Following the integration of the courier operations into Parcels and the end of trading at UK Pallets, the group now only has two segments – mail and parcels. In recent years the courier business has been undergoing a transition away from a traditional same-day courier operation towards an operation which provides specialist service support to the parcels business, hence the integration.

The group has now released its interim results for the year ending 2016.

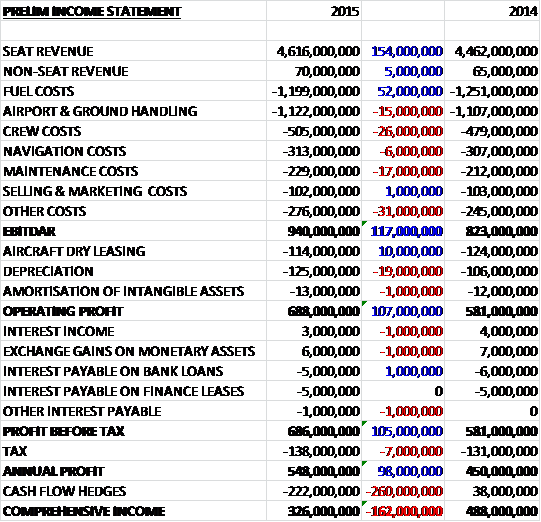

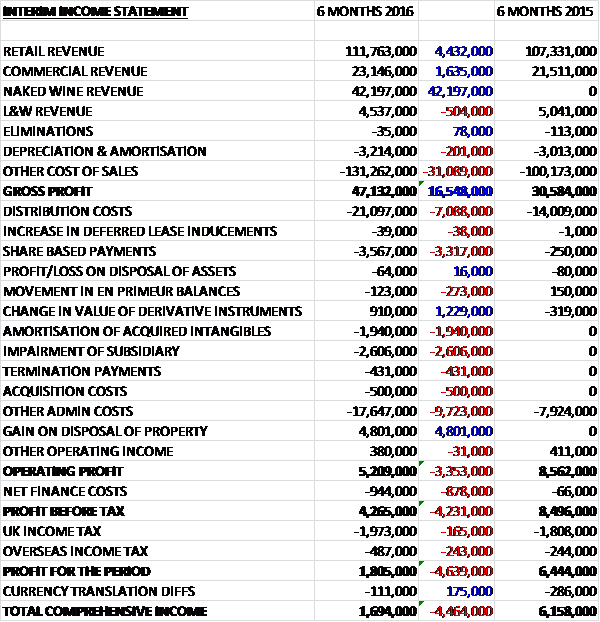

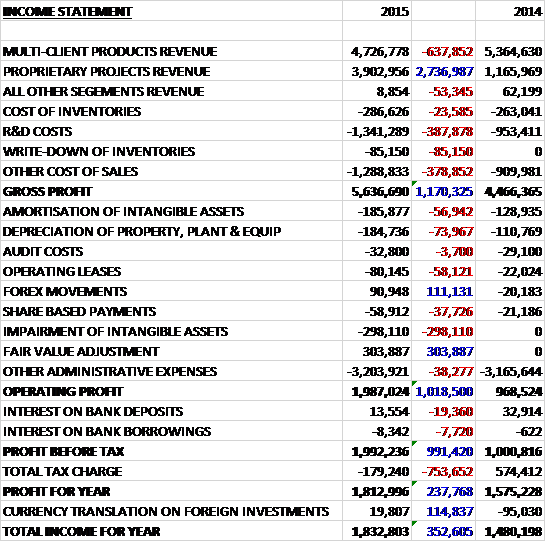

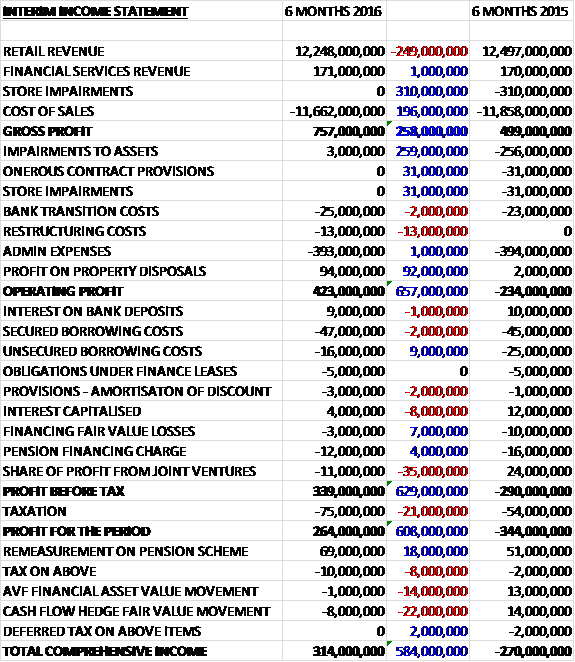

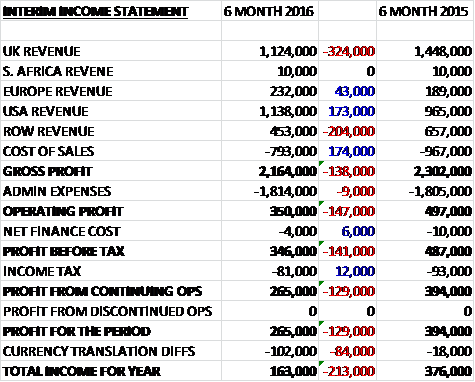

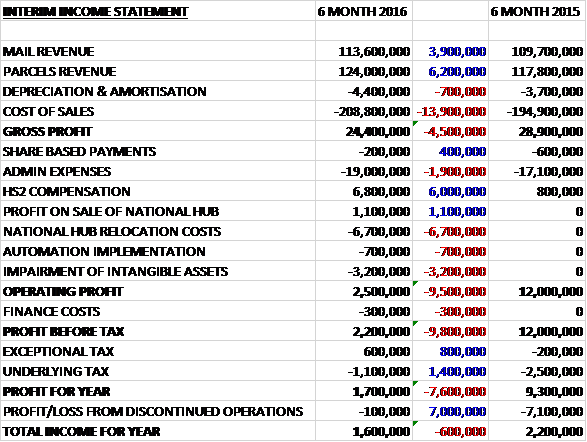

Revenues increased year on year with a £3.9M growth in mail revenue and a £6.2M increase in parcels revenue, but cost of sales grew further so that the gross profit was some £4.5M below that of the first half of last year. Admin expense also increased, up £1.9M, and hub relocation costs were broadly offset by the HS2 compensation. We also see a £1.1M profit from the sale of the old national hub but the automation implementation accounted for £700K in costs and there was a £3.2M intangible asset impairment to give an operating profit £9.5M down on last time. Finance costs increased slightly but tax was much lower so the profit from continuing operations was £1.7M, a decline of £7.6M year on year.

