Goals Soccer Centres has now released their interim results for the year ending 2015.

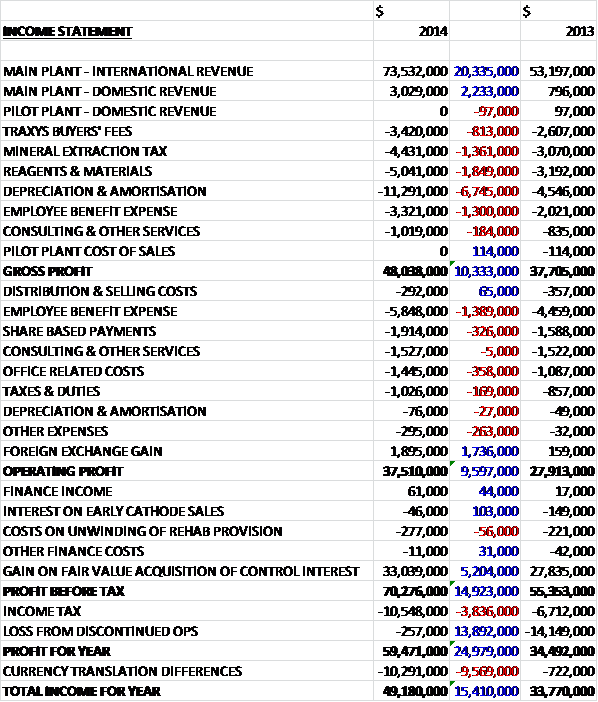

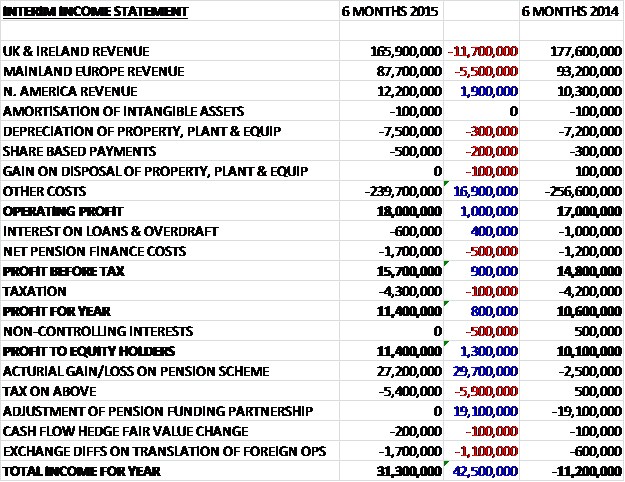

When compared to the first half of last year, revenues were broadly flat, down by just £35K. There was also a small increase in the underlying cost of sales due to rent reviews and increases in business rates but the lack of the £571K bad debt provision that occurred in the first half of last year meant that gross profit was £439K higher. A lower depreciation of tangible assets was more than offset by a growth in other admin expenses as the group increased resources in the head office and hired a US development director so that the operating profit was flat year on year. Underlying finance expenses were some £647K lower, however, due to the reduction in borrowings and the period also benefited from the lack of the cancellation of the interest rate swap and the bank arrangement fees written off last time so that after a higher tax bill, the profit for the period stood at £3.5M, an increase of £3.3M when compared to the first half of 2014.

