Omega Diagnostics has now released its interim results for the year ending 2015.

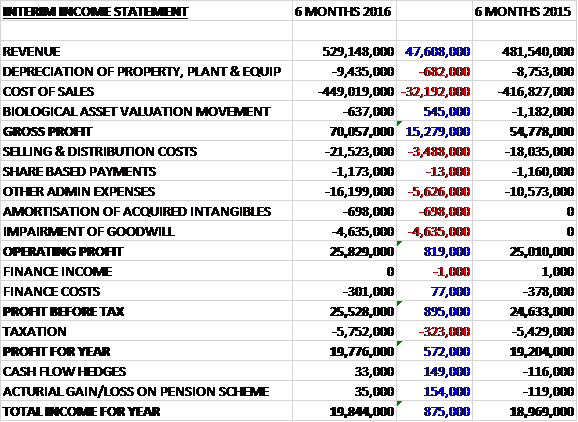

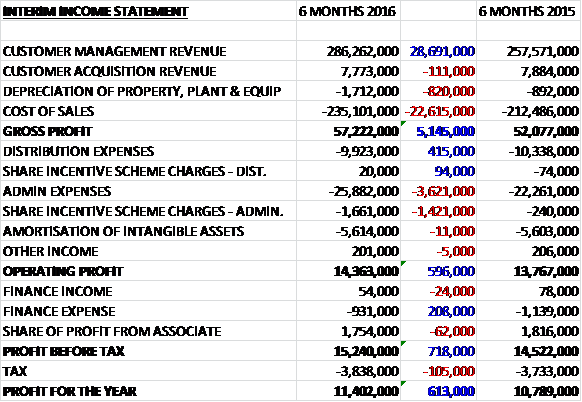

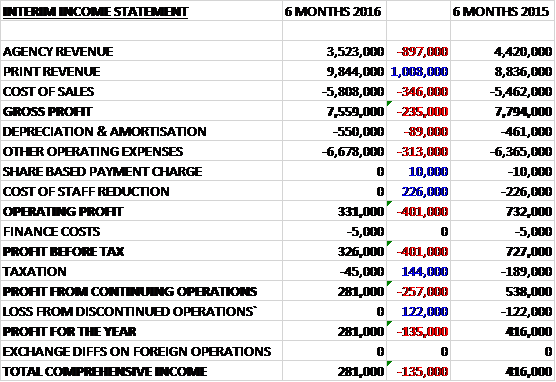

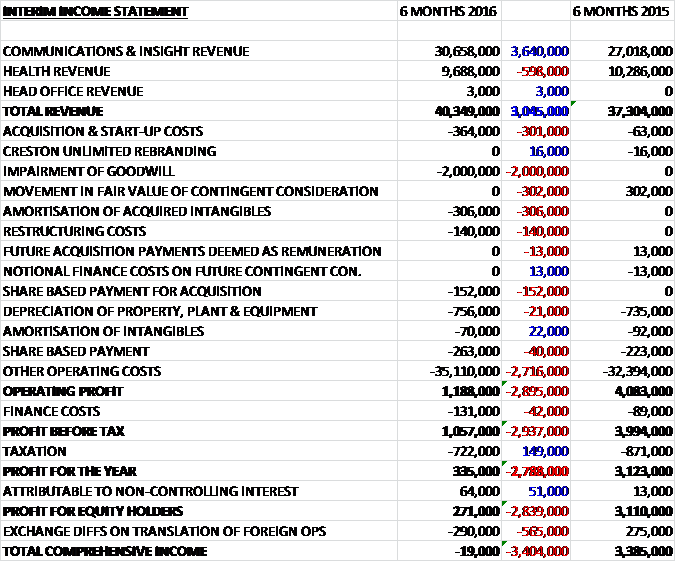

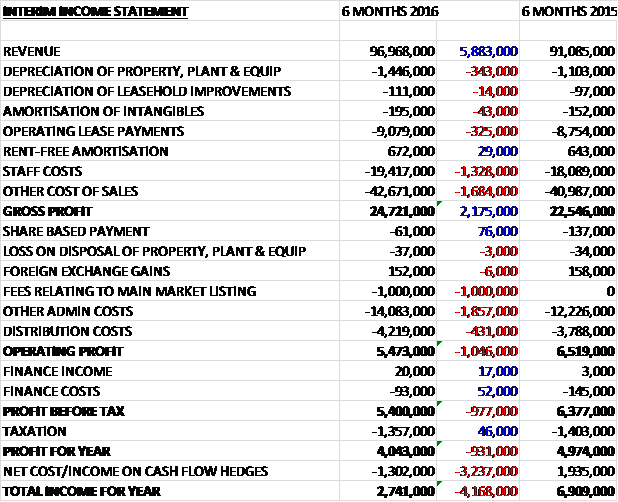

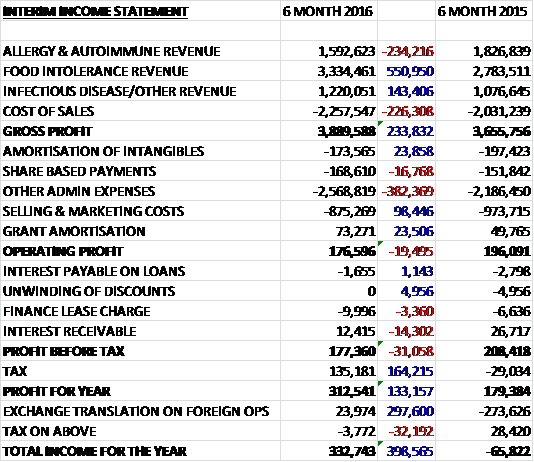

Revenues increased when compared to the first half of last year despite the adverse £180K effect from strengthening Sterling as a £237K decline in allergy & autoimmune revenue was more than offset by a £556K growth in food intolerance revenue and a £143K increase in infectious disease revenue. After a growth in cost of sales, the gross profit was £234K ahead of that of last time. Admin expenses increased by £382K and a £98K fall in selling and marketing costs were not quite enough to prevent the operating profit falling £19.5K. We then see a reduction in the interest received more than offset by a £164K positive swing in tax due to an increase in the deferred tax asset as a result of R&D tax credits to give a profit for the first half of the year of £313K, a growth of £133K year on year.