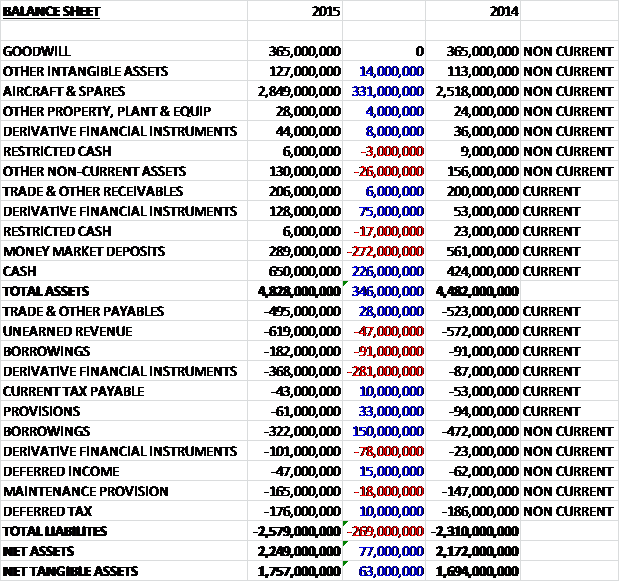

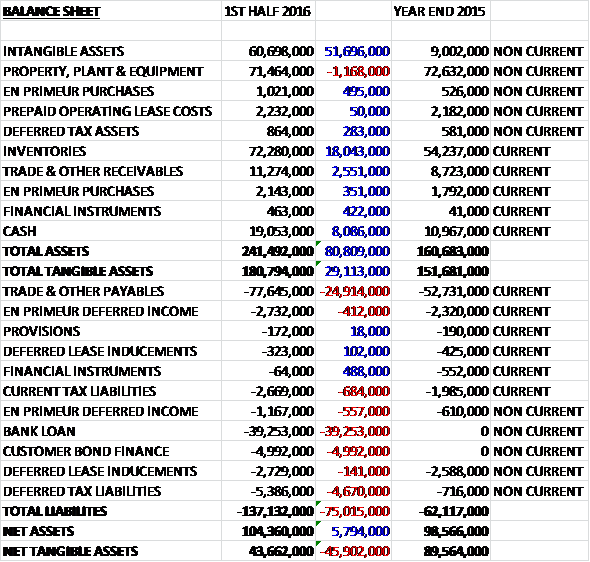

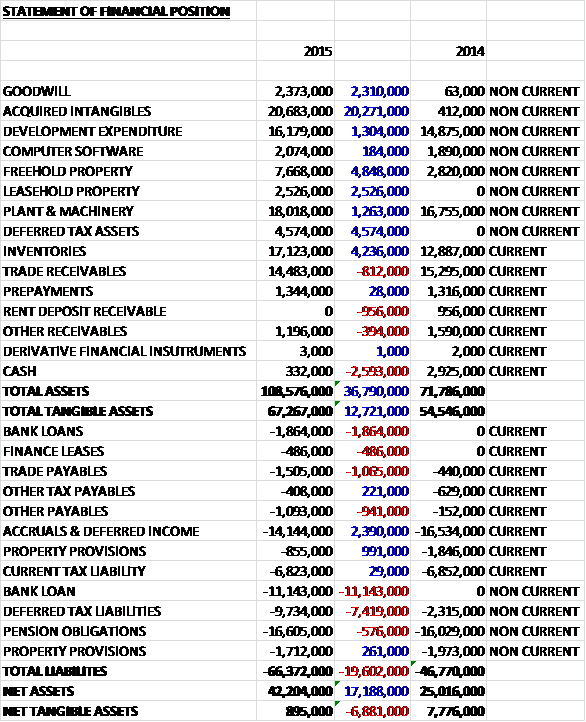

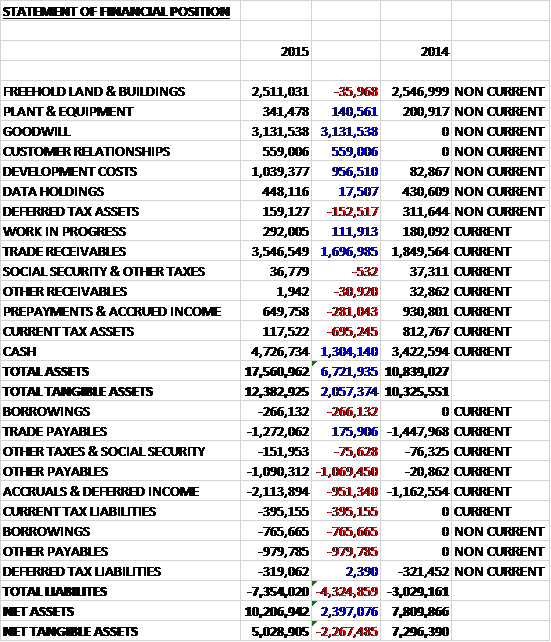

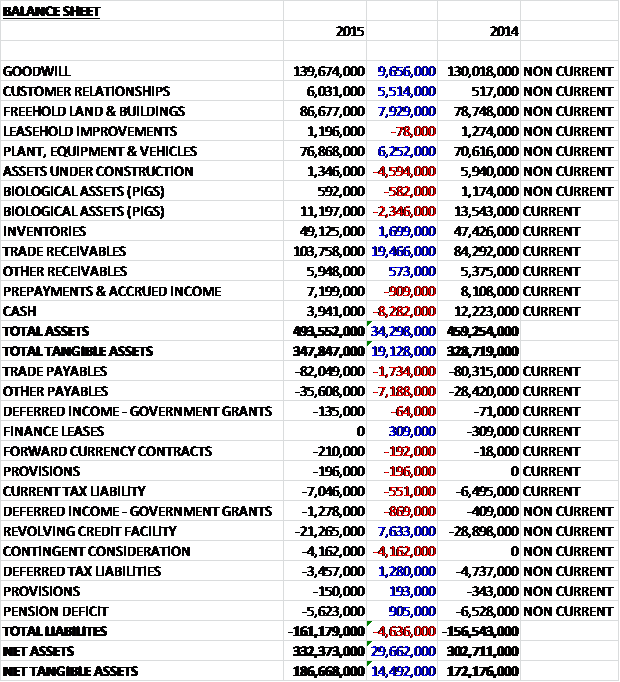

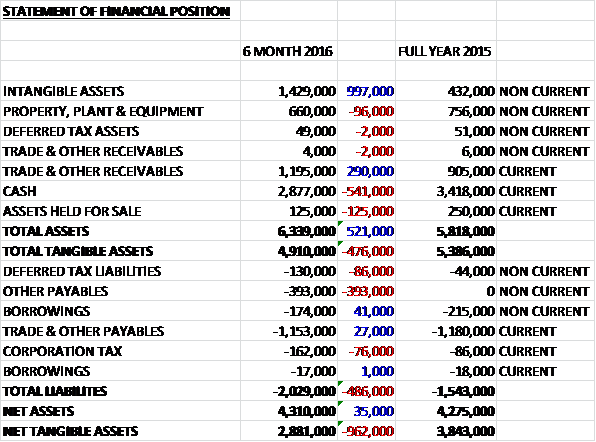

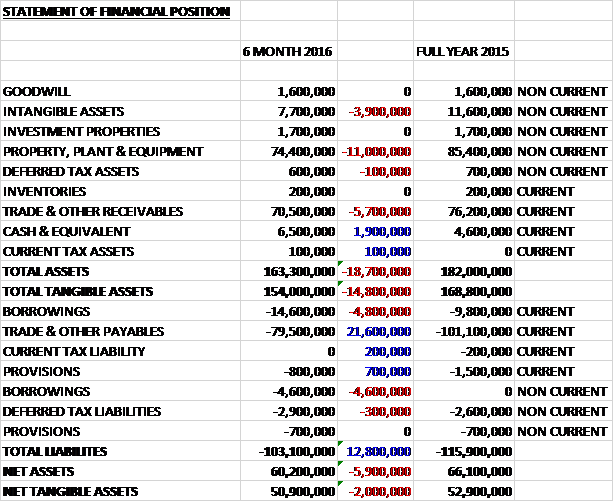

When compared to the end point of last year, total assets fell by £18.7M driven by an £11M decline in property, plant & equipment relating to disposals and HS2 compensation, a £5.7M decrease in receivables and a £3.9M fall in intangible assets, partially offset by a £1.9M increase in cash. Total liabilities also declined as a £21.6M fall in payables was partially offset by a £9.4M increase in borrowings. The end result is a net tangible asset level of £50.9M, a decline of £2M over the past six months.

