Majestic Wine has now released its interim results for the year ending 2015.

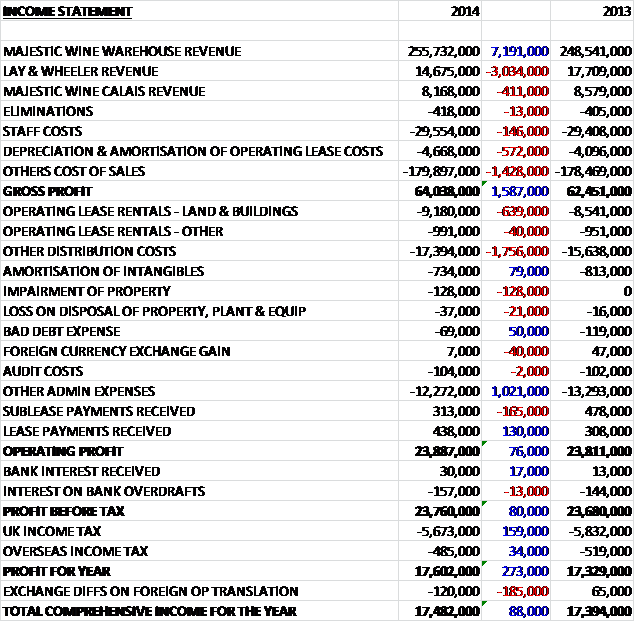

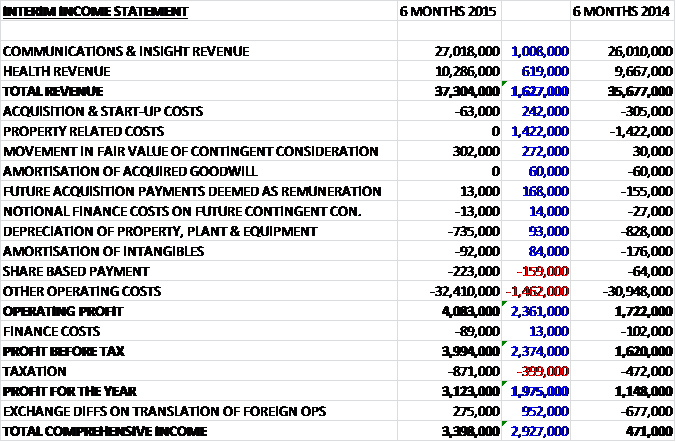

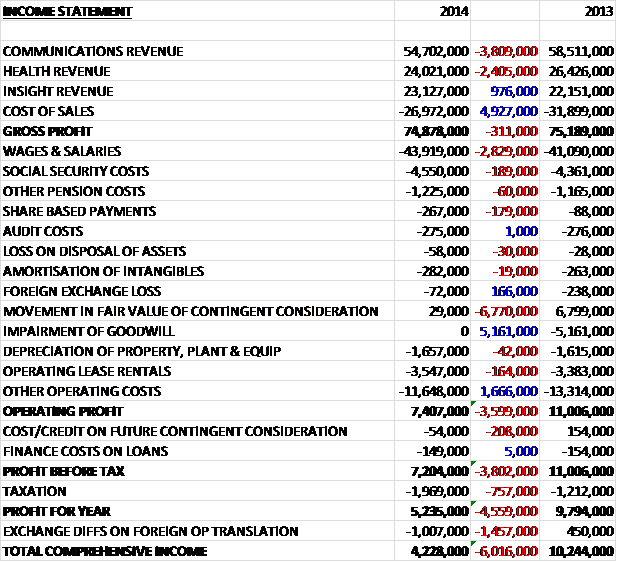

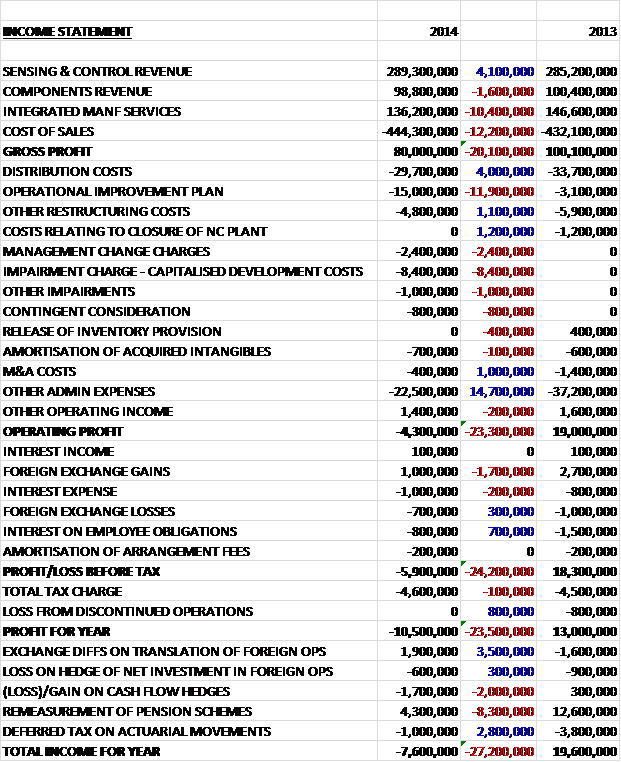

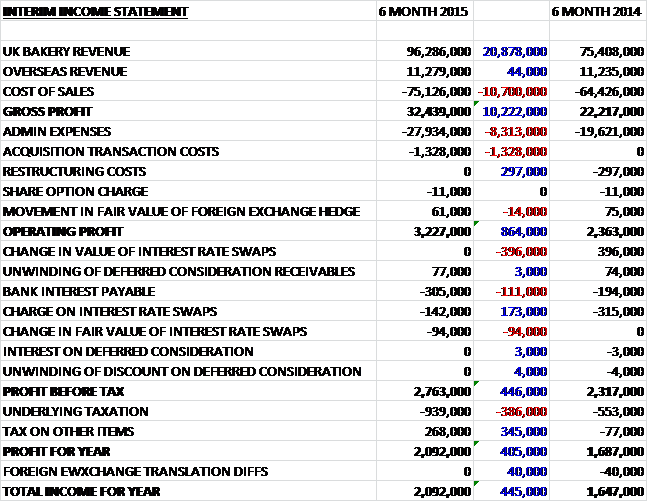

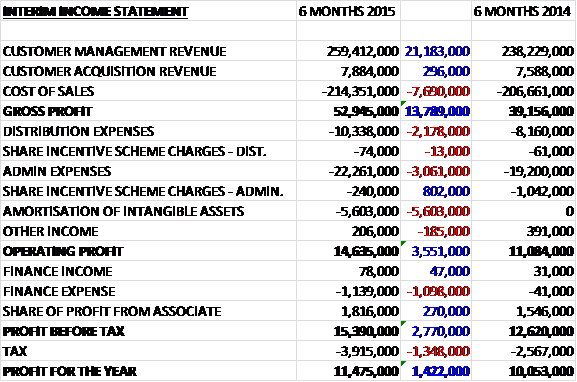

Overall revenues increased when compared to the first half of last year as a £6.8M increase in the core majestic wine warehouse revenue was offset by a £3.4M collapse in sales at Lay & Wheeler and a £239K decline in Majestic Wine Calais revenue. We also see an increase in depreciation and a £2.2M increase in cost of sales to give a gross profit some £1M higher than last time. This was wiped out by a £1.1M increase in distribution costs with a similar increase in overall admin costs so that operating profit fell by £1M. After finance costs, and a lower level of tax, the profit for the half year fell by £809K to £6.4M.

