Gemfields has now released its final results for the year ended 2015.

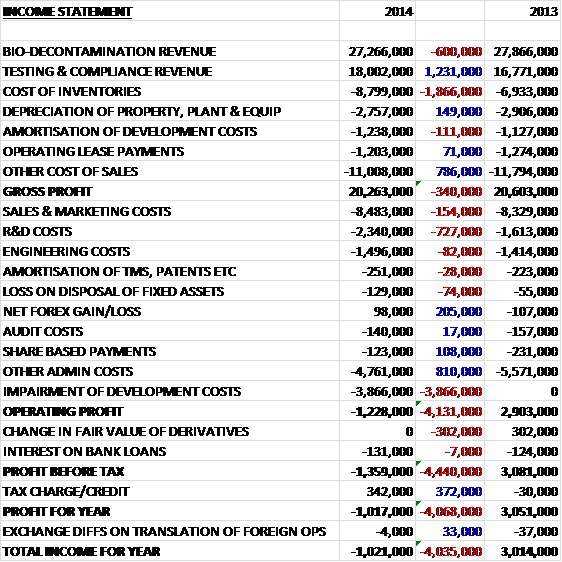

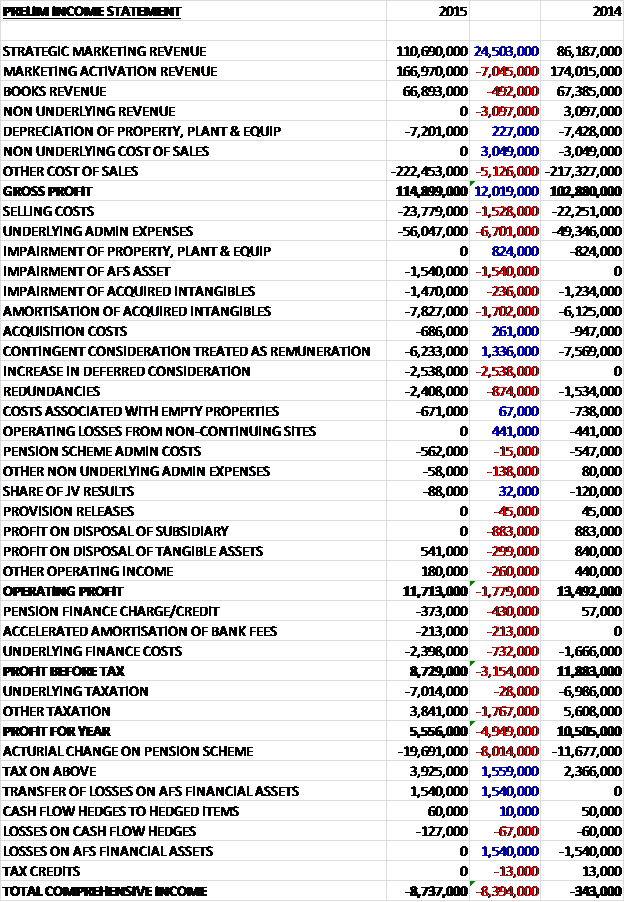

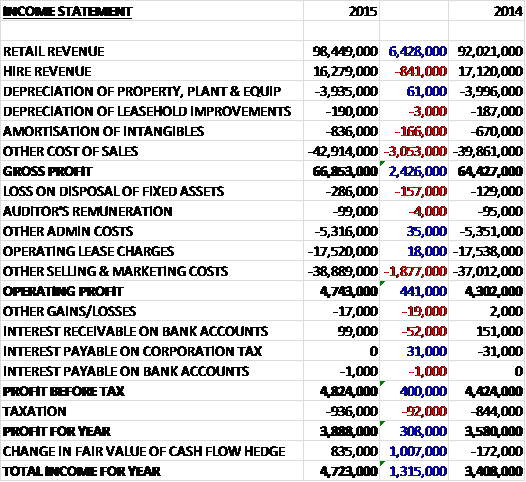

Overall revenues increased year on year as a $55M growth in Montepuez revenue was partially offset by declines in the other businesses. Labour costs increased by $6.1M, royalties grew by $3.7M, fuel costs were up $2.8M and depreciation and amortisation increased by $11.8M. The change in inventory and purchases had a beneficial movement of $19.5M, however, which meant that gross profit was broadly flat when compared to last year. In admin costs we then see another $2.9M increase in labour costs, a $2.6M growth in selling and marketing costs and a $2.4M increase in professional costs so that operating profit was some $6.5M lower than last year. The loan interest grew by $1.7M and there was a $1.9M adverse exchange rate movement which was offset by a lower tax charge so that the profit for the year was $12.3M, the bulk of which was attributable to non-controlling interests (mainly relating to the Montepuez mine) so the profit for the owners was just $3.7M, a decline of $5.1M year on year.