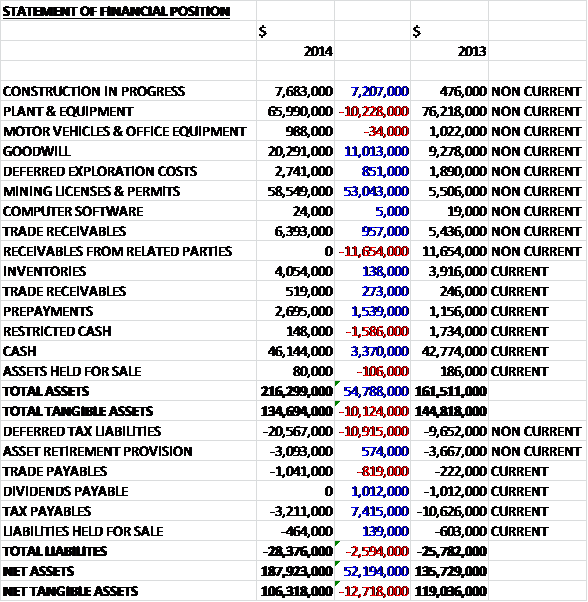

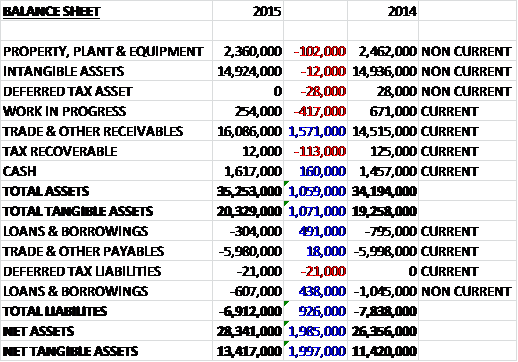

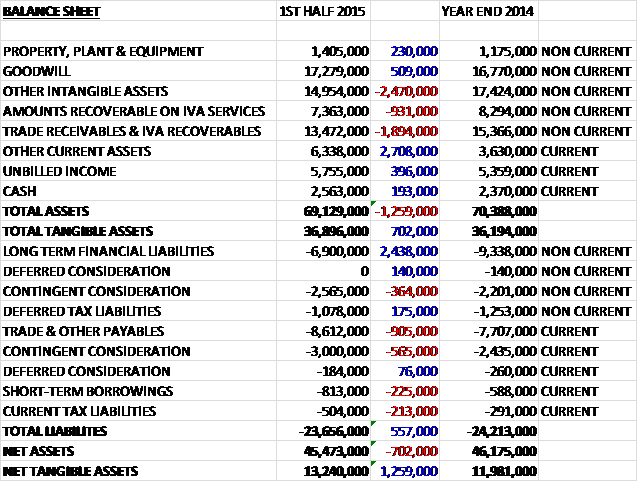

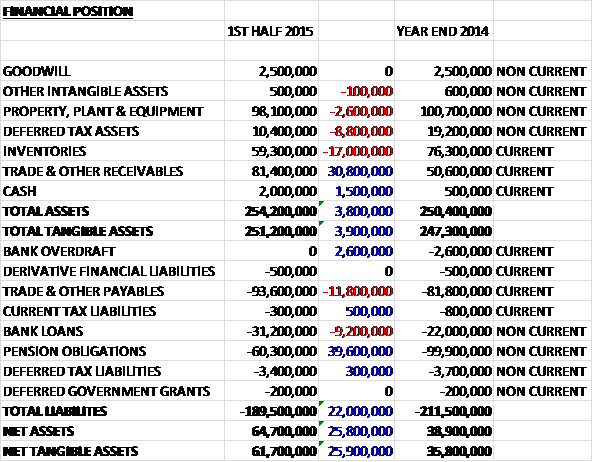

When compared to the end point of last year, total assets increased by £4.5M driven by a £4.5M growth in the value of leasehold property and a £1.8M increase in other receivables relating to VAT on capital expenditure incurred in the company, partially offset by a £1.9M decline in assets under construction, presumably as they were transferred to leasehold property. Total liabilities also increased during the year mainly due to a £1.2M growth in the bank loan and a £509K increase in current tax liabilities. The end result is a net tangible asset level of £73.9M, an increase of £2.2M year on year. I have mentioned before, however, that I am not very comfortable with the bulk of the assets being leasehold properties when the operating lease liabilities are not on the balance sheet.

