QinetiQ provides testing facilities for high-tech defence applications, among other things. Revenue is recognised once the group has obtained the right to consideration in exchange for its performance. When the outcome of a contract can be estimated, revenue and costs are recognised by reference to the stage of completion of the contract activity at the balance sheet date. Amounts recoverable on contracts are included in trade and other receivables and represent revenue recognised in excess of amounts invoiced. Payments received on account are included in trade and other payables and represent amounts invoiced in excess of revenue recognised.

EMEA Services provides technical assurance, test and evaluation and training services, underpinned by long-term contracts, the most significant of which is the long term partnering agreement for test, evaluation and training services which has been delivered to the MOD over the last twelve years. The division is also a market leader in research and advice in specialist areas such as C4ISR, procurement advisory services and cyber security. The C4ISR business provides research, advice and bespoke solutions for secure communications, command and control, surveillance sensors and information management. In the “Explore” category the training business uses commercial off the shelf technology to connect people and assets for mission rehearsal and tactic development.

The air business de-risks complex aviation programmes; the weapons business supplies independent research, evaluation and training services for integrated weapons systems; the maritime business provides independent technical advice and support, particularly in the areas of platform performance, stealth, command information systems and systems integration; and the Australian division provides advice and services predominantly to government customers. The business is underpinned by two long term contract with the Australian Department of Defence – one contact is focused on the provision of engineering services workshops with the other one that supports the airworthiness of military aircraft. The Procurement Advisory Services provides tender assessment, cost and analytical services principally to support complex procurement programmes in highly regulated markets.

The US Products business involves contract-funded R&D and products that protect people and assets such as military objects; the Optasense business is a bespoke fibre sensing business that delivers decision ready data to multiple markets; the Space Products division provides satellites, payload instruments, sub-systems and ground station services; the EMEA products division provides research services and bespoke solutions developed from IP spun out from other divisions.

The group rarely competes directly with aerospace and defence companies but instead provides research, technical advice and test and evaluation across all military domains and the majority of equipment programmes through the LTPA and other key contracts. The core markets are defence, security and aerospace. Much of the revenue is derived from longer-term contracts with known dates for renewal and re-tender. These contracts exhibit relatively low risk characteristics with low capital requirements and strong, predictable cash flows.

The group has a special shareholder in the shape of the UK MOD and they are required to obtain their consent if at any time the chairman is not a British citizen and they propose to appoint a CEO who is also not British and vice versa. There are other rights too, including the option to purchase defined strategic assets of the group in certain circumstances such as testing and research facilities.

In 2003 the group entered into a long term partnering agreement to provide test and evaluation facilities and training support services to the MOD. This is a 25 year contract with a total revenue value of up to £5.6BN depending on the level of usage by the MOD.

Qinetiq has now released its final results for the year ended 2015.

