Telecom Plus trades as the Utility Warehouse and provides a range of essential services to households and small to medium sized business. Customer acquisition revenues represent joining fees from the group’s distributers, the sale of marketing materials and sales of equipment including mobile phone handsets and wireless internet routers. Customer management revenues are derived from the supply of fixed telephony, mobile telephony, gas, electricity and internet services to residential and small business customers. The group also provides bill payment protection and accidental death cover to customers for a monthly fee, for which it does not retain the insurance risk for. The company does not spend money on advertising but they have 44,000 independent distributers who sign up customers and then get a small cut of the revenues from each new member that they introduce. Telecom Plus has now released its final results for the year ending 2014.

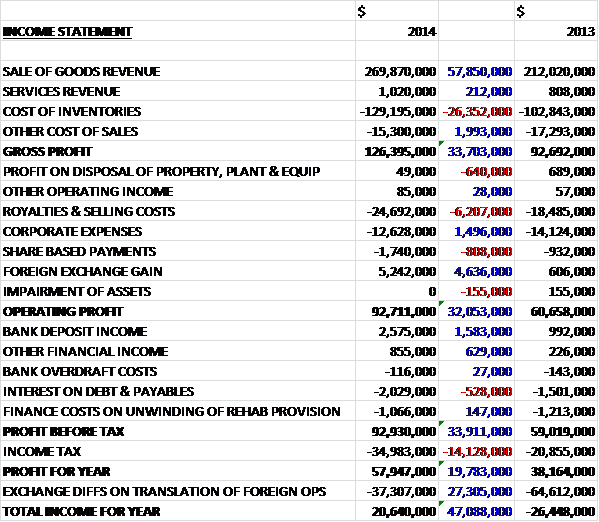

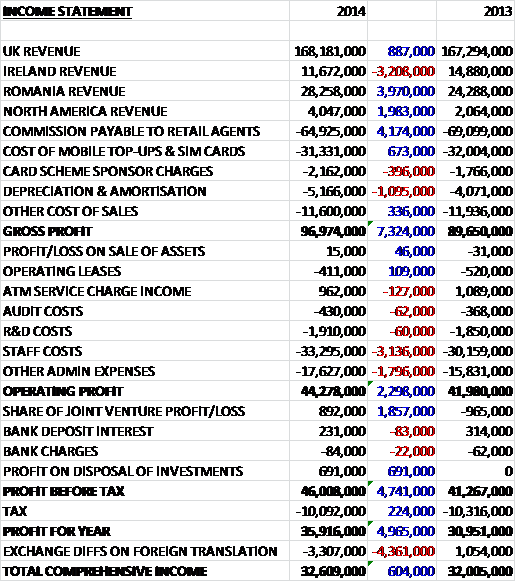

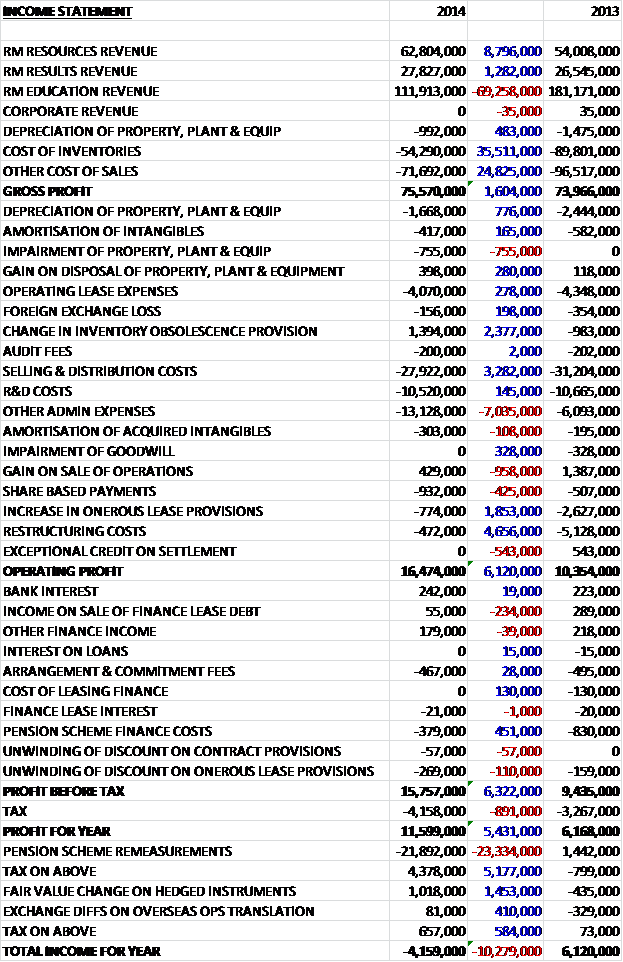

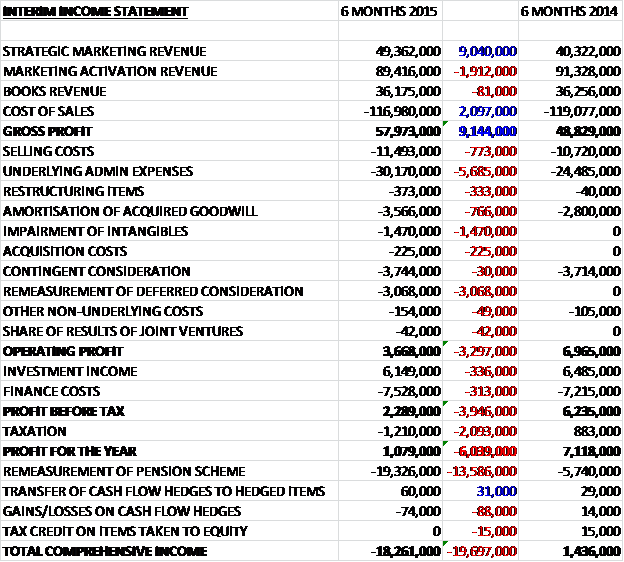

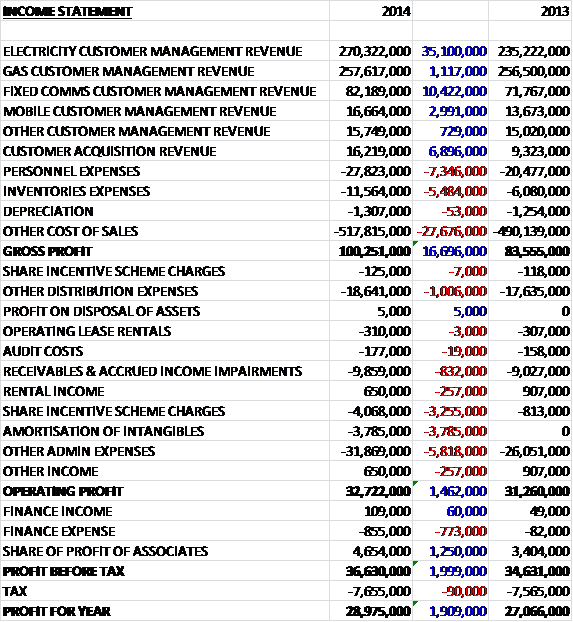

Overall revenues were substantially ahead of last year with particularly large increases seen in Electricity, Fixed Communications and Customer Acquisition revenue. Gas revenues increased by a more modest £1.1M as a result of the warm winter reducing demand. Staff costs increased by £7.3M with further recruitment being made in the second half of 2014 likely to mean another increase in costs next year, inventories expensed increased by £5.5M and other cost of sales were up £27.7M to give a gross profit some £16.7M ahead of last year. We also saw an increase in distribution expenses as a result of higher payments to partners following the continued organic growth and higher revenues; impairments; share incentive scheme charges; amortisation and other admin expenses due to higher staff numbers and telephony costs as the group introduced a free phone line for customer service calls, so that operating profit was just £1.5M above that of last year. An increase in finance expenses was more than offset by a £1.3M growth in profit from associates, relating to the 20% holding in Opus Energy, before a flat tax bill meant that the profit for the year was £1.9M above that of 2013 at £29M.

