E2V is made up of three businesses. RF Power Solutions provides high performance electron devices, sub systems and solutions in radiotherapy, electronic countermeasures and industrial processing systems. High Performance Imaging Solutions provides advanced Charged Coupled Devices (CCD) and Complementary Metal Oxide Semiconductor (CMOS) imaging sensors, cameras and solutions in machine vision, space imaging and scientific imaging. Hi-rel semiconductor solutions provides high reliability semiconductors and services in aerospace and defence semiconductors which includes high assembly, packaging and test services, extended availability of obsolete and end of life integrated circuits and own design high speed data converters. They have now released their final results for the year ending 2014.

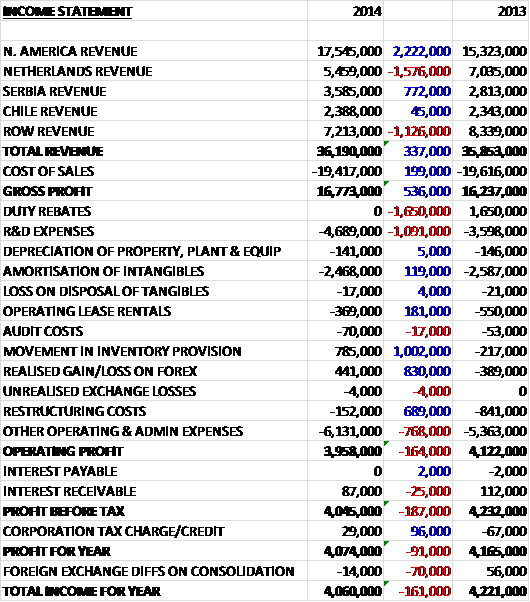

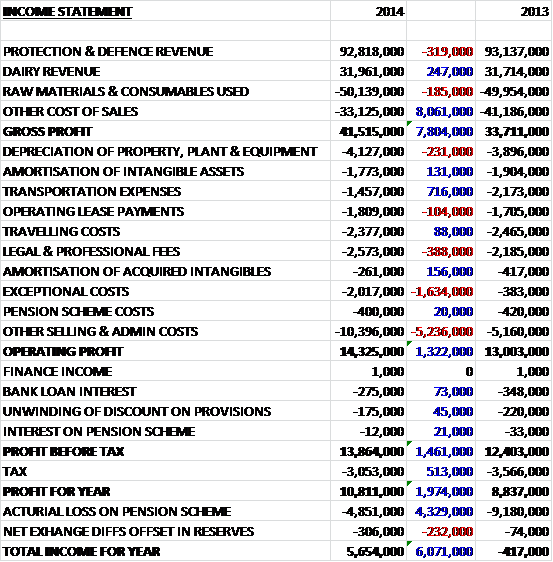

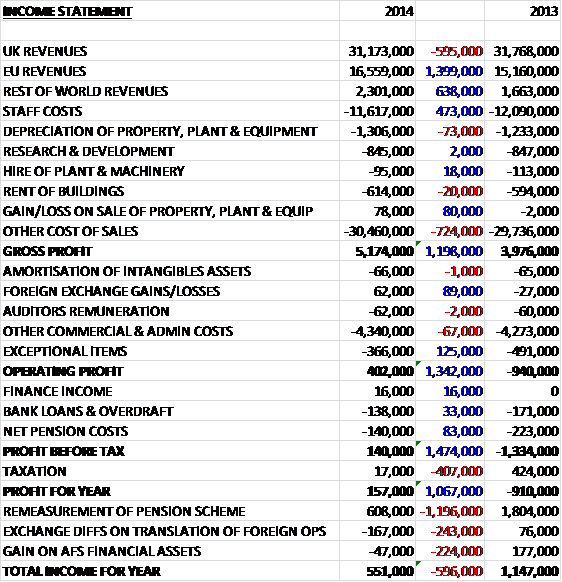

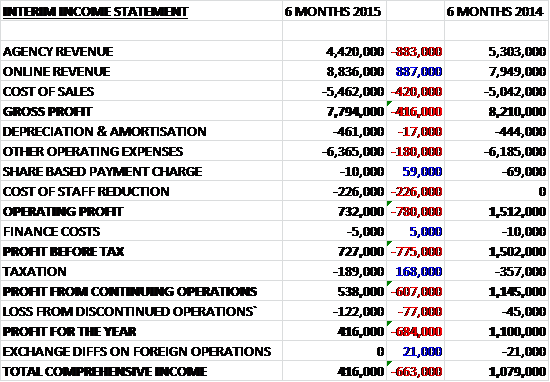