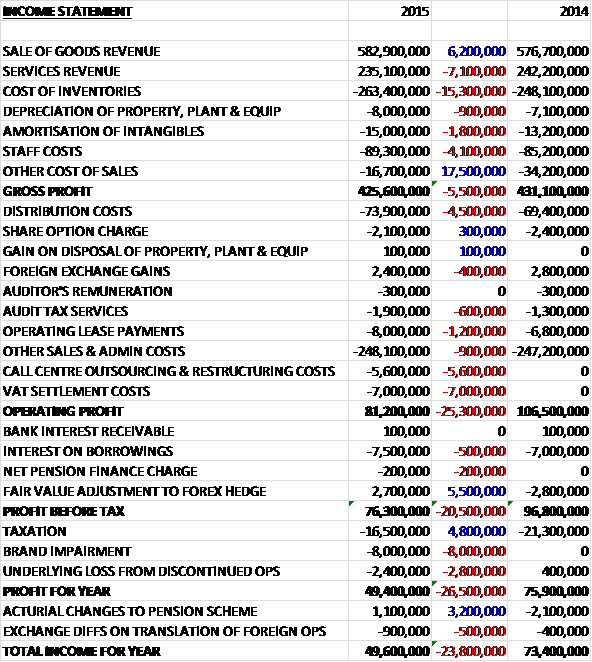

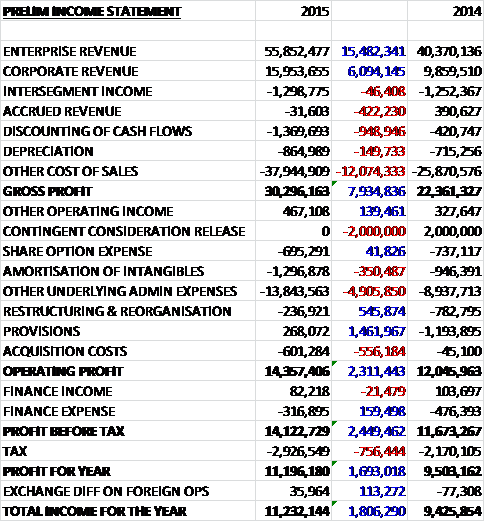

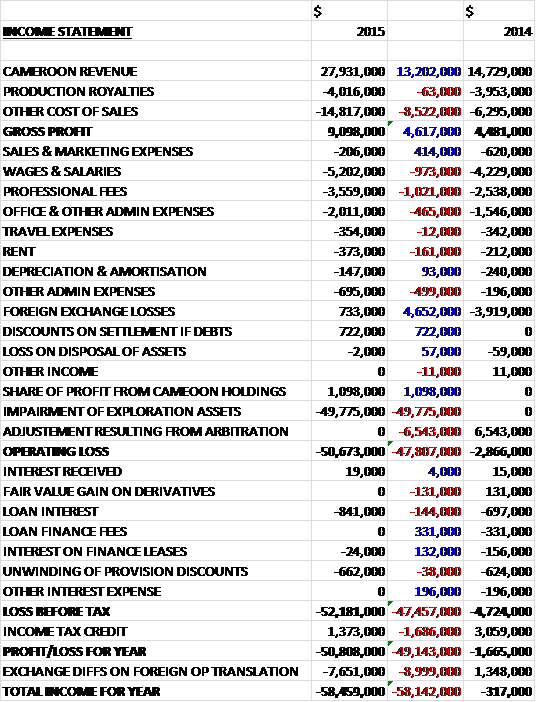

Revenues fell when compared to last year as a £33.7M increase in UK government revenue was more than offset by a £21.7M decline in US government revenue and a £30.8M fall in other revenue. Employee costs were some £184.5M lower and R&D expenditure also decreased but other underlying operating costs increased by £175.9M. Non-underlying costs fell somewhat as last year’s £41.9M goodwill impairment and £4M pension scheme closure mitigation costs was partially offset by a £31.1M reduction in pension liabilities and a £1.4M property impairment reversal to give an operating profit £12.4M higher than last year. Finance costs fell when compared to 2014, mainly as a result of an £8.7M reduction in the interest payable on the USD private placement so that pre-tax profits were £21.4M above that of last year. We then see a £23.8M tax income related to the realisation of tax losses and a £12.7M loss from the discontinued operation, some £68M better than last time. The end result of all this is a profit for the year of £104.7M, a favourable movement of £117.4M year on year.