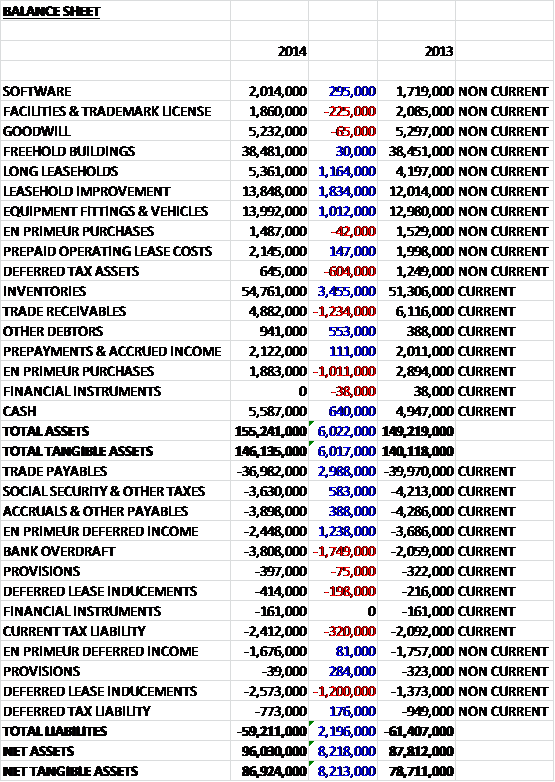

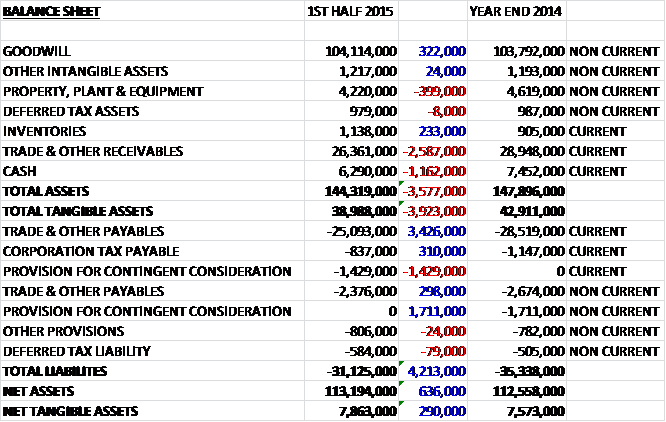

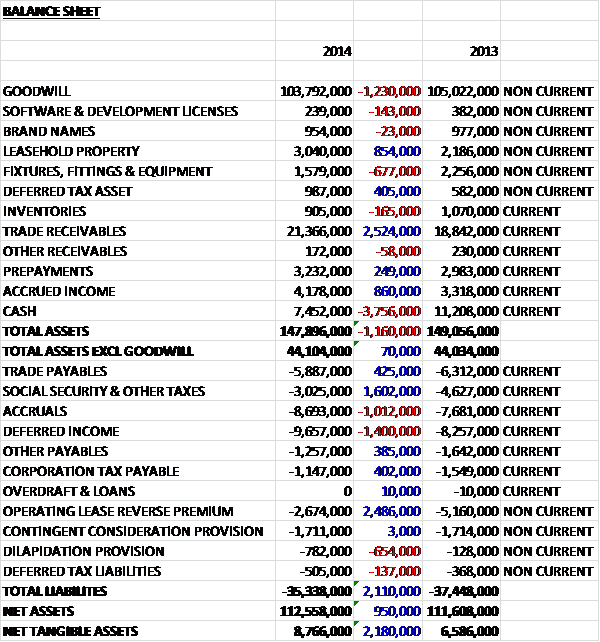

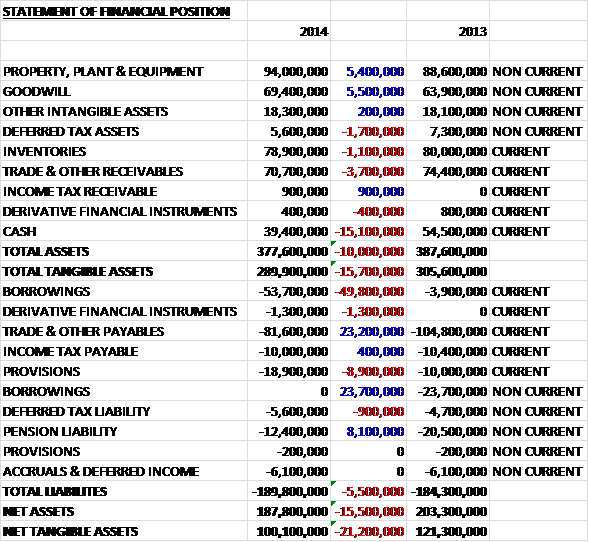

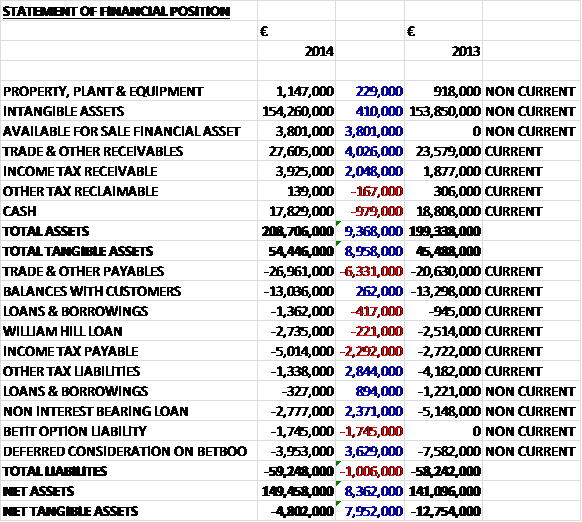

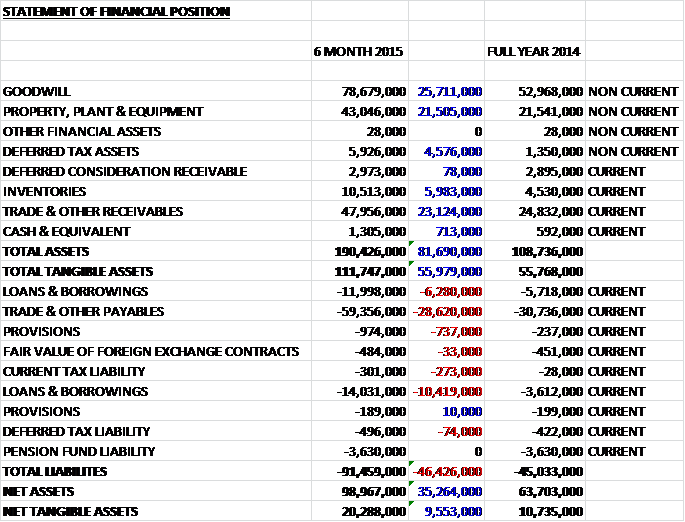

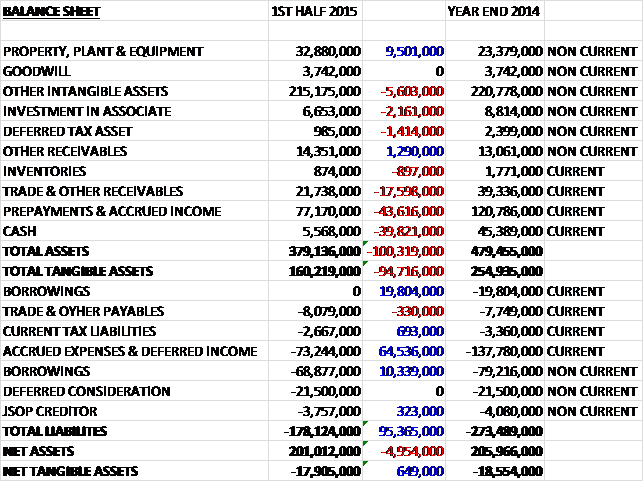

When compared to the end point of last year, total assets increased by £4.1M driven by a £2.5M growth in inventories, a £2.2M increase in receivables and a £1.2M growth in property, plant and equipment partially offset by a £1.4M fall in cash levels. Liabilities also increased during the year as a £5.2M increase in the bank overdraft and a £1.2M growth in payables was partially offset by a £739K fall in current tax liabilities. The end result is a £1.2M fall in net tangible assets to £1.2M.

