital and tax payments increased by £700K to give a net

cash from operations of £12M, a decline of £4.9M year on year. The group spent £2.8M on capex to give a free

cash flow of £9.2M. This did not cover

the £13.5M paid out in dividends or the £6.2M spent on share repurchases so the

group took out a net £12.5M. This gave a

cash flow of £1.7 for the period and a cash level of £16.7M at the period-end.

The gross profit in the carbonates business was £47M, a

growth of £2.7M year on year. The gross

profit in the still drinks business was £7.4M, a decline of £800K when compared

to the first half of last year.

The gross profit in the other business was £4.2M, a growth

of £500K year on year. The Funkin

business continues to grow in its traditional areas and now also in new formats

and new market segments. They have seen

the take-home packs, initially launched last year, begin to gain sales traction

in the grocery channel while the development of the Funkin draft cocktail

proposition is rolling out into the on-trade and has already enjoyed success at

outdoor events during the festival season.

Retail pricing increased across the market following the

implementation of the Soft Drinks Levy in April. The total market grew by 7.7% in value terms

and 3.8% in volume. The soft drinks

market experienced the effect of weather extremes, from the significant snowfall

in Q1 to the hot summer weather. The

unusual demand pattern which arose was further compounded by the shortage of

CO2 in the early summer which affected soft drinks supply for a number of

weeks.

The group delivered strong volume market share gains, up 15%

with a pleasing performance from IRN-BRU, particularly in England and

Wales. Following the execution of the

reformulation programme they have continued to invest in their core bands with particular

emphasis on IRN-BRU, Rubicon and Strathmore.

The period also saw the group initiate their trading partnerships with

Bundaberg and San Benedetto, both of which have made a positive start and are

already adding value.

The current trading strategy is delivering volume benefits

which they aim to maintain for the rest of the year as they navigate their way

through the changing market. As

expected, the operating margin was 13.4% reflecting the volume focus and investments

made.

There will shortly be a new accounting standard covering operating

leases. Had it been implemented during

the period, the effect would be to increase the net book value of property, plant

and equipment by £6.9M with a corresponding finance lease liability of

£8.2M. The net impact on retained

earnings would be a charge of £1M. To

date, £9.7M of operating lease rentals have been recognised in respect of the

assessed leases. Based on management’s

ongoing exercise on leases identified to date, under these standards, £8.6M of

depreciation would have been charged plus a further £2.1M of interest charges.

Going forward the group plan to invest further across the

second half of the year which they expect will have a moderate impact on

margins but they remain on target to meet their profit expectations for the

full year.

At the current share price the shares are trading on a PE

ratio of 25.1 which falls to 23.4 on the full year consensus forecast. After a 5% increase in the interim dividend

the shares are yielding 2.1% which is forecast to remain the same for the full

year. At the period-end the group had a

net cash position of £4.2M compared to £7.9M at the same point of last

year.

On the 25th January the group released a trading update

covering the year. Revenue is expected

to be 5% up on last year at £277M. They

gained further market share in the UK which saw volumes up 3% and value up

8%. The impact of the soft drinks levy

has been evident across the market with value growth significantly outstripping

volume and having taken the opportunity to drive volume growth during the

period the group are now expecting to return to a more value led trading

strategy.

They have invested across brands, assets and people which

has supported growth but had a moderate impact on margins. They remain confident overall of delivering

profit in line with board expectations, however. Going forward, further regulatory

intervention is on the horizon but the board are confident of profitable growth

next year.

Overall then this has been a fairly steady period for the

group. Profits declined due to no

freehold sales during the period, underlying profits were up; net assets

increased but the operating cash flow deteriorated with free cash not covering

dividends. This was not helped by

adverse working capital movements, however, and cash profits increased. The Carbonates and Funkin businesses did well

but the still drinks business saw profits decline, it is not clear why this

was. This is a good company but the

recent performance has been a bit lacklustre in my opinion and the shares are

looking a bit expensive with a forward PE of 23.4 and yield of 2.1%. I’m tempted to take profits.

IQE has now released their interim results for the year ending 2018.

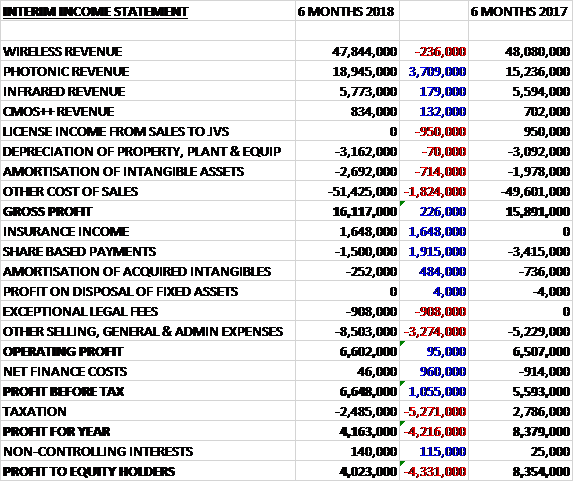

Revenues increased when compared to the first half of last year as a £236K reduction in wireless revenue was more than offset by a £3.7M growth in photonic revenue, a £179K increase in IR revenue and a £132K growth in CMOS++ revenue. License income from sales to joint ventures fell by £950K, however. Amortisation costs were up £714K and other cost of sales increased by £1.9M to give a gross profit £226K higher. The group received £1.6M in insurance income, share based payments fell by £1.9M and amortisation of admin expenses declined by £484K. Offsetting this was a £908K legal fee and a £3.3M increase in other general costs which meant that the operating profit was £95K higher. There was a £960K swing to a finance income but tax charges increased by £5.3M which gave a profit for the period of £4M, a decline of £4.3M year on year.

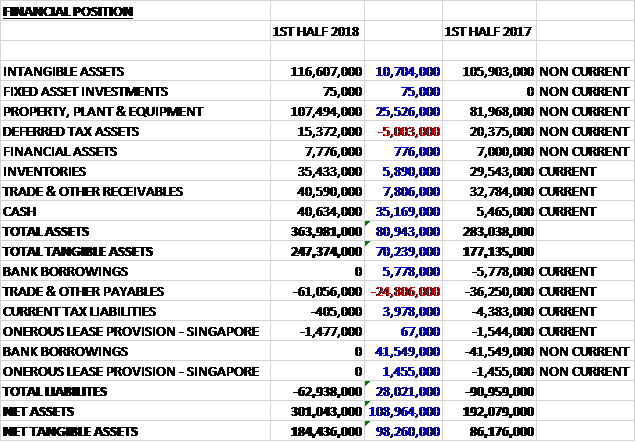

When compared to the end point of last year, total assets increased by £80.9M driven by a £25.5M growth in property, plant and equipment, a £35.2M increase in cash, a £10.7M growth in intangible assets, a £7.8M increase in receivables and a £5.9M growth in inventories, partially offset by a £5M decrease in deferred tax assets. Total liabilities declined during the period as a £24.8M growth in payables was more than offset by a £47.3M decline in bank borrowings and a £4M decrease in current tax liabilities. The end result was a net tangible asset level of £184.4M, a growth of £98.3M over the past six months.

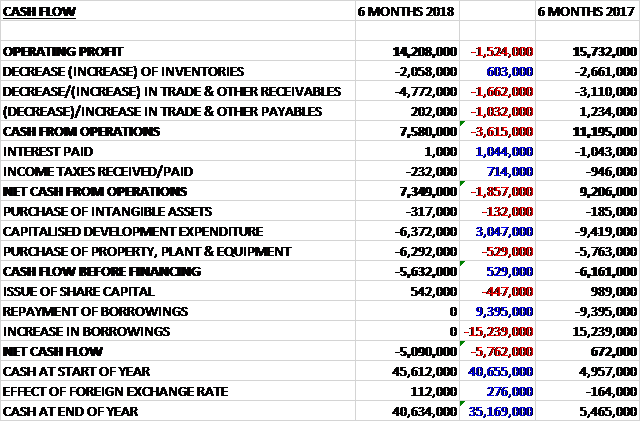

Before movements in working capital, cash profits declined

by £1.5M to £14.2M. There was a cash

outflow from working capital but interest payments fell by £1M and tax payments

were down £714K to give a net cash from operations of £7.3M, a decline of £1.9M

year on year. The group spent £6.4M on

development expenditure, £6.3M on property, plant and equipment and £317K on

other intangible assets to give a cash outflow of £5.6M before financing. The group brought in £542K from the issue of

share capital to give a cash outflow of £5.1M and a cash level of £40.6M at the

period-end.

Currency headwinds, accelerated customer qualification

programmes and Newport foundry pre-production costs resulted in a drag on

profits of around £3.5M.

The operating profit in the wireless business was £6.6M, a

decline of £876K year on year. Inventory

channels, depleted as a consequence of the rapid ramp of VCSELs in H2 2017 were

partially replenished during the period and photonics capacity was directed to

satisfy more than twenty VCSEL chip manufacturer engagements. Operating margins reduced as a consequence of

reactor conversion costs related to switching reactors from photonics to

wireless production.

Despite slower growth in smartphone sales in recent years

the increase in data traffic continues to drive the need for more sophisticated

wireless chip solutions in handsets. The

group sees the roll out of 5G infrastructure as a significant upside potential. Current infrastructure applications such as

base stations, radar and CATB are a small but fast growing part of the

business. The fastest growing segment of

the wireless chip market over the past few years has been for high performance

Bulk Acoustic Wave filters.

The wireless segment continues to be a significant and

stable business for the group and is expected to grow at a rate of up to 5% in

the near term. The division has a number

of developments which provide routes for a return to double digit growth such

as innovation in smartphone hardware, adoption of GaN on silicon technology for

base stations and the transition to 5G communications. The group have also announced that they had

renegotiated a long term supply contract with a tier 1 wireless customer through

to September, securing an extended range of products and increased share of

their epiwafer requirements.