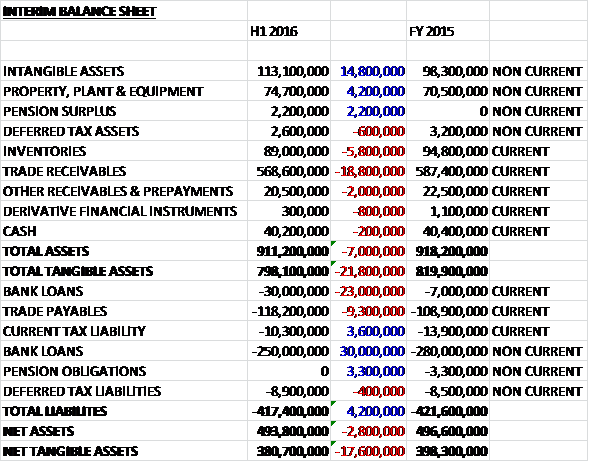

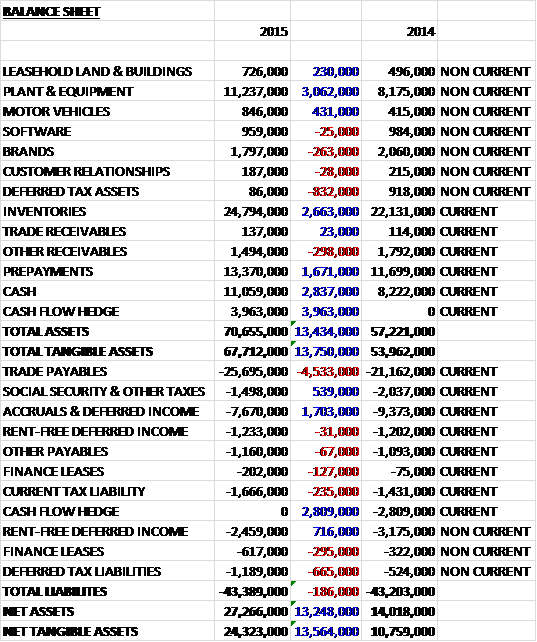

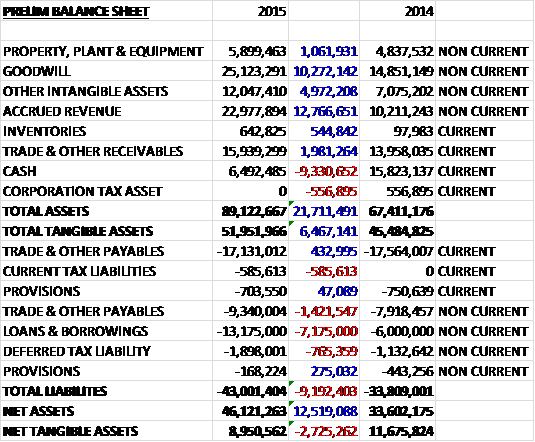

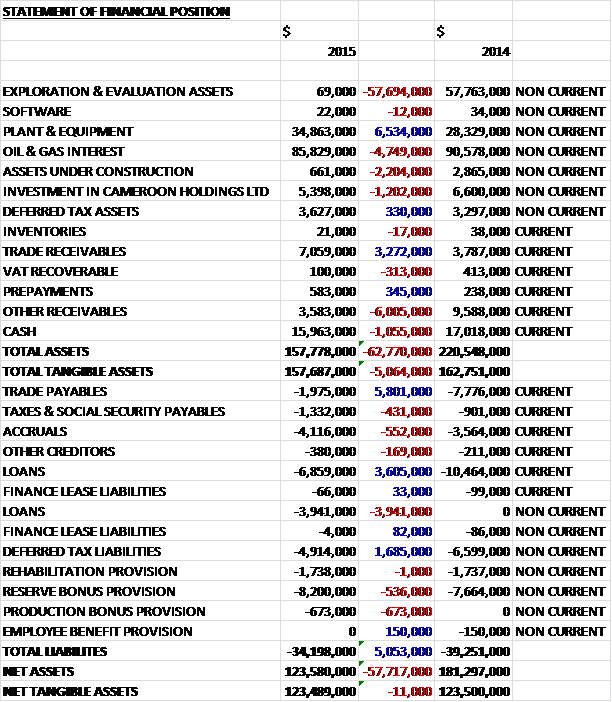

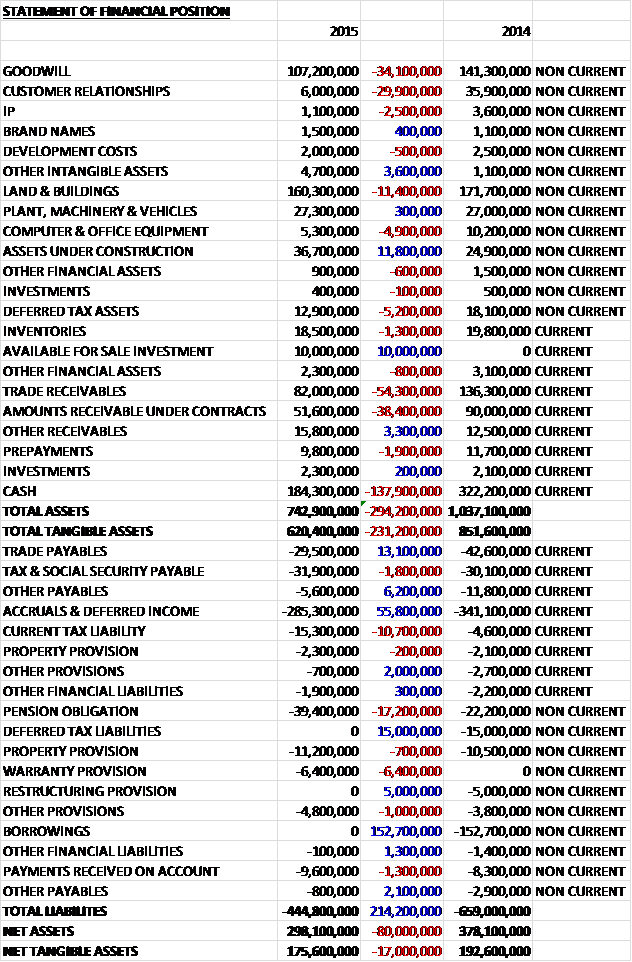

When compared to the end point of last year, total assets declined by £294.2M driven by a £54.3M fall in trade receivables, a £38.4M decrease in amounts receivable under contracts, a £34.1M decline in goodwill, a £29.9M decrease in customer relationships and an £11.4M fall in the value of land and buildings, partially offset by an £11.8M increase in assets under construction and a £10M available for sale investment. Total liabilities also fell during the year as a £152.7M elimination of borrowings, a £55.8M decrease in accruals and deferred income, a £15M fall in deferred tax liabilities and a £13.1M decline in trade payables was partially offset by a £17.2M increase in the pension obligation and a £10.7M growth in the current tax liability. The end result is a net tangible asset level of £175.6M, a decline of £17M year on year.

