Braemar Shipping has now released its interim results for the year ending 2016.

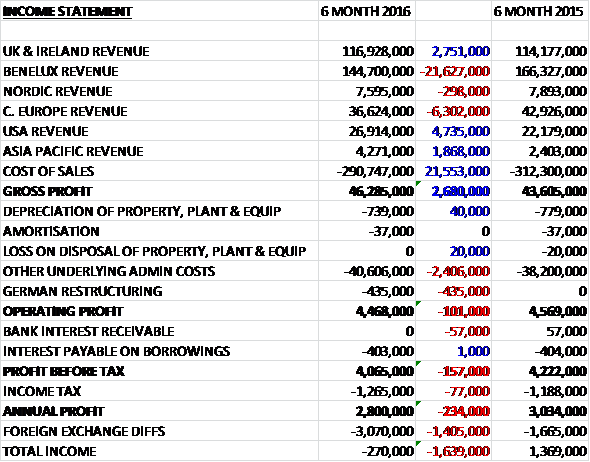

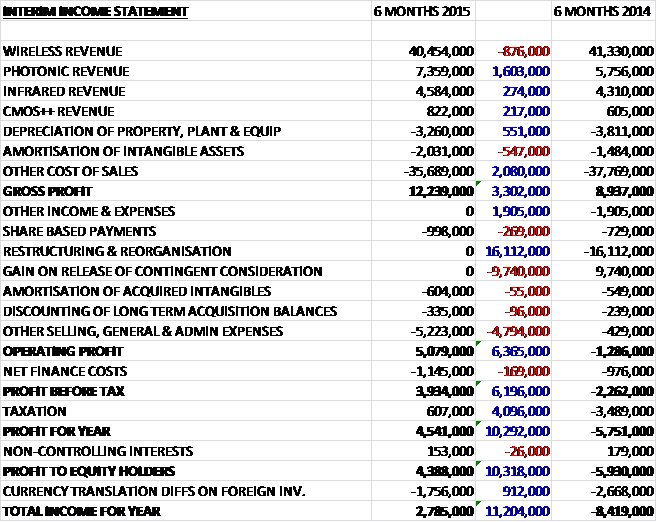

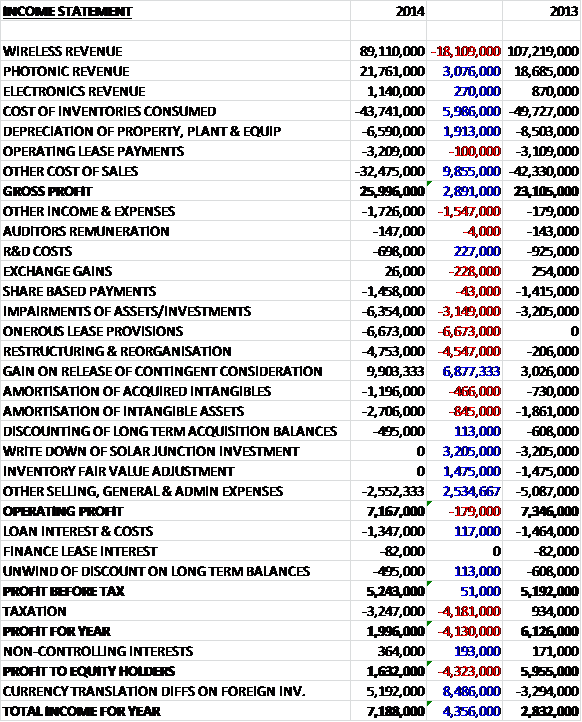

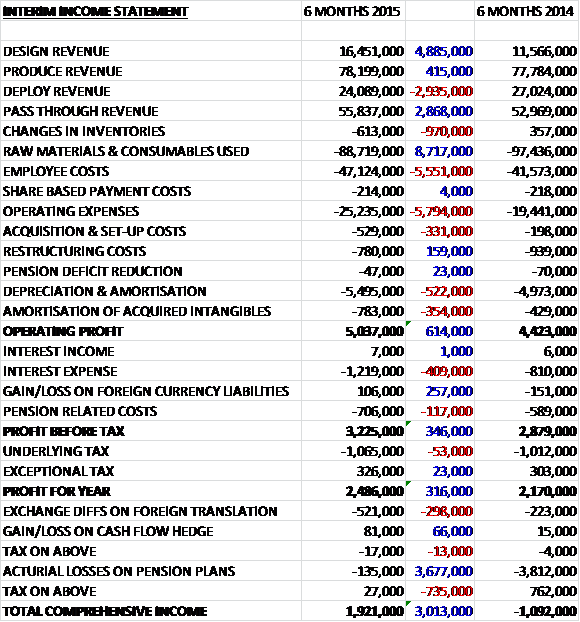

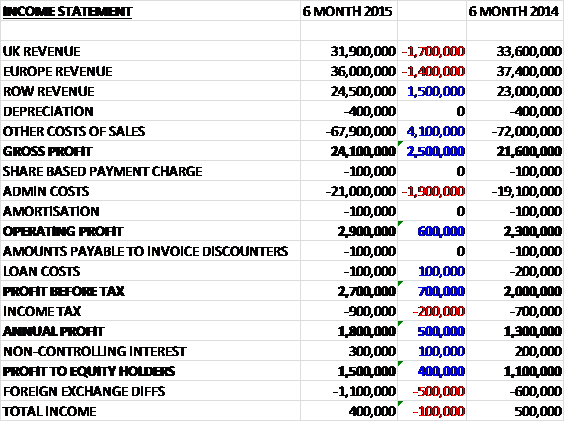

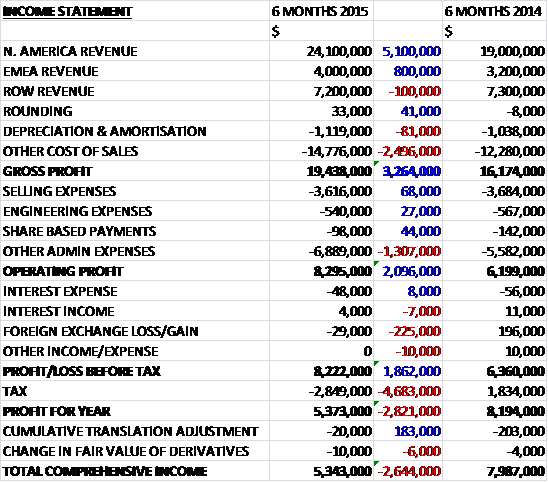

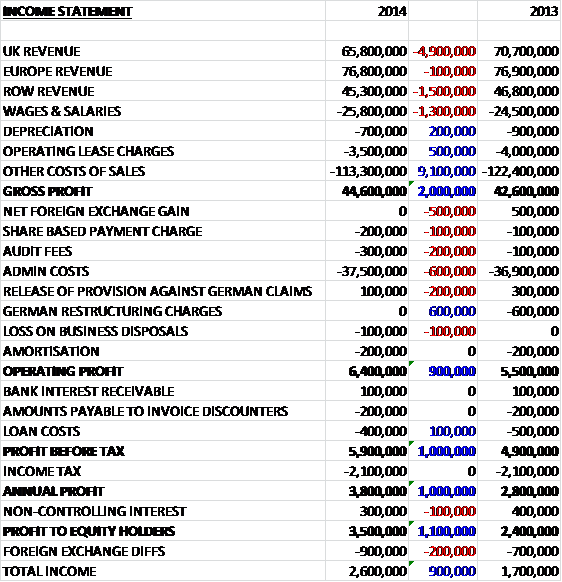

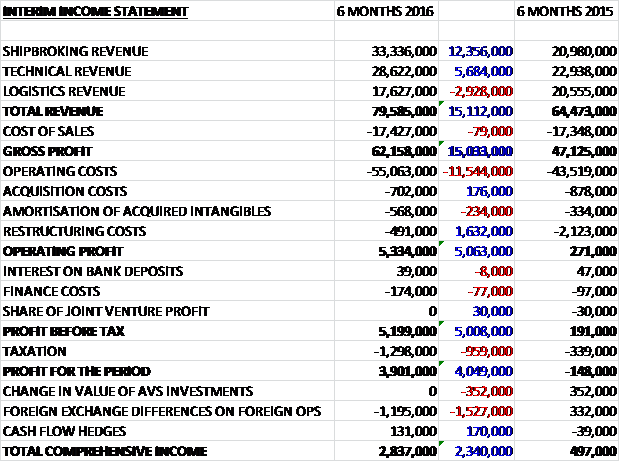

Revenues increased when compared to last year as a £2.9M decline in logistics revenue was more than offset by a £12.4M growth in shipbroking revenue and a £5.7M increase in technical revenue. Cost of sales were broadly flat so gross profit was £15M ahead of last time. Operating costs increased by £11.5M, however, which was partially offset by a £1.6M decline in restructuring costs so that operating profit was £5.1M over the first half of last year. Finance costs increased slightly and tax increased more considerably so that profit for the half-year came in at £3.9M, a £4M improvement year on year.