The operating profit in the photonics business was £4.9M, a

decrease of £1.5M when compared to the first half of last year. Revenue from the largest photonics customer

was flat as inventory from the first mass market ramp of VCSEL epiwafters in H2

2017 was consumed in the supply chain.

Other photonics customers were up 40%.

Gross profits were adversely impacted by the Newport foundry

pre-production costs of £900K and low margin customer funded product

development reducing margins by a further £600K. Margins should improve again in the second

half as the production efficiencies of the ramp in output are realised.

Sensing technologies such as 3D sensing and gesture

recognition will represent a growth area in the near term. The group is engaged in a number of

programmes for tier 1 OEMs who are targeting mass market ramps in 3D sensing

applications over the next year and a half.

Alongside the growth in the VCSEL business, the InP business continues

to perform well. This market is being

driven by the need for higher speed, higher capacity fibre optic systems to

address continuing growth in data traffic.

The group are engaged in qualifications with several customers for this

technology and received their first milestone production order for DFB lasers

made using their NIL process.

The operating profit in the IR business was £1.4M, flat year

on year. Beyond defence, the IR division

has been successful in broadening its customer engagements into product

development for mass market consumer applications. They are now engaged with major OEM and

device companies in developing IR products for consumer applications including

sensing.

In the solar business, the terrestrial market remains an

opportunity but as a result of the shifting macroeconomics, focus has shifted

to the space market where these advanced materials are used to power satellites

and UAVs where the higher efficiency has a dramatic cost benefit on

payload. Product qualifications are

underway with leading UAV/satellite manufacturers, paving the way for

commercial revenues.

The operating loss in the CMOS++ business was £791K, an

improvement of £186K compared to the first half of 2017. The group is involved in multiple programmes

across the globe which are developing the core technologies from which they

expect significant revenue streams to emerge over the next three to five years.

The Newport foundry construction and fit out it proceeding

well. Five reactors had been installed

by the end of the period and a further two have been delivered in August with

three more scheduled in H2 to bring the total to ten reactors during the second

half. Commissioning and qualifications

are ongoing and initial production is expected to start in the latter part of

H2 2018

There have been a number of one-off costs during the

period. There was insurance income of

£1.7M relating to the accrued insurance income receivable following the death

of the CFO in April. There were

exceptional legal costs of £900K incurred in respect of a patent dispute

defence.

During the period the group received no revenue and made

purchases of £1.8M from its joint venture in Singapore; and made purchases of

£3.8M and recharges other costs of £1.6M with its joint venture in the UK

Compound Semiconductor Centre.

There are a total of nine Compound Semiconductor Centre

projects underway with a value of £5.4M.

The projects have resulted in formal product development partnerships

with five multinationals, four mid-sized companies, four SMEs and three additional

academic partners. Routes to commercial

income streams are now maturing and the first commercial orders were delivered

in the period. The percentage of non-IQE

revenue received by the centre is increasing steadily and is expected to be in

the range of 15-20% for the full year.

A second phase of capital expansion focused on the

installation of a new cleanroom and a GaN MOCVD reactor designed for Cardiff

Uni research activity was completed in April.

The business looks forward to progressing several key areas in the

second half of the year including delivery of further exploitable outcomes of

the CRD programme, diversification of the research roadmap and wider industry engagement

to develop the commercial revenue pipeline.

The Compound Semiconductor Development Centre in Singapore

is engaged in a number of early stage qualifications for new customers in

China. Twelve new customer engagements

were initiated for fifteen separate product qualifications including five for wireless

pHEMTs and seven for photonics products.

Following the growing tensions in the US and China’s trade and economic

relations, China is reported to have sought to accelerate its efforts to gain

semiconductor self-sufficiency by increasing funding.

The VCSEL wafer ramp for existing 3D consumer applications

started as expected at the end of the period and since the period-end, the

first production for new 3D sensing customers has also started. At this time the group has customer forecast

demand to meet consensus revenue with a 40:60 revenue split for H1/H2 2018.

The group will invest around £6M in expanding GaN capacity in

the US which will start in H2 and be completed in H1 2019. This will enable the closure of the NJ plant

as the transfer of business to Taunton is completed. This consolidation is expected to save around

£1.5M in 2019 and around £3M per annum thereafter.

They will also invest £15M in additional wireless capacity

in Taiwan. This project will start in

September and will complete in the first half of 2019, increasing capacity

there by 40%. With this investment they

will be able to avoid the cost of converting and reconverting reactors from

wireless and photonics and back again which have totalled around £3M over the

last year and a half and provide additional capacity for the wireless

business.

The board remain confident of achieving current market

expectations as long as there are no major forex movements. Next year wireless revenue growth is expected

to be 0-5%, photonics 40-60% and IR 5-15%.

The adjusted operating margins for wireless is expected to remain the

same at 15% with photonics increasing 5% to 40% and IR up 1% to 28%. Capex on intangibles is expected to be

£10-£15M with capex on fixed assets being £20-£30M. Sales phasing is expected to be 42:58.

At the current share price the shares are trading on PE

ratio of 39 which increases to 42 on the full year consensus forecast. At the period-end the group had a net cash

position of £40.6M compared to a net debt position of £41.9M at the same period

of last year as a result of the placing to raise £90M to repay debt and fund

capacity expansion.

On the 13th November the group announced that a

major chip company had received notice from one of their largest customers for

3D sensing laser diodes that they would materially reduce shipments for the

current quarter. As a consequence of the

change in market conditions the group now expected to deliver revenues of £160M

for 2018.

Photonics demand was facing a later but steeper ramp for

VCSELs for consumer products moving into Q4 and with the impact of this recent

announcement coming at this critical time, Photonics wafer revenue growth for

2018 is now expected to be 11% compared to previous guidance of 35% to 50%, and

based on initial indications, it is currently expected to return to 40% to 60%

revenue growth in 2019.

Wireless wafer revenue growth is expected to be 8%, above

the 0% to 5% guidance. Wireless demand,

especially for GaN products, has been strong and capacity was retained through

Q3 to continue to address demand following the replenishment of inventory

channels depleted in H2 2017. IR

revenues are expected to grow at or exceeding the top end of the current

guidance of 5% to 15% this year and to remain at in this range for 2019.

As a result EBITDA for 2018 is now expected to be around

£31M compared to £37.1M in 2017.

On the 25th January the group released a trading

update covering the year as a whole.

They expect to deliver revenues of at least £156M and EBITDA of £27.5M

compared to £154.4M and £37M last year.

Net cash at the year-end was £20.8M compared to £45.6M at the end of

2017.

They closed their facility in New Jersey in order to

consolidate US-based GaN manufacturing capacity in the Massachusetts

facility. The cost of the closure is

estimated to be £3.4M, of which £1.2M will comprise the cash costs of severance

and reactor decommissioning with £2.2M of non-cash impairments. These costs will be an exceptional charge on

the 2018 accounts and the group expects to achieve annual operating cost

savings of around £3M per annum.

They also expect to incur an additional exceptional charge

of £4.5M relating to onerous lease accounting provision for the period through

to the end of the lease Q2 2022 for the unused and unlet space in the Singapore

facility. They reiterate their 2019 guidance.

By the end of the first half of 2019 they will have

completed a significant two year investment programme across their global

operations, commissioning their new mega-foundry in Newport which is dedicated

to photonics, installing additional wireless capacity in Taiwan, expanding

their GaN capacity in the US and IR capacity in Milton Keynes. They will bring additional capacity into

production in Phase 1 in the Newport foundry during H1 with 12 companies

already actively qualifying the new facility.

Overall then this has been a rather difficult period for the

group. Profits were down due to an

increased tax charge – the operating profit was broadly flat. Net assets increased but the operating cash

flow declined with no free cash generated.

The photonics business suffered due to the excess inventory in the

supply chain and the pre-production costs at the Newport foundry and the

wireless business also saw profits decline, seemingly due to having to switch

reactors from the photonics business.

The shares are expensive with a forward PE of 42 but there is promise of

future exciting growth. The trouble is

this has always been the case here.

Success has always been just around the corner and I’m growing a bit

weary of it. I don’t think these offer

good value at this price.

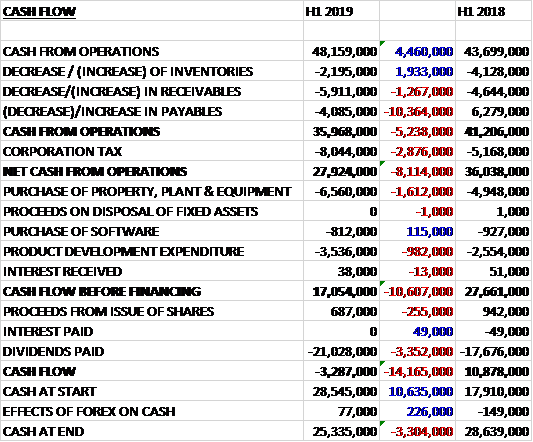

Games Workshop have now released their interim results for the year ending 2019.