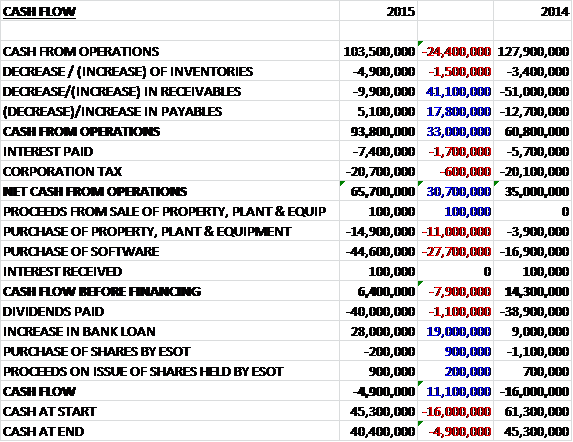

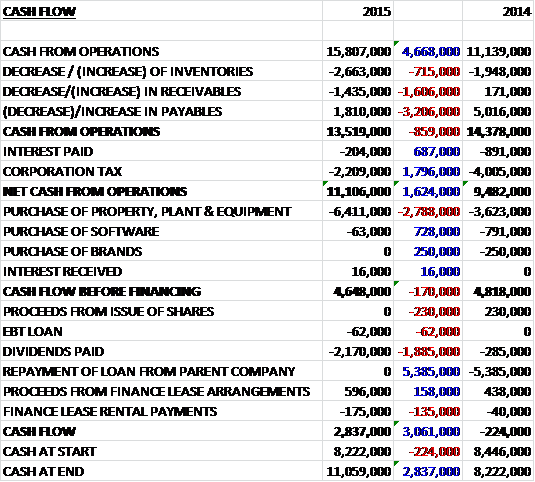

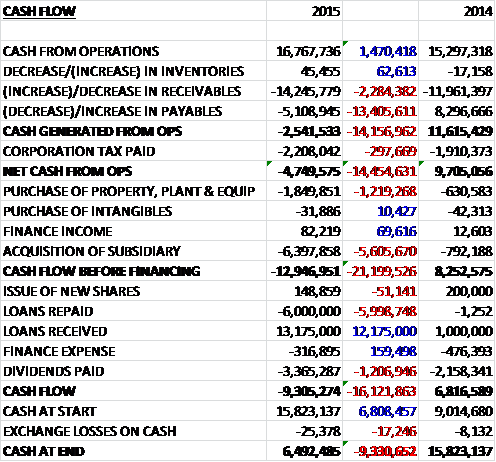

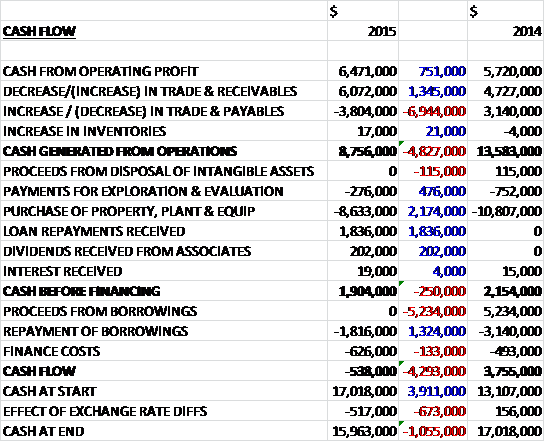

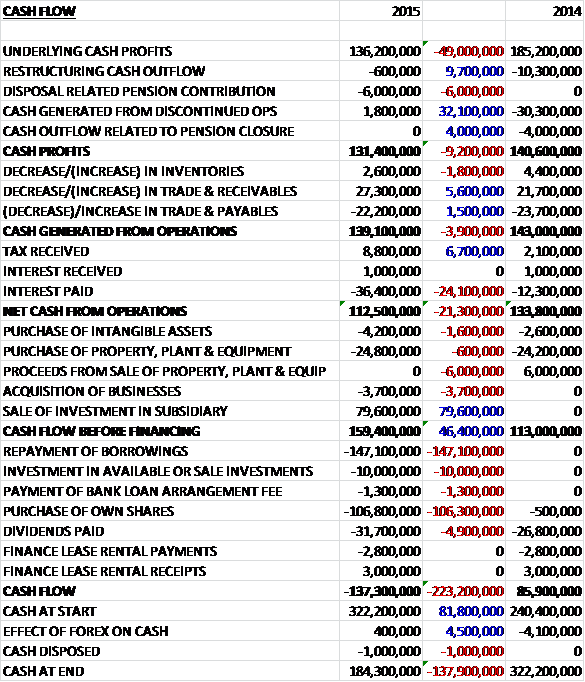

Before movements in working capital, underlying cash profits fell by £49M to £136.2M. After taking into account the non-underlying items, the actual cash profits fell by £9.2M to £131.4M. A large fall in receivables and in increase in tax received was offset by a big hike in the interest paid(presumably due to the early redemption of the debt) meant that net cash from operations stood at £112.5M, a decline of £21.3M year on year. The group spent £24.8M on fixed tangible assets and £4.2M on intangibles to give a free cash flow of £83.5M before a net £75.9M was received from the sale of a subsidiary to give a cash flow before financing of £159.4M. The bulk of this was used to pay back borrowings with the rest going on the investment in the available for sale asset. The group also paid £31.7M on dividends and used £106.8M to buy-back shares to give a cash outflow for the year of £137.3M and a cash level of £184.3M at the year-end.

The EMEA services operating profit was £93M, an increase of £3.3M year on year assisted by an insurance recovery and the completion of a final milestone on an international project. Each of the core air, weapons and maritime businesses performed well despite the uncertainty in the UK defence market resulting from the MOD transformation programme and strategic defence and security review. Orders, excluding the £998M third term of the LTPA contract, grew 3% to £461.6M and revenue was also up 3% on an organic basis at constant currency. At the beginning of the new year, 80% of the division’s annual revenue was already under contract.