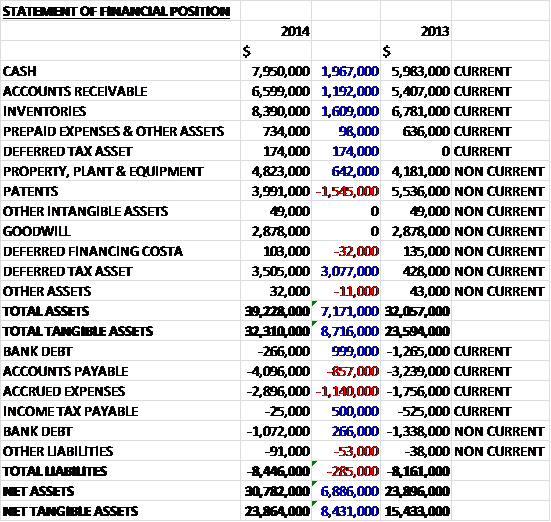

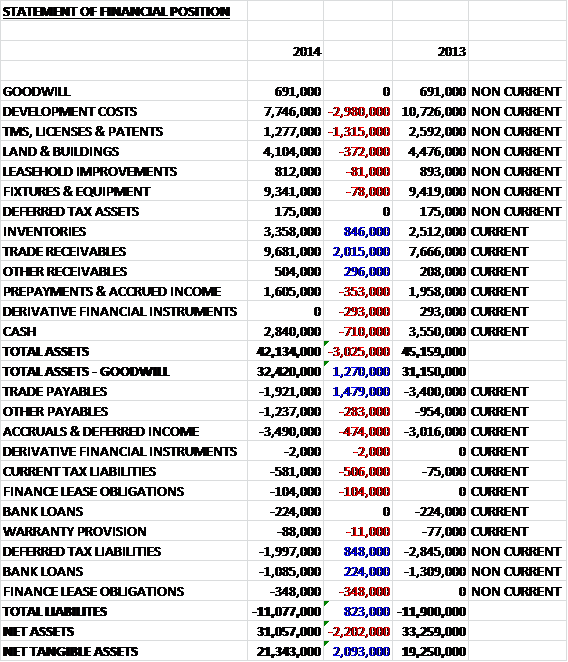

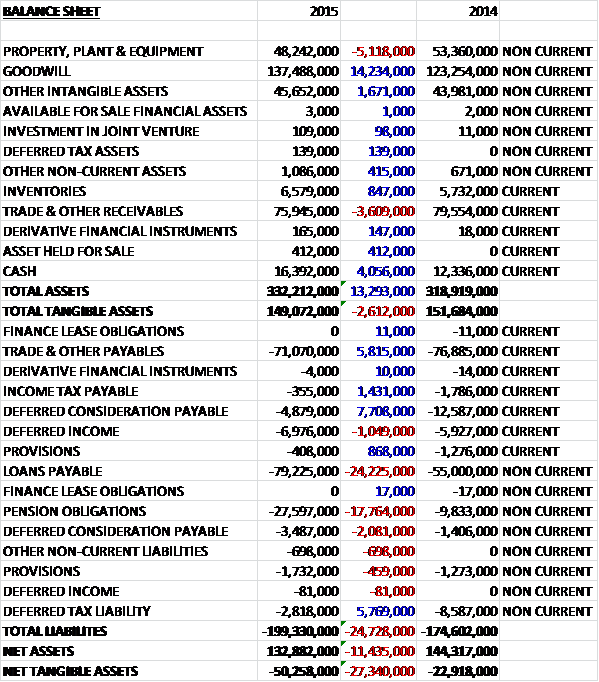

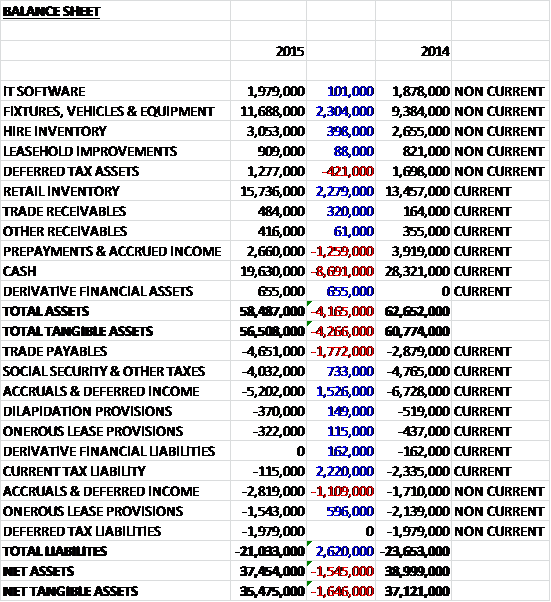

When compared to the end point of last year, total assets increased by $40.6M driven by a $16.4M growth in inventories, a $9.7M growth in property, plant & equipment, a $7M growth in VAT receivable, a $5.6M increase in deferred stripping costs, a $4.7M growth in the loan receivable and a $4.3M increase in unevaluated mining properties, partially offset by an $8.9M decline in cash and a $6.8M fall in the value of evaluated mining properties. Liabilities also increased during the year due to $28M hike in borrowings and a $4.7M increase in trade receivables. The end result is a $6.7M increase in net tangible assets at $254.3M.