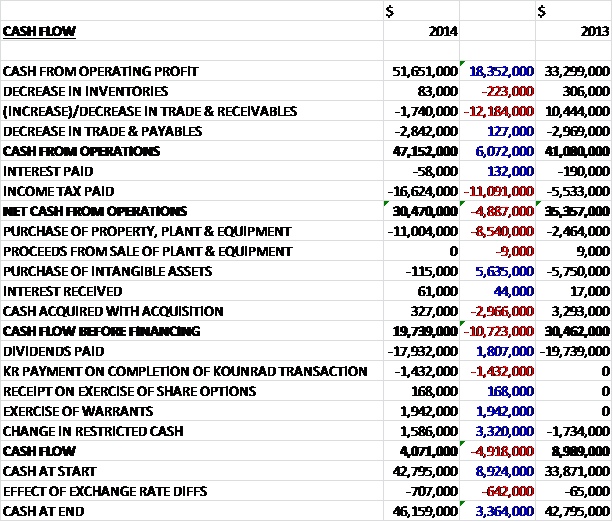

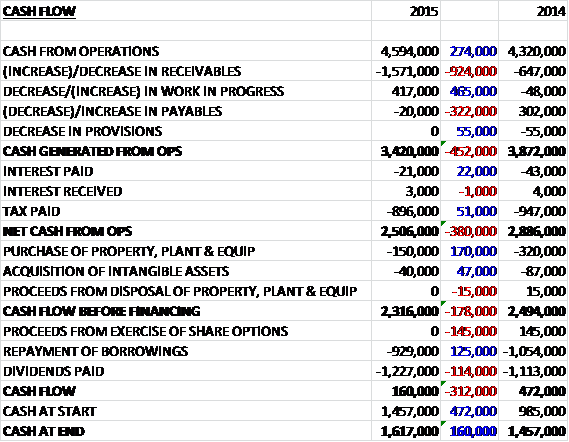

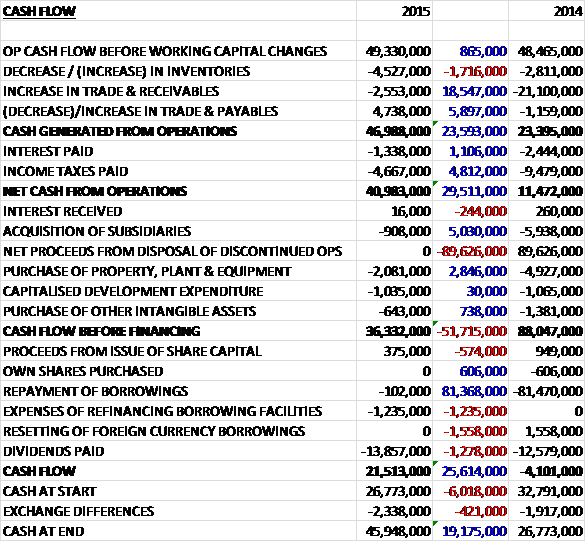

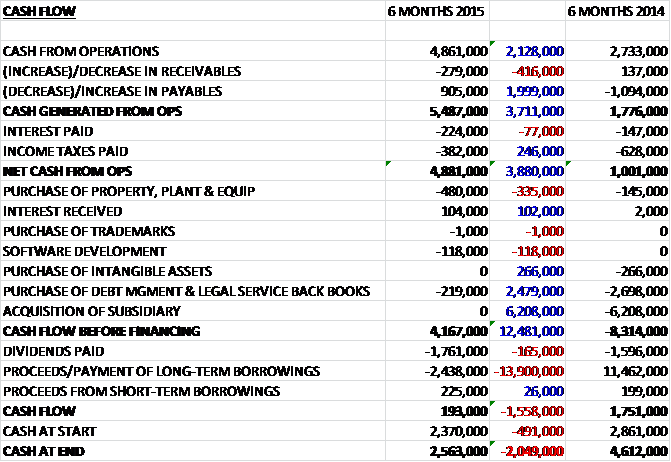

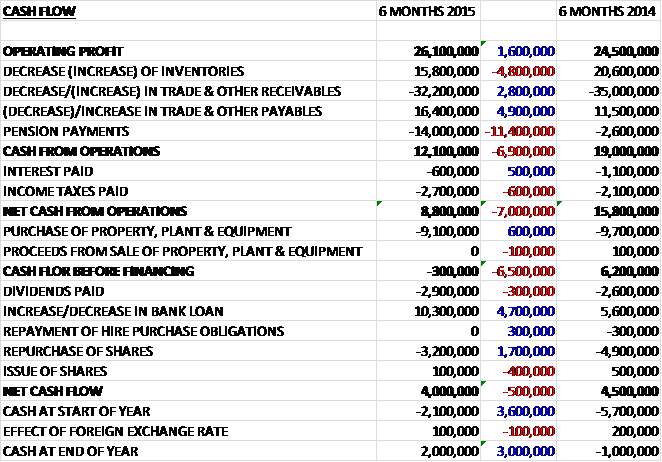

Before movements in working capital, cash profits fell by £221K to £6.2M. This was further eroded by an increase in receivables, partially offset by a decline in tax so that net cash from operations stood at £4.3M, a decline of £1.4M year on year. The group spent £3.6M on tangible assets with £2.5M being incurred on the new centres and £1.1M on upgrading existing centres, £349K on interest and £612K on software development so that there was no free cash flow for the period. The group then drew down £1.2M in loans in order to pay the dividends and give a cash flow for the year of £208K and a cash level of just £77K at the period end.

In the UK business, sales for the first half of the year fell by 1% to £16.4M with like for like sales down 2%. Football, bar, vending and other revenues all fell 2% on a like for like basis. During the period the group experienced some softness in the casual football product, which represents about 45% of sales with like for like sales declining by 5%. This product performed particularly strongly last year when the majority of grass 11-a-side pitches across much of England were closed due to flooding during Q1 resulting in an influx of teams seeking artificial pitches for training and play.

A few centres have lost some casual footfall customers as a result of local authorities actively marketing their all-weather pitches at lower prices, but the board are confident that their focus on delivering a quality experience in facilities with dedicated 5-a-side arenas will allow them to maintain their market leading position in the sector. A new loyalty initiative has been implemented along with a focus on customer service to ensure they continue the best experience in the sector. Like for like bar and vending sales were down 2% despite the mid-week sales increasing by 2% due to declines at the weekends, although margins were held during the period.