During the year the air business secured a £16M extension to its largest MOD test and evaluation contract, and a four year £5M contract for research into aircrew performance. The business also continued to grow its engineering services offering and now provides maintenance, repair and overhaul services for fixed and rotary wing aircraft across three main contracts with opportunities to take this capability into new international markets.

The weapons business delivers the MOD’s conventional weapons research programme through the Weapons Science and Tech centre which secured £17M of orders during the year. In response to the growing complexity of weapons systems trials work, major infrastructure improvements took place at a number of the ranges that the business runs under the LTPA contract including new communications infrastructure in the Hebrides and a new range control centre in Wales. The group has also undertaken work for the South Korean government as well as some European customers.

The maritime business won a £5M contract from a competitor to deliver the MOD’s mobile underwater targets service at the BUTEC range it operates off NW Scotland, which also benefited from over £20M of investment to modernise its acoustic measurement system, enhancing the group’s ability to deliver stealth related services. During the year the business supported the integration of a new radar on the Type 23 frigate and a new command system for the helicopter carrier HMS Ocean. This expertise underpins a new mission systems integration service to meet demand from international customers, particularly from the Asia Pacific region. The business was also awarded a contract to deliver technical support for ship procurement for the Canadian government. The Portsdow site was selected to host the defence growth partnership’s centre for maritime intelligent systems which will help UK industry meet customer interest in emerging technologies such as autonomous systems.