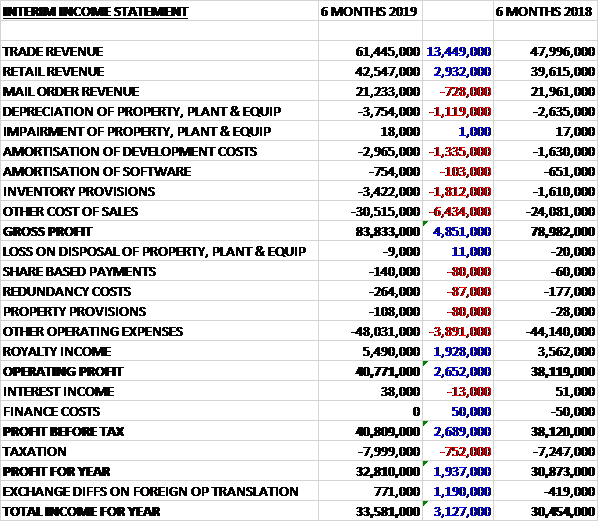

Revenues increased when compared to the first half of last year as a £728K decrease in mail order revenue was more than offset by a £13.4M growth in trade revenue and a £2.9M increase in retail revenue. Depreciation was up £1.1M, amortisation increased by £1.4M, inventory provisions rose by £1.8M and other cost of sales were £6.4M higher to give a gross profit £4.9M above that of last time. Operating expenses increased by £3.9M but the royalty income grew by £1.9M which meant that the operating profit was £2.7M higher. Finance costs were broadly similar but tax charges were up £752K to give a profit for the period of £32.8M, a growth of £1.9M year on year.

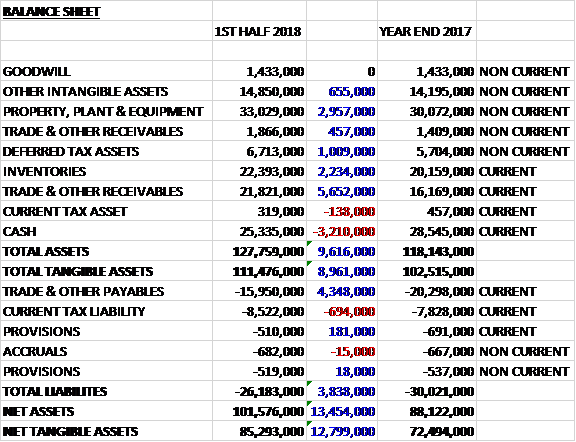

When compared to the end point of last year, total assets increased by £9.6M driven by a £6.1M growth in receivables, a £3M increase in property, plant and equipment, a £2.2M growth in inventories and a £1M increase in deferred tax assets, partially offset by a £3.2M decline in cash. Total liabilities declined during the period, mainly due to a £4.3M fall in payables. The end result was a net tangible asset level of £85.3M, a growth of £12.8M over the past six months.

Before movements in working capital, cash profits increased

by £4.5M to £48.2M. There was a cash

outflow from working capital and after tax charges increased by £2.9M the net

cash from operations was £27.9M, a decline of £8.1M year on year. The group spent £6.6M on property, plant and

equipment, £3.5M on development expenditure and £812K on software to give a

free cash flow of £17.1M. This didn’t

quite cover the £21M paid out in dividends so there was a cash outflow of £3.3M

and a cash level of £25.3M at the period-end.

The operating profit in the Trade business was £22.5M, a growth

of £5.3M year on year with growth in all territories. The net number of trade outlets increased by

300 accounts which helped drive forward sales.

A large number of independent retailers now also sell the group’s

products online.

The operating profit in the Retail business was £4.8M, an

increase of £1.9M when compared to the first half of last year. There was growth in all territories except

Australia and New Zealand. They opened

23 stores and closed 5 with recruiting new store managers an area of

focus.

The operating profit in the Online business was £13.1M, a

decline of £566K when compared to the first half of last year. Sales in the Citadel online shop were flat

and the Forge World and Black Library stores declined slightly. Sales of digital titles remain comparable to

last year and the group continue to increase the functionality of their online

stores.

The operating profit in the Product and Supply business was

£9.6M, a decrease of £3.5M year on year.

The operating profit from Royalties was £5M, a growth of £1.8M when

compared to the first half of last year reflecting the change in accounting

mentioned below.

As the group moves to complete a series of major investment

projects, the gross margin and stock levels are now currently where they’d like

them to be. The completion of the new

Nottingham factory and ERP projects will allow them to fully optimise their

Nottingham site. From there, they will

begin to upgrade their warehousing capacity in both Memphis and Nottingham. These further investments will help them maintain

their current volumes, increase efficiencies and give good scope for sales

growth in the future.

The community website continues to increase its readership

with visitor numbers up 30% with almost a million visits to the site per week. Elsewhere on social media they have over

250,000 people signed up to the Warhammer.tv site.

There have been a number of accounting changes that have had

the effect of reducing EPS by 0.7p.

Amounts receivable from customers in respect of delivery charges are now

recognised as revenue when previously the income was offset against delivery

charges in cost of sales. Also the minimum

royalty guarantee will be recognised in full at inception of the contract when

previously it was deferred and recognised in accruals and deferred income and

released with licensee sales.

Going forward, December trading continued in line with the

performance in the first half.

At the current share price the shares are trading on a PE

ratio of 16.2 which increases to 17 on the full year forecast. After an increase in the dividends the shares

are yielding 4.4% which falls to 4.1% on the full year forecast. At the period-end the group had a net cash

position of £25.3M compared to £28.6M at the same point last year.

Overall then the group had a pretty decent period overall. Profits were up, net assets increased but the operating cash flow deteriorated somewhat with the dividends not quite being covered by free cash. This was due to adverse working capital movements related to the recent investments being made, however, and free cash saw an improvement. The trade and retail sectors are performing well but there was a bit of a blip in online. The reason for this wasn’t really given so this is a bit concerning. The shares are also no longer that cheap with a forward PE of 17 and yield of 4.1%. I do feel this is a great company but not sure the value is quite right at the moment.

On the 12th April the group announced that trading has continued well. Compared to last year, sales and profits are ahead. Royalties receivable are also ahead of the prior year following the signing of new license agreements. The board’s current expectation is that pre-tax profit for the year will be around £80M.

On the 7th June the group released a trading

update covering the year. They expect

sales to be £254M and the group’s pre-tax profit to be at least £80M. Royalties receivable from licensing are

around £11M.

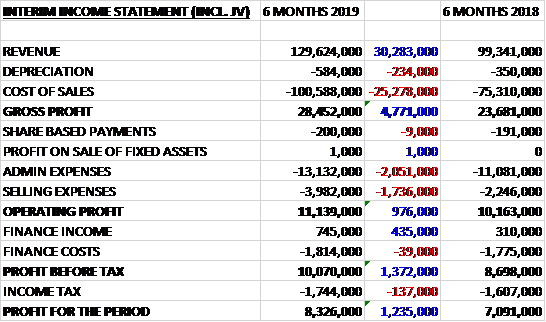

Telford Homes have now released their interim results for the year ending 2019.

Revenues increased by £30.3M when compared to the first half of last year and after cost of sales also increased the gross profit was £4.8M higher. Admin expenses grew by £2.1M and selling expenses rose £1.7M which meant the operating profit increased by £976K. Finance income grew by £435K but tax charges rose £137K which mean that the profit for the period was £8.3M, a growth of £1.2M year on year.

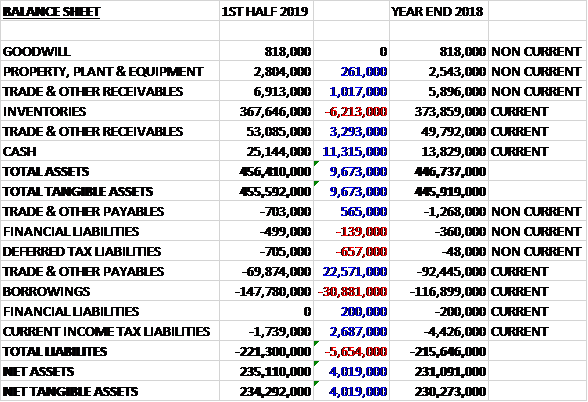

When compared to the end point of last year, total assets increased by £9.7M driven by an £11.3M growth in cash and a £4.3M increase in receivables, partially offset by a £6.2M decline in inventories. Total liabilities also increased during the period as a £23M decline in payables and a £2.7M decrease in current tax liabilities was more than offset by a £30.9M increase in borrowings. The end result was a net tangible asset level of £234.3M, a growth of £4M over the past six months.

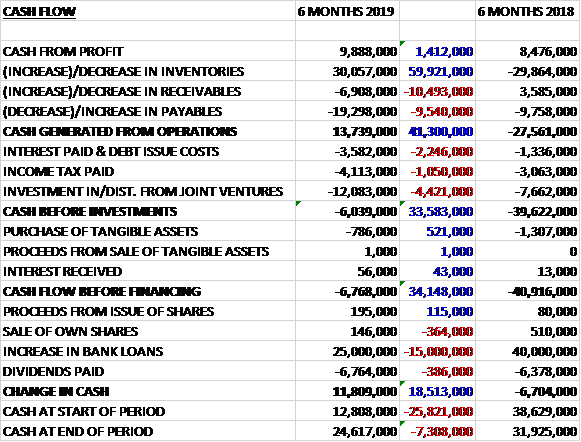

Before movements in working capital, cash profits increased

by £1.4M to £9.9M. There was a cash

inflow from working capital but interest payments increased by £2.2M, tax

payments were up £1.1M and there was a £4.4M increase in the investment into

joint ventures which meant that the cash outflow before investments was £6M, an

improvement of £33.6M year on year. The

spent £786K on intangible assets which meant that before financing there was a

cash outflow of £6.8M.

The group are progressing well with their existing build to

rent projects and in August they handed over The Pavilions, their first build

to rent development which was purchased by L&Q in 2016. They are getting closer to build completion

of the two schemes they are working on with M&G in Carmen Street and

Redclyffe Road and the same applies to the build to rent block at New Garden

Quarter which was sold to Folio. They

are now moving towards entering a full build contract with Greystar for 894

build to rent homes at Parkside in Nine Elms and they expect to start on site

early in 2019. In addition, they have

announced that they started contractual negotiations with a major build to rent

investor for the sale of 257 homes in Walthamstow and that process is nearly

complete.

