Bonmarche has now released their final results for the year ended 2018.

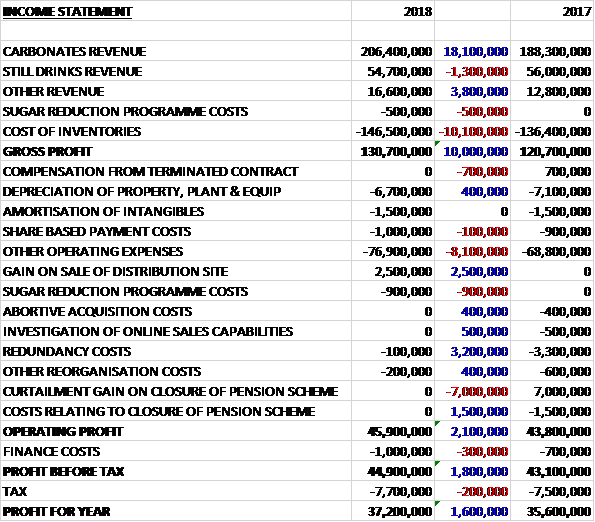

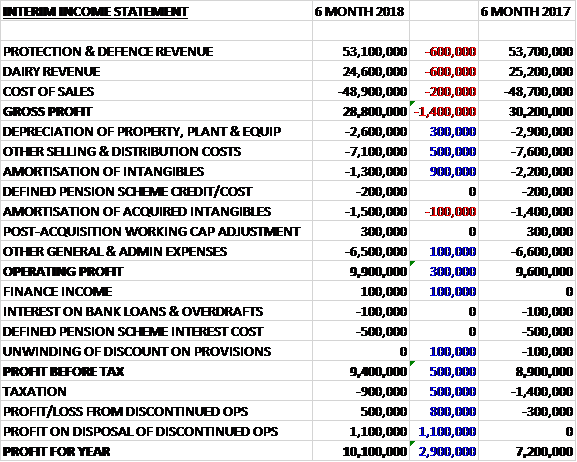

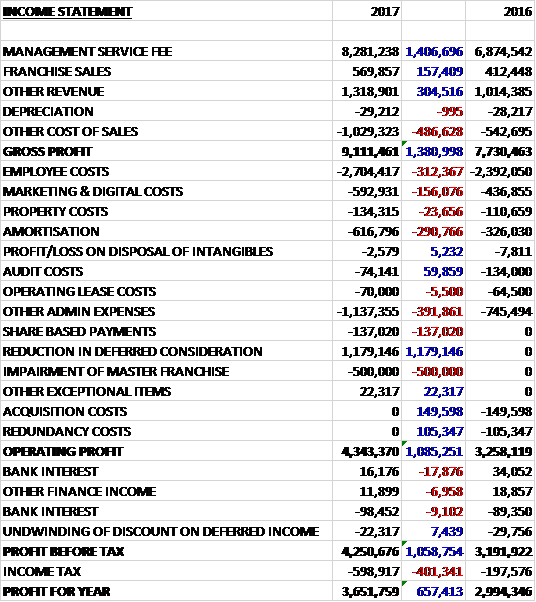

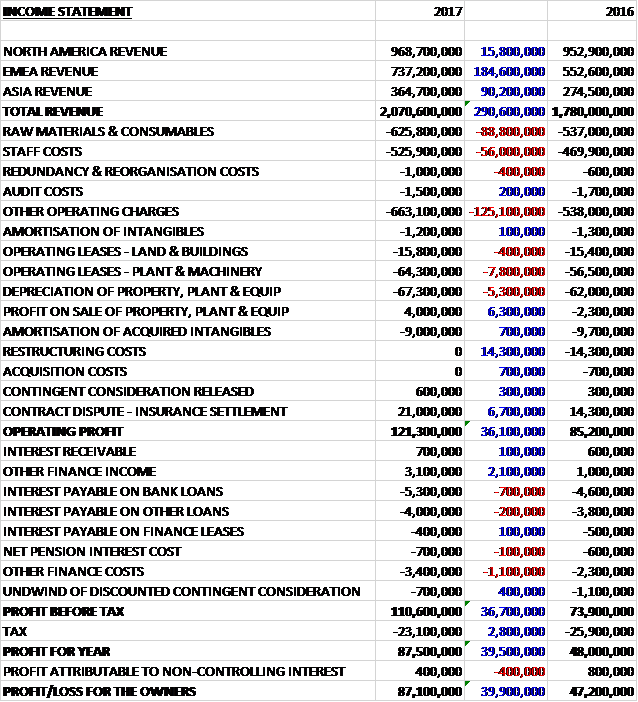

Revenue decreased by £4.1M when compared to last year. Depreciation was up £723K and amortisation increased by £432 but other cost of sales decreased by £3.4M to give a gross profit £2.2M lower than last year. There was a £1.1M positive movement to a gain on disposal of fixed assets, nothing was spent on implementing the new EPOS system, which cost £417K last time, and other admin expenses were down £2.1M. In addition, distribution costs fell by £556K which meant that the operating profit was £2.2M higher. After tax charges increased by £290K the profit for the year came in at £6.3M, a growth of £1.9M year on year.