The centre in Los Angeles delivered very good growth with sales up 22% to £600K, although they were “only” up 12% on a constant currency basis. EBITDA at the centre increased by 23% to £343K which is a strong performance from a centre that has 11 pitches and does not benefit from bar or function sales. The group are currently making progress in developing good relationships with local government as well as local school districts and property developers and they now have a solid pipeline of quality sites. Legals have been concluded, planning consent achieved and building permits are at an advanced stage on one site with construction planned to commence in the second half of the year. In addition, they have agreed heads of terms and commenced the legal process on a further three sites. In the UK, the group opened a new centre in Manchester in February and Doncaster in April

The new mobile app and responsive website were launched in December, providing an improved experience for customers. Downloads of the app are running ahead of expectation with over 34,000 to date and continuing at a rate of 500 each week. Whilst downloads have been ahead of expectations, use of the various features is variable with those relying on full team interaction taking longer to be adopted than those used by single players. Functions such as league fixture and results are heavily accessed by players whist team organisation and player payments are taking longer.

One encouraging area is the use of the Player Blast functionality where team organisers and potential players are brought together to save a game that might otherwise have been cancelled due to a lack of participants. Customers have sent over 5,000 player blasts in the current year resulting in 4,500 games going ahead which may otherwise have been cancelled. Some functions such as league information, online booking and team management are aimed at improving the customer experience while others such as Player Blast and individual player payments have a direct financial benefit for the company.

The group are continuing to promote the app and are developing a new app based loyalty scheme which will provide benefits to organisers and players when they use specific functionality. The board believe that, once fully adopted, the functionality within the app will help reduce cancellations and make the game far more accessible to a wider audience. It will also allow the group to develop a relationship with each player for the first time, tracking their playing habits and allowing them to market directly to the customer via email, SMS and in-app with tailored offers. A new mobile friendly website was launched in Q1 2015 in the UK and Q2 in the US. Since launch, online booking have increased by 23% and online kids party bookings by 24%.