In October they announced that they have been chosen to

partner a major land owner to obtain planning consent for around 700 homes on a

site in East London, with a view to developing a combination of subsidised

affordable housing, build to rent homes for the landowner and individual sale

homes. This partnership with an

established property owner is a key milestone in the build to rent strategy.

Also, with the help of Savills they are making progress

towards identifying at least one institutional investor with whom they can

forge a long-term partnership for future build to rent activity. The aim is to create a significant long-term

build to rent pipeline to the benefit of both parties. They anticipate being in a position to select

a partner by the end of 2018 with a view to entering into a contractual

arrangement in early 2019.

Despite lower liquidity in the market as a consequence of

uncertainty around Brexit the group have continued to secure individual sales,

particularly for homes prices below £600K on developments that are complete or

close to completion. Homes priced above

£600K are currently more difficult to sell, especially if customers already own

a home and are delaying a new purchase.

This price point represents a relatively small proportion of the overall

portfolio, however.

The group held their second off-plan sale at New Garden

Quarter. The combined UK and overseas

launch of Gallions Point resulted in 15 sales with performance supressed by

Brexit worries and the potential risk of increased stamp duty for overseas

investors. The majority of these homes

are priced under £600K with completions due in 2020 so the board are confident

they will be attractive to owner-occupiers at the appropriate time. Sales to individual investors, whether in the

UK or overseas, no longer represent a significant part of the future pipeline with

build to rent transactions and individual owner-occupier sales now drawing

focus.

The open market sale remains an important part of the

business model with the recent purchase from Greystar of part of their site in

Greenford. The group will deliver 194

homes for individual open market sale at an average selling price of £500K, and

84 affordable homes for shared ownership.

They intend to begin work on site in mid-2019 with completion expected

in 2022. The group are engaged in

discussions on two land acquisition sites.

The current development pipeline stands at just over 5,000, including

Parkside in Nine Elms, and has a gross development value of £1.65BN.

The group expect a much greater number of open market

completions in H2 together with a number of new construction contracts and

therefore the results for the year will be weighted towards the second

half. There have been a few isolated

cases of modest build cost pressures in later trades as projects complete but

general construction activity in London, particularly residential development,

does appear to have reduced a little in recent months which tends to take some

of the pressure off trades that are otherwise in high demand.

Going forward the group still have work to do in order to

achieve their original target of exceeding £50M of total profit before tax for

2019 and Brexit brings a certain amount of unpredictability.

At the current share price the shares are trading on a PE

ratio of 6.9 which is forecast to remain the same for the full year

forecast. After a 6.3% increase in the

interim dividend the shares are yielding 5.1% which increases to 5.2% on the

full year forecast. At the period-end

the group had a net debt position of £122.6M compared to £103.1M at the

year-end.

Overall then the performance during the first half has been an improvement on last year. Profits are up, net assets improved and although the group wasn’t cash generative at the operating level, the cash flow did improve. The build to rent focus should cushion the group somewhat but there is no doubt that conditions in the housing market are being affected by a number of issues, not least Brexit. The forward PE of 6.9 and yield of 5.2% suggest the shares are good value but I feel there is a real possibility that the group might not make its target sales if conditions continue to deteriorate.

On the 11th February the group announced that it

had exchange contracts for the purchase of a site in Stratford for a total cash

consideration of £20M. The land has been

acquired from the Department for Transport.

The 1.14 acre site is expected to deliver 380 homes with subsidised

affordable housing expected to make up 50% of the development. The gross development value is expected to be

at least £160M.

On the 19th February the group announced that it

had exchanged contracts for the sale of its Equipment Works build to rent

development site in Walthamstow to a joint venture between Henderson Park and

Greystar. The transaction comprises the

sale of the freehold interest in the land and the construction of 257 build to

rent homes for a net consideration of £105.5M.

The sale will consist of an initial land payment followed by regular

payments throughout the construction period and a final profit payment.

The 3.16 acre site was purchased in December 2017 and has

full planning consent for 337 new homes including 80 affordable homes and

18,830 square feet of flexible commercial space. The development is under construction and is

expected to be completed in late 2021.

On the 5th March the group announced that it has

chosen Invesco and M&G as their long term strategic partners for future

build to rent transactions. M&G will

be their priority partner for schemes including up to 200 build to rent homes

and Invesco will have priority for the larger schemes.

On the 28th February the group released a trading

update. Despite the positive outlook on

build to rent the London sales market remains subdued. Whilst sales are still being secured they are

being achieved at a slower rate than under normal market conditions and

customer expectations of increased incentives and discounts are putting some

pressure on sale margins.

In addition, two build contracts that were expected to

exchange in 2019 are now likely to happen in Q1 2020, due primarily to planning

issues, and this moves around £5M of profit between the two years. New individual sales secured since November

effectively offset these contracts such that they still expect pre-tax profit

for 2019 will be around £40M.

At this time they do not expect a significant improvement in

the individual sale market in the short term and as a result expect a continued

impact on sales rates and margins in 2020.

They have also experienced some frustrating challenges in achieving

planning consents on some developments including most notably the LEB Building

in Bethnal Green. Planning delays can

increase costs, push back the timing of profit recognition and impact on their

ability to invest in new opportunities.

Finally they have experienced a disappointing delay to the construction

programme in Finsbury Park of around six months due to matters dealing with

transport bodies and the need to coincide with works undertaken by third

parties. Given that completions were

largely due in the second half of 2020 this will have a significant impact in

terms of moving profit of around £15M into 2021.

These factors, combined with the impact of lower margin

build to rent transactions, are changing their profit expectations for the next

few years and they now expect pre-tax profit in 2020 to be significantly lower

than 2019. After 2020 profits in each

year will grow again, albeit at lower margins due to the increased focus on

build to rent.

Zytronic has now released their final results for the year ended 2018.

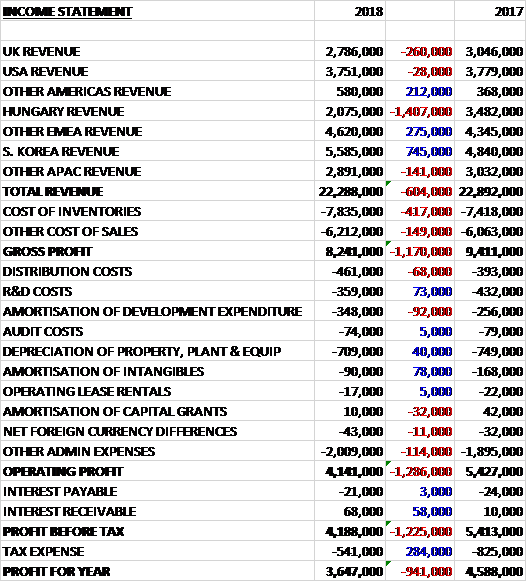

Total revenues declined by £604K when compared to last year as a £745K growth in Korean revenue was more than offset by a £1.4M decline in Hungarian revenue. Cost of inventories were up £417K and other cost of sales grew by £149K to give a gross profit £1.2M higher. Admin expenses also saw a modest rise but there was a £58K growth in interest receivable and a £284K decrease in tax expenses to give a profit for the year of £3.6M, a decline of £941K year on year.

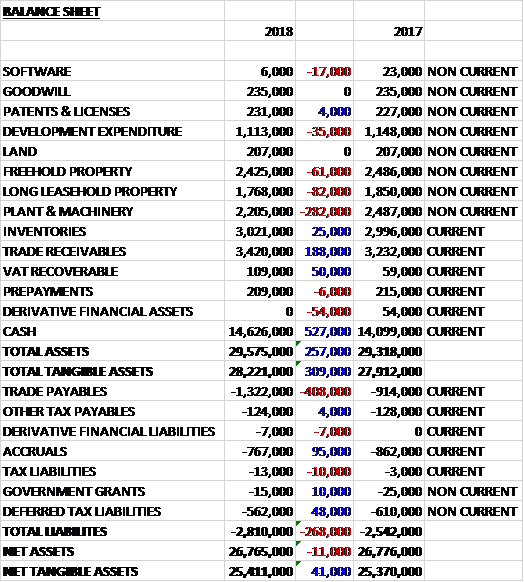

When compared to the end point of last year, total assets increased by £257K driven by a £527K growth in cash and a £188K increase in trade receivables, partially offset by a £282K decrease in plant and machinery. Total liabilities also increased during the year Due to a £408K growth in trade payables. The end result was a net tangible asset level of £25.4M, a growth of just £41K year on year.

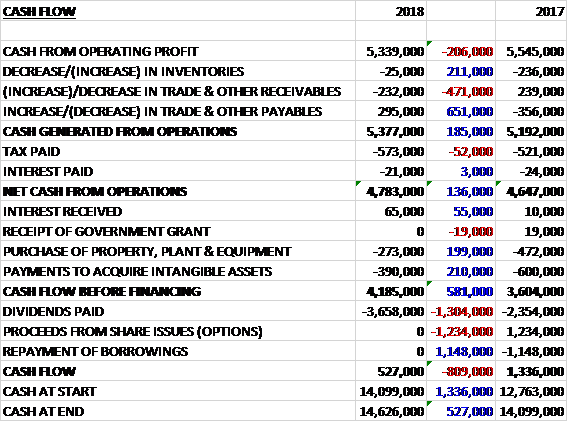

Before movements in working capital, cash profits declined

by £206K to £5.3M. There was a slight

cash inflow from working capital compared to a cash outflow last time and after

tax payments increased by £52K the net cash from operations was £4.8M, a growth

of £136K year on year. The group spent £273K on property, plant and equipment

along with £390K on intangible assets which meant that the free cash flow was

£4.2M. Of this, £3.7M was spent on

dividends which meant that the cash flow for the year was £527K and the cash

level at the year-end was £14.6M.