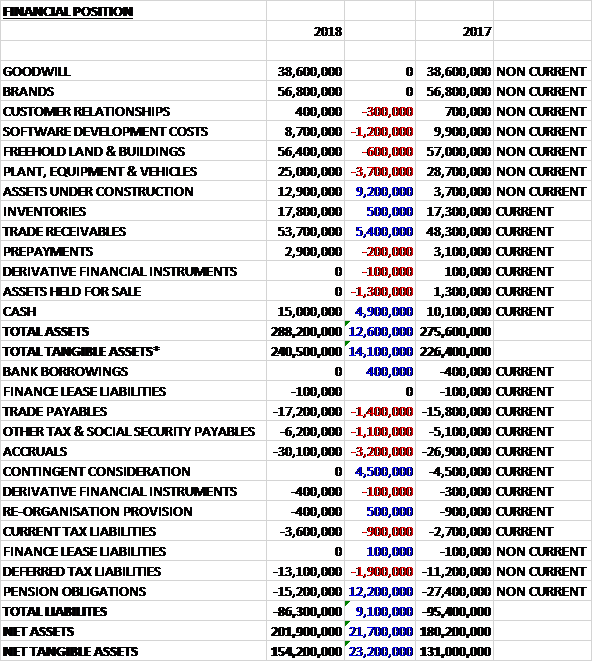

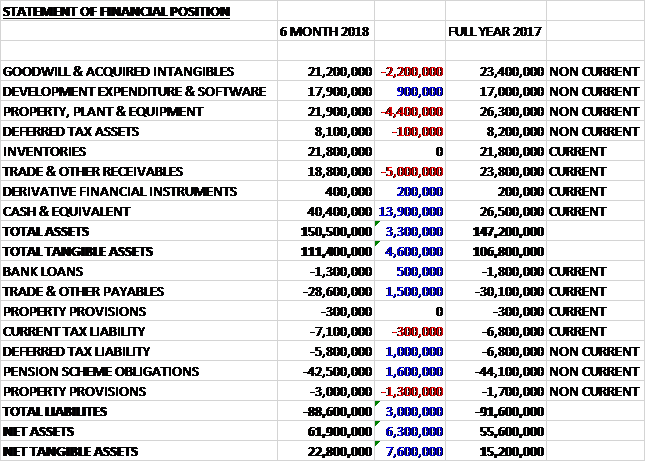

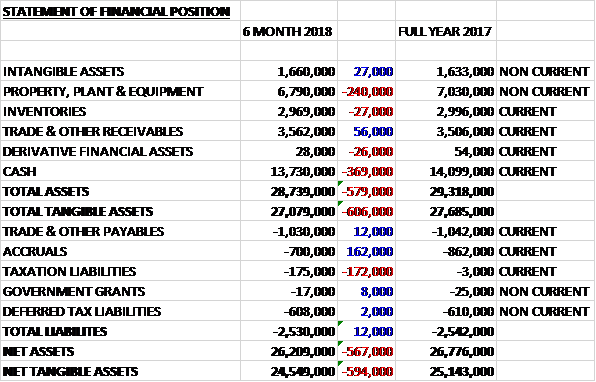

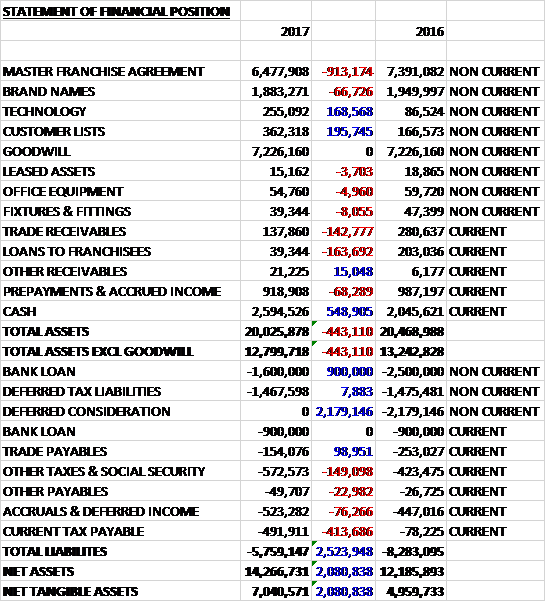

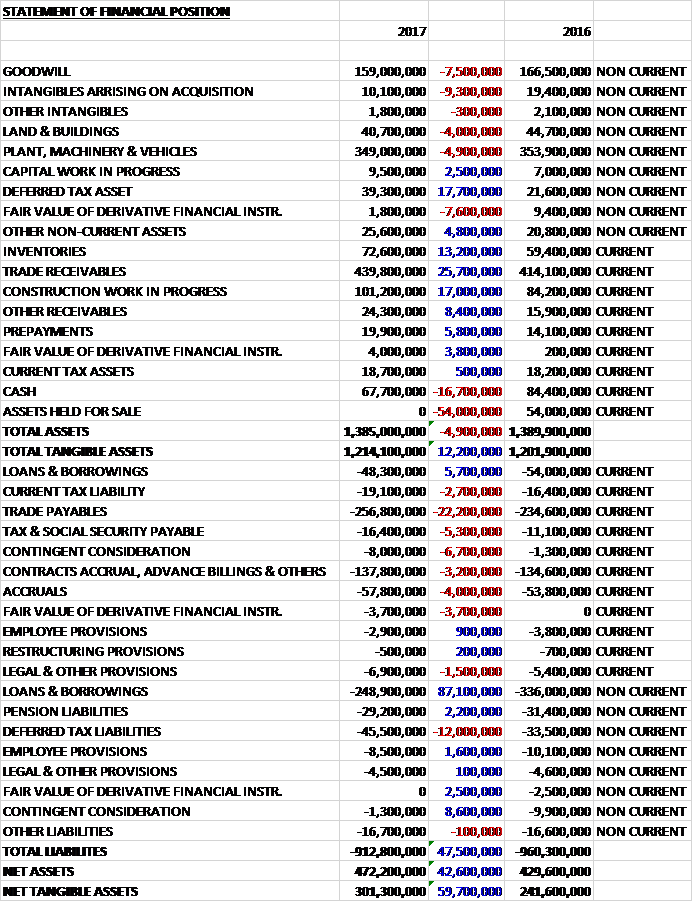

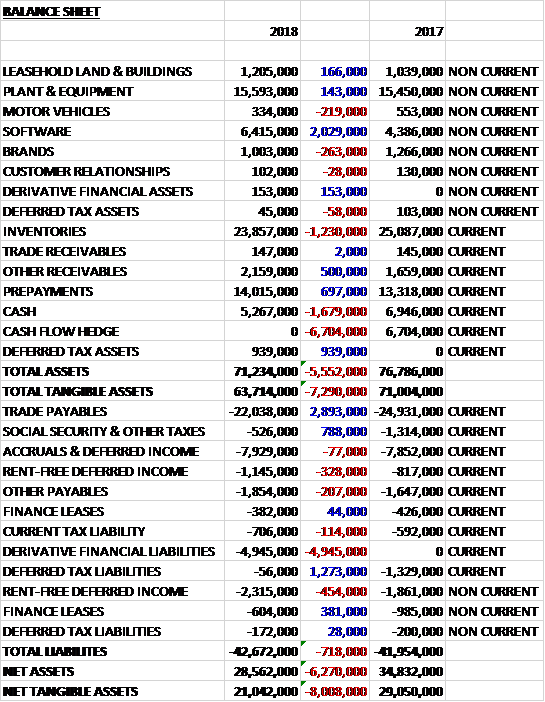

When compared to the end point of last year, total assets declined by £5.6M driven by a £6.7M reduction in the value of the cash flow hedge, a £1.7M fall in cash levels and a £1.3M decrease in inventories, partially offset by a £2M growth in the value of software. Total liabilities increased during the period was a £2.9M decline in trade payables and a £1.3M decrease in deferred tax liabilities was more than offset by a £5M growth in derivative financial liabilities.