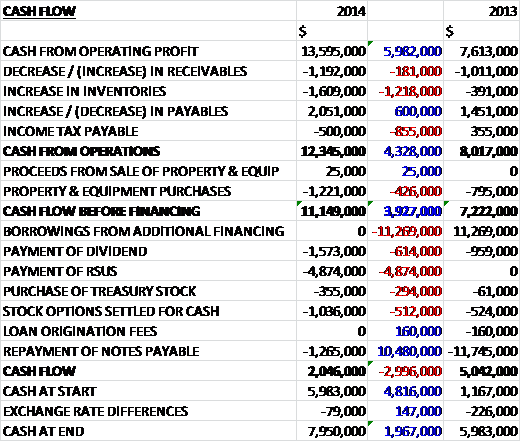

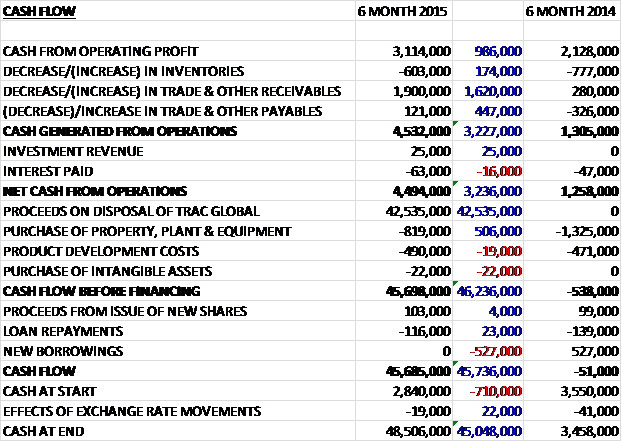

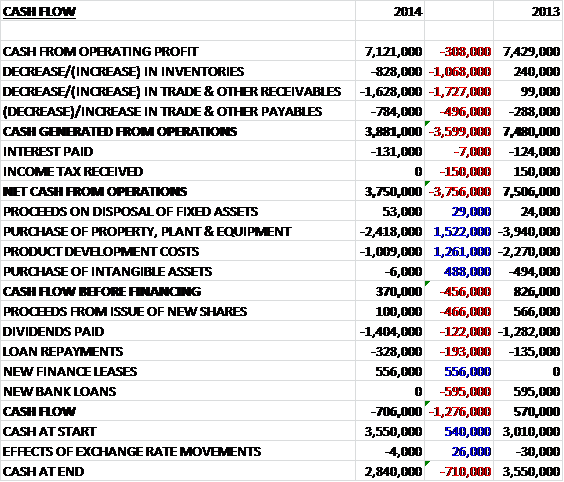

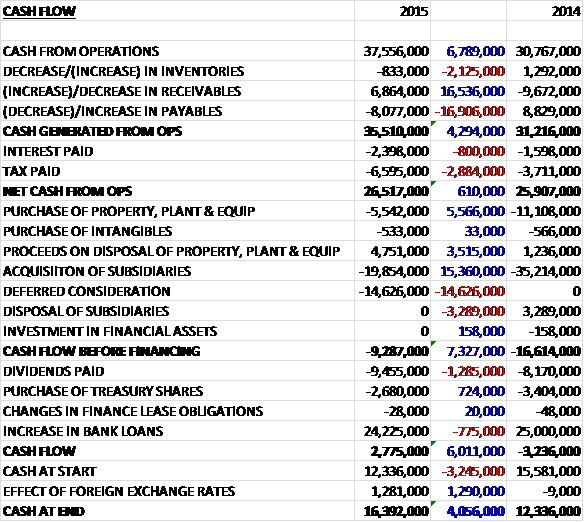

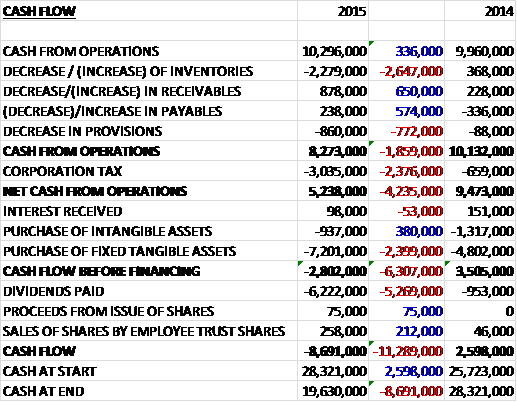

Before movements in working capital cash profits increased by $3.5M but a large increase in receivables and inventories along with a $7.2M increase in tax paid meant that the net cash from operations came in at $16.9M, a decline of $28.8M year on year. The group then spent $4.4M on unevaluated mining projects, $24.5M on property, plant and equipment with $9.8M being spent on mining equipment, upgrades to the wash plant and infrastructure at Montepuez; and $17.4M on stripping costs. They also granted a $4.7M loan to Kariba Minerals so that before financing, there was a cash outflow of $33.4M. After a $2M interest payment, the group took out a net $28.2M in new loans so that the cash outflow for the year was just $8.7M to give a cash level of $28M at the year-end.

The world’s top jewellery markets experienced double digit growth in the import of coloured gemstones. The US grew by 29%, Europe by 22% and the high jewellery manufacturing centres of France, Italy, Switzerland and the UK reported growth of 22%, 21%, 42% and 44% respectively. Hong Kong imports rose by 23% while India remains one of the most significant markets with imports rising by 6%. The highest quality rubies are commanding higher prices than diamonds of similar weights. Despite some market uncertainty, demand for coloured gemstones is expected to remain strong through the current year.

The profit at the Kagem Emerald mine was $9.3M, a decline of $19M year on year. During the year the mine progressed its fourth high wall pushback programme at the Chama pit. The programme commenced in 2014 and was designed to expose the emerald mineralisation at the SE edge by 75 metres for open pit ore production for at least two to three years at the current rate of operations. The programme progressed well and was completed in September 2015. The mine has updated its plan and is now planning for a continued waste stripping of the Chama pit over the life of the mine. The accelerated waste stripping will provide for about two to three years of ore available for mining at any given point in time.

Gemstone production for the year increased by 49% to 30.1M carats of emeralds. This production came from the Chama pit (27.8M) and the bulk sampling projects (2.3M). The increased production is mainly as a result of improved volumes of ore mined throughout the year and production was second half weighted with 18M carats produced in H2. The increase in annual carat production is in part due to the fluctuation nature of gemstone deposits as well as a result of the better rain management employed during the rainy season. The mine has the potential to increase production to around 40 to 45M carats in the forthcoming years.

Total operating costs were $44.5M with unit operating costs of $1.48 per carat compared to $1.58 per carat last year. On a cash basis, operating costs were $1.45 per carat compared to $1.36 per carat last time. The updated JORC compliant resource and reserve statement showed indicated and inferred mineral resource of 1.8BN carats at a grade of 281 carats per tonne with a net present value of $520M based on a 10% discount rate.

During the year a total of $34.8M was invested in new mining and ancillary equipment, deferred stripping costs as well as in improving the facilities and infrastructure (compared to capex of $11.9M last year). Of this total, $20.8M was spent on deferred stripping costs, $7.6M in additional mining equipment to increase production capacity, with the remaining $6.4M spent on replacing existing mining and ancillary equipment.