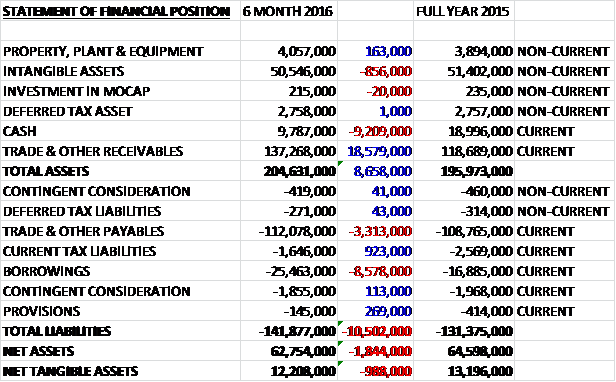

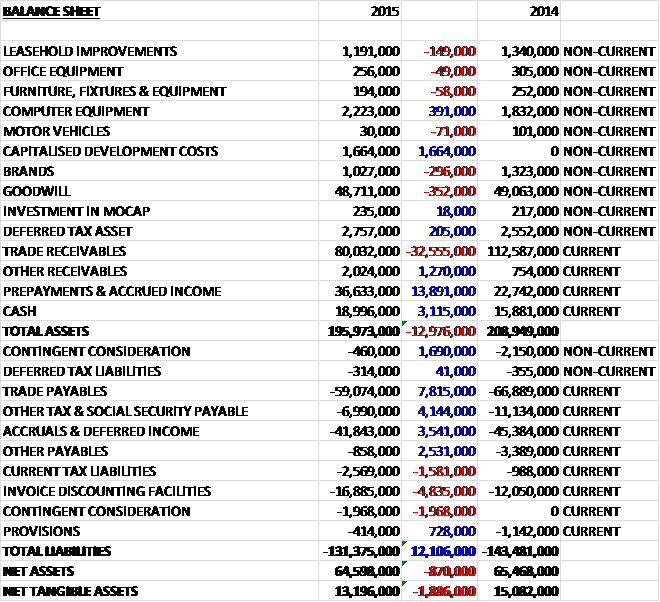

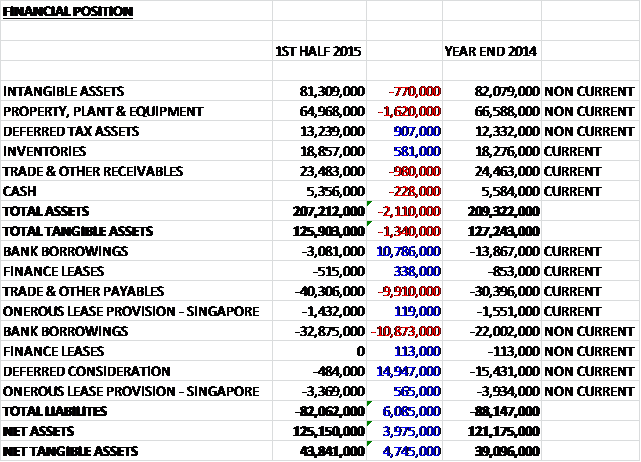

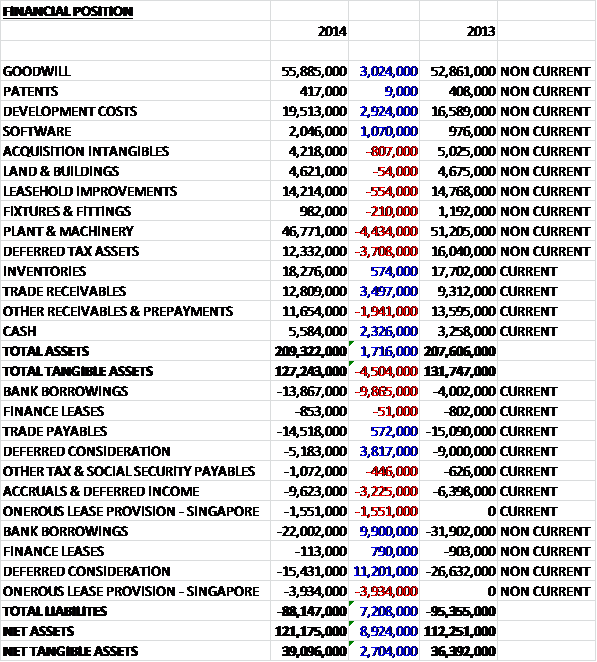

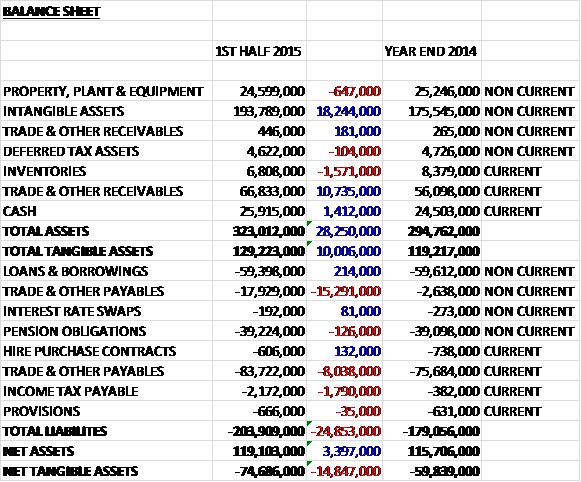

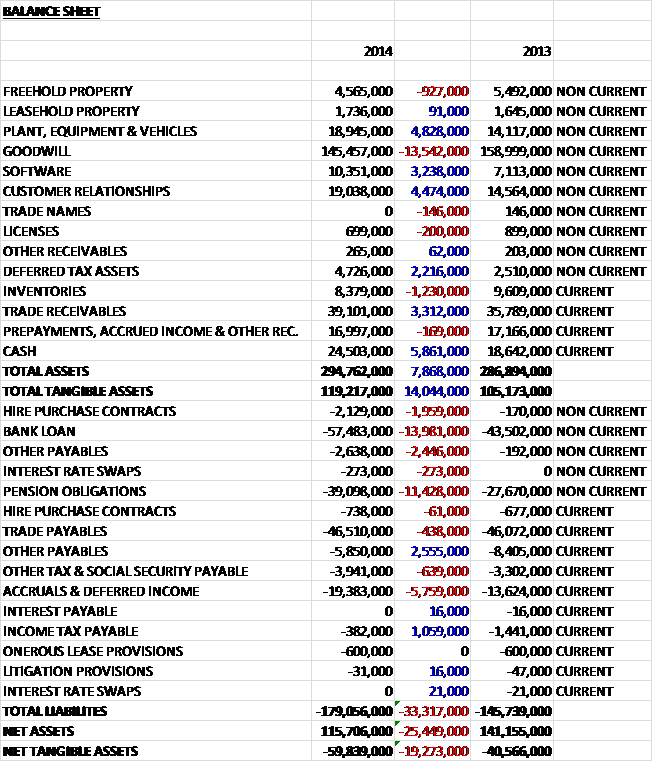

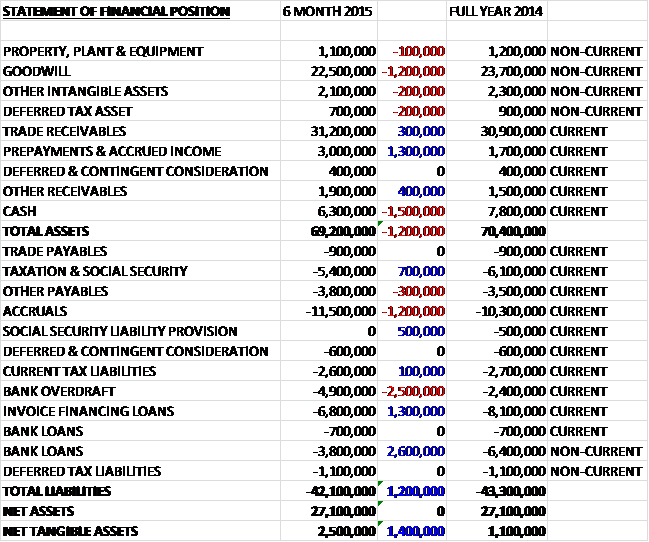

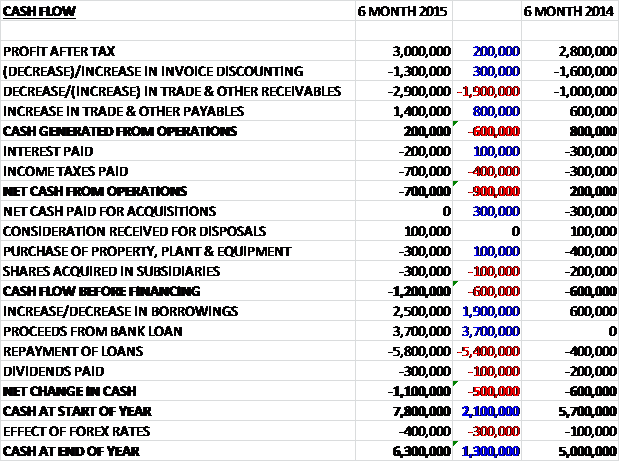

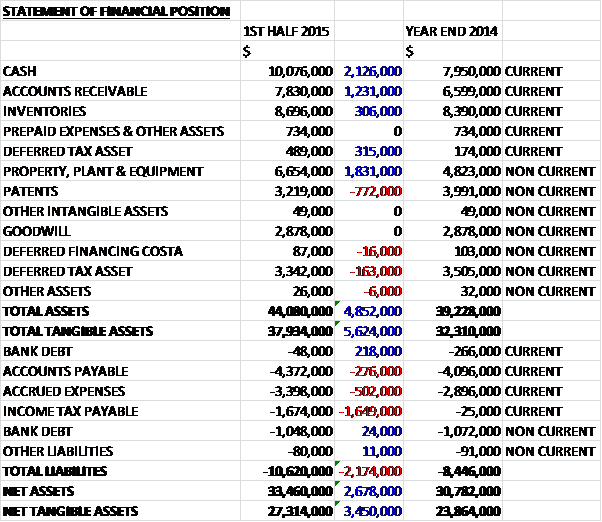