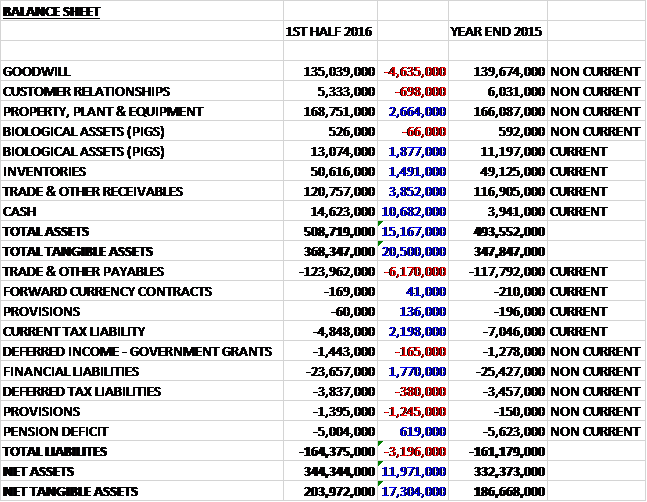

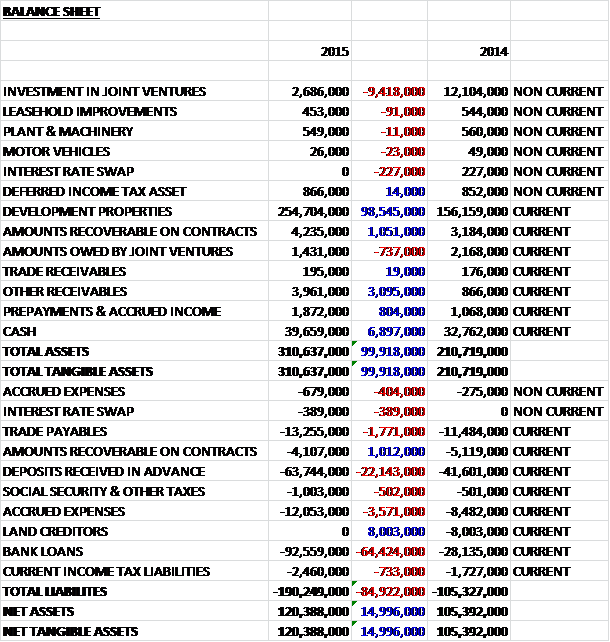

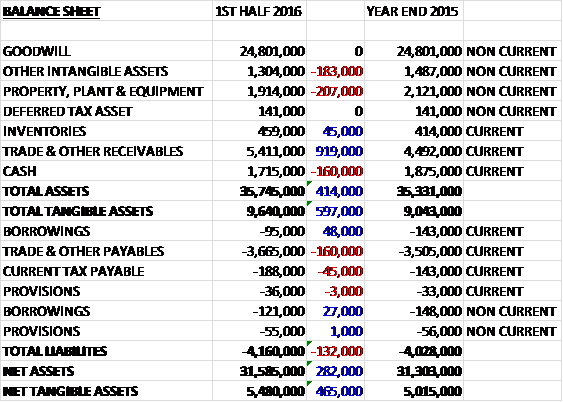

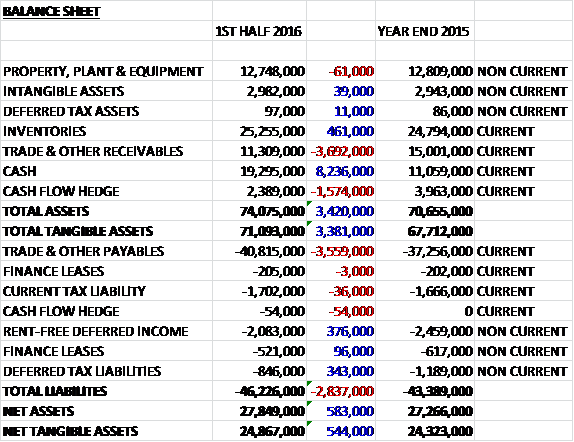

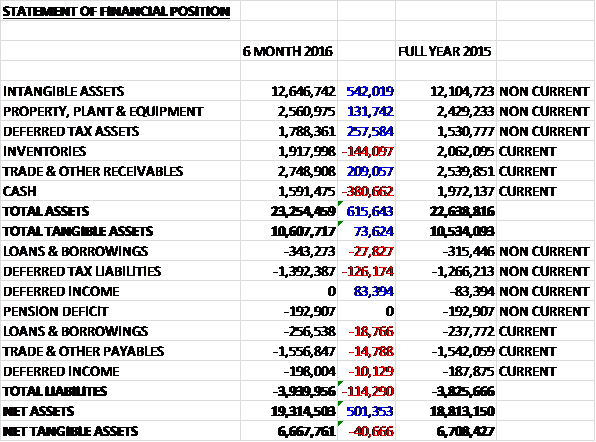

When compared to the end point of last year, total assets increased by £616K driven by a £542K growth in intangible assets, a £258K increase in deferred tax assets and a £209K growth in receivables, partially offset by a £381K fall in cash levels. Total liabilities also increased during the six month period as a £126K growth in deferred tax liabilities was partially offset by a £73K fall in deferred income. The end result is a net tangible asset level of £6.7M, a decline of £41K over the period.