The group started the year with a major marketing push with the Get Fit campaign which promoted the health and fitness benefits of playing 5 a side football. Marketed heavily on social media, they supplemented the benefits of playing football with activities in-branch such as providing fitness tips and the chance to win Jawbone wearable technology. Unfortunately this campaign coincided with a period of adverse weather and did not generate the strong start to the year that is usually experienced at this time.

The group continues to hold national tournaments for clients such as McDonalds, JD Wetherspoon and Odeon. They also, along with two other major providers, hosted teams across England for the FA People’s cup, a major tournament promoted by the FA and BBC. Goals achieved the highest number of entries per centre and the Manchester centre was selected as the venue for the final which was broadcast on the BBC. A major kids party promotion through digital channels has delivered a 16% increase in bookings on top of a strong year last year.

All new centres and resurfaced pitches will now feature the group’s “Stadium Turf”, artificial turf with two shades of green reflecting the pitch perfect conditions of the newly rolled pitch before a big stadium game and feedback from players has so far apparently been excellent. The Goals Cam technology trialled last year has proven successful and this has been extended to five centres this year. In addition, after successful tests in two centres, the group rolled out their new Soccer Blast product, a kids party experience aimed at older children and youths, in Q2

Sales in the first nine weeks of the new period have been challenging in the UK with like for like sales over the summer holiday period falling by 10% due to tough comparable trading in the weeks following the world cup and a significant increase in both league and casual teams cancelling over the holiday period. The board think that this is due to organisers struggling to find sufficient players for their game to go ahead as they took advantage of the strong pound during a period of poor UK weather to holiday abroad ( not sure why that would have a different effect to people holidaying at home). The strong trading momentum at the LA centre has continued into the second half of the year, however.

In response to the weak summer period, the group have enhanced their annual September Uplift marketing campaign aimed at driving summer lapsed and new teams into the centres following the traditional summer period of lower activity. It is expected that this uprated campaign, together with new retention tactics will drive an increase in sales over the next few months. With the lack of visibility, however, having just commenced the campaign, the board is adopting a more cautious view of the full year outcome and is revising its profit before tax guidance for the full year to between £9.3M to £9.8M

The interim dividend was kept the same (not a great vote of confidence) so the rolling annual yield is currently 1.3%. The net debt at the period end stood at £38M compared to £36.9M at the end point of last year.

Overall then this has been a difficult year for the group. Underlying profits were actually modestly ahead of last year due to the reduction in debt meaning less was spent on finance costs and net assets increased due to more leaseholds (my opinion on these leaseholds is unchanged) but operating cash flow fell and the group is making no free cash despite spending money on dividends. The LA centre has actually performed well but it seems frustratingly slow to open any more centres in the area. The UK performed less well due to a lower number of casual players, apparently mostly because last year much of the competition was flooded in Q1 and this year, local authorities have been stepping up their offering.

Sales in the new year so far are down by 10% due to a strong post-world cup comparison this year and apparently more people going on holiday instead of playing football. I am not sure about that, but the revised profit figures of £9.3M to £9.8M actually don’t look that bad. The shares currently yield an unexciting 1.3% and they have a net debt of £38M which still seems a little high to me. So, in conclusion, the US opportunity does look very good but progress at this company really seems to be at a snail’s pace and there does not seem to be much progress. The debt still seems a little high to me and the assets are just leasehold buildings with the lease payments off the balance sheet. I am not that tempted to buy any shares despite the collapse in the price following this announcement.

On the 9th November the group announced a trading update. Conditions in the UK business over the summer period have been challenging. Whilst progress has been made since the September update, delivering week on week sales improvements, the speed of the recovery was not at the level anticipated. In view of this, the board now anticipates that pre-tax profit for the year will be between £8.2M and £8.6M in the absence of adverse weather conditions.

I don’t normally update on changes in ownership but on the 12th November Sports Direct acquired just under 5% of the company through a CFD. It is unclear whether they intend to make a bid by Mike Ashley, Sports Direct owner, seems to be quite a shrewd operator so he obviously sees some value here. I will not be following him in quiet yet but this is an interesting development.