This year they continued to experience encouraging growth in

sales of their touchscreens to the gaming sector which somewhat offset the

decline in sales to financial markets.

The benefit of this growth was partly offset by lower margins, however,

principally from labour and material inefficiencies as new and different

products and methods associated with gaming replaced more familiar touchscreens

for the ATM sector.

The first half revenues were affected by the performance of

the financial market (ATMs) which at £2.8M was £1.1M lower than the prior

year. The second half performance was

also impacted by the financial market but to a lesser degree as the improvement

in the level of sales did not materialise as quickly as hoped. As a result, the total impact was £1.3M of

reduced financial sales for the full year composed of £900K of touch and £400K

of non-touch.

Within touch sales, gaming, which was dominated by

casino-based upright cabinet designs, has continued to be the top revenue

generating application market with growth of £500K. This growth reflects the maturation of

existing projects and new predominantly Asian PCT and MPCT projects which moved

into production.

Financial touch sales saw a decline on the back of total

unit volumes falling by 6,000 to 44,000 units.

The board believe that the decline has been down to several factors

which have generally been felt by the larger ATM OEMs in the market. These were an imposed change in the

procurement practices in China for the Chinese market, a slower than

anticipated change to the outsourcing of ATM assembly to third parties, and the

move by financial institutions to a Windows 10 operating system and consequent

delays caused in them placing new unit orders.

There is also little doubt that consumer digital money management may be

influencing future ATM deployment levels.

Vending continued to be their second highest market in terms

of units produced at 28,000 but this was 7,000 units lower than last year due

in the main to two factors, the finalised supply of the Freestyle Coca Cola

drinks machine and a reduced supply into German-based customers in the field of

parking management and fare collection.

In terms of revenue, it remained the third largest market but declined

by £500K.

The industrial market saw an 8,000 unit increase in sensors

sold to 24,000 units and an increase in revenues generated of £200K. The signage market increased by £400K on the

back of a 1,000 unit increase in large sensors sold to 2,000 units as the

number of smart city type street furniture deployments increased, particularly

for cities in the US which offer on the street internet, wayfinding and WIFI

hotspot capabilities.

The other markets which are predominantly in the small size

ranges and are open to much greater competition from alternative suppliers are

home automation, healthcare and telematics and sales declined by £200K. This reflects the units supplied to home

automation almost halving to 5,000 units, as the Bosch cooktop moves towards

end of design life and those supplied to health reduced by nearly two thirds to

just 1,000 units.

The group ended the year with twelve regional agreements

covering the Americas as they terminated the agreement with one underperforming

agent. Looking forward they are likely

to terminate a further three agencies but have already agreed terms with two

replacements Although previously stating

their intention to increase the US-based business, direct sale teams from two

to three, a decision was made to delay the recruitment. At the end of the period they had twelve agreements

covering the Asia Pacific region. During

the year they employed a further indirect employee in Japan and have been

working closely with a new VAR for Thailand which they should shortly expect to

sign an agreement with.

As of the year-end there was a pipeline of opportunities of

£8M compared to £8.2M at the end of last year.

Over the course of the year ZDL has been in dispute with a

former licensor, over the process used to write micro-fine wire to a

substrate. The licensor alleged that ZDL

owed it duties of confidentiality in relation to information alleged to have

been imparted to ZDL in 1999 and asserted that ZDL had breached that duty in

the content of its MPCT patent applications filed in 2012 and ZDL’s processes

infringed that a patent filed by the licensor in 2014 in response to the

alleged breach of duty.

A claim was made against ZDL through the patents court. While the group did not accept it was liable,

they took a commercial approach to dealing with the claim, mindful of the time

and cost associated with high court litigation they made an offer by which they

agreed to pay £72K in settlement of the claim, which was accepted with costs of

£25K.

Going forward revenues and trading are currently at similar

levels as last year and the focus will be to improve margins from production

efficiencies and to secure new projects from the launch of the new electronic

ASIC controllers.

At the current share price the shares are trading on a PE

ratio of 16.4 which falls to 14.7 on next year’s consensus forecast. After the final dividend remained the same

the shares are yielding 6.1% which grows to 6.7% on next year’s forecast.

Overall then, this has been a bit of a difficult year for

the group. Profits were down, net assets

were broadly flat and although the operating cash flow improved, this was due

to working capital movements and cash profits declined. There was still a decent amount of free cash

generated, however. The gaming market

seems to be going well, but the real problem has been the financial market

which has been beset by a number of one-off issues. There remains the fact, however, that ATM

usage is probably in structural decline.

This year has started off on similar levels to last year and although

the yield here at 6.7% is impressive, the shares are not overly cheap on a PE

level – 14.7. This is a quality, cash

generative business but there doesn’t seem to be any evidence of growth here at

the moment. Another tricky one, not sure

it is worth the gamble at the moment though.

Cambria have now released their final results for the year ended 2018.

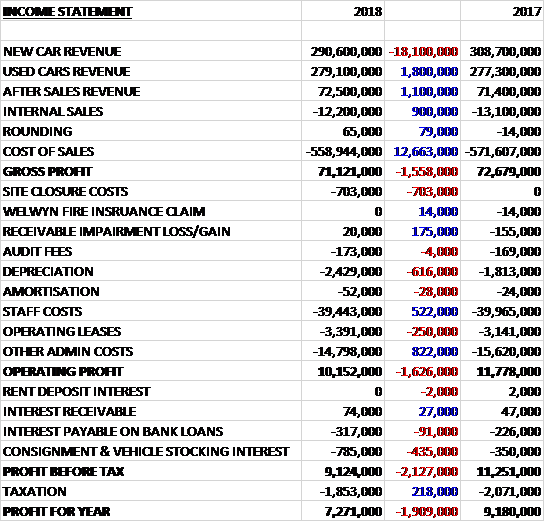

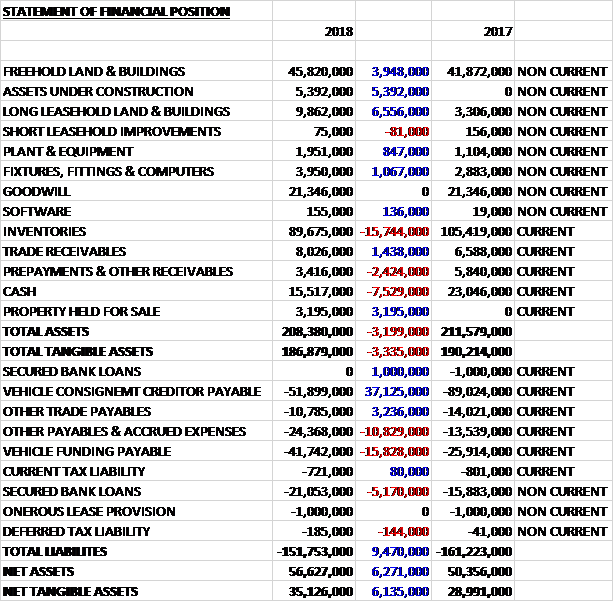

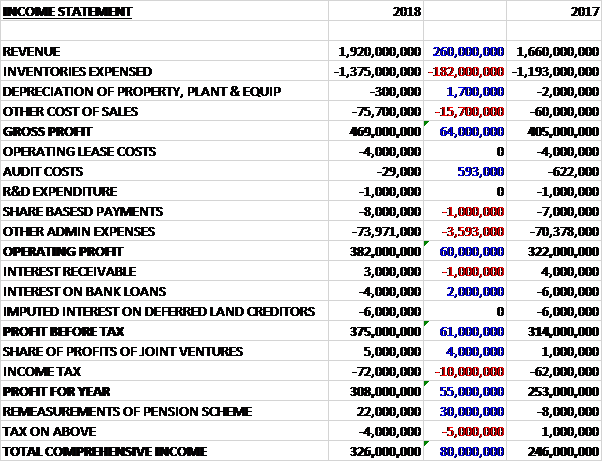

Revenues declined when compared to last year as a growth in after sales and used car revenue was more than offset by an £18.1M decline in new car revenue. Cost of sales declined by £12.7M to give a gross profit £1.6M lower. The group incurred site closure costs of £703K, operating lease payments were up £250K and depreciation increased by £616K, although staff costs declined by £522K and other admin costs were down £890K which meant that the operating profit was £1.6M lower. Consignment and vehicle stocking interest grew by £435K to give a profit of £7.3M, a decline of £1.9M year on year.

When compared to the end point of last year, total assets declined by £3.2M driven by a £15.7M decrease in inventories, a £7.5M fall in cash and a £2.4M decline in prepayments and other receivables, partially offset by a £6.6M growth in long leasehold land and buildings, a £5.4M growth in assets under construction, a £3.9M increase in freehold land and buildings and a £3.2M property held for sale. Total liabilities declined during the year as a £15.8M increase in vehicle funding payable, a £10.8M growth in other payables and accrued expenses and a £4.2M fall in secure bank loans were more than offset by a £37.1M decline in the vehicle consignment creditor payable and a £3.2M decrease in other trade payables. The end result was a net tangible asset level of £35.1M, a growth of £6.1M year on year.