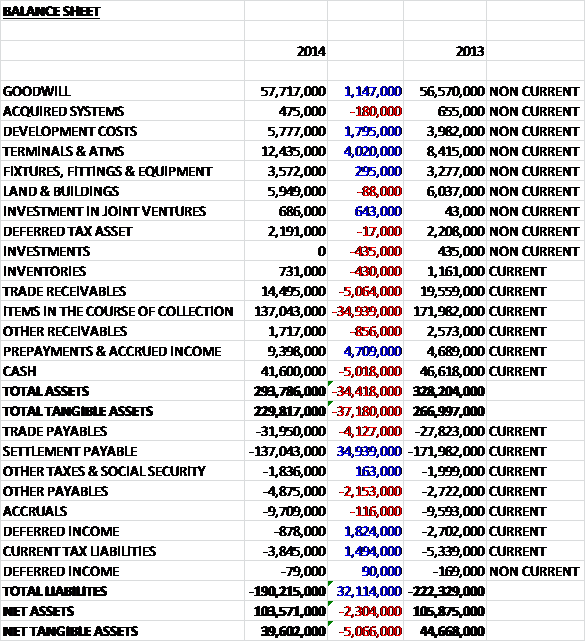

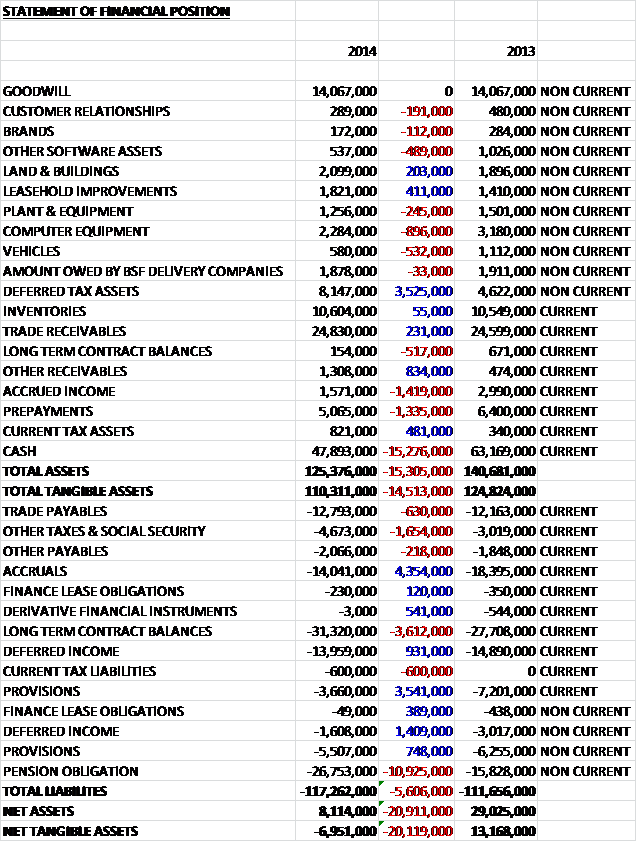

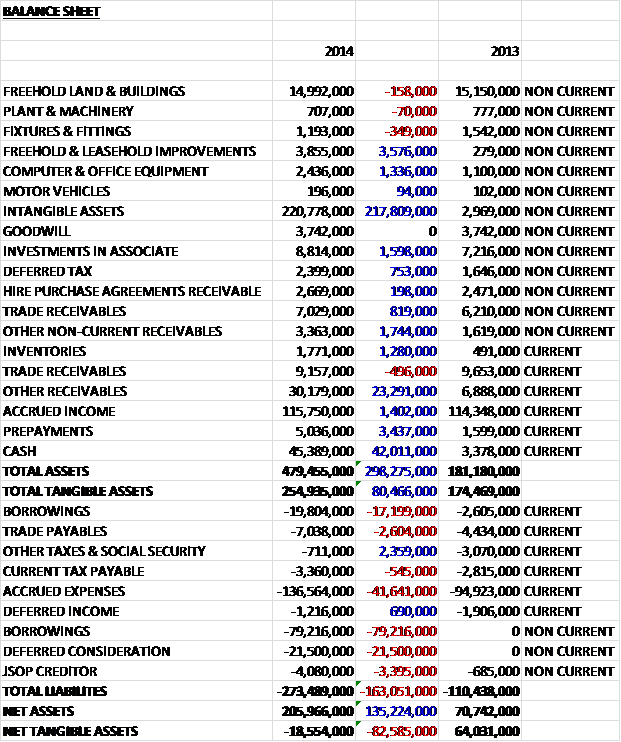

When compared to the end point of last year, total assets increased by £298.3M driven by a £217.8M increase in intangible assets which represents the “goodwill” spent on acquiring the Electricity Plus Supply and Gas Plus Supply from N Power as a result of the new energy supply arrangement, a £42M growth in cash and a £23.3M increase in “other” receivables. Liabilities also increased during the year due to a £97M increase in borrowings, a £41.6M growth in accrued expenses, a £21.5M increase in accrued income and a £3.4M growth in JSOP creditor so that net tangible assets fell by £82.6M to a negative £18.6M.