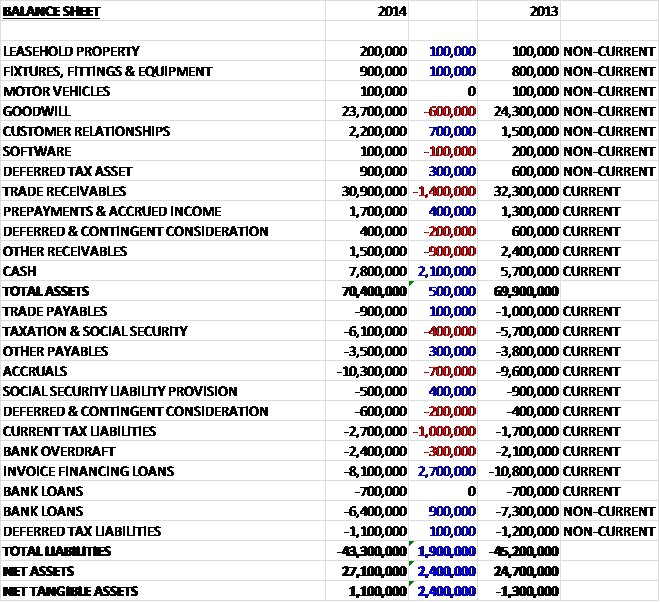

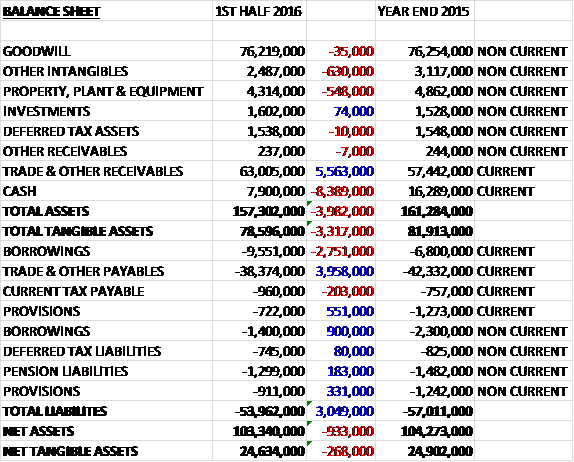

When compared to the end point of last year, total assets fell by £4M driven by an £8.4M decline in cash, a £630K fall in intangible assets due to the amortisation of the acquired future order book and a £548K decrease in property, plant and equipment arising from the disposal of the former HQ, partially offset by a £5.6M increase in receivables. Total assets also decreased during the period as a £4M fall in payables, and a £882K decline in provisions partially offset by a £1.7M increase in borrowings. The end result is a net tangible asset level of £24.6M, a decline of £268K over the past six months.