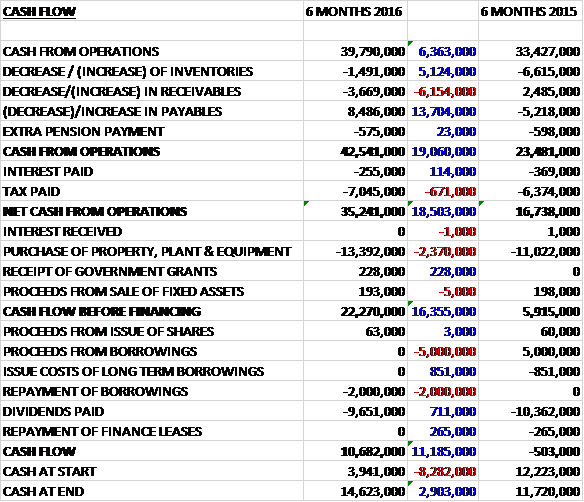

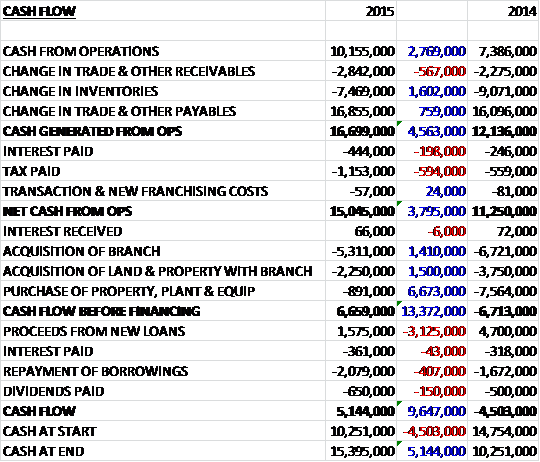

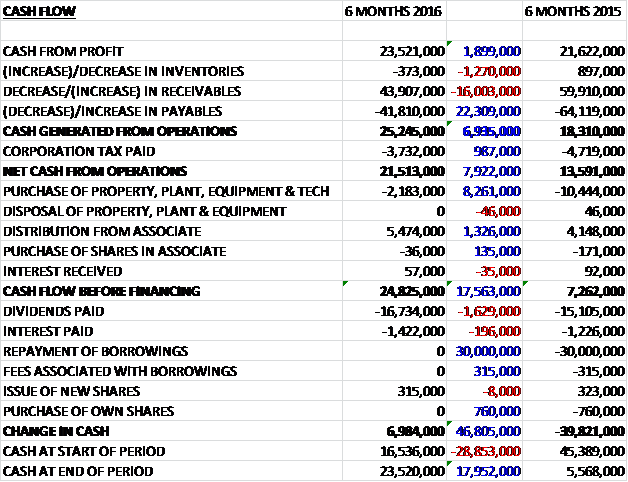

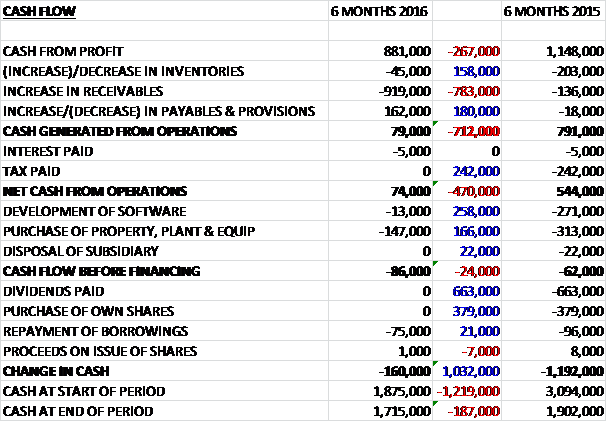

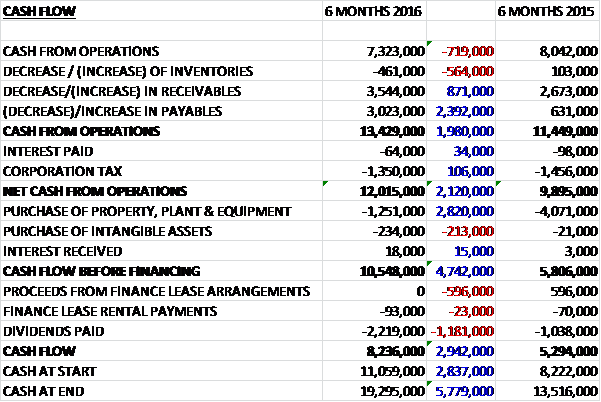

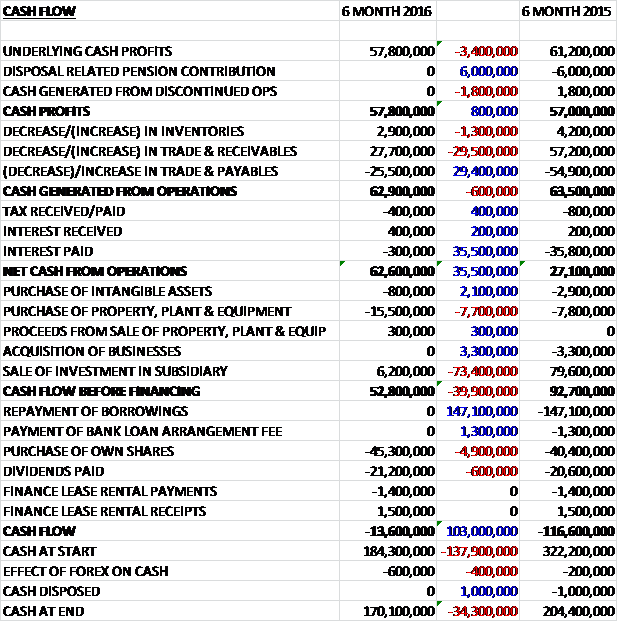

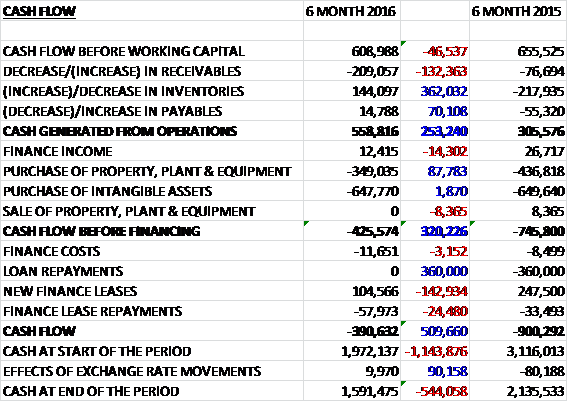

Before movements in working capital, cash profits declined by £47K to £609K. Despite showing a small cash outflow, the cash performance from working capital improved when compared to last year, mainly as a result of a fall in inventories to give an operating cash flow of £559K, an increase of £253K year on year. This did not cover the investment into intangible assets (presumably R&D) and after the £349K spent on tangible assets, there was a cash outflow of £426K. There was a net increase in finance leases which gave a cash outflow of £391K in the six month period and a cash level of £1.6M at the period-end.

Overall the first half performance was in line with management expectations. The group are in the process of putting together a three to five year business plan which should be interesting. The automated allergy product is approaching the point at which the group can begin to earn a commercial return but things are not progressing as well with Visitect CD4. They are systematically progressing with all the potential variables which takes time and there is apparently no guarantee of a positive end-result so this product is looking more and more precarious to me. There are, however, growth prospects in the food intolerance area given the greater understanding of the gut microbiome and the interaction between the food people eat and their overall wellbeing.

The pre-tax loss in the allergy and autoimmune division was £154K, a £49K increase year on year. The business has suffered the duel headwinds of a weaker exchange rate and a declining business in the domestic German allergy market. Whilst autoimmune sales grew by 17% to £300K, allergy sales declined by 18% to £1.29M with half the reduction due to the currency impact. Unfortunately the allergy business is higher margin so this decline has a bigger effect on profits.