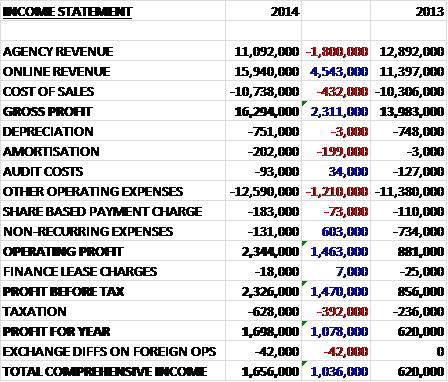

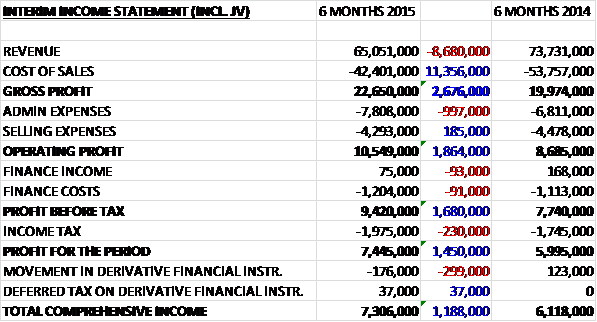

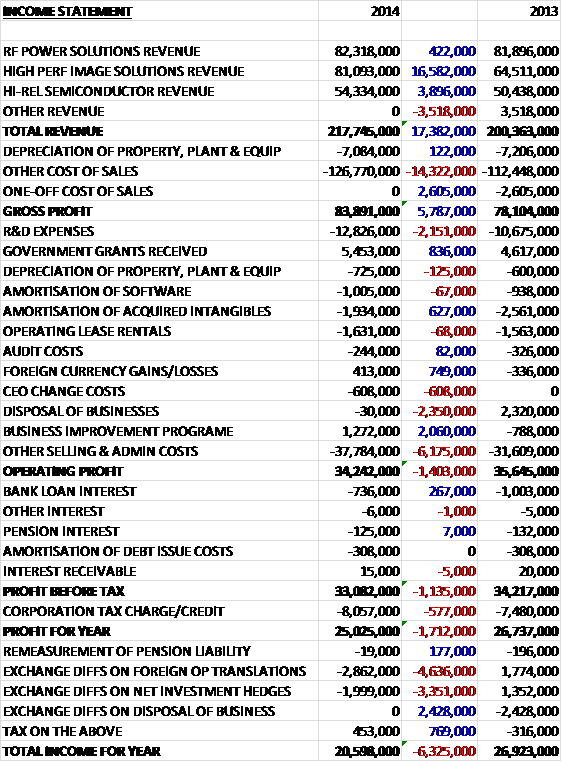

Total revenue increased by £17.4M, predominantly driven by a £16.6M hike in High Performance Image Solutions, somewhat offset by a £3.5M decline in other revenue relating to the lack of any property sales. The increase in cost of sales , somewhat offset by the lack of the one-off costs (amortisation of acquired intangibles) that occurred last year, meant that gross profits were some £5.8M higher. As far as operating expenses are concerned, we saw a £2.2M increase in R&D expenses, partially offset by an increase in government grants. We also see the lack of a windfall from the sale of the business and a swing to a profit from the business improvement programme but a £6.2M increase in other sales and admin expenses meant that operating profit was £1.4M lower at £34.2M but a higher tax rate meant that the profit for the year was £1.7M below that of last year at £25M.