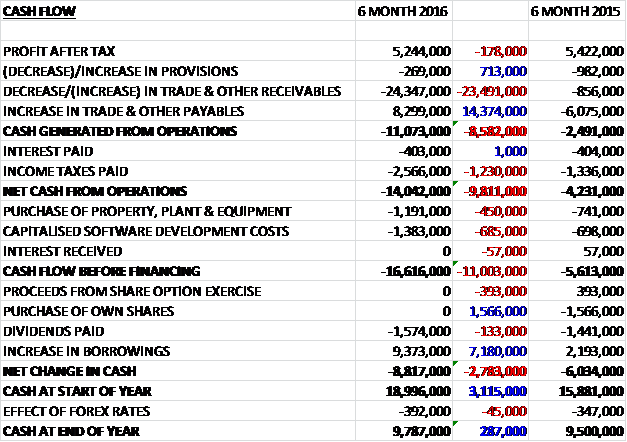

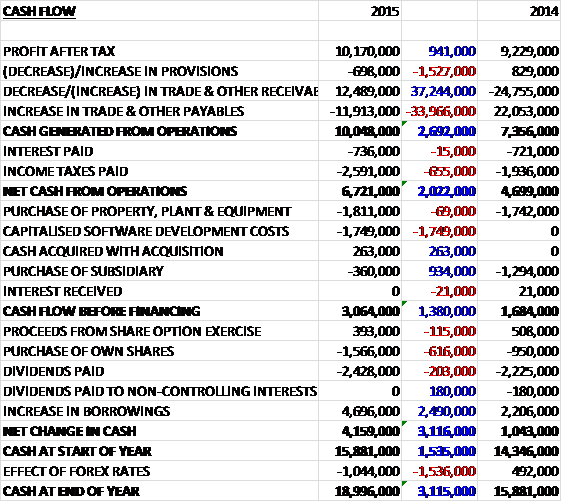

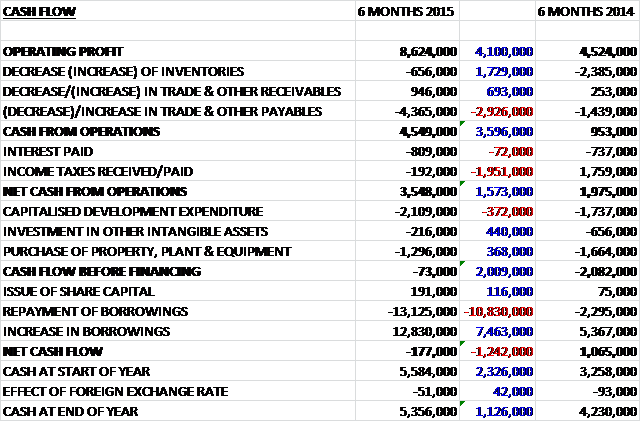

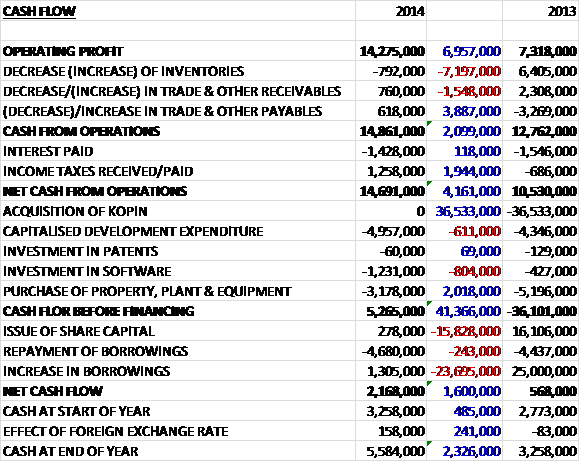

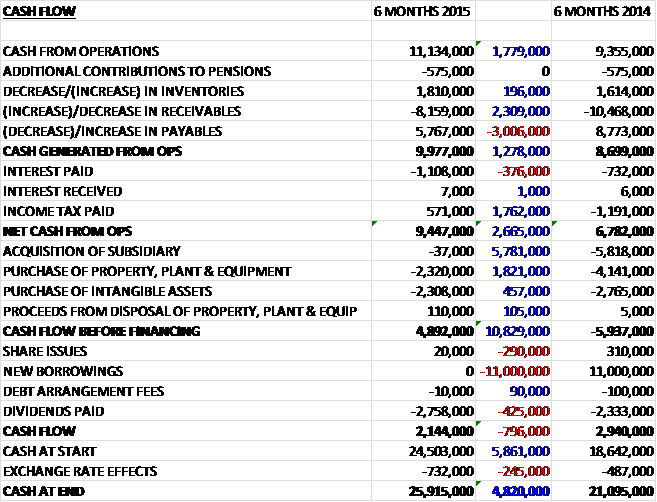

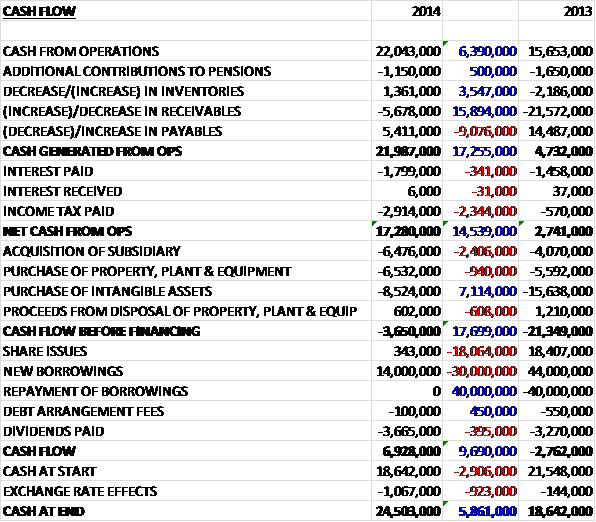

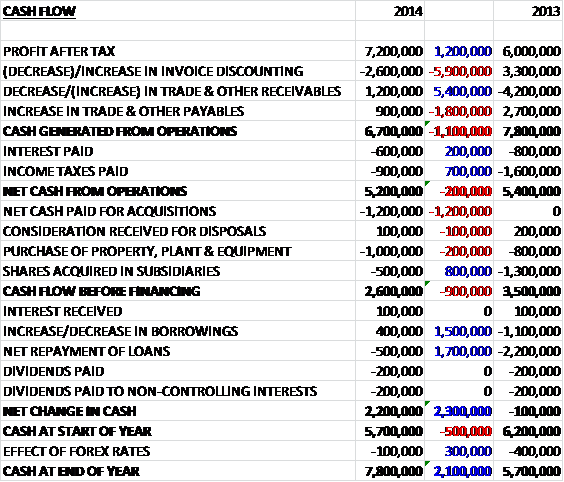

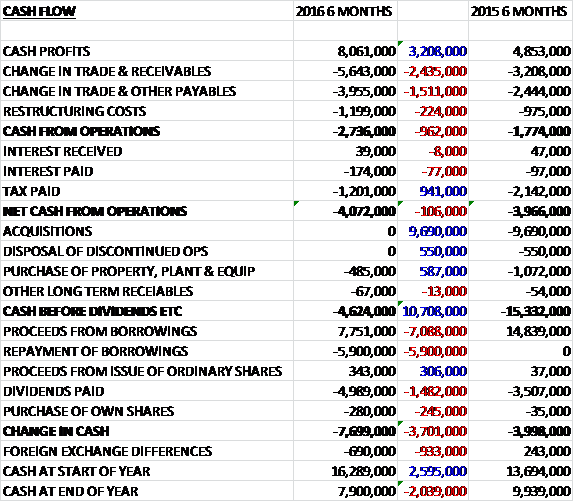

Before movements in working capital, cash profits increased by £3.2M to £8.1M. A big outflow of working capital cash, with a particularly large increase in receivables meant that there was a cash outflow of £2.7M before a lower tax payment meant that the net operating cash outflow was £4.1M, a detrimental movement of £106K year on year. The group did not spend much on capex, however, with £485K spent on fixed tangible assets so that before financing the cash outflow was £4.6M. The group still spent nearly £5M on dividends, however, and after a net increase in borrowings, the cash outflow for the half year came in at £7.7M to give a cash level of £7.9M.

The divisional operating profit in the shipbroking division was £4.6M, an increase of £3.2M year on year with much of the increase attributed to the full period impact of the merger with ACM. The total forward order book remains consistent at about $56M, of which approximately $14M relates to the second half of this year. The increase both in oil production and crude oil tonne miles reported over the last year has had a beneficial effect on the tanker market and freight rates have been strong throughout the first half and are expected to remain so during the coming quarter. The fall in the oil price has had the opposite effect on the offshore market, however, where exploration budgets have been cut back significantly and the demand for offshore supply vessels have fallen.

With lower oil prices, the tanker and offshore markets can behave counter-cyclically and with the group’s greater weighting in tankers they would expect a net benefit to shipbroking income while oil supply and tanker demand are strong. The dry bulk market is suffering from an over-supply of tonnage and a softening in Chinese demand for raw materials. Although the market will take time to re-balance, the group are apparently appropriately structured to operate in these conditions.

Sales and purchase activity, both in second hand and demolition, has been steady. The rise in the tanker market stimulated investment interest in the sector, especially earlier in the period, and they have been involved in a number of significant market transactions, some of which will benefit income in the second half of the year. In addition, the time charter market for tankers has seen a rise in both rates and activity and they have been able to conclude some good multi-year business for their clients in the half.