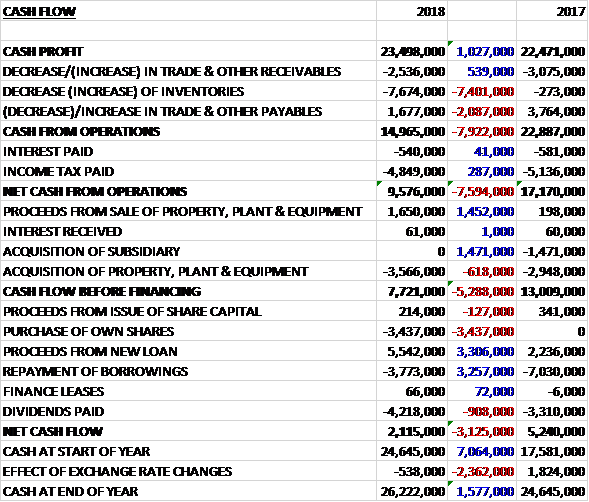

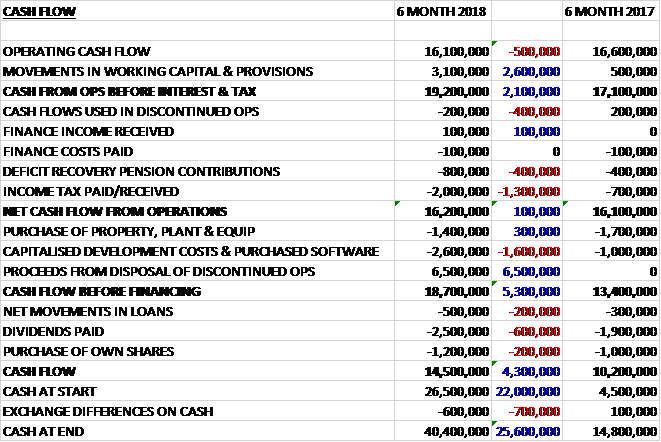

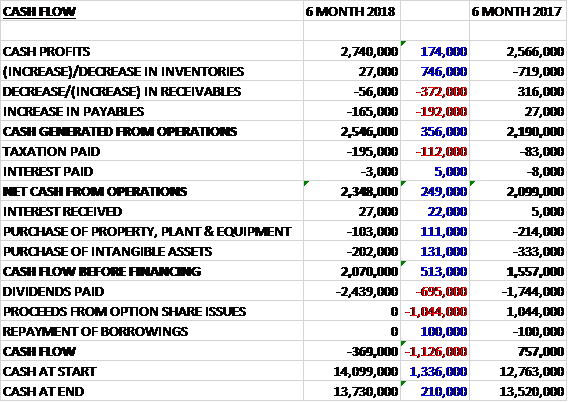

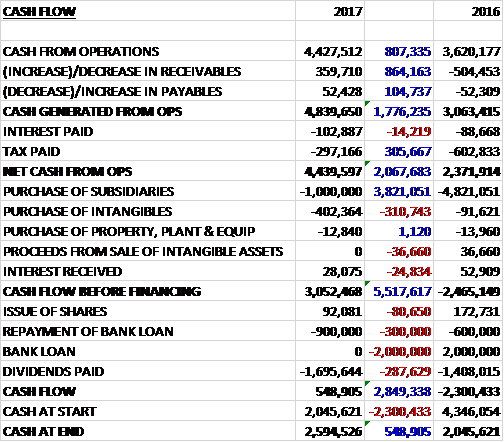

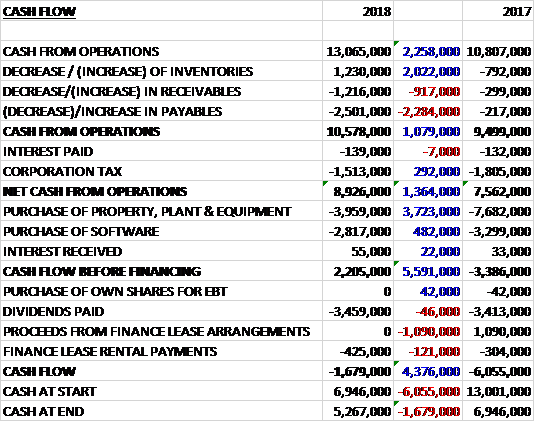

Before movements in working capital, cash profits increased by £2.3M to £13.1M. There was a cash outflow from working capital and after tax payments fell by £292K the net cash from operations came in at £8.9M, a growth of £1.4M year on year. The group spent £4M on property, plant and equipment along with £2.8M on software to give a free cash flow of £2.2M. This did not cover the £3.5M paid out in dividends or the £425K finance lease payments so there was a cash outflow of £1.7M and a cash level of £5.3M at the year-end.

Overall, whilst the high street challenges continued, online sales were more resilient due to the evolution of the group’s customers’ shopping habits and the improvements made to the online store. Overall demand was stronger during the first half and fell back noticeably and remained weak during autumn and winter.

Total sales for the year declined slightly (0.5%) but the gross margin was resilient in the face of adverse forex movements, mitigated through tight stock control and improvements to the loyalty scheme which led to lower discounting. Through improved operational efficiency and reduced market expenditure the group made some overhead cost savings.

Total like for like store sales declined by 4.5% year on year. The store like for like was strong in Q1 and September but weakened significantly in the second half of the year.

Total online sales increased by 34.5% when compared to last year and in the second half, when store sales were poor, online sales maintained a 30% growth rate against stronger H2 comparisons last year. Many improvements have been made to the online store which has led to a much better shopping experience and increased sales. Profitability has also improved, mainly due to more efficient marketing.

Key priorities for next year include introducing online exclusive ranges and brands to enhance the offer, improving online content, improving the checkout process, making the interaction between online and stores more seamless, and improving the delivery options for customers.

The devaluation of the pound against the dollar had a negative effect on margins but the decline this year was smaller than expected. The hedging policy has delayed the impact of the currency fluctuations but there will be a further negative impact in 2019 as hedges put into place this year mature.