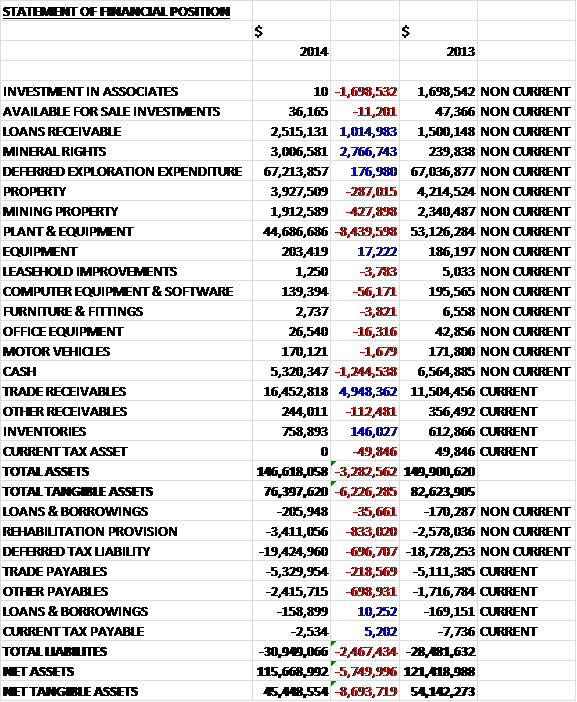

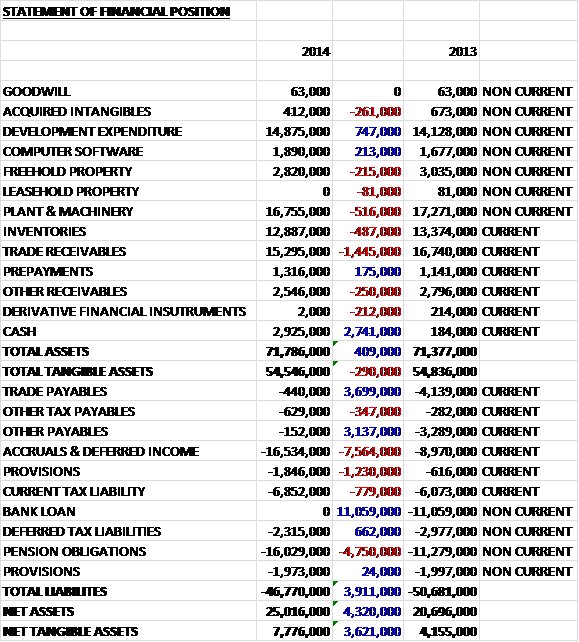

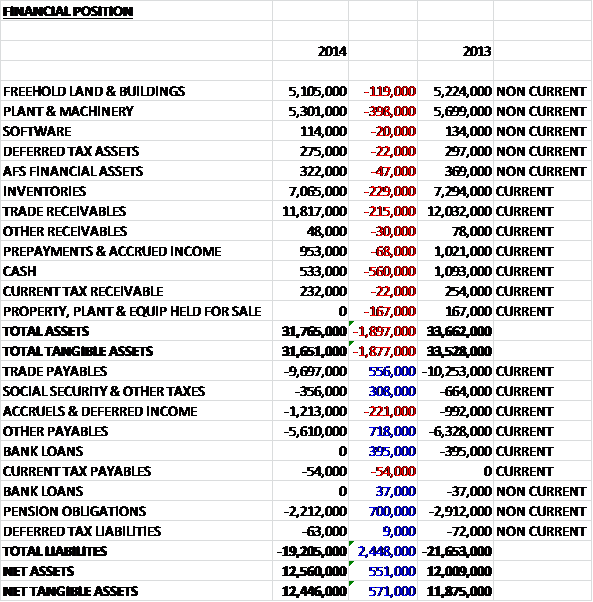

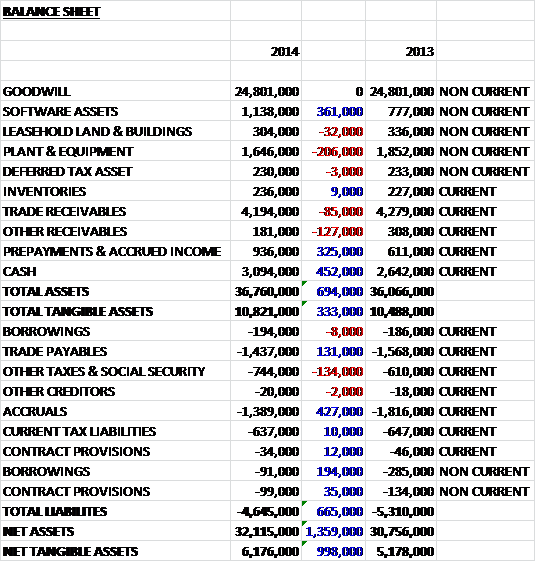

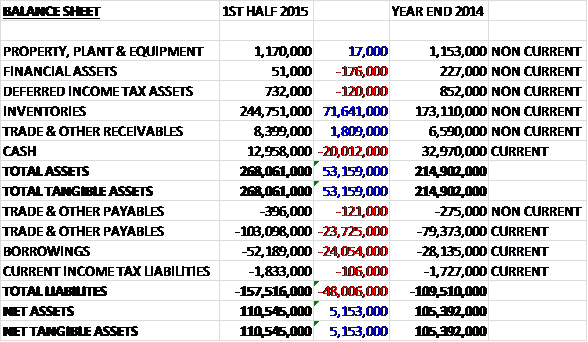

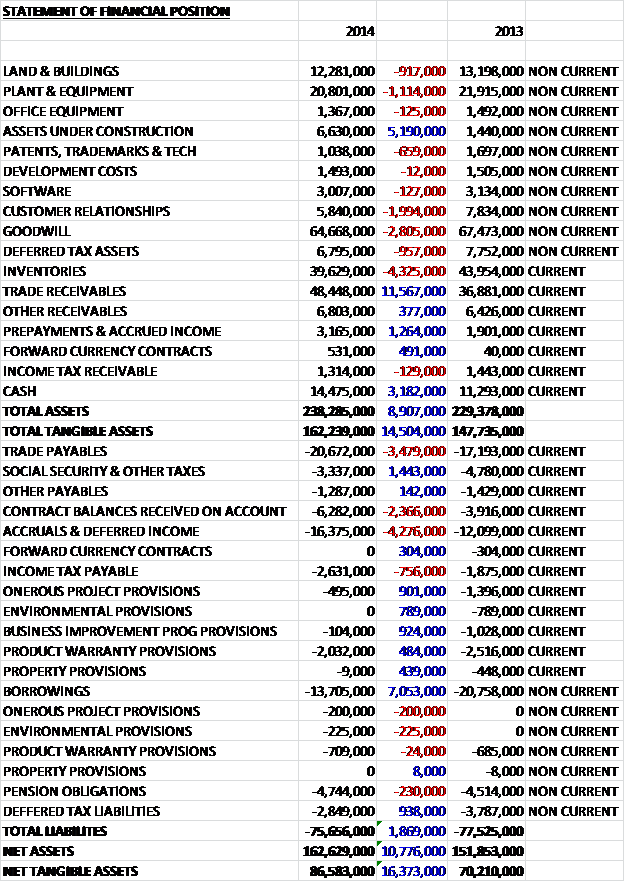

When compared to the end point of last year, total assets increased by £8.9M. This was driven by a £5.2M increase in assets under construction, a £3.2M growth in cash and an £11.6M hike in trade payables, somewhat offset by a £4.3M fall in inventories driven by a £3.2M reduction in Space inventory due to the increased deliveries in that sector, a £2.8M decline in goodwill and a £2M fall in the value of customer relationships. Conversely we saw total liabilities fall due to a £7.1M decline in borrowings and a decline in tax liabilities offset by a £4.3M increase in accruals & deferred income, a £2.4M growth in balances received on contract and a £3.5M increase in trade payables. The outcome of all this is that net tangible assets increased by an impressive £16.4M at £86.6M.