The divisional operating profit in the technical division was £3.1M, a growth of £807K when compared to the first half of last year. While the reduction in the oil price has had a detrimental impact in some parts of the division, this has been offset by growth elsewhere. Braemar Engineering has had a very successful first half and is currently working on a number of major LNG projects for clients based in Europe, USA and Africa and is well positioned to capitalise on future growth in LNG. Braemar Offshore, the marine warranty surveying and engineering consultancy, was affected by the slowdown in offshore-related activity following the drop in the oil price. The business has continued to diversify its activity, however in order to try and achieve a solid performance.

Braemar Adjusting, the energy loss adjusting business, performed well against the backdrop of the downturn in the oil and gas sectors of its market with the Middle East office a major contributor during the first half. Despite the market pressure, they were able to maintain good staff utilisation and have managed expenditure whilst continuing to focus on business development. As a result, the group are beginning to see an increase in the volume of instructions in both onshore and offshore business. The hull and machinery damage surveying and marine consultancy business performed steadily throughout the period. The number of new instructions fell compared with last year reflecting global market conditions but the average incident value increased. Braemar Howells, the incident response and environmental consultancy services business, has reported good results for the first half without attending any major incidents in the period.

The divisional operating profit in the logistics sector was £981K, a decline of £65K when compared to the first half of 2015. Whilst the general port agency market has been quiet, business performance in the UK was secured by several ongoing and ad hoc support projects. The new Houston office is beginning to secure port agency business and during the period they augmented their Singapore port agency with added commercial sales skills in order to develop local markets. Sea freight volatility continued, although imports were strong within the logistics sector. They are developing new client relationships following their decision to develop specialist areas such as reefer and European overland. Contract logistics remains a key sector with their use of digital technologies such as “shiptrak” allowing them to add value by optimising their customers’ processes.

There were a few non-underlying items during the period. The group incurred £702K in respect of the acquisition of ACM and £491K in relation to restructuring activities as a result of the acquisition.

The majority of the cash flows have followed the normal business cycle whereby the second half is more cash generative due to the timing of staff bonus payments, although there has been an increase in working capital requirements arising from revenue growth. The group are actively seeking to reduce the level of working capital without inhibiting the normal business operations and the objective of growing the business. The outlook for the full year continues to be in line with the board’s expectations which is supported by the early indications of trading in the second half.

After the interim dividend was kept the same, the shares are yielding 5.9% on an annual basis which is great but hardly covered by cash flow. Net debt at the period-end stood at £3.1M compared to £4.9M at the same point of last year and a net cash position of £7.2M at the end of last year.

Overall then this has been a fairly solid period for the group. Profits have increased year on year but net assets fell back slightly. The operating cash flow also worsened but this was due to working capital movements and cash profits increased. The very large working capital outflow meant that there was a negative cash flow at the operating level, however. The shipbroking division increased profits, mainly as a result of the contribution from ACM, with the increased demand for tankers offsetting a declining demand in offshore supply vessels and bulk carriers.

The technical division seems to be performing well, mainly as a result of some large LNG projects but the logistics business fared less well due to port agency work being quiet. With a dividend yield of 5.9% and PE ratio of 13.1, the shares are not exactly expensive but there does not seem to be a great deal of organic growth, the global economic outlook looks precarious and the large working capital outflow is a little concerning so I think I might stay out of this share for the time being.

It’s possible that the recent fall in share price has been halted but we will have to wait for some confirmation.

On the 14th January the group issued an update covering the trading period since the end of October. Positive momentum continued through the company and they are on track to meet their objectives this year – not sure that really tells us much. The shipbroking division continued to perform well in a volatile environment. They have seen strong activity in the tanker markets driven by the increase in oil production. The sale and purchase business has been pleasing but as expected, the dry cargo and offshore markets remain challenging.

The technical division is performing in line with expectations with the LNG engineering business in particular continuing to grow which has offset the effect of lower exploration activity on the offshore energy business. Overall the board remain confident that the group is on track to meet market expectations for the full year.

On the 2nd March the group announced that CEO of Braemar ACM James Gundy sold 27,500 shares at a value of £117.6K. This leaves him with 468,852 shares in the company.

On the 19th February (only being reported now!), director Denis Petropoulos purchased 19,500 shares at a value of nearly £84K to bring his holding up to 620,934 shares. This is a pretty decent buy actually, not prompted by any need to support the share price.