The pre-tax profit in the food intolerance business was £1.1M, an increase of £188K when compared to the first half of last year. Food Detective continues to be popular, exhibiting growth in eight out of the top ten markets in the EU, Latin America and the Far East. The Foodprint System has also grown across those markets and included a significant customer win that will lead to sizeable repeat business.

The pre-tax loss in the infectious disease division was £204K, an increase of £39K year on year. The market is the most congested in which the group operates which results in the most price pressure. Revenues did increase, however, with stronger performances in Africa, the Middle East and the UK.

It was previously reported that there was a stability issue with Visitect CD4 that manifests after five weeks storage at room temperature. The group built additional devices to monitor ongoing stability, both up to and well beyond the five week period to attempt to establish a cause for the instability and to gain a better understanding of the time over which the problem might occur.

The group then reported an ambient temperature effect which manifests as a change in test line signal, with no corresponding change in reference line signal identified as being linked to a single step. The group have not been able to replicate the stability issue and they now have data which provides evidence for little or no decline in test performance at ambient temperature six months after being manufactured. In addition, the pilot batches showed no further deterioration in performance when tested four months later.

They have identified the cause of the ambient temperature effect and have found a potential solution to it which they are trying to incorporate into the test. In terms of the ongoing investigations, they are where they expected to be at this point in time and remain committed to the development plan and once they have a satisfactory design they will recommence the verification and validation work plan. So that is all as clear as mud then.

