Gemfields have now released their interim results for the year ending 2015.

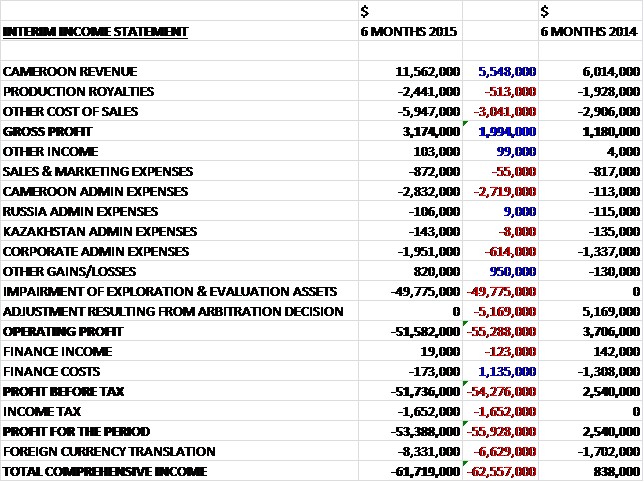

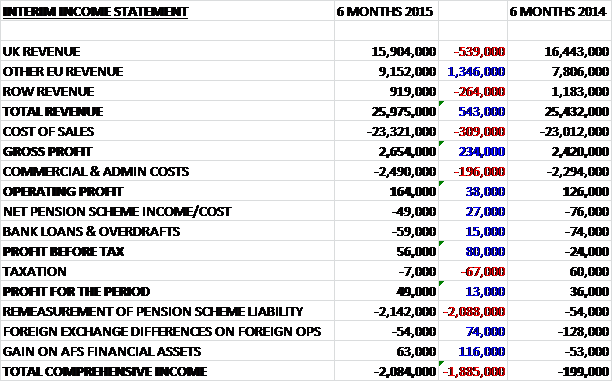

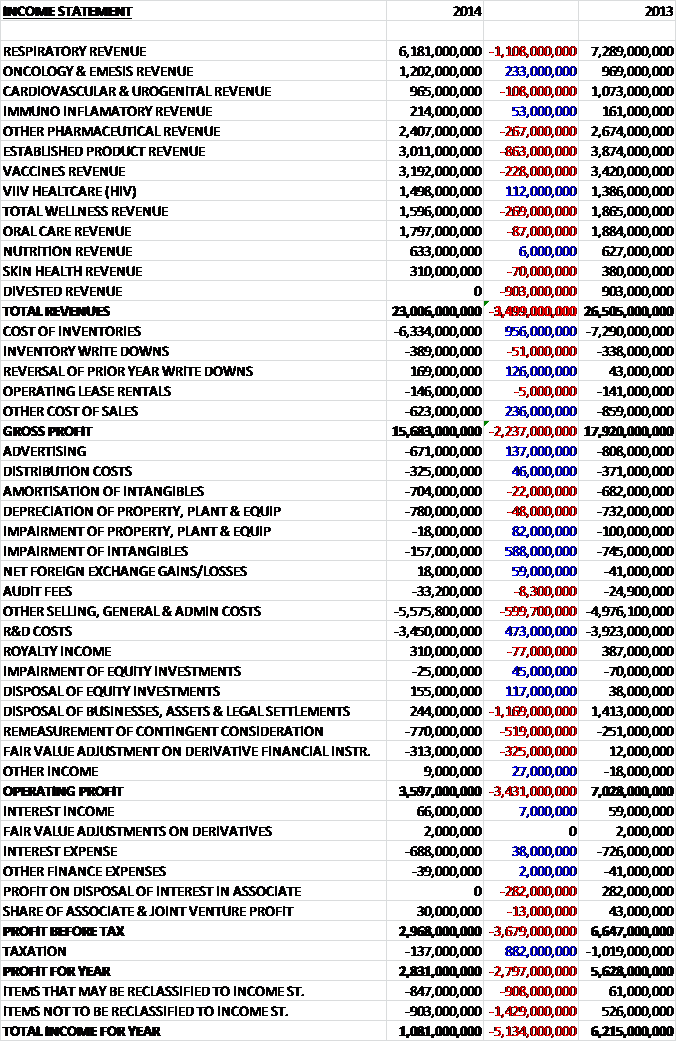

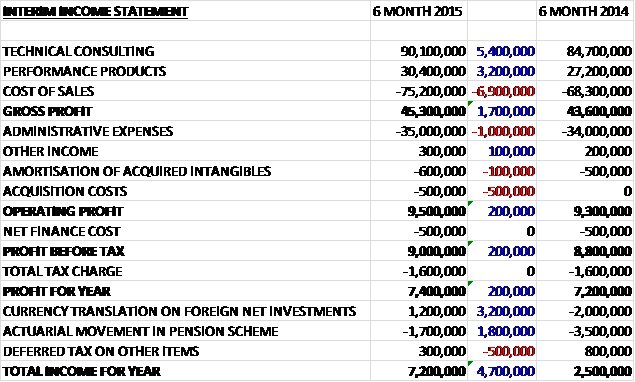

When compared to the first half of last year, revenues romped ahead, increasing by $37.7M to $103.4M. We also saw a $7.2M increase in depreciation & amortisation, a $4.1M growth in mineral royalties & production taxes, a $1.8M increase in fuel costs and a $936K growth in repairs and maintenance. This was all counteracted by a $20.1M change in inventory, however, to give a gross profit some $39.7M higher at $67.8M. We then see a near $4M increase in staff costs and a $1.2M increase in professional costs, partially mitigated by lower selling and advertising costs to give an operating profit $36.6M higher than in the first half of 2014 before an $882K increase in finance costs and a huge $13.9M hike in tax meant that the profit for the period was $21.8M higher at $23.2M, $16.3M of which was attributable to owners of the company.

