Circle Oil has now released its interim results for the year ending 2015.

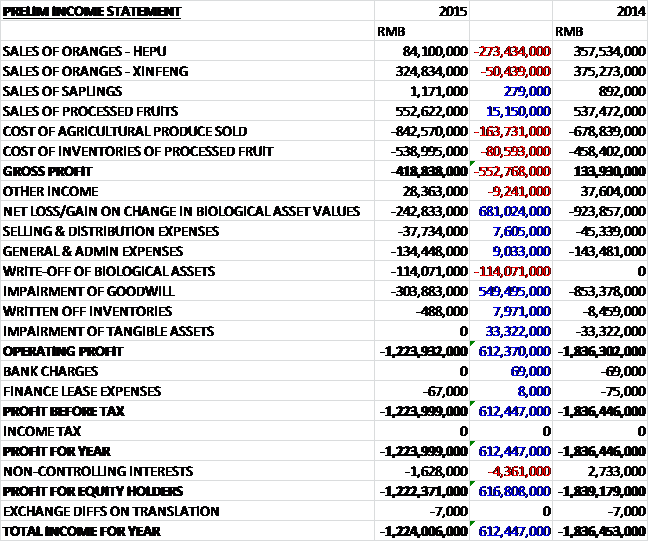

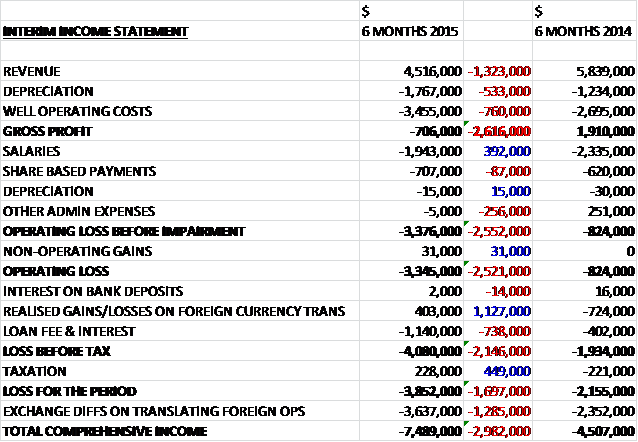

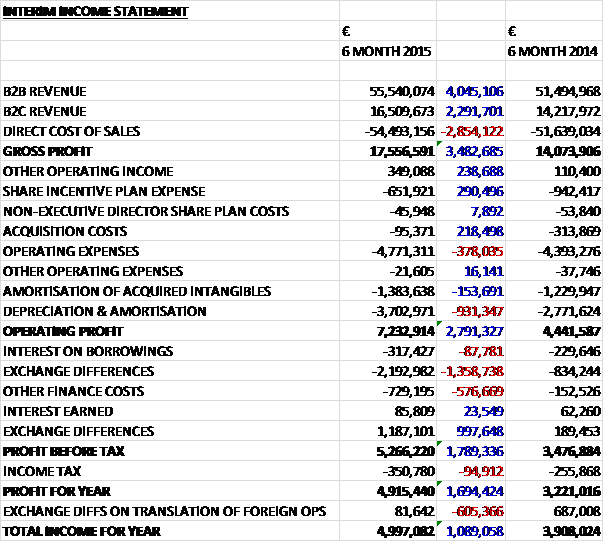

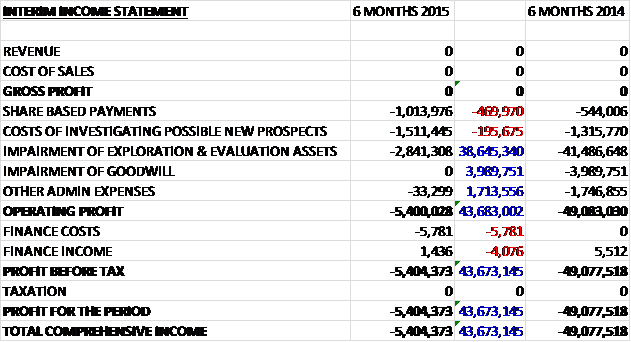

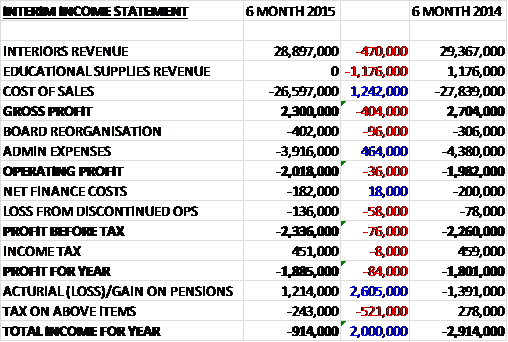

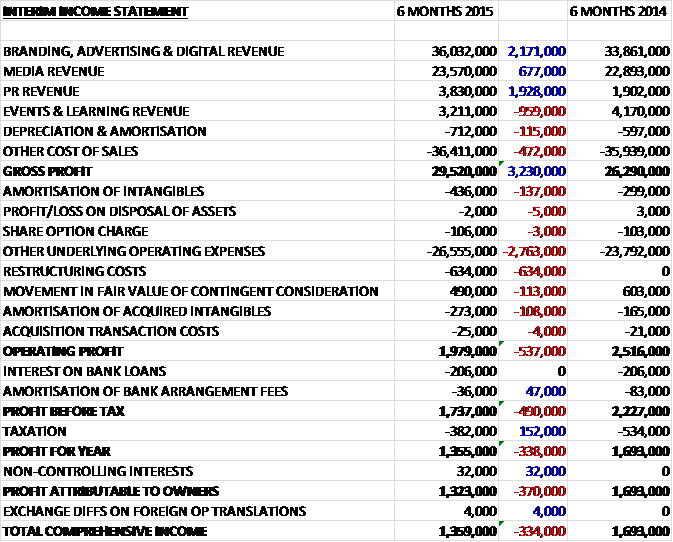

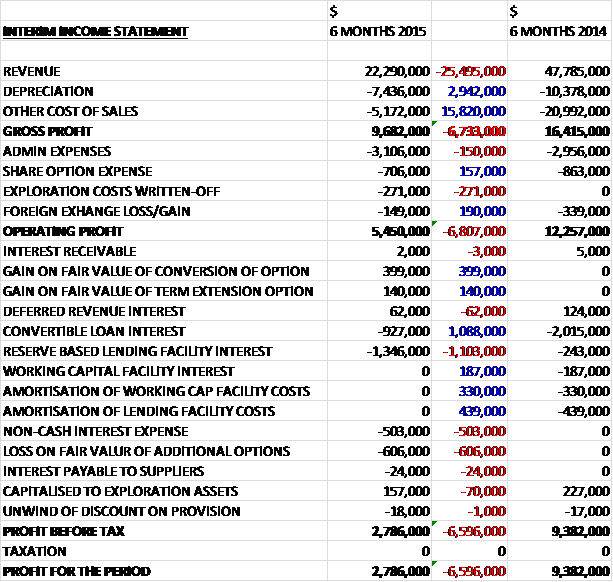

When compared to the first half of last year, total revenues more than halved to $22.3M which related to $15M of mostly oil sales in Egypt and $8.3M of gas sales in Morocco. This reflected the fall in oil prices and lower production volumes in Egypt. There was also a small reduction in Moroccan gas sales due to the end of one customer contract. Both depreciation and other cost of sales also fell so that gross profit fell by $6.7M to $9.7M. Admin expenses increased slightly, and there was $271K of exploration costs written off relating to the failed well in Oman, offset by a $157K decline in the share option expense and a $190K decline in foreign exchange losses so that operating profit declined by $6.8M to $5.5M. There were numerous finance income items and cost items with the largest being a $1.1M decline in convertible loan interest, offset by a $1.1M increase in reserve based lending facility interest. We also see a $503K non-cash interest expense (not sure what that could be) and a $606K loss on the fair value of additional options. The end result is a profit or the year of $2.8M, a decline of $6.6M year on year.