In Pune, India, the group has completed the fit-out of their new rapid test manufacturing facility and are currently installing equipment, IT systems and quality management systems. They are planning to manufacture a range of Malaria tests at a much lower cost of goods to expand the market reach significantly beyond the limited coverage of the current product range.

Since the last update, the group have optimised another allergen so that 37 allergens now match the performance of the market leading product. In addition to the successful Spanish evaluation, with the help of the partner Immunodiagnostic Systems, they have now commenced an evaluation in Italy with further ones planed for France and Germany in the near term. They are building up an extensive set of data which supports the speed and ease of use of their Allersys Reagents on the instrument and they expect to obtain CE marking early in the new financial year.

Overall then, this was a bit of a subdued half year from the group. Profit was up, but this was due to R&D tax credits and pre-tax profits fell. Net tangible assets were also down, and although operating cash flow increased, this was only because of the increase in inventories last time and cash profits fell year on year and no cash was produced if we count the development expenses as operating costs. The only segment performing well is the food intolerance business with profits being boosted by a big customer win. Unfortunately these gains were offset by an increase in the infectious disease loss due to tough competition and a similar increase in losses in the allergy business due to Euro weakness and continued declines in the German market.

The comments about the Visitect CD4 device are a little concerning. They have found a potential solution to the issue but there is no guarantee of a positive end result. On the other hand the allergy product is reaching commercial viability. So, these results suggest that the food intolerance isn’t quite profitable enough to carry the other divisions and the shares are certainly pricing some success in at the moment. I suppose the question is, would a successful allergy product be enough to offset the disappointment from a non-viable Visitect product? Obviously I don’t have the answer to that but I am keeping these shares for now as a speculative punt.

On the 21st April the group released a trading update covering the year ended 2016. Overall results will be in line with market expectations. Revenues are expected to be £12.7M, 5% ahead of last year, and adjusted pre-tax profit will be between £1.2M and £1.3M. Food Intolerance revenues are expected to be £7.1M, a growth of 19%; allergy revenues are expected to be £3.2M, a decline of 13% and infectious disease revenues are expected to be £2.5M, a decline of 1%.

In allergy, the group have now reached their target and have optimised 41 allergens which will be included in the initial launch panel. All of the Allersys reagents have been evaluated on the IDS iSYS analyser to demonstrate performance that matches the market leading product. They are currently in the process of building up inventory levels to support a market launch in the near future and the scientific team is already working on delivering menu expansion beyond the initial launch panel.

External evaluations have now been completed in Spain, Italy and France with a fourth ongoing in Germany. Of the three completed beta studies to date, they have now tested over 1,000 patient samples with 18 different allergens from the range and results are in line with the initial claim support work. These external evaluations in conjunction with the claim support work will enable the group to CE mark all 41 allergens during the early part of the coming year in readiness for launch.

In infectious diseases, the group have now determined the root cause of the ambient temperate effect in the CD4 devices and have demonstrated that they are able to manufacture prototype tests for a lab setting which are capable of operating between 15 and 32 degrees. They are mow working with design engineering companies to incorporate a solution that eliminates the issue to enable the test to be used in the field. The board remain confident that they will be able to find a solution.

They have also established that finger price and venous blood give equivalent results and the board believe the difference seen in the Indian study was due to the then unidentified ambient temperature effect. Beyond this, they are also working on extending the test performance to demonstrate that it will operate up to 35 degrees. On being able to achieve this level of performance on a consistent basis, they will continue with their planned programme of validation work.

The Food intolerance business is currently the driver of growth for the group. The allergy business in Germany continued to decline as the group saw a reduction in buying levels due to increased competition for reimbursement with tests for other conditions. The market in the country is also being squeezed from the automated lab test sector but this should reverse once the Allersys range of tests are launched. The group have maintained their established customer base and are also expanding the panels of tests available on their Allergodip dipstick test. This, alongside introducing a mobile phone app that allows quantification of the test result with provide them with a broader product offering.

Overall, this is a decent update. The food intolerance business is performing well and although the reduction in the allergy business is disappointing, the launch of the allersys system should provide a boost. The CD4 product still seems a long way off but at least some progress is being made on identifying the issues with the test. Overall I will continue to hold here.