The Australian division delivered a steady performance against a background of fiscal pressures and defence reform, securing a two year extension to the services it delivers to DSTO Fishermens bend in Melbourne. The training business secured its largest ever contract for the continued provision in the UK of Distributed Synthetic Air Land Training valued at £33M over five years. It also beat a number of competitors to win the next stage of a core research programme worth £3M over four years. As a result the business is well positioned for future opportunities as the MOD moves towards its vision of a network of simulators across the UK to augment live training. Having established an office in Florida, the business has secured a positon on three IDIQ contracts working in partnership with established prime contractors such as Alion and developing a promising pipeline of opportunities in the US.

The Cyber Security business won a new £3M contract to deliver secure monitoring and hosting services for a major financial institution. The business is integrating the group’s human science expertise into its consulting offering and is investing in its cyber intelligence capabilities. It launched a cloud based cyber threat centre that monitors the internet, provides alerts and delivers data on domain names, IP addresses, phishing and malware attacks. During the year the procurement advisory services business provided horizon scanning for the UK Cabinet Office, cost forecasting services to the MOD, and won a £2M MOD contract for business case support to help address frontline challenges such as the supply of water, fuel and power. The division is spear-heading the group’s presence in Canada, where an office was opened during the year.

The Global Products operating profit was £18.3M, a decline of £8.7M when compared to last year due to a reduction in revenue due to reduced sales of conflict related products along with about $5M of one-off costs. Orders grew by 2% to £152M as demand for EMEA products offset the slow order intake in the US products business with about half of 2016 revenues already under contract at the beginning of the year.

The US Global Products business won $24M of orders to reset TALON robots, modernising them for future operations. These awards position the business well for future US DoD Programs of Record although to date these have been slow to emerge. The fifth generation of TALON was launched during the year, incorporating the ability to use third party commercial components to capitalise on the continued divergence of military and civil robotic technologies. In addition, $14M of orders for unmanned systems were won from international customers. In response to the growing use of robotics in the construction and demolition industries, the business launched DriveRobotics, a kit that transforms Bobcat vehicles into an unmanned vehicle. Demand for survivability products continues to be impacted by the drawdown for US military operations, although new orders were received for armour for the C-130 aircraft.

The sale of the US Services division removed organisational conflict of interest barriers that prohibited the US Global Products business from pursuing DoD R&D contracts and the division saw a modest increase in these activities during the year. It was one of two suppliers to receive a contract from the DARPA for the first phase development of the Hydra programme to develop a distributed undersea network of modular unmanned platforms and payloads. This positions the business well for follow-on phases of the programme and other projects with the US Office of Naval Research.

Optasense made progress implementing its strategy of developing partnerships with leading industry players to exploit its key markets. In rail, the business continues to work with Deutsche Bahn and also won a $5M initial award from the Saudi Rail Organisation to provide security monitoring for over 1,000km of rail line. In oil and gas, the product development agreement with Shell continues to deliver significant technological progress but the fall in the oil price has slowed the adoption of DAS for well completion but improved the economics of its use for flow monitoring and seismic profiling.

After the year-end the business entered into a non-exclusive strategic alliance with Weatherford to deliver solutions to optimise well planning, construction and production. In infrastructure security, the delivery of some key projects was, ironically, interrupted by a worsening security situation in the Middle East but this also increased demand. At the end of the year the business signed a framework supply agreement to protect critical national infrastructure including pipelines, airports and other facilities for a customer in the Middle East. When complete, the two year project could involve 200 units and encompass up to 8,000km of assets.

At the end of the year the space products business was awarded a contract worth €16M over three years to develop the computer ad avionics for the European Space Agency’s Proba-3 satellites that will fly in formation and use an eclipsing mechanism to study the sun. The business is also playing a vital role in the ESAs IXV mission launched in February 2015 as its technology will be responsible for guiding the “space taxi”, a smaller version of the US space shuttle, safely back to Earth. Commerce Divisions delivered record profit in 2015, securing an enterprise-wide contract for the third year from the MOD for its “Award” procurement software, as well as delivering growth in the UK health and transport markets. The business also secured its first order in Canada shortly after the year-end.

Field evaluations are underway for the Linewatch power line sensor system, which precisely measures voltage and currents on power grids. The product is designed to meet emerging Smart Grid requirements for the detection of faults and power theft, condition-based maintenance, and distributed power generation. In addition the US products business is developing a high power density generator which can provide modular roll-on/roll-off power required for emerging defence and civil applications.

During the year the UK business launched ASX, a small sensor that delivers airborne surveillance capability. The MOD selected the Modular Electronic Warfare System ahead of more established products to form the basis of its medium weight electronic surveillance capability for expeditionary operations. Further milestone orders won during the year included a $3M contract with the US Transportation Security Administration to develop the next generation of Qinetiq SPO stand-off Millimetre Wave threat detection system.