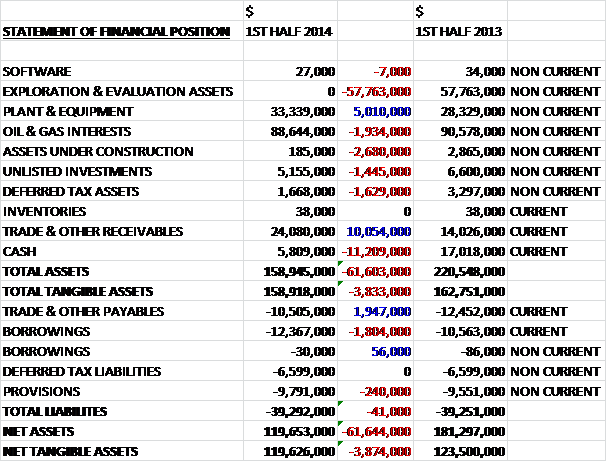

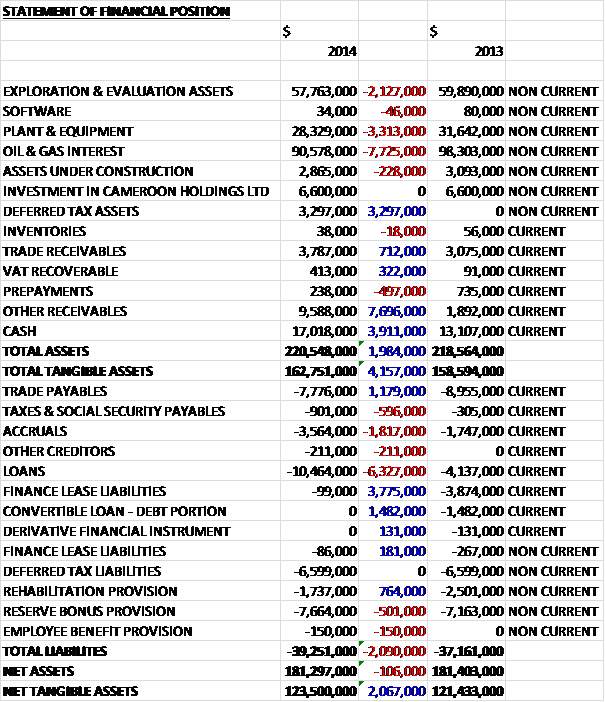

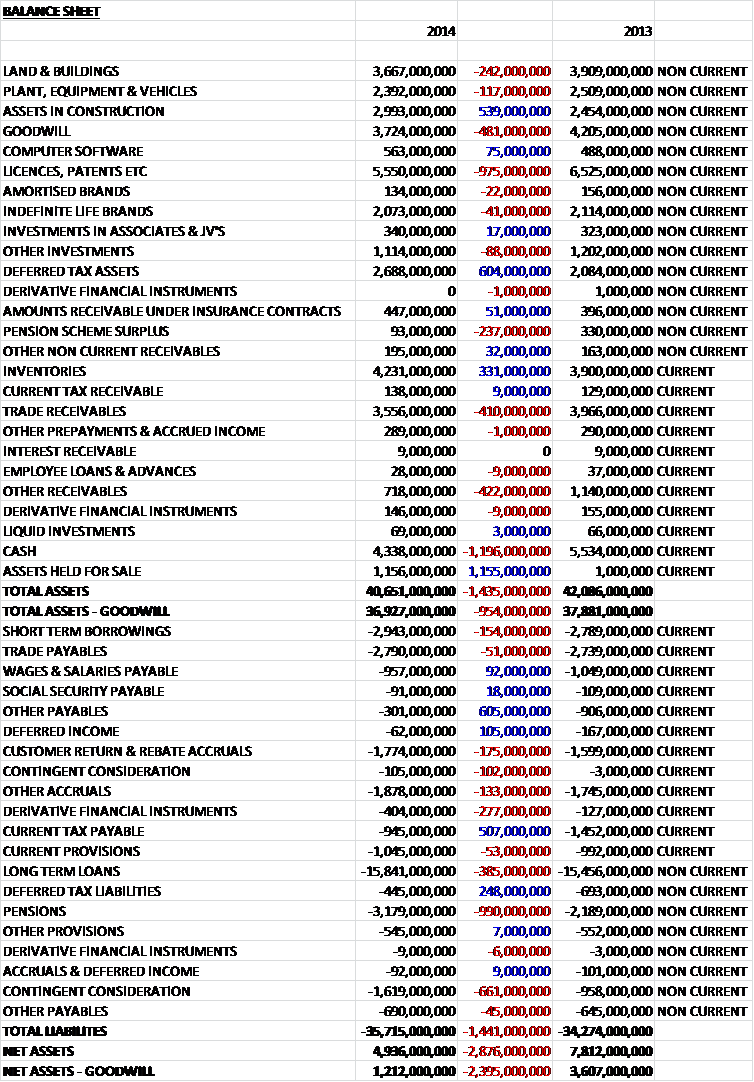

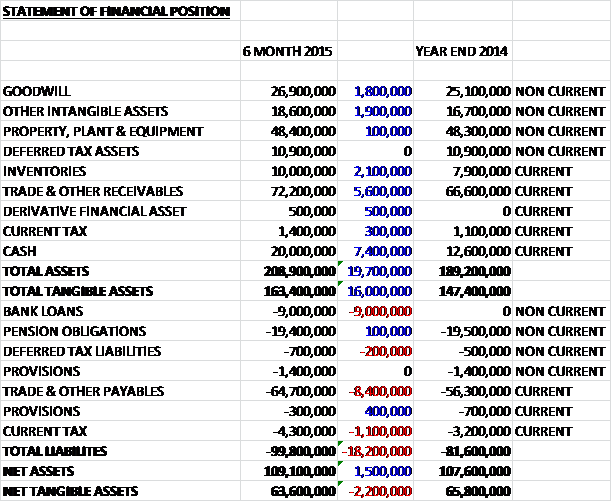

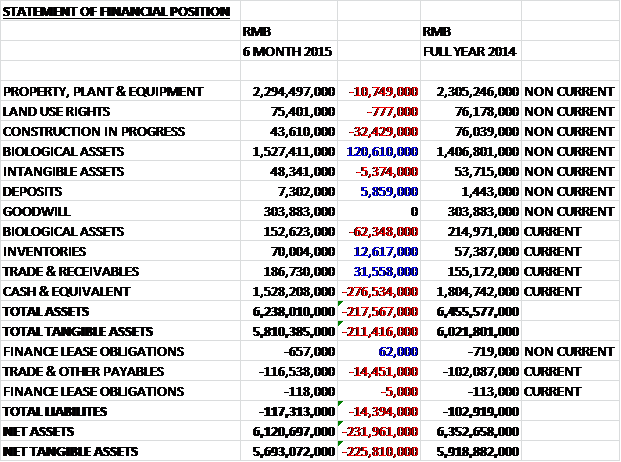

When compared to the end point of last year, total assets increased by $44.4M to $471.1M driven by a $12.8M increase in cash levels, a $12.7M growth in inventories, presumably due the large number of unsold Emeralds from the last auction, a $10.8M increase in property, plant & equipment, a $4.4M increase in “other” non-current assets and a $4.2M growth in intangible assets, only partially offset by a $1.3M decline in deferred tax assets. Liabilities also increased during the period with a $13.3M increase in borrowings and a net $11.6M growth in tax liabilities, partially offset by a $3.9M reduction in trade & other payables. This gives a $19.7M increase in net tangible assets to $267.4M which seems pretty strong to me.