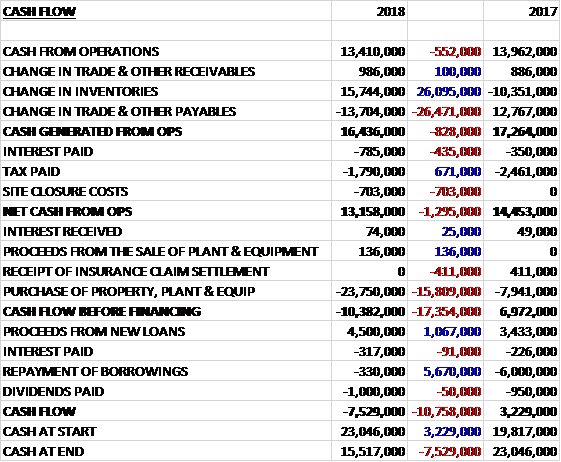

Before movements in working capital, cash profits declined

by £552K to £13.4M. There was a cash

inflow from working capital but this was slightly less than last time and after

interest payments increased by £435K, and the site closure costs of £703K were

slightly offset by a £671K reduction in tax payments, the net cash from

operations was £13.2M, a decline of £1.3M year on year. The group spent £23.8M on capex to give a

cash outflow of £10.4M before financing.

They took in £4.5M of new loans and spent £1M on dividends which meant

that there was a cash outflow of £7.5M in the year and a cash level of £15.5M

at the year-end.

Total funds invested in capex were £23.8M. The Swindon development incurred £6.6M to

complete the project, the Hatfield development £5.7M for the land purchase and

£5.4M on the development. The Chelmsford

and Tunbridge Wells property developments amounted to £1.9M. Including the fitout cost of Swindon and the

Tunbridge Wells and Chelmsford developments, there were fixtures, fittings,

plant and machinery additions of £3.7M and computer expenditure of £200K.

Over the coming two years the group intends to complete the

following major freehold investments:

Swindon land freehold purchase at £2.3M, Hatfield JLR, Aston Martin and

McLaren completion at £6M, and Solihull Aston Martin at £5M.

This year has seen a difficult new car market that has been

impacted by weakening consumer demand in the face of the uncertainty around the

Brexit negotiations, inconsistent messaging around the future of diesel engines

and the impact on car supply from the change in emissions testing regulations

in September. They have also had to cope

with the Government driven central cost increases including the Apprenticeship

Levy, pension contributions, increases in debit and credit charges and

increased property rating costs.

During the year, however, the group has delivered a

financial performance with profit slightly ahead of market expectations.

The gross profit in the new car business was £18M, a decline

of £3.3M year on year. Revenues

decreased by nearly 6% and sales volumes were down 17%. The reduced volumes were partly offset by an

improvement in the gross profit per unit sold which increased by 1.2%, a direct

reflection of strengthening mix from business additions.

The business has gone through a significant period of

disruption with the closure or development of eight of the group’s franchise

outlets which caused significant disruption in the day to day operations. The addition of two Lamborghini, two Bentley,

one McLaren and a Peugeot franchise will make a major contribution to growth

plans, however. The reduction in sales

volumes was attributable to reductions in unit sales from certain volume

manufacturer partners who have experienced significant reductions in national

registrations.

The group’s sales to private individuals was 17.3% lower,

new commercial vehicle sales improved by 2% and new fleet unit sales decreased

by 42%. The new vehicle registration

data showed total registrations were down 6.8% with the registration of cars to

private individuals down 4.7%. The sale

of diesel engine vehicles was hardest hit as a result of the negative media

coverage around diesel engine emissions and sales were down nearly 28%.

The gross profit in the used car business was £24.6M, an

increase of £1M when compared to last year.

Revenues increased by £1.8M but the number of units sold declined by

nearly 7%, partly driven by site closures.

The gross profit per unit sold increased by 11.6%. They have focused on increasing the

efficiency with which they source, prepare and market their used vehicles which

gave rise to a twelve month rolling return on used car investment of 125%,

slightly down from the 129% achieved last year.

The gross profit in the aftersales business was £28.5M, a

growth of £700K when compared to 2017.

Revenues increased by 1.5% with improved margins on the back of the

increase in labour hours sold. The 0-3

year car parc continues to be replenished as the increase in new car sales

experienced over the previous year’s produces cars ready for aftersales

operations, although this is obviously reducing.

To facilitate the development of the Chelmsford and

Tumbridge Wells Bentley and Lamborghini sites, the group closed two bodyshops

along with an Alfa Romeo and Jeep business in Chelmsford and a Honda and Mazda

business in Timbridge Wells. They took

the decision to close the loss making Blackburn site in July which comprised of

a leasehold showroom for Fiat and Alfa Romeo and the break clause has been

exercised. The Renault and Volvo

showrooms were owned freehold and are therefore held for sale currently.

The completion of the Swindon JLR facility in July on the

group’s long leasehold premises facilitated the relocation of Swindon Land

Rover from the property in Royal Wootton Bassett to the new facility. The Wootton Bassett site is now held for

sale. After the year-end the group has

secured the freehold title of the land in which the development sits from

Swindon Borough Council.

The major property development at Hatfield which is due to

complete in January 2019 will relocate the group’s JLR and Aston Martin

dealerships in Welwyn Garden City which currently operate in short leasehold

facilities into a purpose built freehold property with the addition of the

McLaren franchise which will operate on the same site.

During the year the Royal Wootton Bassett freehold property

was vacated following the transfer of the Land Rover business to the newly

developed site in Swindon so have been classified as held for sale. The same is the case for the freehold

property at Blackburn following the closure of that dealership.

The group have secured a new development site in Solihull

for a permanent facility in line with Aston Martin franchise standards. The group has exchanged contracts and

completion is subject to planning permission and the conclusion of extensive

highway works to define the site. It is

expected that the total freehold investment will be £5M. Due to delays in the highway works, it is now

expected that work to the dealership will begin in Q2 2019.

Going forward so far this year trading has been in line with

board expectations in September and October and that of last year, supported by

strong performances in their used car and aftersales operations. The new car market will see a further reduction

in 2018 with forecasts 11.5% lower.

There is little doubt that market sentiment has been impacted since the

Brexit vote. With the current weakness

in Sterling there is ongoing downward pressure on the number of cars registered

in the UK as the manufacturer landed cost of imported cars and components

increases. Diesel engine vehicles have

received the largest negative impact with a significant amount of negative

media coverage and clear political positioning in relation to diesel vehicle

emissions.

Whilst 2018 delivered a solid set of results, as a result of

the uncertainty in the economic outlook the board remains cautious about the

new car trading environment in 2019.

At the current share price the shares are trading on a PE

ratio 7.9 which falls to 7.4 on next year’s consensus forecast. After the dividend remained the same, the

shares are yielding 1.7% which increases to 1.8% next year. At the year-end the group had a net debt

position of £5.5M compared to a net cash position of £6.1M at the same point of

last year.

On the 4th January the group released a trading

update for the first quarter which was in line with board expectations and

ahead of the corresponding period last year.

As expected the new car market was significantly affected by the impact

of the changes in the emissions testing regime from September onwards and the

market was down 15.4%. Whilst this led

to a reduction in the group’s new vehicle sales, this was offset by improved

gross profit. New vehicle unit sales

were down 25% with the sale of new retail cars to private buyers down 19%. Some of the volume manufacturer franchises

experienced the largest reduction in sales.

The gross profit per unit improved significantly on a total

basis as a result the stronger mix from the new franchised outlets representing

Bentley, Lamborghini and McLaren. Group

profit per unit also improved on a like for like basis and the overall impact

of the improved profit per unit mitigated the reduction in unit sales.

Used vehicle sales continued to perform well. Whilst total

used unit sales were down 10.5% (like for like down 3%) this unit reduction was

offset by continued improvement in gross profit per unit. The significant changes in portfolio mix and

closure of the Blackburn site last year had a material impact on sales volumes

but as a result of the improved profit per unit, the like for like profit from

the division improved year on year. The

group’s aftersales operations delivered a good performance, with revenue

increasing by 1.9% and gross profit up 6.5%.

The group opened its second Lamborghini dealership in

November alongside the Bentley dealership in Tunbridge Wells. The major property development for JLR, Aston

Martin and McLaren at Hatfield is progressing well and the JLR facility was

completed for occupation in December as planned. It is now expected that the Aston Martin and

McLaren facility will be ready in February.

In December they completed the sale of the Wootton Bassett freehold

property for £2.8M.

The board remain cautious about the general uncertainty in

the economy and around the consumer environment, particularly the ongoing uncertainty

around Brexit. The new luxury franchises

and other redevelopments leaves the business well positioned for the year

ahead, however. All very non-committal!

Overall than this has been a difficult period for the

group. Profits were down, the operating

cash flow deteriorated with no free cash being generated, although next year

capex seems like it’s going to reduce. Net

assets did improve, however. There was a

lot of disruption from the investments being made but the real issue is a

declining market due to uncertainty over Brexit, weakening Sterling and the

issues surrounding diesel emissions.

Profits in used cars and aftersales offset the decline in new car

profits and the volume declines were offset by increases in unit profits due to

an improving mix.

One issue that I am concerned about is that the reduction in new car sales will at some point have a knock on effect on aftersales as less people have purchased cars and the debt levels are creeping up. Still, this is potentially priced in with a forward PE of 7.4 and yield of 1.8%. This is a tricky one, it could be an interesting value play but obviously not without risks as mentioned above.

On the 6th March the group released a trading

update covering the first five months of the year which was ahead of the same period

last year, both on a total and like for like basis.

During the period the new car market has been significantly

affected by a number of factors including the impact of the changes in the

emissions testing regime and the negative impact of the weak sterling position

on the imported price of the cars which has led to price increases for many

manufacturers. In the period, the total

new car market was down just over 10%.

The diesel segment of the market was worst hit, down 30%.