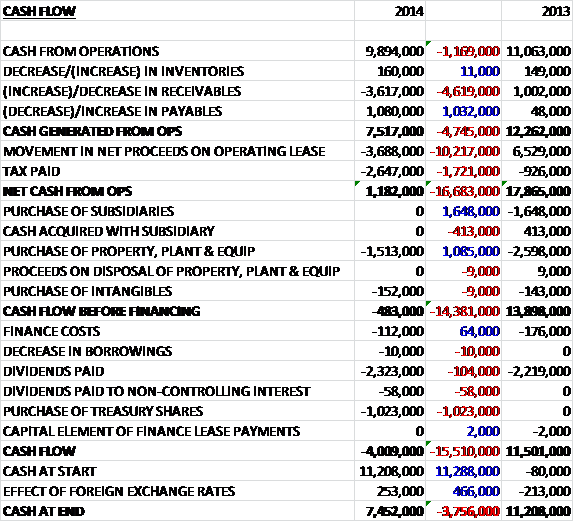

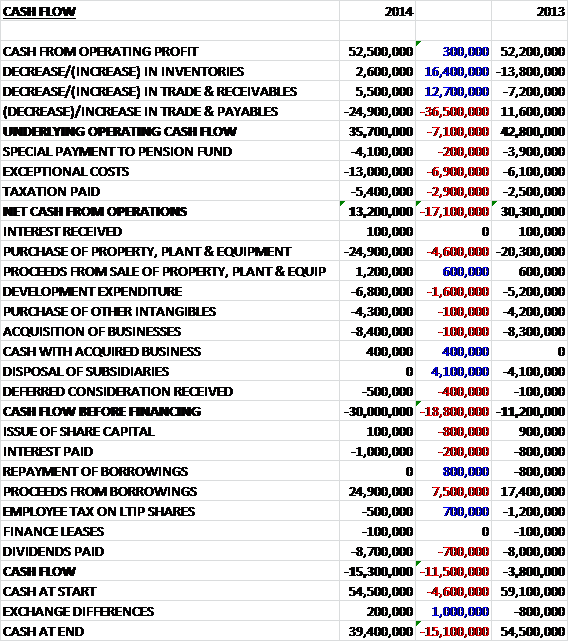

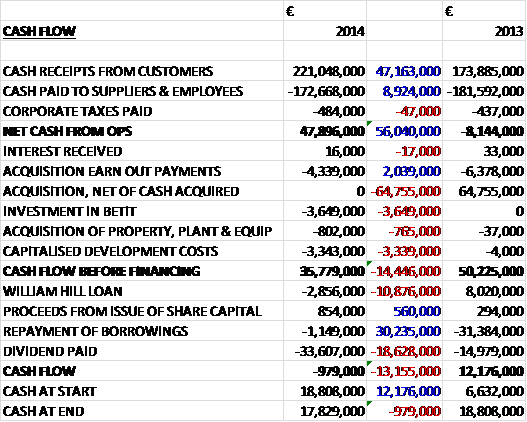

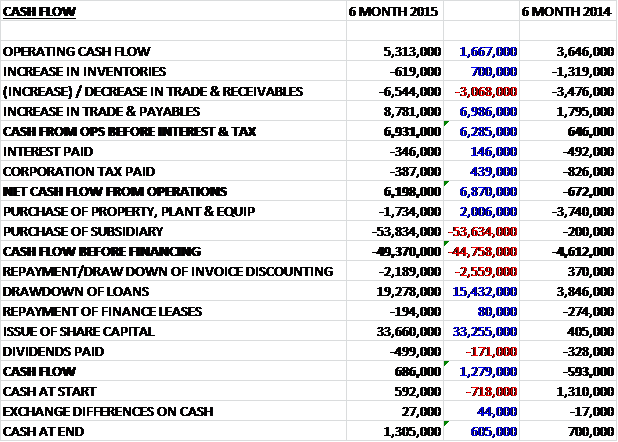

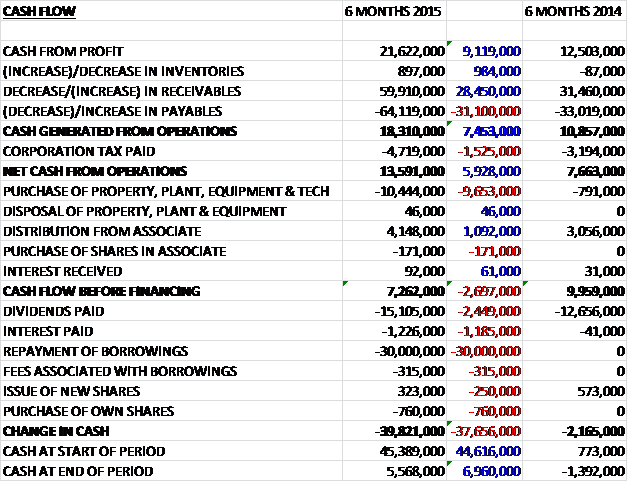

Before movements in working capital, cash profits fell by £2.1M to £12.2M which, after decreases in inventories and receivables were partially offset by an increase in payables, meant that cash from operations increased by £2.4M to £8.5M. After tax this became £5.8M which was enough to pay for the capital expenditure to give a free cash flow of £1.3M, clearly not enough to cover the £7.7M paid out in dividends to that the group had to eat into its overdraft with a negative cash position of £4.8M.

The retail environment in which the group operates remained highly competitive but the group increased market share by 0.1% to 4.3% and UK like for like sales grew by 2.8%. During the current year the group has been investing in market and customer insight; better infrastructure; and the latest technologies necessary to secure future growth and the cost of these investments has impacted upon results, along with the weak Bordeaux 2013 vintage. The lease on the old head office was coming to an end which prompted the group to purchase a long leasehold and locate all the teams into one facility. In addition, the old distribution centre was operating at full capacity and the new facility is large enough to handle the expected future growth and although these investments should drive future value, they will have an adverse effect on costs in the short term.

The Majestic Wine Warehouse posted a result of £7.7M, a decline of £700K when compared to last year due to the investments made in the period to support future growth, sales were actually up 5.7% with like for like sales up 2.8%. The average spend per transaction increased by £3 to £130 and the average bottle price of still wine is up from £7.71 to £8.02. The business in currently investing to grow their in-house multi-channel team which to support online growth which increased by 12.3% when compared to the first half of last time. The group has also appointed a CRM agency to enhance their communications and the first part of the CRM strategy has been executed which involved segmenting the database to deliver better targeted customer communication and since the end of the half year, they have launched a welcome programme to increase the proportion of new customers who return for future visits.

Total sales to business customers grew by nearly 5% to £26.8M and now represent 21.5% of all UK sales. There is a regional sales team who secure restaurant, pub and hotel business with the logistics being handled by the nearest store. In London there is a dedicated depot near King’s Cross that sells to larger business customers in the City and West End. In order to capitalise further, more investment has been put into the commercial sales team. During the half, four new stores were opened with two more being opened after the period end to give the group 210 outlets. It is expected that three new stores will be opened before Christmas and the group are currently conducting a revalidation of the locations and total footprint required to service the targeted segment of the UK wine market so it sounds like the store opening programme may be slowing.