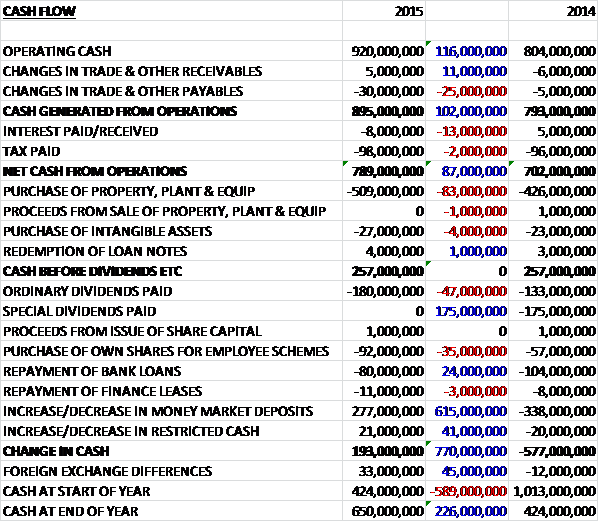

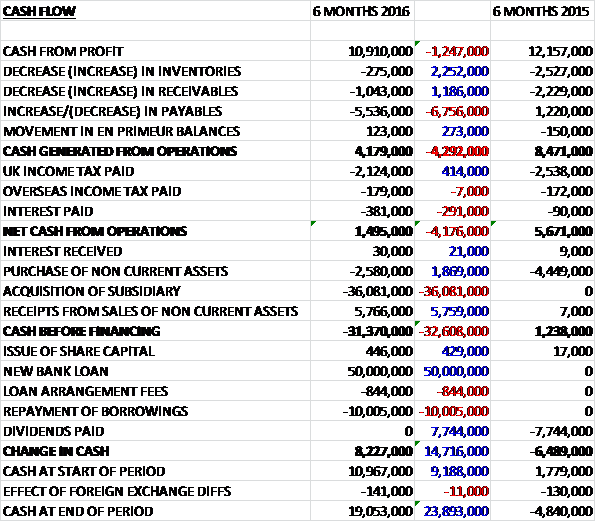

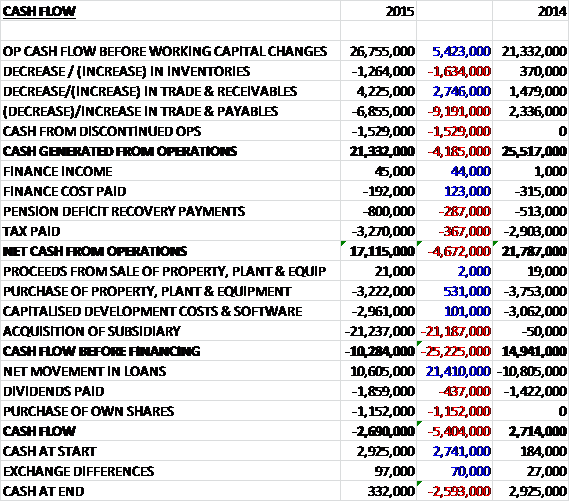

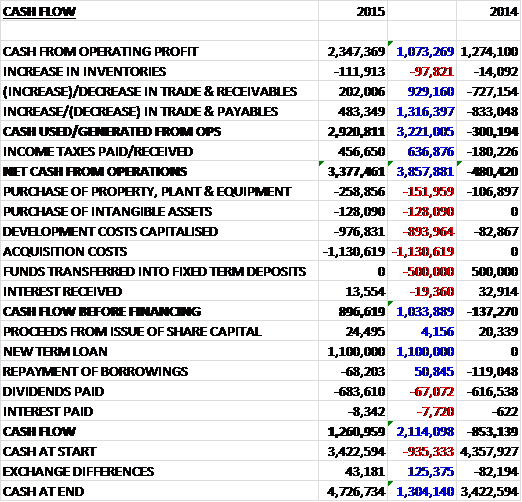

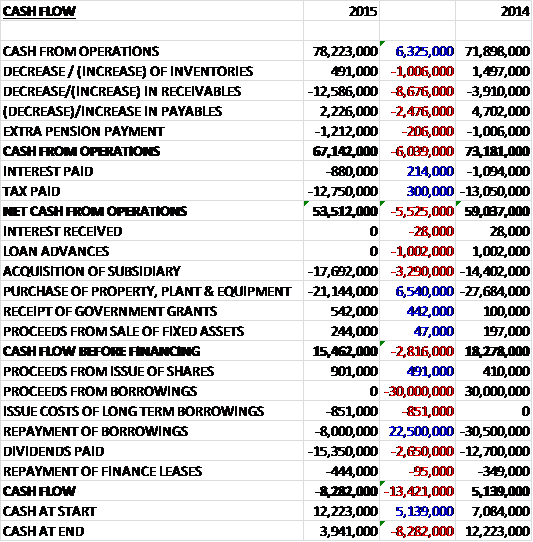

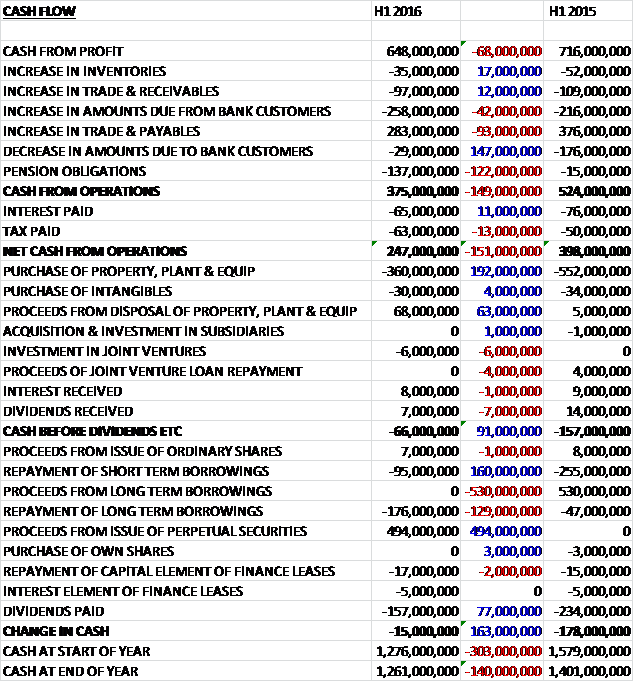

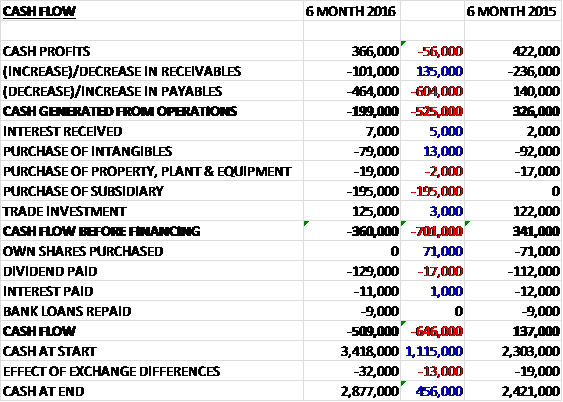

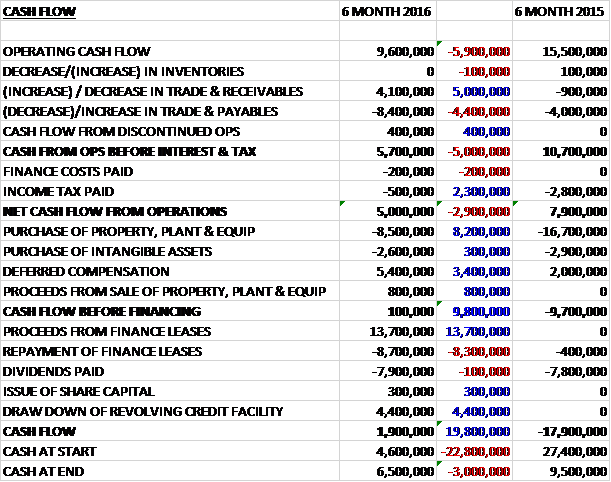

Before movements in working capital, cash profits fell by £5.9M to £9.6M. There was then a further working capital outflow due to a decrease in payables, although overall the cash spent on working capital was less than last time. After this, and a much lower tax payment, the net cash from operations came in at £5M, a decline of £2.9M year on year. The group then received £5.4M from the HS2 compensation but spent a net £7.7M on property, plant & equipment including £1.3M on the new hub and £1.5M in automation along with £2.6M on IT which meant that before financing, the group broadly broke even. They then took out a big finance lease and drew down on the revolving credit facility to pay the dividend and give a cash flow for the period of £1.9M and a cash level of £6.5M at the end of the first half of the year.

The operating profit at the Parcels business was £8.8M, a decline of £4.6M year on year on revenues that grew by 5.3%. This revenue growth as supported by average daily volume growth of 9%, reflecting some important new customer wins and weighted towards B2C customers due to the growth of online shopping. The impact of the sales mix effect combined with the increased operating costs the group have incurred as a result of the relocation of their operations, has meant that the parcels operating margin reduced from 10.7% to 6.3%.

As well as increasing operating costs, the operational issues related to the move to the new hub reduced volume growth slightly and resulted in an increase in customer churn. Following a detailed review, despite the fact the automated sortation equipment is working well and capable of delivering the anticipated benefits over the medium term, the group are facing a number of challenges as a result of a combination of inefficiencies in the new hub and the transport network. This, combined with the volumes of incompatible freight that cannot be handled by the new equipment, has placed added pressures on the new facility which resulted in the additional costs and the temporary reduction in service levels.