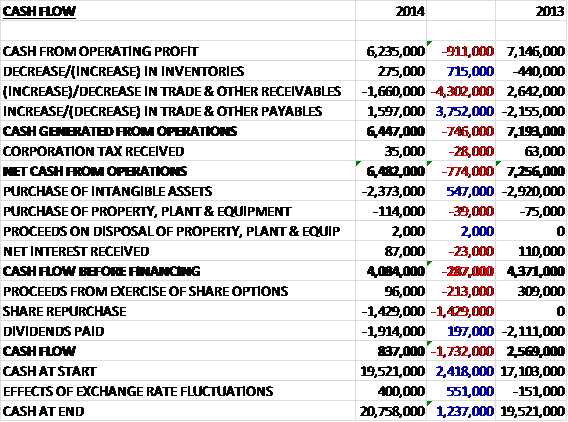

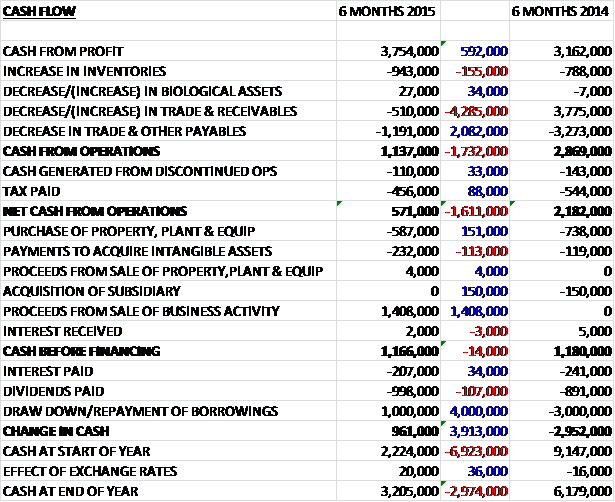

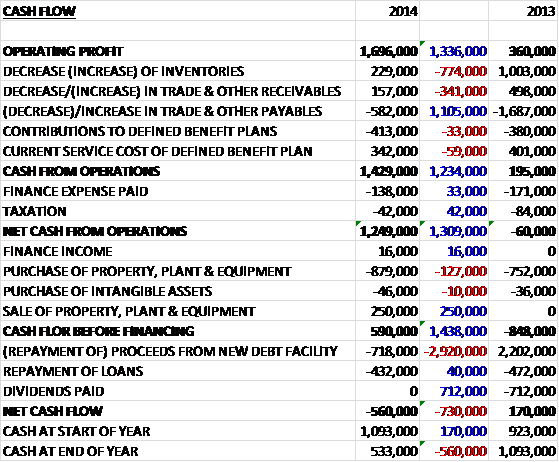

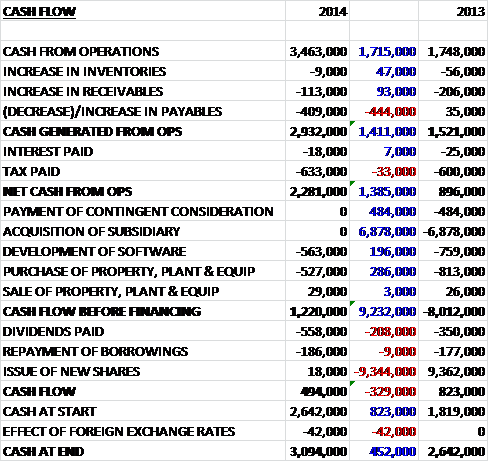

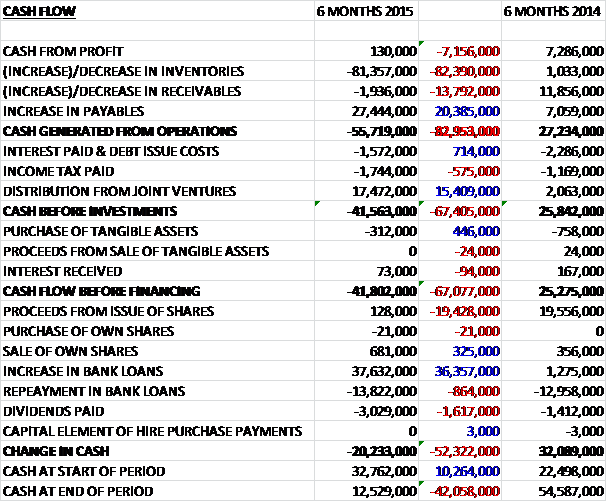

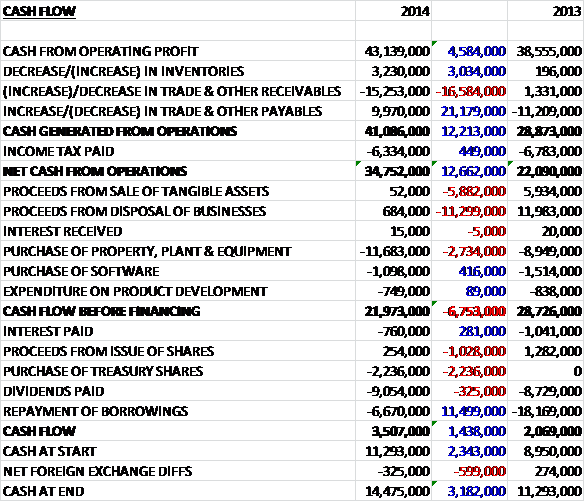

Before movements in working capital, cash profits were some £4.6M higher at £43.1M before working cap broadly cancelled itself out, although the swing in an increase in payables meant that cash generated from operations increased by £12.2M to £41.1M, which became £34.8M after tax. The bulk of this cash, some £11.7M was spent on property, plant and equipment but the lack of the large one-off receipts from disposals that occurred last year meant that the cash before financing was down £6.8M at £22M. Of this, £6.7M was spent on repaying loans, £2.2M on treasury shares and £9.1M on dividends and at the end of this there was still a positive cash flow of £3.5M so we can see that this business is very cash generative which is what I like to see.

Adjusted operating profits increased by 8% to £34.7M and represents a 15.9% margin, a slight fall on last year. There was a stronger performance towards the end of the year, particularly in Q4 in Asian industrial markets; US defence customers, particularly for semiconductors; and UK space products. There was also a steady growth in semiconductor activities, radiotherapy returning to growth in the second half after a slow start and new product introductions winning market share in professional imaging markets for industrial fire, security and medical.

As far as the group’s markets are concerned, key drivers in the medical and science sector are ongoing demand for spares reflecting growth in the installed user base and OEMs that are expanding their activities in Asia with increasing local competition. The board estimate sustained growth in medical with government funding for scientific research remaining steady. In Aerospace and defence there is increased demand for earth observation associated with climate change monitoring, space science and growing commercial aircraft production. In defence there is a shift to platform life extension and upgrade programmes. Electronic warfare and communications is receiving funding against an overall decrease in defence spending and there is a growing focus on semiconductor counterfeit and obsolescence management. In Commercial and Industrial, capital investment remains subdued but there are opportunities in Asia and emerging markets for new product lines.