The Lay & Wheeler business suffered a loss of £23K during the period compared to a profit of £467K last time. Over the summer, they experienced a disappointing Bordeaux 2013 campaign as the vintage was not great and sales were down across the industry which has further knock on effects on ancillary trading and broking of older vintages. The business has increased the frequency of diversified offers, such as the recent launch of Penfolds Grange 2010 to try and offset the decline. Since the end of the half year period they have re-launched their fine wine subscription club and rebranded it as Cellar Circle which offers members benefits.

The French business showed a profit of £738K, an increase from the £660K during the first half of last year and the business has recently simplified its pricing structure and spent time highlighting to customers that they can make substantial savings on the UK market and customers are encouraged to order through the click and collect proposition which accounted for 45% if sales from the division.

An unchanged interim dividend means the shares are currently yielding 5.2%. At the half year point, net debt stood at £4.8M, an £800K increase when compared to the same point of last year but a big change when compared to the £1.8M net cash position at the end of last year. Going forward, the rest of this year will be one of investing to “put in place the building blocks to deliver future growth” so it looks like profits aren’t expected to improve in the second half of the year.

Overall then, this was quite a disappointing update. Profits fell, net assets were down and although operational cash flow did improve, this was due to improvements in working capital when compared to the first half of last year and the free cash flow was no-where near enough to pay for the dividend. The core performance at the Warehouse offering was fairly decent as sales improved, in particular to businesses but the result was dragged down by increased costs related to investment in the business. Lay & Wheeler suffered a very disappointing half year due to continued problems with the quality of the latest Bordeaux vintage but the French business did seem to improve slightly. Management seem to be guiding expectations to non-growth this year and I remain un-invested.

On the 7th January the group released its Christmas trading statement. Total UK store sales for the 10 weeks over the period increased by 3.7% but like for like sales were only up 1.1% which means that year to date like for like sales have increased by 2%. The period was challenging due to increased levels of competitive promotional activity and whilst the group traded effectively over the period, the company invested gross margin into ensuring that pricing remained competitive in the more promotional environment. For the rest of the year, it is anticipated that this competitive pricing environment will continue which doesn’t sound very promising.

The chart shows that the shares are on a pretty clear downtrend and reinforces my decision to wait and see with this company.

On the 10th April the group announced a trading update and acquisition. Since the last update, total store sales grew by 4.1%, up by 1.5% on a like for like basis. January and February were in line with expectations but March was weaker which, when combined with adverse foreign exchange movements in March means that the group now expects to announce adjusted pre-tax profit of £21M for the full year.

The other announcement was the acquisition of Naked Wines, a privately held international wine business for a total consideration of £70M. Initially £50M will be paid in cash and a further amount up to £20M in Majestic shares. Naked Wines is an online crowd funded business model whereby its subscription customers help fund independent winemakers worldwide in exchange for access to exclusive wines at preferential prices. It is active in the UK, the US and Australia and recorded sales of £74M in 2014 with an EBITDA loss of £3.3M with the business expected to break even by 2016. Naked Wines will continue to operate as a separate brand with its own management team.

The cash component of the deal is being financed by a new five year revolving credit facility of £85M and will be supplemented by the withholding of the final dividend in 2015 and interim dividend in 2016. Rowan Gormley, the founder and CEO of Naked Wines will take over as CEO of the enlarged group with the current interim CEO returning to his role as CFO.

Whilst no one can get excited about the trading update, this acquisition looks transformational. Whilst Naked Wines is not yet profitable and Majestic has certainly paid a lot for it, this transforms the group away from an industry that could be argued to be in decline towards one that seems very fresh and exciting. I will keep a close eye on the share price and perhaps enter here as a slightly risky investment for the future.

It was also announced that non-executive director Ian Harding acquired 3,000 shares at a cost of nearly £90K to give him a total of 8,000 in all so he certainly seems to think the acquisition augers well.

On the 10th June the group announced the appointment of Anita Balchandani as non-executive director. She is a partner and sector head of the UK Retail Practice for OC&C Strategy Consultants and non-executive director at Space NK. Previously she held senior management positions at Shop Direct and Asda.