On the 27th November the group announced the appointment of Nick Basing as deputy chairman with a view to him stepping up to the role of Chairman at the company’s AGM next year.

On the 14th January the group released a trading update covering 2015. Trading for the year was in line with revised market expectations with sales of £32.9M representing a UK like for like decline of 7%. The US business delivered strong growth, however, with sales for the year up 9%. It was also announced that CEO Keith Rogers will step down and relocate to the US business to become president which is an interesting development. To be honest I can’t seem much potential here so this will be my last update for the company.

On the 3rd June the group released an interesting update covering their strategic review, the conclusion of which was that they will raise about £16.75M through a placing of 16,750,000 new shares at a price of £1 per share.

The board have admitted that the group has suffered from long periods of site under-investment which has restricted the modernisation of existing centres, largely due to legal commitments to invest in new centres along with a need to deleverage the balance sheet. This has resulted in 14 centres having an average age of over nine years compared to an expected life of ten years.

The net proceeds of the placing will be used on an arena modernisation and catch-up programme, a clubhouse refurbishment programme, a committed US pilot site and to deleverage the balance sheet. The placing shares will represent about 28.6% of the existing share capital and the placing price represents a discount of just 3.4% on the latest closing price.

The arena modernisation programme will cost £3.5M and is being immediately implemented with 25 centres scheduled to be modernised before October. This will include the playing surfaces to be replaced by high quality twin stripe 5G artificial turf and all new pitches will have shockpads installed under the playing surface to help extend pitch life and improve game quality, along with new LED floodlights which will also reduce lighting costs. Furthermore, 14 seven a side pitches will be created through the conversion of 28 five a side pitches to meet increased demand. The pitch age profile will significantly improve upon the above investment with 30% of pitches being less than a year old. In addition to this £3.5M catch-up investment, £1.6M has also been committed to be spent on Arena modernisation in 2016.

The clubhouse refurbishment programme will cost £7.9M. A new brand vision has been developed and a 2020 Club concept will be retrofitted to upgrade the estate. Selected centres will be significantly redesigned and facilities relaunched to drive enhanced returns. All centres will benefit from the refurbishment of reception and changing areas, new signage, upgraded café facilities and the utilisation of unused space. The new club concept will be introduced at two pilot centres in Q3 and then rolled out across the remainder of the estate over the next two years.

The US pilot will cost £2.6M. The group is contractually committed to a new pilot site in Pomona, LA, which is due to open in December. A new centre concept has been developed for the US, refining the design of the Southgate centre with ten arenas and a new clubhouse format. There is an advanced pipeline of four additional potential centres, all situated in the LA area, but no further centres will be committed until target returns at Pomona are meeting expectations.

There are four strategic priorities that have been set, which are to grow and innovate the UK core estate through refurbishment of the existing buildings to a new upgraded brand format, and accelerating the Arena modernisation programme and introduce new technology to enhance the customer experience; to develop new capabilities aimed at underdeveloped growth segments, relaunching quality offering for advanced booked customers, upgrade IT systems and refresh the operating environment.

Other initiatives include the international expansion of centres with another centre to be opened in LA in the second half of the year and investigating the market potential to leverage the brand in Asia; and to inlock underlying asset potential through the development of additional revenue generating lines of business.

The new aim is to improve ROCE and increase value for shareholders which means a targeted EBITDA return of 30% on the arena modernisation, a 15% return on clubhouse refurbishments and a 20% return on a committed US pilot. The board are also looking to maintain net debt/EBITDA below 2.5x and return to paying dividends in 2017 when the balance sheet recovers.

Trading so far this year has been similar to that announced last time with like for like sales marginally negative. Overall, it really sounds like the new leadership team are giving the group the best chance for success. I like the idea of the investments and the placing seems to have been well received. Given further improvements in the balance sheet and the investment in the company’s assets, this might just be investible again and is looking rather interesting in my view.

On the 4th July the group announced that founder and MD Keith Rogers sold 70,000 shares at a value of £79K. He still owns 3,960,446 shares in the company.