The Kagem washing plant achieved a total of 5,247 hours of operation. As part of the efficiency drive the wash plant processing capacity and its security arrangements are being upgraded with a view to increasing the plant output from 33 tonnes per hour to a potential 66 tonnes per hour. This will lead to an increase in optimisation of the process flows, increased operating flexibility and enhanced overall production capacity and productivity with the upgrade expected to be complete by December. The modified and new picking belts are located within an improved washing facility, leading to a better working environment with enhanced levels of ventilation, lighting and noise reduction resulting in better overall control. These improvements will also result in reduced maintenance costs, more efficient gemstone selection from the belts and enhanced overall security.

The Libwente pit, located 3km from the Chama pit is one of two new bulk sampling projects at the mine and has the potential to extend the Fwaya Pirala belt in the NE direction. Bulk sampling of the pit commenced in 2014 and has progressed well, resulting in an increase in overall scale of operations during the year. The pit was developed by the removal of the overburden which has recently reached the productive level of top TMS. A total of 2M tonnes was excavated during the year and 161K carats were produced at a grade of 37 carats per tonne, indicating the presence of potential production system.

The Fibolele pit, located 2.7km from the Chama pit also saw increased gemstone production and bulk sampling during the year. Based on the encouraging results achieved during the first of two phases of bulk sampling, a third phase has now been planned. This will increase the pit size to 590 metres in length and 50 metres in depth. A total of 2.1M carats were excavated at a grade of 167 carats per tonne.

Security initiatives implemented during the year include extensive upgrades to the CCTV infrastructure in the mining pit, security gates and sort house and the implementation of professional CCTV monitoring personnel. These measures have yielded considerable improvements but with the associated consequence of an increase in the number of apprehensions.

The profit at the Montepuez Ruby mine was $39M, an increase of $25.6M when compared to last year. During the year the group expanded the scale of the operation including additions to the fleet which saw an increase in total rock handling to an average of 250,000 tonnes per month compared to 130,000 tonnes during the last year. The total tonnes excavated in 2015 was 3M tonnes compared to 1.6M tonnes the previous year. There was an increased focus on the Mugloto block as a result of the discovery of higher value deposits spread over a large area in the alluvial gravel beds. This resulted in an overall decrease in grade, supported by a considerable increase in the value of goods mined. Around 325,000 tonnes of ore were processed by the wash plant with an average grade of 26 carats per tonne compared to 158,000 tonnes at 41 carats per tonne.

A total of 8.4M carats of rubies were produced during the year compared to 6.5M carats last year with 8.2M carats coming from the Maninge Nice primary and secondary ore and 200K carats from the Mugloto secondary ore. Total operating costs were $21.6M and unit operating costs were $2.57 per carat, an increase from the $1.12 per carat last year. Cash costs were also up, increasing from $1.68 per carat to $2.18 per carat but rock handling costs decreased by 10% to $6.16 per tonne.

During the year an additional rinsing screen was installed to replace the dry screen and improve the performance and capacity of the wash plant during the rainy season. This helped support the processing performance achieved over the year to 100 tonnes per hour. Further upgrades are proposed to increase capacity to 150 tonnes per hour with an expected run rate of 120 tonnes per hour. A water reservoir and large dam have been constructed adjacent to the wash plant for the collection of rain water. Seven large-diameter water bore holes combined with the use of water collected within the exposed bulk sampling pits further supplemented water supplies.

There are potential plans to increase the mine’s current processing capacity through the installation of a second wash plant with a 250 tonnes per hour capacity, operating at 200 tonnes per hour to give a total capacity of 320 tonnes per hour. The new process plant will incorporate washing, screening, and dense media separation optical sorters to recover rubies together with fine tailings dewatering.

The new resource statement suggested an indicated and inferred mineral resource of 467M carats of ruby at a grade of 62.3 carats. The report also confirmed probable ore reserves of 432M carats at a diluted ore grade of 15.7 carats per tonne. The mine has a projected life of 21 years producing 432 carats over its life. The projected real cash flow is about $2.76BN over the 21 years and a post-tax net asset value is $996M on a 10% discount rate with a capital expenditure totalling $305M.

During the year a total of $9.8M was invested in new mining equipment, as well as improving the infrastructure of the mine. Of this total, $7.7M was invested in additional mining equipment to increase the production capacity of the mine with the remaining $2.1M spent on replacing existing equipment. The mine’s campsite is due to undergo a significant upgrade in the coming year and a contract has been awarded for the construction of a large expansion to the residential camp. This includes new permanent housing units as well as improved roads, water purification capabilities, office and leisure facilities.

Given the size of the mine, unlicensed mining activity remains a threat. New infrastructure, a significant security presence and ongoing efforts have resulted in an improvement, however. An extensive security plan is being implemented at site level which will aim to separate the security department into an independently functioning unit. Internal security personnel with experience in the Mozambique military have been hired with the aim of increasing the skills and discipline available.

The acquisition of a controlling interest in two additional ruby deposits in Mozambique was completed during the year. The licenses of 25 years were granted to Megaruma, of which Gemfields has a 75% interest. The two licenses share a boarder with Montepuez and are expected to provide a platform for the expansion and development of the Mozambique ruby operations.

At the Kariba amethyst mine, total rock handling stood at 276,000 tonnes compared to 110,000 tonnes last year. Work commenced on the installation of a new solar power system to support a more consistent and reliable electricity supply to both the mine site and the surrounding community. The majority of the mining activity continued to take place around the Top Curlew pit which produced around 90% of the ore but in March a new pit was opened, the Curlew Main, which recently started production.

In September 2014 the group entered into an agreement with East West Gem Investments to progress opportunities in Sri Lanka for sapphires. As part of the agreement the group created a company called Ratnapura Lanka Gemstones, of which they have a 75% interest. The business has been granted a trading license which allows them to procure several small shipments of Sri Lankan sapphires for analysis. The venture has also acquired a 75% interest in certain exploration licenses covering diverse minerals and plans to commence a preliminary geological assessment covering these licenses.