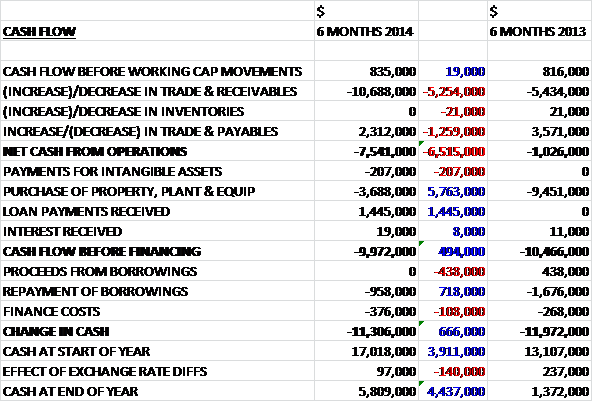

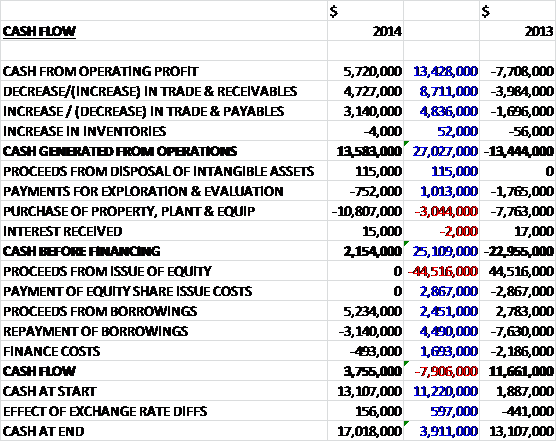

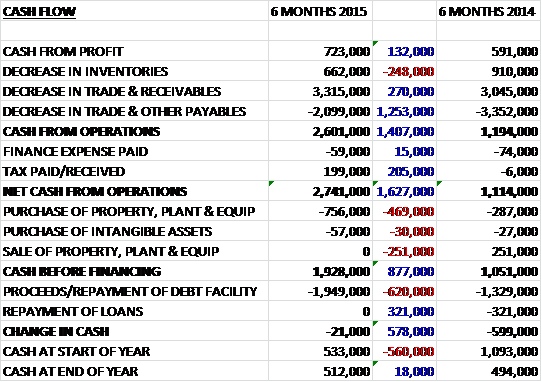

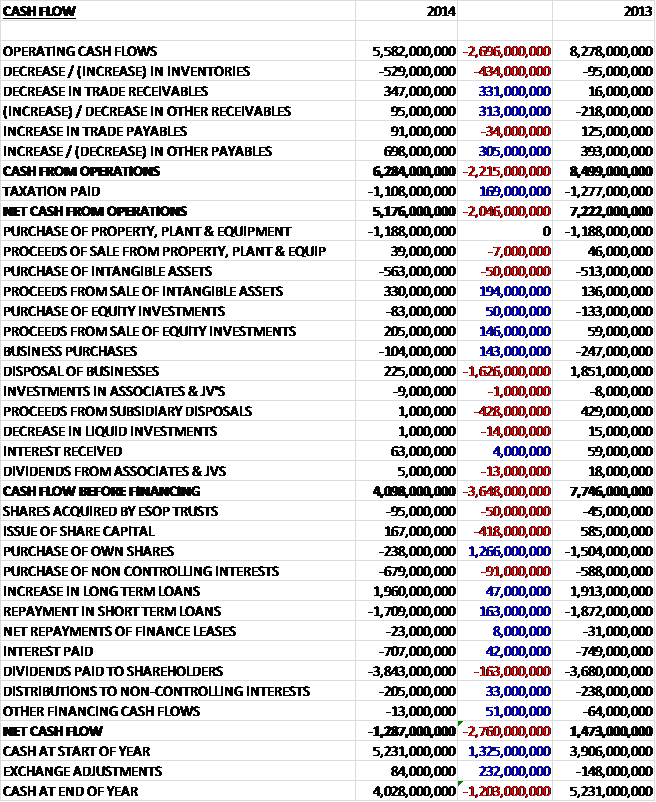

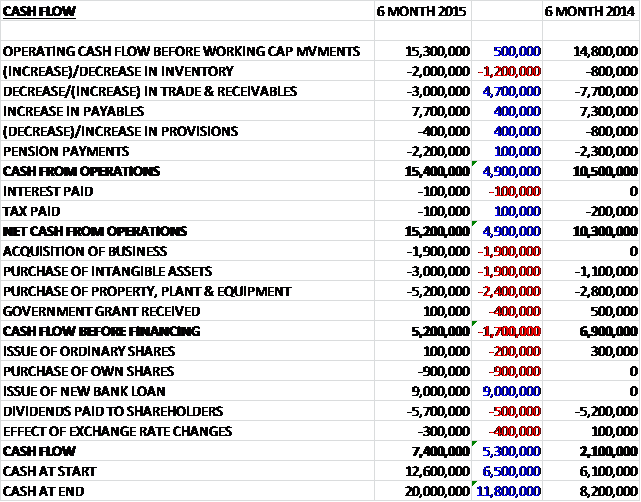

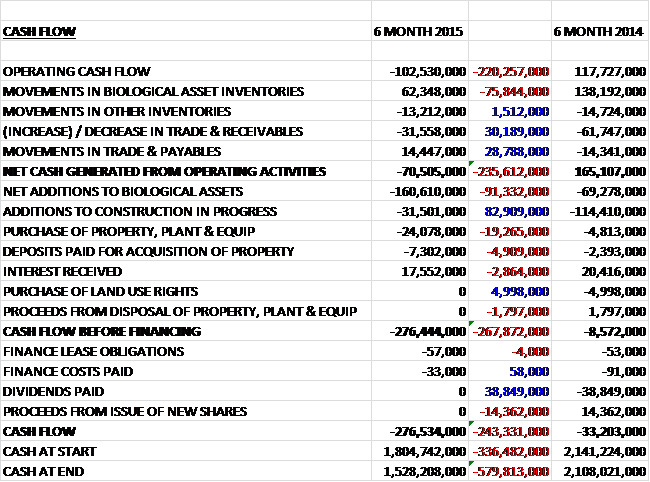

Before movements in working capital, cash profits increased by an impressive $42.6M when compared to the first half of last year, before a large increase in inventories, along with a smaller growth in payables meant that cash from operations was a more modest $23.3M higher at $43.7M before the tax bill dragged this down to $36.3M, a $17.9M increase. The group spent the bulk of this on property plant and equipment ($17.3M, with $6.1M being spent at Montepuez) with another $10.2M being spent on stripping costs and $4.4M each being spent on intangible assets and new loans granted. The upshot of this is that cash flow before financing was just $347K, albeit an $8.3M improvement on last time. There was then interest to pay of $1.3M with a net $13.6M increase in borrowings meaning that the cash flow was $12.7M to give a total of just under $50M at the end of the period. This is a decent cash pile but there is certainly no room to squeeze any shareholder returns into that.

At the Kagem Emerald mine in Zambia, significant progress was made on the fourth high wall pushback during the period which will extend the Chama pit by a further 75 metres. More than 7.3MT of waste rock was removed and the 17 month stripping programme is currently running ahead of the original targeted completion date of September 2015. During the first half of the year, $11.2M was invested in new mining equipment to support the scale of operations at the Channa pit as well as accelerating bulk sampling of the Libwente and Fibolele pits. During the first half of the year the mine produced 12.1M carats at a grade of 202 carats per tonne compared to 10.4M carats at 267 carats per tonne produced during the same period of last year. The gemstone deposit has a fairly considerable grade fluctuation and the overall grade was also impacted by the dilutive effect of the bulk sampling work being carried out at the Fibolele and Libwente pits. Total operating costs were $1.81 per carat compared to $1.38 per carat last time round which reflects the pit expansion operations. Cash rock handling unit costs fell to $2.92 per tonne from $3.52 per tonne, however, with the increased scale of mining operations delivering improved efficiencies.