RF Power Solutions had an adjusted operating profit of £16.1M, a decline of £800K when compared to 2013. The decline reflects the mix of revenue along with increased R&D activity. The order book at the year-end decreased by £8M to £100M due to the cycle of the multi-year radiotherapy contracts with delivery against the Accuray and Elekta contracts partially offset by the renewal of a three year contract with Varian. There was also a reduction in the defence order book reflecting delivery on the key programmes. In Radiotherapy the group provides RF power systems for the generation of high energy x-rays for the treatment of cancer. They are the market leader in the supply of magnetrons, thyratrons, modulators and services. The main customers are the radiotherapy OEMs such as Accuray, Elektra and Vairan. Revenue in this market was steady reflecting some destocking by one of the major customers in the first half of the year before returning to growth in the second half. In the coming years it is expected that spares revenue will grow in line with the past expansion of the installed user base. Growth is expected to come from continued new build demand, accounting for about a third and the growing installed user base that accounts for the rest.

In Electronic Countermeasures the group provides technology for platform life extension programmes and upgrades to enhance capability and provide electronic countermeasure protection of high value air, land and naval assets. These products are generally European made so not restricted under the US International Traffic in Arms Regulation, which is an advantage in international markets. Key customers are the system level OEMs including BAE, EADS, Raytheon, Salex Galileo and Thales. Revenue growth was driven by existing programmes including the ALE-55 programme for the F18 Super Hornet and the group has completed qualification for the MPM product for the SAAB Gripen. Western defence budgets are likely to remain subdued but some decline in short term uncertainty has been observed in the US with a continued shift to platform extensions and upgrade programmes.