In February the group completed the acquisition of 75% of shares in Web Gemstone Mining, an Ethiopian company. It holds an emerald exploration license covering a total concession area of 200 square kilometres. A base camp has been established on the concession and a team was stationed there in June 2015. Exploration work has recently been started for the coming year with a preliminary ground survey, mapping and preparation of base plans. A manual pitting and trenching exercise has been initiated on a promising area in the north of the license and the results of these activities will help guide the future course of exploration in the area. Oriental Mining in Madagascar has not been subject to any large scale ground activity this year due to several political changes in the country.

The loss at Faberge came in at $15.1M which was the same as in 2015. The business continued to expand its global presence during the year via an increasing number of agreements with retail partners. Faberge products are now available in Australia, Czech Rep, Malta, Qatar, Saudi Arabia, Switzerland, Thailand, UAE, Ukraine and the US. Since the year-end further agreements have been completed resulting in their products also being available in Azerbaijan, Bahrain and Canada.

During the year Faberge underwent further optimisation of the business, including management appointments, as part of a strategy to become a profitable standalone business within the group. Progress was made across all the product categories of jewellery, time pieces and the relaunch of Imperial Class Objects. Political turbulence in important markets such as Russia and Ukraine, and investment in branding and marketing campaigns which are yet to be released, impacted overall sales growth at the business. Record orders were received at Basel World 2015, however, with these revenues being recognised over the coming year when the deliveries are made. The business also recorded improving revenues from sales of larger coloured gemstones through its Devotion collection.

Cost saving initiatives resulted in a 5% saving on admin costs with total operating costs of $18.1M but this didn’t prevent the hefty loss. The total number of Faberge boutiques increased from 16 to 20 during the year. Faberge continued its association with Harrods in the run up to Easter with events including the Faberge Egg Burst, which allowed clients to design their own Faberge Egg that was then displayed in the Harrods front window using 3D mapping. In addition, the in-store Faberge Egg Hunt engaged visitors in hunting for six collectors’ eggs hidden throughout Harrods using a specially designed app. Faberge also exhibited at the design fair Masterpiece London for the first time in June.

During the year the group relaunched the Imperial Egg class objects and the first one, the Faberge Pearl Egg, was introduced at the Doha International Jewellery show and was purchased in Doha by Hussain Al Fardan, one of the largest pearl collectors in the world. The second Imperial Class Objet set is close to completion and comprises a series of four eggs that reflect the four seasons. Each egg is designed to carry a surprise inside (a bit like an expensive Kinder Egg then). The summer egg was presented at the Faberge salon at Masterpiece London in June.

During the year the group launched the timepiece collection including the Faberge Lady Compliqee Peacock and Winter timepieces, and the Men’s Visionnaire I. The ladies watches offer a movement that has been created for Faberge and comprises of a four-cog mechanism that enables a peacock’s tail, or a snowflake, to fan out with the passage of time. The men’s Visionnare I offers a flying tourbillon. The dial is made up of seven separate segments that cover the movement only partially. The timepieces will be available to buy at Faberge boutiques and partner’s points of sale from November.

Basel World saw the release of the jewellery collection “Summer in Provence” and the new Rococo and Heritage core collections. The Secret Garden collection was presented at the Internaltional Jewellery Show in Doha in February. Faberge’s new advertising campaigns will launch in November and combined with the expanded presence globally, this should set the stage for further improvements in overall sales. The business is particularly pleased with the reception for its timepiece and Objets collections.

During the year the group held three rough emerald auctions as well as three rough ruby auctions. The first emerald auction was an auction of lower quality stones and out of 12.1M carats offered, 11.6M were sold generating revenue of $15.5M at a price of $1.34 per carat. The second emerald auction was of higher quality stones and out of 600K carats offered, 530K were sold generating revenue of $34.9M at an average price of $65.89m per carat, a significant increase over the previous high of $59.31 per carat. At the third emerald auction, revenues of $14.5M were realised on the sale of 3.9M carats of lower quality stones at a price of $3.72 per carat. It is notable that of the 10.1M carats offered, only 3.9M were sold. After the year-end the group conducted a high quality emerald and amethyst auction which yielded revenues of $34.7M for the emeralds and $440K for the amethysts.

The first ruby auction was of higher quality stones which generated $43.3M for 62,936 carats sold from the total of 85,491 carats offered with an average realised price of $688.64 per carat. The second auction was one of lower quality rubies which generated $15.9M for 3.96M carats sold out of the total of 4.03M carats offered at a price of $4.02 per carat. The third auction generated revenues of $29.3M for 47,451 carats sold out of the total of 72,208 offered. The average realised price was $617.42 per carat. There was also an amethyst auction with a total of 27.7M carats of higher quality amethyst being offered. The sale of 13 of the total 14 lots generated revenues of $450K at an average value of 1.77c per carat.

At the year-end the group has capital commitments of $3.2M for the overburden removal at Kagem and $4.4M for the purchase of mining equipment and mine camp expansion at Montepuez.

In September the group acquired controlling interests in two emerald projects in Colombia. The Coscuez Licence includes exclusive rights for the exploration, construction and mining of emerald deposits granted by the Colombian government within the area of Coscuez in San Pablo de Borbur, Boyaca. In the past the area has hosted the Coscuez mine, one of history’s more significant emerald mines, having been in operation for over 25 years. In 1990, open pit mining was replaced by small scale underground mining in the upper reaches of the deposit with extraction taking place from adits mines into the hillside. Under the terms of the agreement, Esmeracol will transfer the license to a newly incorporated company imaginatively called Coscuez NewCo and Gemfields will acquire an indirect 70% interest in this company. Further exploration activity needs to be carried out to support the development of a geological model and a prelim mine plan, all of which is likely to take up to two years.