Supply side market influences have contributed to a

reduction in the group’s new vehicle sales, although this was partly offset by

improved gross profit per unit in the like for like businesses and fully offset

by the improved gross profit per unit across the total group as a result of the

stronger mix from the new Bentley, Lamborghini and McLaren outlets. New vehicle unit sales for the period were

down 23% (like for like 20%) although he prior year comparative included a low

margin commercial vehicle deal which has not been repeated. The sales of new retail cars to private

purchasers was down 16% (like for like 11%).

Used vehicle sales continued to perform well. Total used unit sales were down 11% (like for

like 4%) but this unit reduction was offset by an improvement in the gross

profit per unit. The significant changes

to the franchise portfolio mix and closure of the Blackburn site in the prior year

had a material impact on sales volumes but as a result of the improved profit

per unit, both the total and like for like profit from the business improved

year on year.

The group’s aftersales operations delivered a good

performance with revenue increasing by 7% (like for like 3%), gross profit up

4% (like for like 2%) and aftersales contribution up 10% (like for like 7%).

Going forward, whilst challenges remain given the ongoing

uncertainty around Brexit and the terms of the UK’s departure from the EU, the

group’s ongoing franchising development activities have enhanced their

dealership portfolio mix and the changed made in the prior year have further

benefited the group. These new

businesses are still in their infancy, but have exciting potential.

Redrow have now released their final results for the year ended 2018.

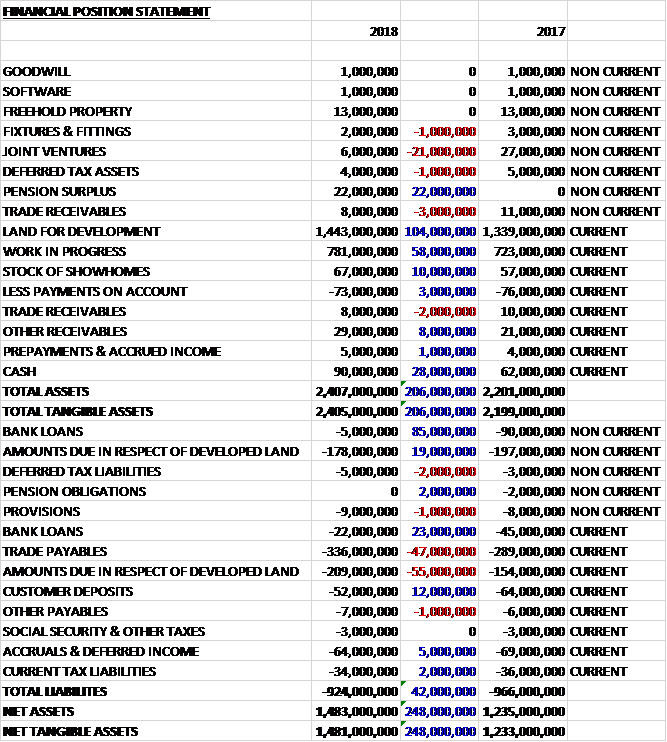

Revenues increased by £260M and after inventory expenses grew by £182M and other cost of sales were up £14M the gross profit was £64M higher. Share based payments increased by £1M and other admin expenses were up £3.6M to give an operating profit £60M higher. Interest costs fell by a net £1M, the profits from joint ventures increased by £4M but tax charges were up £10M which meant that the profit for the year was £308M, a growth of £55M year on year.

When compared to the end point of last year, total assets increased by £206M driven by a £104M growth in land for development, a £58M increase in work in progress, a £28M growth in cash, a £22M increase in the pension surplus and a £10M growth in the stock of show homes, partially offset by a £21M decline in the value of joint ventures. Total liabilities declined during the year as a £36M growth in the amounts due in respect of developed land and a £47M increase in trade payables were more than offset by a £107M decline in bank loans and a £12M decrease in customer deposits. The end result was a net tangible asset level of £1.481BN, a growth of £248M year on year.

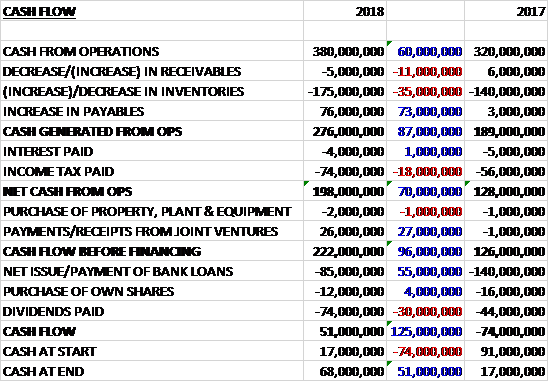

Before movements in working capital, cash profits increased

by £60M to £380M. There was a cash

outflow from working capital but this was lower than last time and after tax

payments increased by £18M the net cash from operations was £198M, a growth of

£70M year on year. The group spent £2M

on capex but received £26M in payments from joint ventures to give a free cash

flow of £222M. Of this, £85M was used to pay back bank loans, £74M on dividends

and £12M on share buy-backs. The end

result was a cash flow of £51M and a cash level of £68M at the year-end.

Group turnover rose by 16% as a result of the increase in

legal completions to 5,913 along with a 7% rise in the average selling price to

£332K. The increased selling price was

mainly due to the faster growth of the Southern business. With firm control to operating costs, operating

expenses as a percentage of turnover reduced from 5% to 4.5%.

Despite the uncertainty surrounding Brexit, demand for new

homes continued to be robust and overall house price inflation has moderated to

2%. With the exception of Central London

where they only have a handful of properties to sell, they continue to see

encouraging levels of demand for their homes.

The group entered the year coming year with an order book of £1.14BN, an

increase of £110M. Help to Buy continues

to support home buyers and the housing industry and in the last year, 1,794 of

private reservations were secured through the scheme (a similar amount to last

year).

During the year the group added 7,455 plots to their current

land holdings. Of these, 2,727 were

converted from their strategic land. As

a result, net of completions and re-plans, their current land holdings

increased by 1,530 plots to 27,630.

Their strategic land holdings also increased by a net 4,300 plots to

30,700. Growing the number of outlets in

line with the increased land holdings remains a challenge as the journey from

outline planning permission to implementable planning permission remains

bureaucratic. The gross development

value of their total land holdings now stands at £20M.

The new East Midlands division made its first full year

trading contribution and the Southern divisions continue to grow strongly as

they target increased market share.

Colindale Gardens in North London also made a significant contribution,

delivering its first completions. They

have announced the launch of a new division in Thames Valley and reorganised

their London operations into East and West to focus on growth in this

area. They have also restructured Harrow

Estates to help manage and support their forward land activities.

The land market remained attractive throughout the year,

they acquired 7,455 plots and increased to 27,630 plots in total, representing

4.8 years of supply. Pull through from

Forward Land accounted for 2,727 of the plot acquired. The average size of sites acquired was around

180 plots and the larger sites were generally acquired on more favourable

terms. The owned plot cost increased by

£1,000 per plot to £71K, reducing slightly to 19% of the average selling price

of legal completions.

The £24M improvement in the pension scheme is mainly due to

the increase in corporate bond yields along with a decrease in the market’s

long term expectations for inflation.

Going forward, demand for the group’s homes remains

strong. Despite Brexit and the

exceptional summer weather, sales revenue in the first nine weeks of the year

is in line with last year. They expect

to grow their land holdings and increase the number of average outlets by 5% to

130.

At the current share price the shares are trading on a PE

ratio of 6.7 which falls to 6.4 on next year’s consensus forecast. After a 65% increase in the full year dividend

the shares are yielding 5.1% which increases to 5.4% on next year’s

forecast. At the year-end, the group had

a net cash position of £63M compared to a net debt position of £73M at the end

of last year.

On the 7th November the group released a trading

update. For the first 18 weeks of the

year they have traded in line with expectations. They continue to see good demand in their

regional businesses with most sites sold well in advance. The London sales market has remained subdued,

however, affected by high stamp duty and Brexit uncertainty.

The value of net private reservations was in line with last

year at £588M. The average selling price

was up 4.6% to £388K but the sales rate per outlet reduced slightly entirely

due to the London market. The total

order book increased by 11% to £1.2BN.

The operational cash flow was strong with net cash currently standing at

£132M compared to a net debt position of £25M last year.

Overall then this has been a good year for the group. Profits increased, net assets grew and the

operating cash flow improved with plenty of free cash being generated. Both the number of completions and average

selling price improved, the land market remained good and outside London demand

remained strong. The issues in London

are a concern and of course Brexit looms large but with a forward PE of 6.4 and

yield of 5.4% these risks seem to be at least partly factored in and I think

the shares are looking decent value.

QinetiQ has now released their interim results for the year ending 2019.

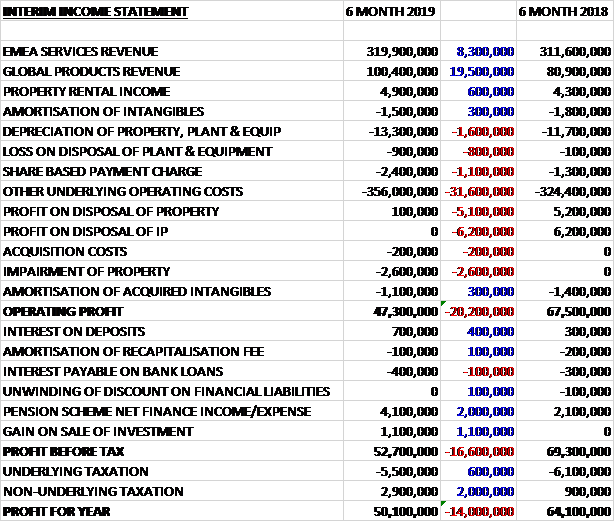

Revenues increased when compared to the first half of last year due to a £19.5M growth in global products revenue, an £8.3M increase in EMEA Services revenue and a £600K growth in property rental income. Depreciation was up £1.6M, share based payments increased by £1.1M and other underlying operating costs grew by £31.6M. We also see a £5.1M reduction in the profit on property disposals, a £6.2M fall in the profit of IP sales and a £2.6M property impairment which meant that the operating profit declined by £20.2M. Pension scheme income increased by £2M, there was a £1.1M gain on the sale of an investment and tax charges reduced by £2.6M due to a £2M increase in tax income related to share based payments, to give a profit for the period of £50.1M, a decline of £14M year on year.