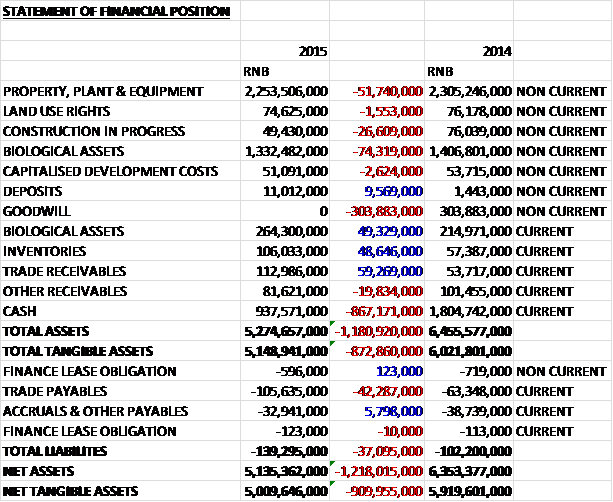

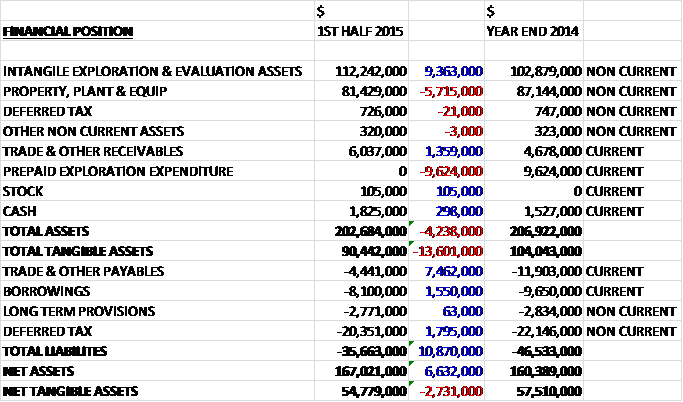

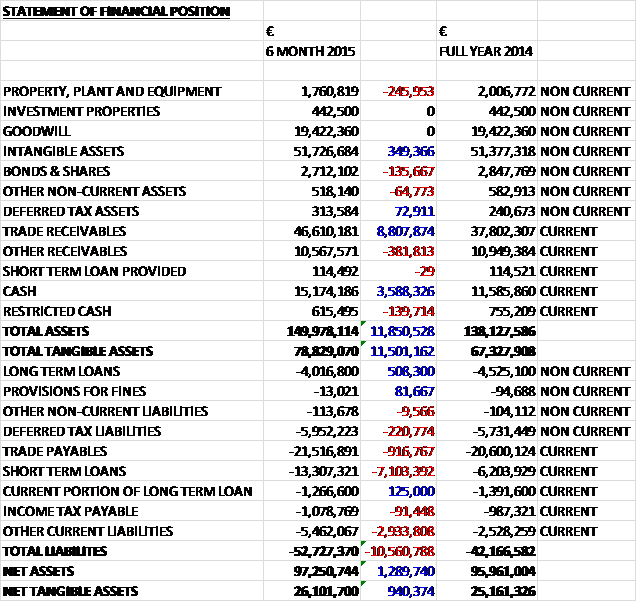

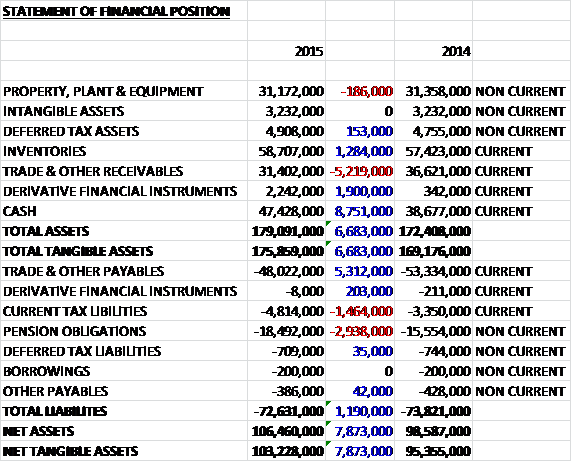

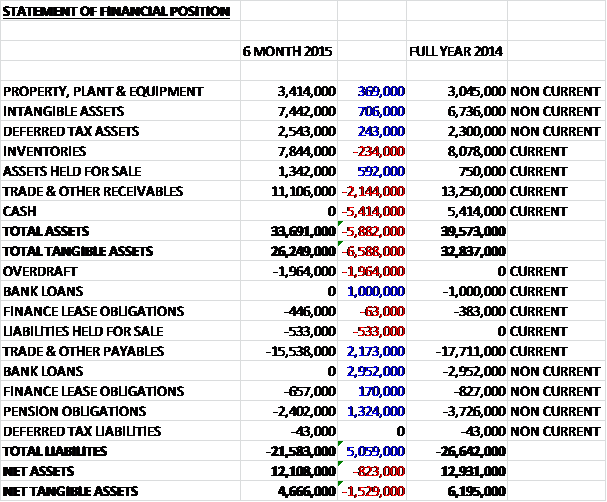

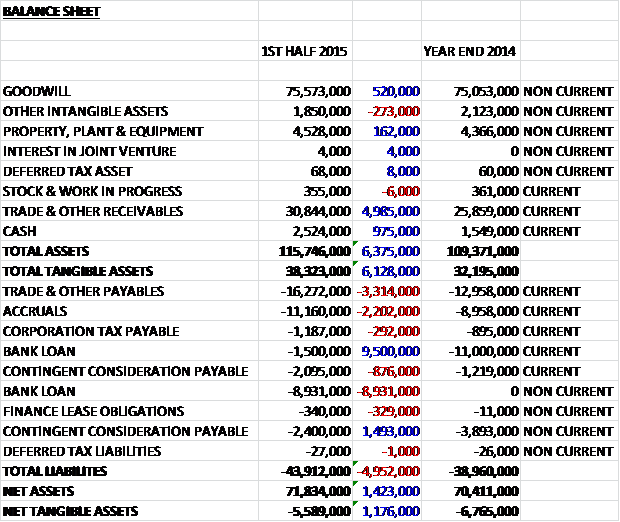

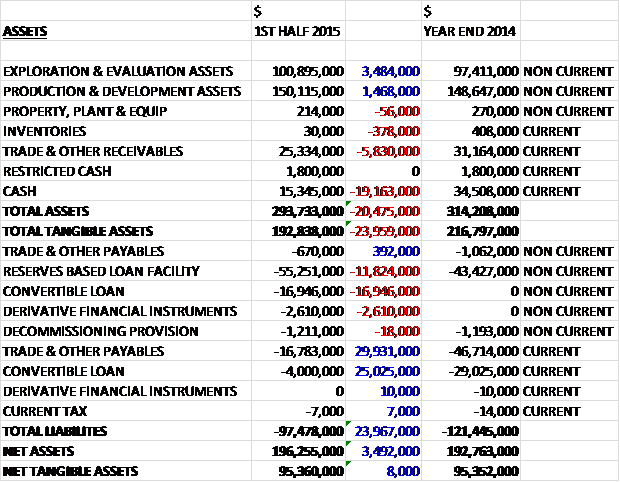

When compared to the end point of last year, total assets fell by $20.5M driven by a $19.2M decline in cash levels and a $5.8M decrease in receivables due to the lower oil price environment and the receipt of cash from EGPC with the receivable days now at levels not seen since before the Arab spring, partially offset by a $3.5M growth in exploration and evaluation assets and a $1.5M increase in production and development assets. Total liabilities also declined as a $30.3M fall in payables due to the payment of substantial obligations relating to the EMD-1 well in the Mahdia permit and the final well drilled in Oman, and an $8M decrease in the convertible loan were partially offset by an $11.8M growth in the reserves based loan facility and a $2.6M increase in derivative financial liabilities. The end result is a net tangible asset level of $95.4M which was unchanged over the period.