The total consideration payable is $15M with the first tranche of $7.5M due on completion, $5M in cash and $2.5M in Gemfields shares. A second tranche of $2.5M is due on the first anniversary of completion and a third and fourth tranche of $2.5M each upon attainment of agreed profit targets. Completion is expected to occur by March 2016.

The second project comprises a number of new license applications and assignments to existing concession contracts administered by the Colombian Mining Agency. The applicants for the mining licenses are a number of Colombian companies indirectly controlled by ISAM Europa. Gemfields has acquired indirect 75% and 70% effective interests in underlying licence applications and assignments through two holding companies which own the assorted Colombian companies. The total package of mining license applications and assigned concession contracts cover about 20,000 hectares in the Boyaca and other Colombian departments and comprise mostly greenfield sites, although small scale mining has occurred in some of the license area. Eight of the assignments have been approved and issued so far with the remaining applications under review.

The total consideration payable is $7.5M with the first tranche of $450K being paid on acquisition. A second tranche is payable upon granting of certain license applications, a third tranche is payable when bulk sampling commences on certain license areas, a fourth tranche is payable on the commencement of commercial mining and a fifth and sixth tranche (comprising more than half of the total consideration) is payable upon attainment of agreed revenue targets.

There are now a number of new projects and assets. The group has a 100% interest in Oriental Mining with nine exploration licenses covering emeralds, rubies and sapphires in Madagascar. There are eleven additional licenses in the process of being transferred with initial stages of geological evaluation being completed. The group also has a 75% interest in the Megaruma licenses, two additional ruby deposits in the Motepuez district and share a boundary with the current mine. They have a 75% interest in Ratnapura Lanka Gemstones, a trading company which will source rough diamonds from local parties. They have a 75% interest in Web Gemstone with an interest in an emerald exploration license in Ethiopia. Exploration work has commenced for the coming year with a prelim ground survey, mapping and preparation of base plans.

There also have a 70% interest in the Cosuez Emerald mine in Colombia, one of the largest emerald mines in the world with completion expected to occur in March,; and 75% and 70% interests in selected Colombian exploration prospects.

During the year the group took out a $25M medium term loan with Macquarie which bares interest of US LIBOR + 4.5%. This loan was used to repay the $15M related party loan with Pallinghurst and to fund working capital requirements. The group also has a $20M revolving credit facility with Barclays with the same interest rate which was mainly used to pay the contractor undertaking the removal of waste in the Chama pit in Kagem and to fund working capital requirements. The $15M related party loan was repaid in full during the year. After the year-end, two debt facilities of $10M were entered into with Barclays Mauritius and Pallinghurst. The interest rate for both loans was the same as above and the Barclays loan was to support the overburden removal and financing of capital expenditure whilst the Pallinghurst loan, which is repayable in December this year is for inventory investment and working capital.

With further emerald and ruby auctions scheduled to take place in the latter part of 2015, continued organic growth at both Kagem and Montepuez, and a focus on acquisitions and expansion, the board “look forward to another strong and successful year”. The group are targeting at least three emerald and ruby auctions next year. Following the acquisition of exploration licenses in Sri Lanka, Colombia, Mozambique and Ethiopia the group are forecasting an increase in exploration costs though. They are targeting 25M to 30M carats of emerald and beryl production in Kagem and 8M carats of ruby and corundum at Montepuez.

Going forward, the group are installing a second washplant at Montepuez and an upgrade to the washplant to increase processing capacity to 320 tonnes per hour by 2017 is being considered and this should allow increased production to 20M carats of rubies by 2018. Additional capital expenditure is planned for exploration in existing mines and new projects and accelerated waste stripping in the Chama pit operation should increase production to around 40 to 45M carats in the forthcoming years.

At the current share price the PE is a huge 117.2 falling to 23.6 on next year’s consensus forecast which seems more reasonable but still rather costly.

Overall then this was a very disappointing set of results. Profits fell considerably, although net tangible assets did increase year on year. The operating cash flow was also down but this was due to a large increase in inventory, possibly as more gems remained unsold at the auctions, and underlying cash profits actually increased when compared to 2014. The operating cash flow is not covering capex at the moment, though, so it doesn’t look like we are at a cash break-even point here. The decline in fortunes seems to have been due to a crash in the profits made at Kagem, despite the increase in carats produced. The reason for this is a little puzzling as unit costs did not increase, perhaps more lower quality gems were produced during the year.

Progress at Montepuez was much better and the rubies are looking like a better prospect now than the emeralds in my view. The losses at Faberge continued but did not get any worse. If the group could get the division even to a breakeven point, then that would considerably improve earnings at Gemfields. Despite the lack of progress this year, partly as a result of the conflict in Ukraine and increased marketing costs, next year does seem as though it could offer some improvements with increasing demand for some of the products. In conclusion, at a forward PE of 23.6, this still looks a little expensive so I will wait on the side lines for now.

The market did not react well to the results, as would be expected. The shares now trade below the 200 day moving average.

On the 4th November, the group released an update covering Q1 2016. At Kagem, production of emeralds increased from 6.3M carats to 7.5M carats with an average grade of 237 carats per tonne compared to 214 carats per tonne in Q1 2015 although in Q4 2015, 8.1M carats were produced at a grade of 222 carats per tonne. Total operating costs of $11.1M grew slightly on account of the increased scale of mining and exploration activities being carried out across the mining licence. Unit operating costs of $1.48 per carat was lower than the $1.63 recorded in the same quarter of last year.

The fourth high wall pushback at the Chama pit progressed during the period and completed in September. A total of 4MT of waste was moved during the quarter. The group have revisited their mine plan for the pit, following the updated resource statement, and they are now looking at the option of continued waste stripping over the life of the mine. This will ensure that two to three years of ore is available for mining at any given point in time. In addition the exploration and bulk sampling activities at the Fibolele and Libwente pits are progressing well and have yielded some promising results.