The trial underground mining project at Kagem was placed on hold towards the end of the period as the continued viability of open pit operations, supported by robust emerald prices and the flexibility of extending the open pit operations as required, has negated the need for accelerated underground operations at this time. Kagem increased its processing efficiencies following an upgrade of the washing plant facility and the associated security arrangements. A climate controlled environment was also established within the picking belt facility which resulted in an improved working environment and better operating controls which helped lead to fewer breakdowns, reduced maintenance costs and more efficient gemstone recoveries.

The Libwente South Pit in the Kagem license was one of two bulk sampling projects at the mine and has recently been expanded in scale with the current project expected to handle 1.9MT of rock to produce 41,000 tonnes of reaction zone ore. The core drilling continued to extend to the TMS outline to identify additional prospective TMS resources in the area which resulted in the delineation of another bulk sampling pit targeting a shallow TMS body of depths between 6 and 24 metres with an average thickness of 16 metres. Gemstone production from bulk sampling at the Fibolele pit also increased during the period, mainly due to the increased width of the TMS being mined and yielded considerably improved grades which bodes well for the remainder of the Fibolele TMS belt. A third bulk sampling phase has now been planned at the pit which will increase the pit size to 590 metres in length and 50 metres in depth.

There were two Emerald auctions held during the period. In August an auction was held of lower quality emerald in Zambia that generated revenues of $15.5M at an average price of $3.61 per carat ($1.34 per carat if the Beryl is included) having sold 88% of the lots by value. The other auction of higher quality Emeralds was held in November generating revenues of $34.9M at an average price of $65.89 per carat, which was a record high, having sold 89% of all lots by value. In February, after the period end, the group held an auction of lower quality Emeralds which raised $14.5M at $3.72 per carat.