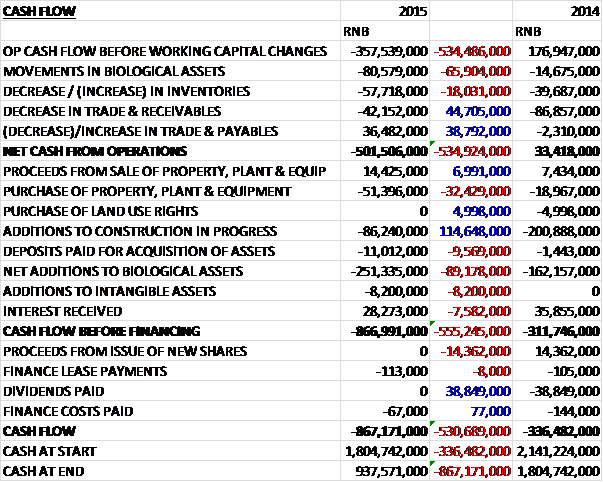

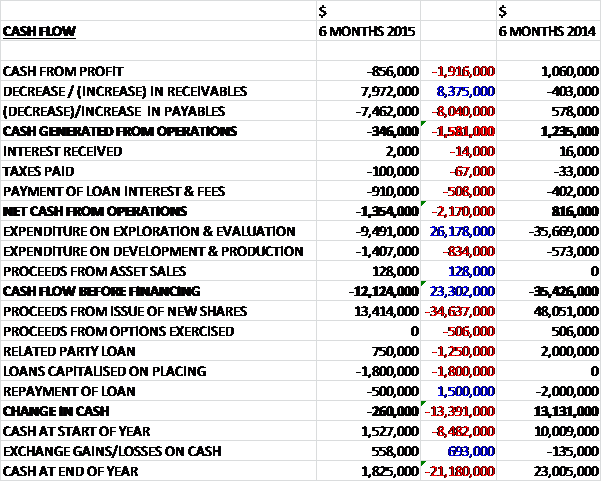

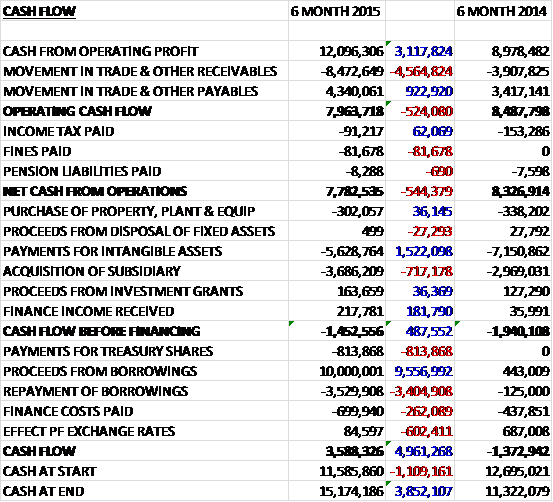

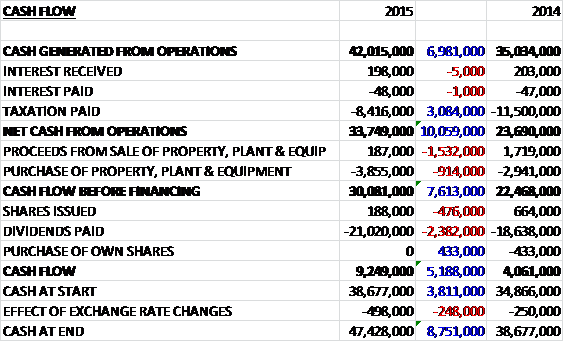

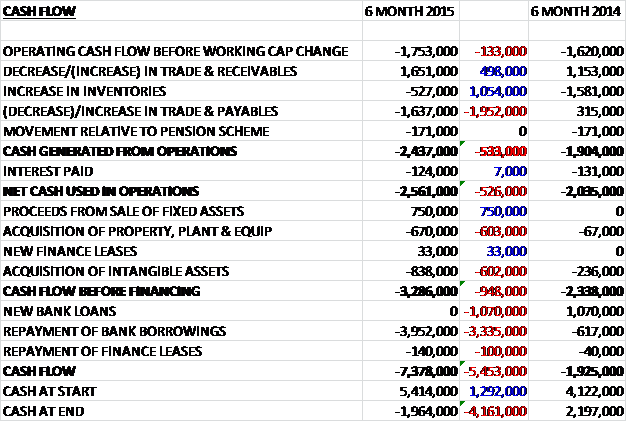

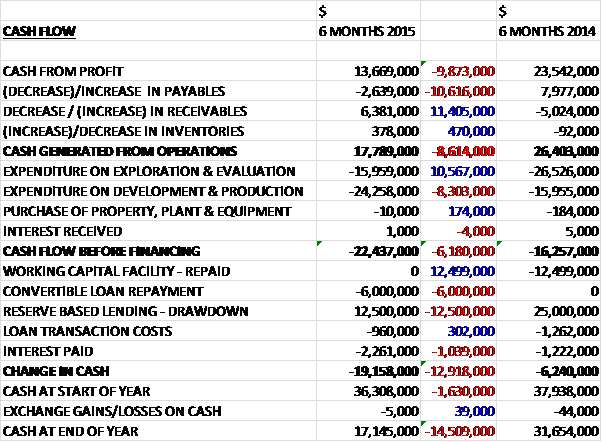

Before movements in working capital, cash profits fell by $9.9M to $13.7M. This was improved by a large fall in receivables so that the cash generated from operations was $17.8M, a decline of $8.6M. This cash did not cover the $24.3M spent on development and production, however and certainly not the $16M spent on exploration which meant that the cash outflow before financing was $22.4M. The group then repaid $6M of the convertible loan but drew down $12.5M of new reserve based lending and after the $2.3M interest payment the cash outflow for the period was $19.2M to give a cash level of $17.1M so at this rate of cash burn, it is not going last much longer.