The September auction of higher quality emeralds held in Singapore saw 590K carats being sold, representing 88% of the value offered and generating revenues of $34.7M at an average of $58.42 per carat, the third highest average price achieved to date but below that of the last auction.

At Montepuez, the focus on delineating additional areas of higher quality alluvial resource resulted in production of 500K carats of ruby versus 2.9M carats in Q1 2015 at an average grade of 7 carats per tonne against 41 carats last time attributed to a greater proportion of higher quality but lower grade alluvial ore deposit processed during the quarter. Total operating costs of $6.1M were above those of $4.3M in Q1 2015 due to the increase in scale of exploration, processing and mining activities. Unit operating costs of $12.2 per carats against $1.48 last time was driven by the shift in focus to mining and processing ore from areas of higher quality but lower grade.

The ongoing mining and bulk sampling operations continued to provide positive results and insight into the geology of the deposit. The ongoing test work has led to an enhanced understanding of the ore characteristics, supported the identification of additional higher value but lower grade alluvial ore resources and improved throughput in the existing semi-mobile processing plant. These improvements saw a 4% increase in tonnes processed when compared to Q1 2015.

With the key focus being on mining the Mugloto block, where the higher value deposit is spread over a large area, as well as the delineation of an additional and recently identified area that has the potential to produce material of exceptional quality resulted in a reduced overall grade of seven carats per tonne and the production of just 500K carats of ruby but with a 96% increase in the volume of higher quality rubies being recovered. The construction of the new Montepuez camp started in March. A total of 102 housing units, a recreation unit, canteen and new kitchen will be built. The first set of new housing will be ready for inhabitants by the end of November with completion of the camp and grounds scheduled for early 2016.

At Faberge, gross profits from sales orders agreed during the quarter increased by 61% when compared to Q1 2015. The gross profit margin on sales orders agreed increased from 30% to 51% over the same period. The number of items included in sales orders increased by 241% while revenues from sales orders agreed fell by 4% with results for Q1 2015 being skewed by the sale of a single exceptionally high value item. Total operating costs increased by 6%, largely due to an increase in advertising spend. In July, the retail partner in Bangkok held a grand opening and press call. The event attracted significant interest from local media and a number of sales were made. By the end of September, Faberge opened four of its own retail outlets and a further 22 points of sale with retail partners.

In September an auction of higher quality rough amethyst held in Singapore generated revenues of $440K at an average price of 4.32c per carat, the highest ever achieved at any of Gemfields’ amethyst auctions. In Sri Lanka the group continued to set up procedures and equipment required for trading operations. Placement of the key management team has been completed and sapphire trading is expected to start in Q2 with associated supply chain mechanisms being developed.

In Ethiopia, following the completion of the acquisition of 75% of an exploration licence, an exploration team was recruited and established on site to help develop a better understanding of the license area. A base camp has been established on the concession and a team was stationed there in June. Exploration work has recently commenced, consisting of a ground survey, mapping and preparation of base plans. A manual pitting and trenching exercise has been initiated on a promising area in the northern part of the license, selected on geological indicators and past artisanal activity.

At the end of the quarter, the group had a cash position of $41.1M with a net debt position of $18.9M with general expenses of $11.5M. The production target for rubies remains at 8M carats for the year and for emeralds it is 25M to 30M carats.

Overall then, this seems to have been a bit of a difficult quarter for the group with Kagem production down compared to the previous quarter and Montepuez production much lower as the group mined higher quality but lower grade ore. Faberge at least seems to be making progress but I don’t think the time is right to jump back in here.

On the 23rd November the group released the results from its auction of lower quality rough emeralds which was held in India, the first time a lower quality emerald auction was held outside Zambia since 2012. The auction saw 5.07M carats of the gem on offer with 18 of the 23 lots being sold generating $19.2M at a value of $4.32 per carat which compares favourably to the $14.5M generated at $3.72 per carat last time.

The event was also used to sell higher quality emeralds purchased on the open market which yielded $1.1M.

Overall then, these are pretty robust results although really it is the higher quality emerald and ruby auctions which are more important though.

On the 3rd December it was announced that Finn Behnken, a director of the company, purchased 75,000 shares at a value of £29.3K. This represents his first purchase.

On the 21st December the group released the results of their recent auction of higher and medium quality rough ruby held in Singapore. The auction generated revenues of $28.8M at an average price of $317.92 per carat with 45 of the 49 lots being sold. Given that the quality mix offered at this auction comprised a new blend of both higher and medium quality rubies, the result apparently cannot be directly compared with prior auctions but the per carat price achieved apparently remained broadly consistent with previous auctions. This is just as well given that the last auction of higher quality ruby generated an average price of $617.42 per carat and generated revenue of $29.3M, although less lots were sold in that auction.

Although some degree of softening in the demand for certain darker tone and lower quality grades remains, this is expected to be overcome as the group’s consumer education initiatives continue to reach a broader cross section of markets as key economies continued to strengthen. So far this year, two emerald and one ruby auction have raised $82.7M in revenue. Overall, this is not too bad but there is not a great deal to get excited about if I am honest.

On the 16th February the group released an update covering trading in Q2. The total production at Kagem was 8.2M carats compared to 7.5M carats in Q1 and 5.8M carats in Q2 last year. The average grade was also higher with the 272 carat per tonne figure comparing favourably to the 237 recorded in Q1 and the 190 recorded in Q2 2015. The capital expenditure on the mine was also well down and the total gemstone unit costs was $1.38 per carat compared to $1.48 in Q1 and $2 in Q2 last year.