In Mozambique the bulk sampling programme at Montepuez continued to increase in scale and delivered pleasing results. They were focused on alluvial deposits found within the Maninge Nice and Mugloto areas. After a technical review the rock handling approach has been optimised and additions to the fleet have brought the total rock handling capacity to an average of 310,000 tonnes per month compared to 120,000 tonnes per month last year. About 6.3M carats of ruby and corundum were produced during the period an increase from the 5.1M carats produced during last year with rock handling during the period hitting 1.5MT and total cash operating costs of $8.6M, nearly double that of last time.

About 171,000 tonnes of ore was processed by the washing plant with an average grade of 37 carats per tonne coming from the two areas. Total investment in property, plant and equipment was $6.1M with much of this being spent on improved washing plant facilities and mining equipment which has increased the washing plant capacity. An extensive exploration programme is underway across the entire license in order to generate a solid baseline geological map with sufficient data to better understand the extent and trend of the amphibolites, the gravel bed thickness and its distribution and indicative grades. The group is aiming to complete its first resource statement for Montepuez in the second half of the year. It is envisaged that a total of 25,000 metres will be drilled across the central part of the license with 7,000 metres being already completed in the first of three planned blocks with the initial drilling programme expected to be completed by December. The study has already delineated significant paleo-channel deposits with occurrences of ruby mineralisation within the Mugloto area and these have been proven by bulk sampling. Other areas with potential have been delineated as a result of the exploration programme.

Drilling in the Maninge Nice area recovered about 3,500 metres of core to date with the drilling mainly used to establish the continuity of mineralised amphibolite within the subsurface areas. The boundary of the amphibolite body and the subsurface continuity of ruby mineralisation to below 30 metres have been delineated and established and white marble bands of up to 30m in thickness and to a depth of 45m with intermittent bands of amphibolite have been observed.

During the period an additional rinsing screen was added to improve the performance of the washing plant during the rainy season which helped drive the increased processing performance achieved. A water reservoir and large dam have also been constructed next to the plant for the collection of rain water and seven water boreholes further supplement water supplies. Further capacity increases and recovery improvements are being studied which will be an important step towards finalising the planned increase in washing capacity required for the potential ramp up in production expected at the license in future.

The second ruby auction was held in Singapore in December of higher quality material which generated $43.3M, a record total for any Gemfields auction yielding an average value of $688.64 per carat. An exceptional 40.23 carat ruby, dubbed the Rhino Ruby, was part of this auction which was sold for an undisclosed price. In honour of this stone, the group have committed to supporting the anti-rhino poaching aircraft operated by game reserves, contributing to its flying costs during 2015, which I think is a nice touch. The next auction will be of lower quality ruby and corundum and is scheduled to take place in India in March with an auction of higher quality rubies scheduled to take place in Singapore in June – that might be the one to watch.

The mine’s camp site is due to undergo a significant upgrade in the coming year with the existing prefab structures being replaced by permanent infrastructure including improved roads, water purification capabilities, office units, accommodation units and leisure facilities. Work has already begun on upgrading the CCTV equipment and sort house areas to reduce the risk of stock losses. As we have seen before, site security has been an ongoing problem at the concession but a significant security presence and new infrastructure have resulted in an improvement. There is now a plan to separate the security department into an independently functioning unit with personnel being inducted from the Mozambique military.

Kariba is the world’s largest Amethyst mine. During the period the Curlew North, Francis West and Cha Cha pits have been actively developed with positive bulk sampling results achieved from the Cha Cha pit that means it is now an actively producing pit. Production of amethyst increased significantly during the period to 574,000 Kg from a level of 223,000 Kg last year and about 8,000 tonnes of ore was processed by the washing plant with the highest recoveries achieved from the Curlew pit. A total of 510 Kg of medium grade amethyst was sold during the period for $750K with the higher grade amethyst being sold at auction, generating $450K from 25.2M carats. A new exploration programme is being put in place for 2015 to confirm the re-estimate of the mineral resources available at the mine.

The Kariba mine is working towards a cost effective solution for energy and has initiated a brief for a 1MW solar farm in conjunction with an Australian solar supplier and the Zambian national electric company. The project aims to also offer excess capacity to the local community at a rate that will be subsidised by the Zambian government. Kariba will lease two hectares of its land to the project and the Australian company will fund construction with Kariba signing an off-take agreement to purchase electricity. The first phase of a new CCTC system was deployed during the period with 15 cameras monitoring key areas including the sort house, washing plant and stores with more extensive coverage being planned for 2015. These infrastructure upgrades will further increase mining volumes and operational efficiencies.

At Faberge the value of sales during the period increased by 2.4% when compared to the same period in 2013, despite a material decrease in sales arising from Ukraine and Russia, and improved practices helped reduce losses by approximately 17%. The business worked on expanding two important luxury categories namely Objets d’Art and high end Swiss timepieces which will be launched during the year. For 2015 and beyond the business will position itself as the artist jeweller, painting with precious gemstones and enamels to create unique pieces of art. It will also be partnering with leading multi-brand retailers and department stores.

During the period the group entered into a joint venture with EWGI, a Jersey registered company in order to progress opportunities in the Sri Lankan sapphire and gemstone sector, which will be 75% held by Gemfields. The company has acquired 75% operating interests in 16 exploration licenses for $400K. A gemstone trading company called Ratnapura Lanka Gemstones will also be established which will focus on sourcing rough sapphires from various sources in the local market. A trading license has been obtained and a token shipment of sapphire has been made to the Gemfields UK office. They are also in the process of establishing infrastructure in Sri Lanka and commencing preliminary geological assessment of the permits.