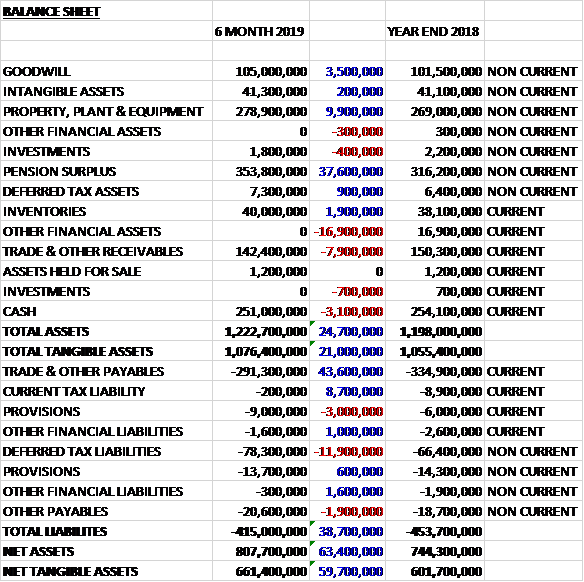

When compared to the end point of last year, total assets increased by £24.7M driven by a £37.6M increase in the pension surplus, a £9.9M growth in property, plant and equipment, a £3.5M increase in goodwill and a £1.9M growth in inventories, partially offset by a £16.9M reduction in other financial assets, a £7.9M fall in receivables and a £3.1M decrease in cash. Total liabilities declined during the period as an £11.9M increase in deferred tax liabilities and a £2.4M growth in provisions was more than offset by a £43.6M decline in payables and an £8.7M decrease in current tax liabilities. The end result was a net tangible asset level of £661.4M, a growth of £59.7M over the past six months.

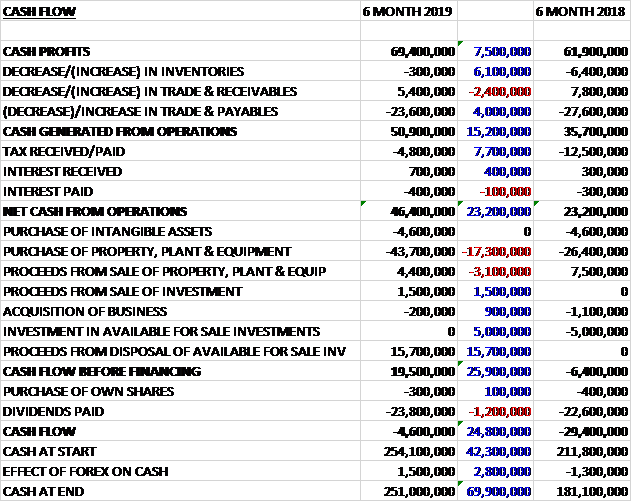

Before movements in working capital, cash profits increased

by £7.5M to £69.4M. There was a cash

outflow from working capital but this was less than last time and after tax

payments declined by £7.7M the net cash from operations was £46.4M. The group spent £43.7M on property, plant and

equipment along with £4.6M on intangible assets but they recouped £15.7M from

the sale of an available for sale investment, £4.4M from the sale of fixed

assets and £1.5M from the sale of an investment to give a free cash flow of

£19.5M. This didn’t cover the £23.8M

paid out in dividends so there was a cash outflow of £4.6M and a cash level of

£251M at the period-end.

After adjusting for non-recurring items, the group reported

stable underlying operating profit in line with expectations. They have been able to offset margin pressure

in EMEA Services through efficiency savings and revenue growth.

The operating profit in the EMEA Services division was

£40.9M, a decline of £6.4M year on year due to a £6.5M benefit from

non-recurring items last year. Excluding

this, profits were broadly flat as the SSRO margin pressure was offset by

efficiency improvements and revenue increases.

There was a £42.2M increase in orders, primarily due to greater volumes

of small value orders in maritime, land and weapons, and cyber, information and

training following greater UK MOD commitments during the period.

Within the air and space business a key success has been

winning the Engineering Delivery Partner framework contract with the MOD. This was signed in early October and covers

the provision of all engineering services to DE&S, the MOD’s procurement

body. The team consists of QinetiQ,

Atkins and BMT and will lead the provision of engineering services with the aim

of providing improved performance at reduced cost.

The group continue to add services to their Strategic

Enterprise contract. During the period

they added work for Chinook and Typhoon mission systems assurance. The deployment of their test aircrew training

is progressing well. Their new fleet of

aircraft are all being delivered to schedule and they are complementing their

new fleet with a modernised syllabus.

The Solar Electric Propulsion System will provide the engine power

behind the BepiColombo mission to Mercury with the spacecraft due to start its

transit in December 2018 with the group continuing to provide ground based

testing to support the mission.

Within the maritime, land and weapons business the group’s

investment in the MOD Aberporth air range will enable the first live weapon

firing in the UK from the RAF’s new F35 Lightning II aircraft later this year

which creates a potential opportunity for the group as the UK and other

European nations assure new fleets of this aircraft. Improvements to the MOD Hebrides range will

enable them to host Formidable Shield 2019 and deliver scenarios that combine

traditional weapons with complex electronic warfare trials.

In addition to missile firings for a new Polish customer and

further work from the German armed forces, the group have also hosted

commanders from the UK Carrier Strike Group and the US Marine Corps as they

prepare to deploy the new Queen Elizabeth class aircraft carriers. Shortly after the period-end they were

awarded a £9M extension to the Naval Combat System Integrated Support Services

contract to cover mission systems on the new UK QE class aircraft carriers.

In the cyber, information and training business the group

were awarded a three year contract with options to extend for a further two

years, worth up to £95M to support the UK MOD in delivering next generation

battlefield tactical communications and information systems. They were also awarded a £7M contract to

assure the Falkland Islands Ground Based Air Defence systems. As part of this they will build and maintain

a synthetic environment for testing the Sky Sabre 3D radar surveillance systems

used by GBAD and provide the support for live fire testing.

The business in Australia continues to perform well,

delivering organic revenue and order growth supported by a number of contract

extensions within the professional services business. The group are in a consortium, led by Nova

Systems, that has been selected as one of only four major service providers

through which the Australian government procured defence capabilities. They expect their involvement in this to

drive further growth in the business. Building

on their UK work on the new QE aircraft carrier, they were selected by Oman to

deliver ship helicopter operating limit trials ahead of a Royal Navy and Omani

Navy exercise. This is the first time

they have delivered such trials for an international customer.

The operating profit in the Global Products division was

£10.2M, flat year on year. Orders fell

by £20.4M against a strong comparator which included a number of significant

multi-year contracts, notably the €24.2M spacecraft docking mechanism order

with the ESA. Revenues were up 24%

driven by an £8.9M increase in QinetiQ North America due to robotic,

survivability and maritime product programmes and £6.5M QTS Banshee target

sales to India. At the start of the

second half the division had 86% of its full year revenue under contract

compared to 80% the year before. The

reduction in margins was the result of timing and mix of product sales during

this period, in particular lower license income couple with lower profitability

in OptaSense. Full year margins are

expected to be in line with previous years.

The North American business was awarded the Route Clearance

and Interrogation System robotics programme of record. This contract with a potential value of up to

$44M is for larger vehicles. They also

secured a contract to convert large army vehicles into ones capable of remote

operation. The broader robotics

portfolio continues to perform well including continued demand to upgrade,

repair and service the Talon product range. They have been selected as one of

two suppliers for the Engineering and Manufacturing development phase of the

Common Robotic System programme of record.

The EMD will last around ten months, during which time the US DoD will

test and evaluate robots from the two suppliers. The total budget for the programme is $429M

in the form of an indefinite delivery and quantity contract over seven years.

They also secured a strategic milestone with an order for

their Dolphin underwater acoustic networking product. This technology allows for full duplex

underwater acoustic networking with many potential applications. Demand for light weight and cost effective

survivability products such as Q-Nets and Last Armor was also strong.

In the OptaSense business the group were awarded the

contract to protect a new pipeline for the Permian Basin in Western Texas. They will provide monitoring of the pipeline,

including leak detection. They have

continued to develop the technology, increasing the effective range of each

sensor by around five times whilst also enhancing the sensitivity. This further supports their offering for long

distance linear assets such as roads, railways and national borders. They have delivered Phase O of the 1,841km

Trans Anatolian Natural Gas Pipeline project, the largest single system award

for the business.

In the Space Products business, the group won a two year

contract with Effective Space Solutions to test and deliver docking mechanisms

for two satellite servicing space drone spacecraft. The mechanism will provide a non-intrusive,

safe and secure attachment between the spacecraft and existing satellites in

ordbit.

In the EMEA Products business QinetiQ Target Systems

continued to deliver good growth and agreed a framework contract with the US

Target Management Office. In addition

they completed the first deliveries of targets to the Indian Army and

Navy. They have launched their secure

satellite communication product Bracer and have seen positive early interest. The product allows for secure but cost