The UK government continues to face a significant budget deficit, and a further period of fiscal austerity looks likely. Defence expenditure is not protected by government ring-fencing but the MOD has made progress over the last five years in balancing its budget. In the US, Obama recently requested an 8% increase to the US defence budget for 2016, forcing the Republican majority to weigh up competing concerns about defence and tackling the ongoing fiscal deficit. The US government, is, however, continuing to drawdown the number of troops deployed on overseas operations and reduce the accompanying procurement budget which continues to depress demand for conflict related products.

One project undertaken during the year was for the UK Royal Navy where the maritime stealth information and range services team provided stealth management capabilities helping to make vessels combat ready. Rather than sailing mine-hunters out and back for six month tours of the Middle East, the technology allows four vessels to be based in the region for years. They place magnetic and acoustic sensors in the water, sail a vessel over them, and then calibrate on board systems to avoid detection by aggressors and make an 8,500 tonne destroyer look like a much smaller vessel.

Elsewhere, the US Transportation Security Administration has awarded the group a $3M two year contract for an innovative threat detection system that uses their passive millimetre wave technology. With the TSA concerned about terrorist threats to targets like railway stations, ferry and bus terminals, it wanted leading-edge technology to help secure these venues. Working at a range of up to 15 metres, the SPO technology scans a crowd and detects if a person is hiding something under clothing without needing to stop. Travellers are not inconvenienced, the system does not emit harmful radiation and no privacy laws are contravened. With earlier versions deployed at locations including New Jersey, Washington and LA, the group also provides maintenance, support and end-user training.

Under a twenty year contract, the group provides aerial targets worldwide for the UK Army, Royal Navy, RAF and project teams working on new weapons. The group now handles all such requirements after several suppliers were consolidated into one. They also completed aerial target projects for the US Air Force, Swiss MOD, Danish Navy and BAE Systems. Demand for this service is rising, a recent contract for Sweden involved working with a US target manufacturer to deliver launchers and operators, and they are now exploring opportunities to bring other suppliers’ targets into CATS to offer even better performance and value for money to customers.

The European space agency awarded the group a €16M three year contract to develop the computer and avionics for its Proba-3 mission which involves two satellites making a virtually fixed structure in space by precise formation flying only 150 metres apart. Proba-3 will study the sun’s corona using an eclipsing mechanism, with a camera fixed on one satellite and an occulting disk on the other, and flying at the optimal distance apart to shield the camera from the sun and create conditions usually only observable during a solar eclipse. The Belgium based team is creating highly compact avionics able to process millions of instructions per second while also operating effectively in the punishing high-radiation environment of space.

Under a five year contract that runs from 2014, the group is delivering the Distributed Synthetic Air Land Training 2 capability for the UK MOD, building on the delivery of a previous five year contract. Operating from the Air Battlespace Training Centre in Lincoln, the £33M DSALT2 training programme provides the UK Army and RAF with realistic and flexible representations of operating environments. Their bid was supported by a pan-Qinetiq team and includes sub-contractors Boeing and Plexsys.

In May the group completed its sale of the US Services division, comprising Qinetiq North America with the proceeds applied in settling the remaining private placement debt which was put in place to finance the acquisition of the division in the first place. This will involve a penalty of £28.8M incurred on the early redemption of the debt. The initial cash consideration was $165M prior to the standard working capital adjustments at completion and there is also contingent consideration of between zero and $50M based on gross profit generated by the disposed business in 2015 which in the event amounted to $9M in cash.

In August the group acquired Redfern Integrated Optics, a US based business that designs and manufactures highly coherent semiconductor lasers which are used in the distributed acoustic sensing market. The business was acquired with initial cash of £3.3M and deferred consideration of £500K and generated goodwill of £2.9M. In November the group acquired SR2020, a US-based provider of borehole seismic services who develop and use purpose written, proprietary software for borehole seismic imaging, micro-seismic monitoring and passive seismic monitoring. The business has extensive oil and gas industry experience. The business was acquired with cash of £400K, all of which was goodwill.

It is interesting to note that the group is actually making money from operating leases, with a total as a lessee outstanding of just £13M compared to £37.3M outstanding with the group as a lessor as it sub-lets properties that are vacant. The group currently has contracted capital commitments of £30.8M in relation to property, plant and equipment that will be wholly funded by a third-party customer under long term contract arrangements. During the year the group recognised a tax asset of £25.2M in respect of unused tax losses relating to UK trading losses which are expected to be utilised in the foreseeable future.