Additionally the group acquired controlling interests in two extra ruby deposits in Mozambique which are valid for an initial period of 25 years through a new company, Megaruma, that is 75% owned by the group. The two licenses both border the existing Montepuez ruby deposit and cover about 19,000 hectares and 15,000 hectares. In February the group also acquired a 75% interest in an emerald exploration license through an Ethiopian registered company, Web Gemstone Mining, for a total consideration of $254K. The license covers an area of 200 square Km in Southern Ethiopia and potentially hosts emerald mineralisation within a geological lineament that stretches over 45 km. Satellite imagery studies of the area have been completed and evidence of emerald mining in the belt is indicated by informal market reports and by the presence of several small pits. Further exploration work in the area, including bulk sampling, will be carried out over the next 18 months.

During the year the Zambian joint venture entered into a $20M revolving credit facility with Barclays bank that bears interest at LIBOR plus 4.5%. This loan replaced the previous loan that had a balance of $6.8M and will be used for Kagem’s working capital and capital expenditure requirements. The outstanding balance on this new loan was $15M at the end of the period.

After the end of the reporting period the company has informed us that the tax regimes in both Zambia and Mozambique have seen legislative changes. In Zambia the two-tier corporate income tax regime has been replaced by a mineral royalty tax regime and in Mozambique there has been a number of changes to the tax code including a reduction in the rate of production tax and the introduction of new taxes. Management are awaiting additional regulations and guidance from the tax authorities in both countries before they understand the implications fully but this all sounds rather worrying.

The next auction will be of lower quality rubies and is scheduled to take place in India in either March or April with an auction of higher quality rubies scheduled to take place in Singapore in June, which would be more likely to give a boost to earnings and the share price. The board expect a steady increase in demand with the associated increase on achievable price to continue for the foreseeable future and the company’s exploration and expansion could also yield positive results.

Overall then this seems like a good set of results. Profits increased considerably and net assets improved to leave the balance sheet in a healthy state. There seem to be quite a lot of sampling operations taking place, both in Zambia and Mozambique but although cash flow has improved there is still no free cash flow. The Faberge business looks unlikely to make money any time soon, though, and they have been hit by the Ukraine crisis as Russia is a large market. At the auctions, the rubies are selling well and seem to bring in a lot of cash which boded well for the future when production is ramped up. The Emerald auction was a bit more worrying, though, as the group failed to sell a lot of the total stones last time round. Also, the news about the tax changes in both African countries outlines some of the risks in operating in such countries and is another potential cause for concern.

In conclusion then, there certainly seems to be a great deal of potential here and the ramp up of ruby production is cause for optimism and this seems like it should be a great investment at some point. The niggling issues restrain me for the moment though and I would like to see some clarification over whether the lack of sales at the Emerald auction is a permanent change or a one-off and also over the changes to the tax regimes in the countries that the group operates in.

Despite the recent short rally, these shares have gone no-where since June last year so I will keep an eye out for a potential break out.

On the 14th April the group released a market update covering the latest quarter. There was an increase in quantity and quality of emeralds produced at Kagem, increasing from 3.6M carats last quarter to just under 10M carats this time. The fourth phase of the wall pushback programme in the main Chama pit continued during the period with about 4M tonnes of waste removed, with a slightly accelerated rate meaning that this is likely to be completed ahead of schedule. The exploration and bulk sampling activities at the Fibolele and Libwente pits are progressing well and the reduction of illegal mining within the boundaries of the license had made considerable progress given that Kagem has re-absorbed these areas into the site’s routine operations.

The February auction of lower quality emerald and beryl saw 3.9M carats being sold, representing 88% of the value offered but only 39% of the total weight offered. The auction generated $14.5M with an average of $3.72 per carat, a new record for the lower quality stones. The next auction of traded rough emerald is scheduled to take place alongside the Ruby auction in India in April.

In Mozambique, bulk sampling operations at the Montepuez ruby deposit continued. The core infrastructure is in place and progress is being made towards formalised mining. The test work led to an enhanced understanding of the ore characteristics and improved throughput in the semi-mobile processing plant which saw an almost three-fold increase in processed tonnes when compared to the same quarter last year, although looking at the figures it seems that the grade of rock has declined somewhat. Unlicensed mining activity and asset loss remains a key challenge at the mine but the new mining law may be a supportive mechanism in partly addressing these issues and in the meantime significant security presence and ongoing efforts have resulted in a strong improvement this quarter.

The group’s second auction of higher quality rough amethyst from the Kariba mine was held alongside the rough emerald auction with revenues of $450K were generated at a realised value of $1.77 per carat. The Faberge Pearl Egg was unveiled at the Doha Jewellery & Watches Expo in Qatar and was sold within houses to local businessman Hussain Al-Fardan. The new jewellery collections unveiled at the expo and presented to press in Basel were apparently well received and helped boost overall sales figures. The new timepiece collections were also well received at the same show and the pear egg in particular has generated a lot of press attention.

In Sri Lanka the group is in the process of establishing initial infrastructure and initiating preliminary geological assessments in areas of interest with the placement of key management in progress. At the end of the period the group held cash of $27.9M and total debt of $35.5M, including $20M of debt at Kagem.

On the 23rd April the group announced the results of its lower quality ruby auction held in India. The auction generated $16.1M at $4.03 per carat and some 93% of the lots sold by value. The group also offered traded rough emeralds at the auction which generated a further $1.6M. The next auction to take place will be of higher quality ruby expected to take place before the end of June.

Overall these are good updates which shows the group is making steady progress and I am tempted to take a position here, funds permitting. Funds permitted, so I did!

On the 23rd June the group announced its results for the latest auction of higher quality rubies in Singapore. A total of 72,208 carats were offered compared to 85,491 last time but only 47,451 were sold, representing just 61% of lots. Moreover, the average carat value realised was $617.42 compared to $688.6 last time with the auction yielding $29.3M, down from $43.3M. This is despite the sale of an exceptional matching pair of rubies with a combined weight of 45 carats that were bought by Veersak Gems of Thailand and named the ‘Eyes of the Dragon’.