A detailed plan is underway to address these issues and therefore to restore the parcels business to its previous levels of profitability and to build from there. There are a number of near-term initiatives that have already eased the pressures on the hub, including securing additional, short term, hub capacity to ease the pressure on the main hub whilst the wider issues are being addressed. The efficiency of the hub will also improve as certain new larger customers come on board whose volumes arrive at the new hub throughout the day rather than just in the peak hours.

More widely, the plan involves re-engineering the line haul template to fully align it with the efficiency of the new hub, and a new operational plan for incompatible freight volumes with a new operations director joining early next year who should be instrumental in the execution of the plan after previously doing the same job at Parcel Force. Some progress has already been made. The sortation equipment is operating at target efficiency with an improving trend of volume performance in the latter weeks of the period; service levels are now back to where they should be; and there are a number of significant potential customers keen to use the services available to the group through the new hub. They will be managing their customer acquisition and overall volumes very carefully, however, as they approach the Christmas period with a focus on profitability and service levels to current customers.

Good progress is apparently being made with product innovations in the division. These include Retail Today, a same day delivery service combining the parcels and courier operations; and ipostparcels, which represents one of the lowest-cost online collection and delivery services available in the UK. Revenues and profits grew well for these operations and the group continues to invest in further enhancing their services in these areas.

Key to the parcels market position is the provision of value added services that customers increasingly demand. The enhanced next day delivery service, which offers advance-notice one hour delivery and collection windows, is now fully operational and is consistently achieving strong service levels of over 95%. In addition, their sales initiative, carrier of contingency, is proving successful with three major retailers already won. They are also progressing parcel drop-off and collection points, with a trial in place with a national multi-site retailer.

The operating profit at the Mail business was £4.9M, a fall of £1.3M when compared to the first half of last year on revenues that increased by 3.6%. Daily mail volumes grew by 8.1% compared to a market that saw an overall volume decline of some 5% demonstrating market share gains. This volume growth was driven by strong customer retention and new customer wins. The competition in the market, however, meant that operating margin fell from 5.6% to 4.5% which is apparently back within the target range after H1 2014 benefited from a particularly favourable product mix. The business has a healthy pipeline of new business opportunities and the group saw continued good progress from imail and related new product innovations.

There are a number of substantial competitor accounts currently out for tender, and the group are seeing a significant success rate in these, albeit with some pricing pressures. Imail, the web-to-print postal service, continued to show good revenue growth. They continued to invest in the product to increase capacity and provide additional services with imailprint being successfully launched. This provides a specialist printing service which, rather than being purely mailed as with the current service, can produce printed documents for general usage. The board see this as a medium term low risk growth opportunity that used the existing infrastructure.

A key growth element of the Access Mail market is the rising popularity of packets, a segment that the group estimates currently represents some £200M of the total Access Mail market of £1.5BN. Whilst they have made some progress in this area in recent years, their share of the packets market remains very low and the business is now being reinvigorated, with investment in specialist automated packets sortation equipment and an increase in the size of the sales team. The board expect to see an impact from early 2016 and it is believed that this area will be key to growing mail revenues and profitability in the future.

As previously mentioned, it has become clear that the near-term challenges associated with the transition have been more significant than originally anticipated. Trading in the initial weeks of the second half has been in line with the revised expectations and expectations for the current year therefore remain in line with previous guidance but due to the timescales required to fully resolve the challenges, the expectations for the next year have softened slightly. The transfer to the new automated facility in Ryton was completed in July and after some initial teething issues, the service levels are now back where they should be in time for the Christmas trading period.

As with most companies it seems, there were a number of non-underlying items during the period. The £1.1M profit on the sale of the national hub represents the compulsory acquisition of the Birmingham hub by the DfT and HS2 as a result of the proposed HS2 railway. There was also a compensation payment of £6.8M reimbursed from the DfT (compared to £800K during the same period last year). The £700K cost relating to automation implementation represents the costs incurred as the group moved towards the roll-out of new automation equipment comprising £500K asset write-offs and £200K of contract termination costs.