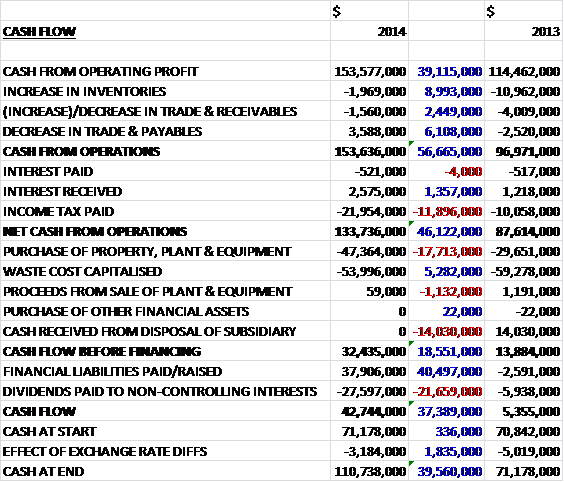

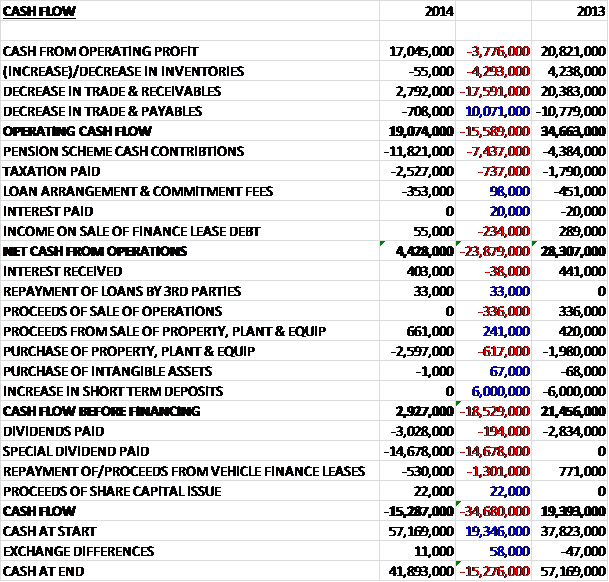

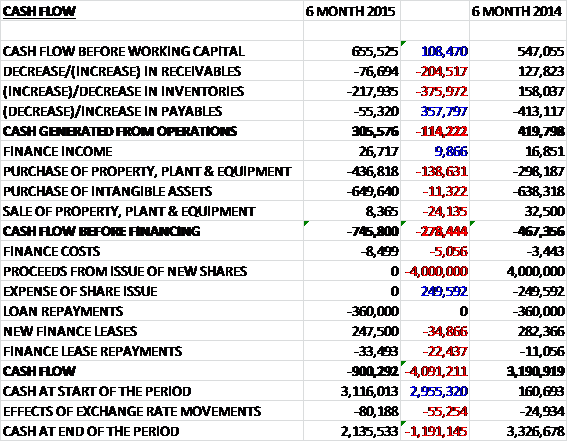

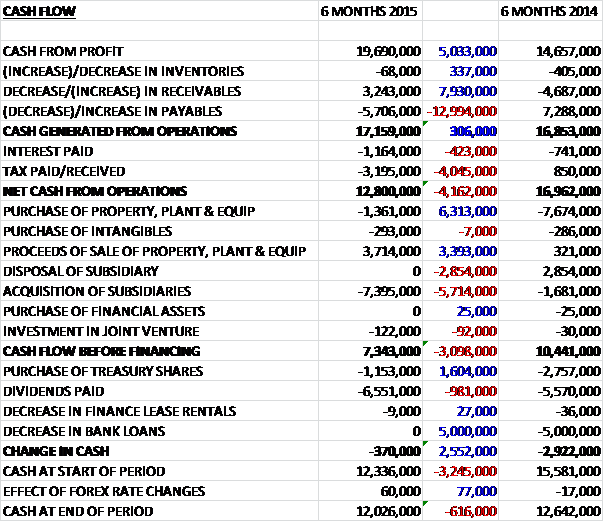

Before movements in working capital cash profits increased by £8.7M to £42.1M before a massive decrease in payables was only partially offset by a fall in receivables to give a £10.1M cash outflow from operations which became a £17.2M outflow after tax was paid. There was then £5.7M spent on capital expenditure, partially offset by a £3.1M received from the associate which was then dwarfed by the £138.5M cash outflow on the new energy supply agreement with N Power. This huge cash outflow was paid for with £100M of loans and £131.1M received from the issue of new shares which gave a cash inflow of £44.6M after the payment of £23.9M in dividends to give a cash level at the end of the year of £45.4M which doesn’t seem like a particularly good performance to me.