The CEO states that demand for fine gems remains healthy and the prices obtained were in line with expectations but there has been some softening in demand for certain darker tone and lower quality grades. This seems like a disappointing auction result to me and I think I might look to sell out at roughly break even with a view to hopefully buying back in at a later date.

On the 22nd July the group released a JORC resource and reserves update for the Montepuez Ruby mine which is the first recorded mineral resource statement. It was noted that to date, rubies from the mine differ geologically from many of the rubies traditionally available in the international markets in that they are amphibolite related rather than marble of basalt related.

The mineral resources statement is as follows (I have included the last estimates of probable reserves and grades in brackets):

Maninge Nice Primary 245M carats indicated and 44M carats inferred at a grade of 115.4 carats per tonne. (253M carats at 114.9 carats per tonne)

Maninge Nice Secondary 107M carats indicated at a grade of 349.8 carats per tonne. (107M carats at a grade of 58.3 carats per tonne)

Mugloto Secondary 72M carats indicated at a grade of 15.3 carats per tonne. (72M carats at a grade of 3.1 carats per tonne)

In total this relates to 289M carats indicated and inferred of the primary mineralisation type at a grade of 115.4 carats per tonne and 178M carats indicated and inferred of the secondary mineralisation type at a grade of 35.7 carats per tonne. As we can see the total number of carats has increased at Maninge Primary and the grades have increased considerably at the other deposits.

The group are targeting an increase in mining capacity from 3.3M tonnes per annum currently to 5.6M tonnes per annum by July 2017 and to increase the annualised processing rate from 399K tonnes per annum of ore to 1.3M tonnes per annum. This will be achieved by undertaking the following capital improvements:

The current wash plant is to be upgraded from 100 tonnes per hour to 150 tonnes per hour; a secondary was plant will be installed with a 250 tonnes per hour capacity; the ore stockpile areas will be expanded onto currently undisturbed land; the existing two-way haul road to the Mugloto pits on which the trucks are currently plying in a convoy system will be replace with two 12m wide one-way haul roads for laden and empty traffic movements; and the existing workforce will increase from 369 people to 1081. The capital cost for the existing wash plant upgrade, the new wash plant and replacement sorting house is approximately $23M.

In total 27.5M tonnes of ore is expected to be processed over the 21 year life of the mine at an average grade of 15.7 carats per tonne and production is expected to make a step-change increase in the year ending 2017 from 11,865 carats in 2015 to 20,152 carats. This is then expected to increase at a more modest rate to 20,520 carats by 2020. Total operating profit in 2016 is expected to be $48M, increasing to $123M in 2017 and reach $220.2M by 2020 and this model assumes an average sales price of $389 per carat for high quality rubies and $1.30 per carat for lower quality rubies and corundum.

The total capital cost is estimated at $305M with $105M outlined for engineering and mining, $63M for the wash plant, $120M for sustaining and exploration capital for the ongoing operations and closure costs of $20M. The bulk of the capital expenditure is expected to be incurred in the year ending 2016, with $49.2M to be spent, falling to $14.8M in 2017 and $11.3M by 2020. So the mine is expected to be considerably profitable from 2016 onwards.

The price of $389 per carat seems very conservative considering the reduced price achieved at the last auction was $617. To me this seems like a great update, I really like the way the information is set out in a clear and concise manner with very conservative cost models – other natural resources and oil companies can really take note of this! The ruby mine has a long life ahead of it and should be very profitable even in a lower ruby price environment and I have re-entered after selling out following the last auction results.

On the 13th August the group released a statement covering trading in Q4 2015.

At Kagem the group produced 8.1M carats of emeralds at a grade of 222 carats per tonne compared to 6.2M carats at 271 carats per tonne in Q4 last year and 9.9M carats at 355 carats per tonne last quarter. Total cash operating costs were $10.5M compared to $8.9M in the same quarter of last year and $11.4M last quarter ($1.58 per carat against $1.79 and $0.99 respectively). The fourth phase high wall pushback programme being carried out in the Chama pit continued to be advanced during the period and the programme remains on schedule for completion at the end of September. In addition, the exploration and bulk sampling activities at the Fibolele and Libwente pits are progressing well. For the year as a whole, the auctions saw 16M carats being sold, representing 89% of the value offered and generating revenues of $64.9M.

At Montepuez, mining and bulk sampling operations continued to provide positive results and insight into the geology of the deposit and the ongoing test work has led to an enhanced understanding of the ore characteristics and improved throughput at the processing plant which saw a 10% increase in processed tonnes when compared to the same quarter of last year. This quarter, the mine produced 700K carats compared to 200K carats in Q4 last year and 1.4M carats last quarter at a grade of 9 carats per tonne (compared to 18 and 3 respectively). The gemstone cash unit cost increased considerably from $2.64 per carat last quarter to $8.57 per carat this quarter (although it remained below Q4 of last year) and the total cash operating cost increased from $3.7M to $6M.

The ruby auctions during the year saw 4.1M carats being sold representing 82% of the value offered and generating revenues of $88.5M. Faberge took part in the art, antique and design fair “Masterpiece London” for the first time where jewellery, timepieces and objets d’art were showcased alongside loose gemstones from the mines of Gemfields. In addition to the new collection Secret Garden, a suite of exceptional coloured jewels inspired by the floral compositions of painter Marc Chagnal and the “Lady Compliquee”, a complicated timepiece featuring a peacock opening its feathers every hour; the first two pieces of objets d’art were unveiled. The set, called the Faberge Four Seasons Eggs, comprises dour decorative eggs, each set with one of the four major gemstones – diamond, emerald, sapphire and ruby to represent the four seasons.