The group operates a pension scheme which was closed to future accrual at the end of October 2013. There is currently a liability of £37.8M attached to the pension but it is a big scheme with assets of some £1.454BN so there is potential here for this to get out of hand.

In October 2014, Leo Quinn tendered his resignation as CEO to take up a role as CEO of Balfour Beatty. Leo arrived at the group in 2009 at a difficult point in the company’s history and has since transformed their fortunes. Following his departure, CFO David Mellors took over as interim CEO but by April 2015 the group had appointed Steve Wadey as new CEO who was previously MD at MDBA UK. It has to be said that the executive directors are very well paid and the last CEO was paid £2.1M last year with the CFO pocketing £1.8M this year. It is also notable that over 15% of votes were voted against the remuneration policy at the AGM so this seems to be a common concern. It’s also notable that the directors do not own many shares in the company.

Defence transformation and the forthcoming comprehensive spending review and SDSR are expected to have an impact on the UK defence market this year and give the potential for interruptions to order flow. The portion of revenue under contract at the start of 2016 was similar to a year ago and the balance is supported by a pipeline of opportunities. Overall given the opening backlog position, expectations for the performance of EMEA Services in the current financial year are unchanged.

In Global Products, newer products are recording notable milestones and the amount of revenue under contract at the start of 2016 is up slightly on a year ago, but the drawdown of American overseas military forces is continuing to depress demand for conflict-related products. As the division has a lumpy revenue profile which is dependent on the timing and shipment of key orders, there is a range of possible outcomes for the year. The board is, however, maintaining its expectations for group performance in the current financial year.

In May 2014 the group initiated a £150M capital return to shareholders by way of a share buyback. By the year-end, the group had bought back £63M shares at a cost of £128M and the board apparently remain committed to maintaining an efficient balance sheet so expect more shareholder returns or acquisitions.

At the current share price the shares are trading on a PE ratio of 15.2 which reduces to 14.9 on next year’s forecast. After a 17% increase in the full year dividend, the shares are currently yielding 2.4% which increases to 2.5% on next year’s consensus forecast. At the end of the year the group had a net cash position of £195.5M compared to £170.5M at the end point of last year. There is currently also £233.3M in undrawn committed facilities with an interest rate of just 0.65%+LIBOR.

Overall then this was a solid set of results. There are various definitions of profit but overall profits increased due to non-repeated non-underlying items last year. Underlying pre-tax profits did improve but this was due to a much lower interest payment as a big chunk of debt was paid off and underlying operating profit fell. The operating cash flow declined year on year on every metric, however, and net assets declined during the period. Despite the decline, the group is still very cash generative and plenty of free cash was generated during the year.

The EMEA Services division performed well with the core air, weapons and maritime business performing well. Profits were boosted by the final milestone payment on an international project, though, so this will not be repeated going forward. It is a shame the value of the project is not mentioned but it is good to see that it is being brought up now and not as an excuse for a profit warning somewhere down the line (other companies should take note). Profit fell in the global products division, however, due to lower sales of combat-related products following the withdrawal of troops from Afghanistan – an issue that is likely to continue into the new-year.

There are clearly a number of risks involved here. The MOD is clearly the most important customer but it is currently undergoing a budget review which could clearly affect the company. The withdrawal from Afghanistan is also going to reduce demand for their products. In addition, the global products division has lumpy orders so earnings visibility is low, there is a new CEO and the huge pension plan is lurking in the wings. The sale of the US Services division looks sensible though and the group has a strong net cash position. At a forward PE of 14.9 and a dividend yield of 2.5% the share price seems to be sensibly factoring everything in, though.

On the 30th September the group released an update covering trading in the first half of the year. The board are maintaining their expectations for group performance this financial year. In the UK, the government’s strategic defence and security review, and public consultation on the proposed approach to calculating the baseline profit for single source contracts are both underway. The EMEA services division continues to see some customer contract award decisions deferred due to uncertainties in the UK market or delayed by requirements for additional approvals. The revenue under contract this year is as expected at this stage, however. As expected the group’s global products division continues to trade at similar levels to last year.

Overall then, this seems steady but not that exciting – the spending reviews in the UK seem to be the main issue at the moment.