The group have seen a strong growth in the number of services being provided with a record increase of 305,000 during the year with a 32% increase in the number of mobile services being a particular highlight, although the additions during Q2 and Q3 were unusually high due to favourable market conditions and increase promotional activity that is unlikely to be repeated. There has also been a doubling in the proportion of new customers taking all five of their core services (gas, electricity, home phone, mobile and broadband) since the introduction of the new bundled structure with the average number of services taken by each residential member increasing from 3.54 last year to 3.64. Overall churn in the customer base has continued to decline, falling from 11.2% to 10.4% but the average revenue per customer fell from £1,363 to £1,302, the second highest amount ever, as the improvement in the quality of the customer base and slightly higher retail prices were more than offset by lower energy consumption during an exceptionally mild winter, further exacerbated by the comparison with the cold winter the year before.

Part of the differentiation for the group’s product is a high level of customer service which has been reinforced by Which who ranked them first in their fixed telephony and broadband supplier survey, helped by their UK based call centre. They also have a higher level of trust amongst their customers than any other utility supplier and a net promoter score between +40 and +45 against a backdrop of a score over 0 being considered acceptable, EON getting a score of -21 and the average among internet service providers being +9. As well as providing good customer service, there are a number of other incentives offered to Telecom Plus customers such as the cash back credit card where £4.6M was paid back to customers during the year, entirely funded by the retailers in the programme, and an online price comparison site.

The group have restructured the way they present and sell their services by introducing a range of “Gold” bundles with enhanced benefits and lower pricing available for members who take all their utilities from Telecom Plus which makes their multi-utility sales proposition simpler for new members to understand. They have also reduced the number of energy tariffs offered in order to comply with their new license obligations following Ofgem’s retail market review.

A number of new tools were launched during the year in order to help the partners promote the group’s services including a new film featuring Sir Terry Wogan to help explain the Discount Club and the benefits offered to new members, a simplified new online application process, an animated video to explain the part time income opportunity, an app which provides access in one place to all the main resources needed and an interest-free hire purchase scheme to enable them to acquire a tablet to take advantage of these new tools.

The group maintains a 20% share of Opus energy and this associate performed well during the year, increasing Telecom Plus’ share of the profits from £3.4M to £4.7M as a result of a continuing strong trading performance and the further progress that has been made in supplying gas alongside electricity into the small business and corporate sector, for which they are now buying renewable energy from over 500 small UK generators. The group expects to receive a dividend of £4.1M in July 2014 and the shareholding is recorded on the balance sheet with a value of £8.8M with the market value likely to be much higher than this. The board are very pleased to have this exposure to this rapidly expanding, profitable and highly cash generative business and I am inclined to agree with them.

One of the main events this year was the new energy supply agreement with N Power. As part of the deal the group acquired Electricity Plus Supply and Gas Plus Supply from them. The total consideration comprised of a payment of £196.5M and a deferred amount of £21.5M payable in December 2016, these payments have been recognised as an intangible asset, similar to goodwill. In order to help pay for this acquisition, the group entered into bank loan facilities of £125M comprising a transaction facility of £100M which was fully drawn down and working capital facilities of £25M, of which none was drawn down. In addition they had letters of credit in place relating to certain energy distribution charges with a total value covered of £11.8M. Of the £100M transaction facility, £30M is repayable by the end of 2015 with the remainder being payable by December 2016 – it is quite hard to imagine that the group will be able to pay this back out of their operational cash flow. As a result of this agreement, the group is enjoying lower energy costs which means that gross margins should be between 15% to 17% going forward instead of the 13% to 15% initially expected.

The group has some £7.7M of capital commitments relating mainly to the refurbishment of their new head office building and once this project is completed towards the end of next year, it will provide sufficient space to support the growth of the company for the foreseeable future and as far as systems are concerned, they have the capacity to manage a substantial increase in current customer and service numbers without the need for any further investment.

The directors of the company own about 23% of the total shares, with the chairman owning a huge amount of shares but there are also a number of institutional investors who own considerable amounts of shares with Standard Life owning 9% of the total equity of the company.