In Sri Lanka, the group continued the process of establishing initial infrastructure for trading operations and the placement of key management is in progress. In Ethiopia, an exploration team was recruited and established on site to help develop a better understanding of the license area. A base camp has been established on the concession and a team was stationed there in June. Exploration work has commenced for 2016 with preliminary ground surveys and plan in place for Q1. These include mapping, preparation of base plans, manual pitting and trenching.

At the year-end the group had cash of $28M and total debt of $45M so net debt of $17M. Overall there was not really much new released in this update – the grades being mined at both mines seem to have fallen when compared to last quarter though, with the consequential increase in costs and decline in carats recovered – there was no explanation given for this but I am just about content to hold on to the shares given the exciting potential revealed from the resource statement last time.

On the 7th September the group announced the results from its auction of higher quality rough emeralds and higher quality amethyst. The auction took place in Singapore following seven successive emerald auctions held in Lusaka and the group sold some 88% of the value on offer which was broadly similar to the last two auctions. The total realised from the auction was $34.7M and the average price per carat came in a $58.42 which, although below the $65.89 achieved last year, is broadly in line with the February 2014 auction. The amethyst auction saw 11M carats placed on offer with 10.1M being sold generating revenues of $440K. This represents an average value of 4.32c per carat, more than double the 1.77c achieved last time.

Considering the slow-down seen in China and the fall in the price of diamonds, these emerald prices actually look fairly robust. I expect this is in part due to the fact the auction was held in Singapore rather than Zambia which I would have thought may have mitigated any price falls. I am finding it hard to know what to do here, there is no doubt that this is a quality company but if the global financial problems do increase, the demand for emeralds and rubies are likely to take a hit. Having said that, after dipping in and out of this share twice now, I am sorely tempted to dip back in.

On the 10th September the group announced that it had entered into binding agreements to acquire controlling interests in two emerald projects with operations and prospects located in the Boyaca state in Colombia.

The Coscuez Licence includes exclusive rights for the exploration, construction and mining of emerald deposits granted by the Colombian government within the area of Coscuez in San Pablo de Borbur, Boyaca. In the past the area has hosted the Coscuez mine, one of history’s more significant emerald mines, having been in operation for over 25 years. In 1990, open pit mining was replaced by small scale underground mining in the upper reaches of the deposit with extraction taking place from adits mines into the hillside. Under the terms of the agreement, Esmeracol will transfer the license to a newly incorporated company imaginatively called Coscuez NewCo and Gemfields will acquire an indirect 70% interest in this company. Further exploration activity needs to be carried out to support the development of a geological model and a prelim mine plan, all of which is likely to take up to two years.

The total consideration payable is $15M with the first tranche of $7.5M due on completion, $5M in cash and $2.5M in Gemfields shares. A second tranche of $2.5M is due on the first anniversary of completion and a third and fourth tranche of $2.5M each upon attainment of agreed profit targets. Completion is expected to occur by March 2016.

The second project comprises a number of new license applications and assignments to existing concession contracts administered by the Colombian Mining Agency. The applicants for the mining licenses are a number of Colombian companies indirectly controlled by ISAM Europa. Gemfields has acquired indirect 75% and 70% effective interests in underlying licence applications and assignments through two holding companies which own the assorted Colombian companies. The total package of mining license applications and assigned concession contracts cover about 20,000 hectares in the Boyaca and other Colombian departments and comprise mostly greenfield sites, although small scale mining has occurred in some of the license area. Eight of the assignments have been approved and issued so far with the remaining applications under review.

The total consideration payable is $7.5M with the first tranche of $450K being paid today. A second tranche is payable upon granting of certain license applications, a third tranche is payable when bulk sampling commences on certain license areas, a fourth tranche is payable on the commencement of commercial mining and a fifth and sixth tranche (comprising more than half of the total consideration) is payable upon attainment of agreed revenue targets.

This is an interesting development and gives the company something to do after the Montepuez mine is up and running properly I suppose. This is a completely new geographic area for the group so probably does come with some execution risk and without a) knowing why mining stopped at Coscuez or b) more about the slightly confusing arrangement with the other licenses it is quite hard to know if this is good value or not. Still, some further diversification is probably not a bad thing.

On the 23rd September the group released a Kagem Emerald Mine JORC Resources and Reserves Update. In total the measured, indicated and inferred mineral resource is 1.8 billion carats at a grade of 281 carats per tonne. The measured mineral resource is 290M carats at a grade of 345 carats per tonne, the indicated mineral resource is 1.33 billion carats at a grade of 335 carats per tonne, and the inferred mineral resource is 181M carats at a grade of 110 carats per tonne. There are proven and probable reserves of 1.1 billion carats at a grade of 291 carats per tonne consisting of 276M carats or proven reserves at 300 carats per tonne and 840M carats of probable reserves at a grade of 288 carats per tonne.

The projected life of mine for the open pit operation is 25 years with the Chama pit is expected to be depleted by 2039 and the Fibolele pit by 2021. They are producing a total of 1.1 billion carats and capacity is expected to increase from 90,000 tonnes per annum to 180,000 tonnes by July 2018 with the inclusion of the Fibolele pit. The average annual production of emeralds and beryl is expected to be 44.7 million carats over the life of the mine and the projected real cash flow over its life is about $1.59BN.

The net present value is $520M based on a 10% base discount rate. Kagem is expected to generate $4.322BN in gross revenue with total operating costs of $1.017BN, assuming an average sales price of $61.5 per carat (compared to $58.4 per carat at the last auction) for higher quality emeralds and $0.88 per carat for lower quality emeralds and beryl. The total capital expenditure is expected to be $516M over the life of the mine. A substantial exploration programme using proven techniques is planned for the next few years to explore the rest of the license area to further determine the remaining resource potential.

Overall then, this mine is likely to generate a decent amount of cash flow over its life time and we can see that both production and profits are expected to ramp up over the next few years. It has to be said, however, that the assumed sales price per carat seems rather aggressive.