The higher than expected margin was mainly due to a reduction in discounting compared to last year. This was achieved from a combination of factors. They bought a lower proportion of stock in advance of the selling season; there was a more agile buying approach, discounts given to loyalty club holders were more targeted and the promotional calendar was made more flexible.

Marketing costs were significantly lower than last year when around £1M was spent on a national TV advertising campaign which was not repeated. Some of the saving was spent in other forms of offline marketing such as the catalogues but some flowed through to the bottom line. Online marketing costs were also lower following the appointment of a new digital marketing agency and better management by the online team.

Denim was relaunched in all stores following a trial and this new range achieved a 50% increase in sales compared to the previous equivalent. Other highlight performances included leisurewear, driven by improved fabric quality and the introduction of stretch fabrics; casual blouses designed to complement the new denim offer; and swimwear due to improved fit. The discontinuation of peripheral product categories such as Ann Harvey menswear during the year have enabled better use of space.

There are still areas of the product proposition where there is scope to improve. The performance during the winter season on knitwear was poor as the ranges lacked enough warmer weight knitwear and they under estimated the extent to which their customers would choose separates and more versatile products that could be worn several ways, over traditional dresses and party wear categories which consequently sold poorly.

The focus of attention in the future will be on product categories in which the market share under-indexes the market, for example coats, and leisurewear, in respect of which there are further opportunities despite the strong performance this autumn. They under index in dresses which is the most searched for online category and they have identified the opportunity to improve their proposition, including the introduction of styles exclusively available online.

Going forward, whilst the board expect the market to remain difficult, trading since the beginning of the year has been stronger than in the second half of last year, and is in line with their expectations. The group will continue to improve their proposition through the implementation of a series of self-help initiatives which should make a difference to customers.

At the year-end the group had a net cash position of £4.3M compared to £5.5M at the end of last year. At the current share price the shares are trading on a PE ratio of 8.9 which falls to 7.8 on next year’s consensus forecast. After an 8.5% increase in the total dividend the shares are yielding 6.9%, increasing to 7.2% on next year’s forecast.

On the 26th July the group released a trading update covering Q1 of this year. Sales grew by 2.7%. Online sales were up 27.3% and store like for like sales were down 1.2%. Overall the board’s expectations for the full year remain unchanged.

Overall then this has been a bit of a mixed year for the group. Profits did increase marginally due to lower costs, mainly in relation to less discounting. Net assets declined and although the operating cash flow improved, there was still not enough cash to cover the dividends. During the year, online sales have been good but store sales have been poor, although this seems to be more of an industry-wide issue than anything specific to the group. The shares still look cheap, with a forward PE of 7.8 and yield (possibly unsustainable) of 7.2%. I am tempted to get back in here.

On the 27th September the group released a trading update covering the first half of the year. During Q2 online sales have continued to grow strongly in line with expectations but sales in the stores have not maintained their momentum gained during Q1 and are below expectations. The continuation of warm weather for an extended period may have delayed demand for early autumn stock but the board believe that the more dominant factor is that underlying consumer demand for the UK high street is weaker, impacting footfall.

In light of the recent downturn in store trading, the board has reviewed their forecasts for the rest of 2019. Online sales are expected to grow at least at the rate seen recently through improvements to the online shopping experience and the extension of online exclusive ranges. Due to the uncertainty regarding high street footfall, they believe it prudent to reduce the store sales forecast for the second half of the year. Planned group discretionary operating expenditure for the balance of the year has been reviewed and reduced where appropriate. As a result of these changes the underlying pre-tax profit for 2019 is now expected to be £5.5M compared to £8M last year.

The revision to the forecast also requires an increase in the provision for impairment of store fixed assets. All central overhead costs are now required to be allocated to stores which results in an increase in the provision of around £1M.

The board’s intention at this time is that the total dividend in respect of 2019 will be maintained at 7.75p per share, in line with 2018.