The fourth high wall pushback was completed in September 2015, leaving about 15 months of exposed ore available for mining and continued waste stripping of the Chama pit will be done in-house for the foreseeable future. Total rock handling during the quarter was 2.8MT, with all of this being moved by the in-house mining team. Increasing the overall strike length at the Chama pit operation and optimising the blasting and scheduling techniques assisted in further improved mining efficiencies and productivity. In addition, the exploration and bulk sampling activities at the Fibolele and Libwente pits are progressing well and have so far yielded some promising results. The mining operations at the Fibolele pit have advanced during the period, taking it to an extended strike length of 600 metres and yielding 1.6M carats of emerald during the period.

Kagem has also increased its processing efficiency and capacity following an upgrade and extension to the existing washing plant facility, as well as the installation of an updated digital security and surveillance infrastructure. An improved climate-controlled environment has also been established within the extended picking facility, resulting in an improved working environment and better operating controls.

The November auction of lower quality emerald held in India saw 2.45M carats being sold, representing 95% of the value offered and generated revenue of $19.2M. The auction yielded an overall average value of $4.32 per carat, which is apparently the highest price achieved to date for lower quality emeralds. There was also a November traded auction of higher quality rough emeralds, originating from Zambia and Brazil and obtained in the open market which yielded revenues of $1.1M with 20,400 carats being sold.

At Montepuez, the total production was 1.6M carats compared to 500K carats in Q1 and 3.4M carats in Q4 last year and in the half year, the production was 2.1M carats compared to 6.3M carats in H1 last year. The grade was 22 carats per tonne compared to 7 carats in Q1 and 34 carats in Q4 last year. Capital expenditure was similar to last year, at $5.1M in the half year period. The gemstone unit cost was $4.31 per carat compared to $12.20 in Q1 and $1.68 per carat in Q4 last year.

The sampling operations led to an enhanced understanding of the ore characteristics and has supported the identification of additional higher value, lower grade alluvial ore resources. Throughput at the existing semi-mobile processing plant saw a 29% decrease in tonnes processed when compared to the same quarter last year, largely on account of the rainy season making the clay-rich head feed difficult to process. Upgrades to the existing wash plant are planned to be carried out in a phased manner throughout 2016 with a view to further improving its processing efficiency.

The total ore mined in the quarter amounted to 132.9KT against 158.2KT in Q2 last year, of which 71.7KT were processed compared to 101.4KT last time. The key focus has been on mining the Mugloto block, where a known higher value deposit is spread over a large area, as well as the delineation of an additional and recently identified area that has the potential to produce material of an exceptional quality, resulting in an increase in the volume of waste mining and a total of 922Kt being moved. Increased processing of the Mugloto ore led to the reduced overall grade but a 1,825% increase in the volume of higher quality rubies recovered.

The construction of the new camp started in March 2015 with a total of 102 housing units, a recreation unit, canteen and new kitchen being built. The first set of housing units have been commissioned and allotted with completion of the project targeted for the end of April. Unlicensed mining activity and asset loss remain key challenges. The implementation of new infrastructure facilities and improved technological interventions such as the enhancement of radio communication ranges, mobile camera lighting towers, increased numbers of CCTV cameras and mobile guard posts resulted in a visible improvement in overall security. An extensive plan has been formulated and is being implemented at site level and a training programme for security staff incorporating human rights and soft skill development has been provided.

The December auction of higher and medium quality ruby held in Singapore saw 90,642 carats being sold, representing 95% of the value offered and generated revenues of $28.8M. It yielded an average value of $317.92 per carat.

Faberge saw a strong quarter with sales orders agreed increased by 13% when compared to Q2 last year and the gross profit margin increased from 31% to 49% with unit sales increasing by 48%. Total operating costs increased by 16% though, largely due to an increase in advertising spend.

In Colombia, exploration and mine planning activities such as drone surface topographic survey, underground survey and prelim assessment of engineering solutions for Coscuez Emerald Mine access were initiated as part of the ground preparations for future operations. Further exploration activity will be carried out over the next two years to support the development of a geological model and a prelim mine plan.

In Sri Lanka the group has completed the establishment of the required infrastructure and equipment for trading in Colombo and Ratnapura. The group have also completed its prelim assessment on some of the exploration licenses covering diverse minerals and expects to continue its assessment of the other licences during the year.

In Ethiopia, the manual trenching exercise has been completed on a promising area in the northern part of the license named Dogogo Hill. The block measures 1.92Km2, covering a strike length of 2.4Km with eight trenches being planned at 100 metre intervals. Excavation of the trenches was completed in November with a cumulative length of 2.2Km. These trenches exposed contacts between pegmatites and talcose schists, and the occurrence of beryl has been recorded. A pitting exercise has been initiated at the contact zones exposed during the trenching. A geological mapping exercise has also been completed at various scales in another block to the south of the license called Karolo Kora Hill. This block measures 13.75Km2 and covers a 5.5Km strike length of the ultramafic belt.

Overall then, Kagem delivered a 41% increase in production volumes year on year while costs continue to be well maintained. Montepuez continues to produce encouraging results including a high level of confidence that the production volumes will soon be supported by the planned shift in mining focus to areas where the grade is higher but with a reduction in value in the coming months. The board maintain their production target of 25 to 30 million carats of rough emeralds and 8 million carats for rough rubies.

At the period-end, the group had cash of $24.9M and total debt of $55M and incurred expenses of $14.5M during the half year.

Overall then, there is a lot of detail here to get through. Kagem seems to be doing well, with increased production and lower costs but Montepuez seems to be a bit more variable and it is difficult to understand how the changes in grade and values will affect the accounts. The cash level seems to be somewhat lower than at the end of last year with an increase in debt so despite the low capex at Kagem, there doesn’t seem to be any cash generated. So, whilst things look promising I think I will wait for the interim results before I buy in here (they are due next week).