The £6.7M of national hub relocation costs comprise of £3.7M of disturbance costs including recruitment and redundancy costs, £2.5M dual running costs which were largely property costs relating to running two sites whilst relocating, £300K compensation paid to customers following a temporary deterioration in service performance, and £200K in relation to the loss of profit resulting from the delay in increasing the hub’s extended capacity. The £3.2M impairment of intangible assets occurred after the group undertook a strategic review of its IT systems during the period which identified a number of software assets that did not fit within the medium and long term strategic goals of the group which offered no future economic value to the group. Last year there was a £7.3M goodwill impairment relating to the discontinued Pallets business and this year there was a further £100K of costs as the group administers the business’ liquidation.

The group has committed bank facilities in place, comprising a five year £25M revolving credit facility available until the end of May 2019 with £14.4M drawn at the period end, and a £20M overdraft facility available until the end of 2015. At the period-end, the group had committed capital expenditure of £1.4M which is a considerable reduction on last year.

In November, after the period end, the group agreed a final compensation payment of £10.3M with the DfT with the funds expected to be received before the end of the calendar year 2015. This final costs mean that the group’s contribution in total to the move will be £12.4M which covers the enhancement of the site and building beyond the scale of the previous facility with some £18.4M in total spent on automation. The costs of the move, including the IT data centre move and related staff costs, have now been largely incurred with some £600K relocation costs expected in the second half of the year with final payments relating to automation of £1.3M also expected to be incurred.

The parcels business is generally busier in the second half of the year due to the Christmas trading period but mail does not have any real seasonality.

At the end of the period the group had net debt of £12.7M compared to £5.2M at the end of last year. The shares are currently yielding 6.1% increasing to 6.7% on Investec’s current forecast but I don’t think that has taken into account the reduced dividend payment likely so I don’t see this as sustainable.

Overall then this has clearly been a difficult period for the group. Profits were down, net assets declined and operating cash flow fell with no free cash generated to speak of. The parcels business struggled due to the higher costs associated with the relocation of the hub but apparently steps are being taken to address these issues. The fact that a decent portion of the parcels are not compatible with the automation machinery is a real problem in my view. Mail profits were also down, with this performance being blamed on strong comparatives with H1 last year and strong competition. It seems to me that the group is grabbing a lot of new market share but at the cost of reduced margins – I hope they have done their sums right and these new contracts are actually profitable.

The expectations for next year have now softened but the £10.3M to be received from the DFT will really help the company and has perhaps been overlooked by the market. In some ways I feel that this is getting close to being an interesting opportunity as the bad news may now all be in the share price and there is a pretty solid balance sheet backing up this business. This sector is cut-throat, however, with City Link going out of business last year and DX recently warning on profits. Also, the temporary reduction in service levels may have a greater knock on effect than is being acknowledged given the competitiveness of the industry. Overall, although these shares look more tempting now I think I will hold off to see how the Christmas trading period goes.

On the 25th November it was announced that CEO Guy Buswell was stepping down with immediate effect after spending ten years in the role. The non-executive chairman and founder Peter Kane will become interim executive chairman. Clearly the board has grown tired of the disruption surrounding the new hub and automation.

On the 12th January the group gave a Q3 trading update. Overall the performance in the quarter was in line with management expectations. The parcels business delivered good volume growth of some 8% compared to the same period last year. This growth was largely driven by an increase in internet shipping related home deliveries. The new automated hub operated very well throughout the peak period, and is starting to achieve good throughput levels so strong customer service was maintained through this busy trading period. The mail business achieved satisfactory volume growth of 2% but due to mix of sales, revenues were down compared to the same period of last year.

Overall not a bad update but it’s not quite strong enough to entice me in yet given the cut throat competition in the industry.

On the 27th January the group announced the appointment of Chris Mangham as IT director. Peter Fuller will also joint as Operations Director. He was most recently Operations Director at Parcelforce.

On the 6th April the group issued an update for the year ending 2016. Revenues for the year are expected to show a 1% decrease and pre-tax profit is anticipated to be in line with management expectations. Overall revenue growth has been impacted by a continued mix effect in the mail business which is expected to result in a revenue decline for the year of some 3% despite mail volumes being up by about 5%.

The parcels business is expected to achieve volume growth of about 4% but growth in Q4 suffered due to the spike in volumes in the comparative period in 2015 as a result of the demise of City Link. The new automated hub continues to operate well and achieved good throughput levels and the group are making further progress with their plans to improve the efficiency of their network in markets that remain highly competitive.

Overall then, not much to get that excited about here in my view.