In Industrial processing systems the group provides microwave and RF generators for the processing of bulk materials with the current focus on mining. During the year work was continued on the development programme with Rio Tinto covering the design and supply of large scale microwave and RF generators for improving the efficiency of mineral recovery. Other applications include radar for commercial shipping and industrial applications such as industrial heating, induction and dielectric welding, lasers and cargo screening. During the year the group completed the sale of the satellite communication amplifier business for a gain of £400K. As anticipated, revenue for the remaining business was lower than last year due to a softer demand in industrial and end user markets. Site restructuring programmes were continued in order to drive further operational efficiencies going forward.

High Performance Imaging Solutions had an adjusted operating profit of £11.2M, an increase of nearly £4M when compared to last year reflecting the revenue growth in machine vision, space and other applications that are mid-margin activities. In the future additional resources in the space business will provide the step-up capacity to support new space programmes. At the year end the order book fell by £2M to £61M reflecting the reduction of overdue deliveries in the space programmes along with the growth coming from businesses that have shorter order cycles.

In Machine Vision the group provides camera platforms for demanding automated optical inspection in semiconductor & electronics manufacturing inspection, food and beverage processing, ophthalmology and document imaging. The end user markets are specialised inspection equipment suppliers including OCT/Ophthalmology Canon, Carl Zeiss, Meditec and Optopol. There was strong revenue growth in the sector reflecting good customer demand in the first half of the year and a recovery in Q4. Growth was driven by the take up of the new CMOS based line scan cameras which provide high speed sensitivity and high resolution for inspection applications.

In Space Imaging the group is a world leader in imaging sensors and sub systems for space and ground based applications including space qualified imaging sensors and arrays for space science and astronomy applications and high speed, high resolution sensors for earth observation satelites. Increasing investment in monitoring climate change is a main driver for growth in demand for new observation satellite programmes. The group is continuing to develop a CMOS based technology platform which is part funded by a £3.8M award from the UK regional growth fund. In recent years E2V have won programmes both in the US and other space markets such as China. Main customers for these products are worldwide space agencies including ESA, NASA, CNES and CAST as well as the prime satellite manufacturers such as Astrium, Ball Aerospace, Lockheed Martin and Thales. The space imaging recovery programme has delivered growth throughout the year with a step up of activity in Q4 reflecting the delivery of milestones on a number of contracts. The business will remain technically challenging but current growth is expected from new programmes currently under discussion with existing customers.

In Scientific Imaging the group provides high sensitivity, low noise sensors enabling scientific instruments. The imaging sensors are used in spectroscopy, microscopy, crystallography, fluoroscopy and broad scientific imaging applications. The market for these scientific cameras is highly concentrated with three manufacturers – Andor, Hamamatsu and Roper, all of which are customers of E2V. The group has a significant market share in this area and revenue was steady with the current macroeconomic environment restricting government science spending. Other applications include CMOS dental oral sensors, 2D barcode reading and thermal imaging products. Growth has come from the dental sensors and new product introductions in thermal imaging with dental growth in Asia in particular as the group released a new product in China with Runyes, one of the largest OEMs in the Chinese dental market. Thermal imaging is now a vital technology in firefighting, law enforcement and security and the group’s new hand held products are targeted at these markets, particularly in the US. The group has also seen a good growth in demand for their industrial sensors from Honeywell and Datalogic.

Hi-rei Semiconductor solutions had an adjusted operating profit of £11.8M, a growth of £500K when compared to 2013. This was due to higher revenues at incrementally higher margins and despite increased R&D activities in Grenoble, benefiting from a grant from the French authorities. The order book at the end of the year fell by £1M to £23M with the order book for aerospace and defence semiconductors strong against a decline in the order book for the legacy smart sensor business.

In Aerospace and defence semiconductors the group acts as a value added channel partner, providing high reliability versions of their customer’s products in civil, space and defence applications. Some of their clients include Freescale, Everspin, Maxim and Micron. There has been good revenue growth and order intake as a result of Freescale’s end of life programme for the 603 family of microprocessors, where E2V has contracts supporting seven defence contractors that generated some revenue in Q4 along with a pick-up in demand in the US. They also benefited from the start of programmes supporting product from their partnership with Micron. In addition the group also provides customers with continuity of supply of over 4000 SMD components including many that have been made obsolete by their original manufacturers. These components are generally sold to distributors Arrow and Avnet but there has been lower demand for them in the US, although some recovery was seen in the final quarter of the year.