As far as risks are concerned, the group is not exposed to fluctuations in commodity prices due the nature of the agreements with wholesale providers in that they can pass the effect of any such fluctuations on to its customers. The sector is in the sights of politicians as the election gets closer but their wholesale energy supply agreement with N Power apparently insulates Telecom Plus from any margin pressure due to the proposed 20 month price freeze likely to be included in the labour party manifesto. Other recent regulatory changes such as the new requirements relating to smart meters, social tariffs and changes to the current decommissioning regime could all have a significant impact on the sector but on the whole new regulations tend to encourage competition which should be a benefit to Telecom Plus given its challenger status. Having said that, any windfall taxes or price controls would have an adverse effect if introduced.

One risk is the possibility that customers do not pay for their energy and potential fraudulent activity. During the year the bad debt charge increased slightly from £9M to £9.9M, partly due to an increase in the number of fraudulent applications for high end mobile phones during the first half of the year which triggered an immediate tightening of credit checking procedures. In order to combat non-payment by customers, the group is installing pre-pay meters where customers cannot or will not pay by any other means. The number of these meters installed increased by 8,958 to just over 50,000, representing under 6% of the energy services supplied compared to an industry average of about 15%. Weather can also have an effect on profits as during warm winters, customers do not use as much energy as during cold winters, which would therefore lead to lower revenue per customer.

Going forward, after reaching the 500,000 customer milestone this year, the focus is on doubling this to one million over the medium term which would represent a market share of only 4%, The improving quality of the customer base gives management good visibility with regards to future revenues and margins and the pre-tax profits next year (adjusted) should show a significant increase over the reported numbers this year reflecting strong organic customer growth achieved over the past year combined with the financial benefits of the transaction with N Power completed in December and as such they remain comfortable with market expectations of profits of £63M which represents a 50% increase. A number of potential new services are being looked at, including water, TV and insurance products.

Cash outflows in the new year are expected to be higher due to the new debt, the completion of the head office refurbishment and further support for the distribution channel with branded Minis and tablets. In addition, the group are expecting a modest rise in working capital requirements over the next two years due to the costs associated with funding the growth in the mobile business as customers can obtain a free premium handset at no upfront cost with a 24 month contract along with the above mentioned support for the distributers although N Power remains responsible for funding the working capital requirements associated with the energy budget plan customers.

At the current share price, after a 13% increase in the dividend, the shares yield 3.4% increasing to 3.8% on next year’s forecast. The board have stated that they remain committed to a progressive dividend policy but the rate of increase will be tempered over the next few years as the group repays the £100M of debt taken out to help fund the transaction with N Power with an increase of 15% expected in the coming year. The shares trade on a rather expensive P/E ratio of 26.6, although this is 20.9 when the incentive scheme charges and intangible amortisations are removed. This falls to 16.3 on next year’s consensus forecast, which looks a little better. The net debt position at the end point of the year stands at £53.6M compared to a modest net cash position of £800K at this point of last year.

This has been an interesting year for the group, profits are up but due to the supply agreement with N Power, net tangible assets are considerably lower than last year and turned negative. There are also £23.3M worth of “other” receivables on the balance sheet, a lot more than last year, and I can’t work out what these actually are which concerns me a bit. There was an operational cash outflow for the year, which is never good to see, mainly due to a huge reduction in payables (again, not sure what these relate to) so the operational cash flow before working capital movements is better than in 2013. Operationally, the group seems to be doing well with new customers, increased services, more services being taken by customers and reduced churn. The fact that the group is both cheap and does well with regards customer service bodes well for the future in this regard.

Clearly one of the most important events this year has been the new supply agreement with N Power. Following the theme of not actually getting much information from the annual report, I am not sure what the exact terms are but it seems Telecom Plus are getting cheaper energy in exchange for a big payment up front and a further £21.5M of deferred consideration due in 2016. Indeed, one theme is that there seems to be a lot of future cash outflows expected as in addition to the deferred consideration due in two years’ time there is also a £30M loan repayment due in 2015, £7.7M in head office refurbishments due within the next six months and the rest of the loan, a full £70M due in 2016 so there seems to be little chance of the group honouring this out of its cash flow so that will have to be renegotiated or new loans will have to be taken out. There is also uncertainty added into the mix by political uncertainty in a sector that has become quite political in recent times so whilst I do see this company as a good investment at some point, there just seems to be too many short term headwinds and uncertainties for be to invest at this time.