The own brand high speed data converters are used for analogue to digital and digital to analogue converters for space radio frequency communications. Some customers for these products include Boeing in the US and Thales in Europe. There has been some growth in these converters into space programmes with two new programmes scheduled for delivery over the next two years. Finally in this sector, the group offers outsourced assembly and test services to customers who do not have the in house capability to do it themselves. Sales of this service have been lower during the year reflecting lower demand in customer’s end user markets.

Semiconductor Lifecycle Management supports platform life extension in aerospace and defence systems when components become obsolete during the lifetime of the system, extending the availability of obsolete semiconductors and providing customers such as Raytheon Space and European OEMs working on the Eurofighter Typhoon programme. The estimated future revenues decreased by £4M to £20M with new programmes being offset by a reduction in future revenues on the Eurofighter Typhoon export orders. Other applications are in the smart sensor market for industrial automation, industrial detectors, automotive safety, engine management and climate control. When the group restructured their Grenoble facility it was decided that they would cease R&D work on these products and the revenue decline reflects the legacy nature of these lines.

The geographic spread of revenues is quite diverse with North America and Europe important markets and Asia Pacific becoming more important. There is some currency risk, although not too much. A 10% weakening in USD against the Euro would affect profits by £277K. Other risks include political and macroeconomic conditions. A number of the group’s products are for use in industries which are dependent upon and subject to government policies and budget constraints. A reduction in military spending or a prolonged economic downturn would have an adverse effect on group profits. Finally, about a quarter of sales relate to long term contracts on fixed prices so if performance costs come in a bit high, the contract could end up being unprofitable.

During the year the group continued its restructuring efforts but made an accounting gain. This was due in part to the fact that staff who were initially supposed to be made redundant at the Chelmsford site were able to be re-employed in the high performance imaging business. In Grenoble the group booked a £1M release of receivables provision. During the year Alison Wood started as the new senior independent director and Steve Blair was appointed as the new CEO after Keth Atwood left having spent 15 years in the role. Neil Johnson has now been Chairman for one year so this is a period of transition as far as management is concerned.

There is a solid order book but at £128M it was marginally lower than the £130M order book last year. Apparently this is because the growth has been delivered to businesses that have shorter order cycles and the recovery programme at the space business has lowered the number of overdue orders there. In all there was a solid order book for the semiconductor customers, full coverage from the radiotherapy customers and an active pipeline of opportunities in space and defence. Going forward the group are focusing on areas that they see growth potential such as radiotherapy, imaging for industrial, medical, fire and security markets along with space applications and semiconductors but they are continuing to support customers in other areas such as industrial process systems and electronic countermeasures as they adopt to the newly developed products.

The board remain cautious about the broader economic environment and anticipate modest revenue growth over the next year. They have indicated that they may consider some bolt on acquisitions if they become available.

At the current share price the group trades on a P/E ratio of 15.7 but this falls to a very cheap looking 9.6 on next year’s estimate. Likewise after a 7% increase this year the shares yield a decent 2.4% at the current share price but this increases to a good looking 4.2% on consensus forecasts for 2015. At the end of the year the group had a net cash position of £770K, a vast improvement on the £9.8M of net debt at the end point of last year and the group has quite a lot of headway, with revolving debt facilities of about £80M, although this is attracting non-utilisation fees.

Overall this was a pretty good set of results. Although profits didn’t really romp ahead, underlying profits were fairly strong. Net assets improved during the year and the balance sheet looks strong. Similarly, although operational cash flow was up, the free cash flow was slightly lower due to the disposal that took place last year. The group is very cash generative though and the move to a net cash position is welcome. Going forward, management do seem a bit subdued, indicating just a modest revenue growth and the order book is somewhat lower than at the end point of last year. The group does make exciting products, such as imaging for space programmes but it is the medical instruments that are probably has the best growth potential. In conclusion I do like this company, and its products but I feel the outlook seems a bit subdued at the moment so I will keep watch but not buy any shares for now.