In Morocco the group has made a number of efficiency improvements. Led by a newly appointed country manager, the focus has been on decreasing costs and improving overall operational and drilling efficiency. A number of local supply contracts have been re-negotiated and the supply chain restructured. As a result the group has reduced operating costs and reduced rig time which has resulted in a fall in well costs by over $1M per well. The group also continues to benefit from the use of its own pipeline which has additional capacity for a new gas supply. As a result of the existing infrastructure the threshold for commerciality for any new discoveries is relatively low and the group continues to look to add reserves both through its drilling programme and any other opportunities that might arise.

Sebou average daily gas production was 6.2MMcf per day during the first half of the year and negotiations are under way for further off-take to increase the supplies to and revenues from both existing customers and new industrial partners moving into the Kenitra region. Demand in the country remains buoyant and whilst the group has been somewhat shielded from falling commodity prices due to fixed gas price contract where the average realised price was $8.66 per Mcf during the period, there is potential for a further improvement on current pricing levels as new contracts are negotiated.

Drilling operations in the onshore Sebou and Lalla Mimouna blocks have continued through the period. In Sebou the notable success was the SAH-W1 well which encountered gas shows at different levels within the target Guebbas sands. The group will produce from the lowermost Guebbas zone where 3.6 metres of net pay was discovered and flowed at a sustained rate of 4.94MMcf/d on a 24/64” choke during a test period of five hours. This well was tied into existing production facilities in July. The KAB-1 bis exploration well, also in the Sebou permit, was drilled in February and encountered very limited gas shows, so it was plugged and abandoned. The KSR-12 discovery well, drilled on the Sebou permit towards the end of last year, has also been connected for production and was successfully brought on line in May with the well producing at rates of up to 2MMcf/d.

Results in Lalla Mimouna have been mixed, with the first well LAM-1 targeting Miocene gas bearing sands similar to the Sebou permit. LAM-1 was tested and the primary target flowed gas at a stabilised rate of 1.9MMcf/d on a 16/64” choke and the secondary target was perforated and flowed at a stabilised rate of 1.1MMcf/d. Post period, ANS-2 and NFA-1 well were drilled and although both encountered gas shows at the targeted depth, the interpretation of wire line logs indicated that the reservoir quality encountered in the wells did not meet the pre-drill estimates. The group is continuing to review the data gathered and in partnership with ONHYM will prioritise the next prospect to drill. Following the Lalla Mimouna wells the rig has now returned to the Sebou permit in the Rharb basin, the location of the existing production wells.

In Egypt the partners continue to carefully manage output with costs of $4.34 per bbl, amongst the lowest in the world. As a result, even in the current oil price environment, the field remains profitable and cash generative. At the end of June, 14 wells in the Al Amir SE field and five wells in the Geyad field were on production, with a combined average gross production rate of 9,648 boepd for the period. Water injection through four wells in AASE and one well in the Geyad field is providing continuing pressure support to maximise recovery efficiency and optimise production levels.

The export gas line to the SUCO facility at Zeit Bay is currently flowing at approximately 7MMcf/d with a total delivered to the terminal of 8.8Bcf at the end of June. Condensate and natural gas liquids are tripped out of the gas and sold to EGPC with gross average daily rates of about 65bbls of condensate and 15 tonnes of LPG. The group is in the final stages of documenting the commercial agreements, but has historically accrued for its share of the gas and condensate revenues from the field.

The AASE-21 well was shut in during April due to a high water cut. The AASE-18 well was recompleted and brought online during May at an initial rate of 650 bopd which will help during the remainder of the year to partially compensate for the loss of AASE-21. Given the group’s material ownership stake in the block, they have taken a much more active role with the operator. The process of good field management will be continued into 2016 through implementation of the dynamic reservoir model of the AASE field.

The group continued to benefit from the historic capex spend on the fields and is working closely with the operator to prudently manage the field and arrest the decline in production through workover and drilling activity. During the second half of the year a programme to perform workovers on up to eight wells commenced. The results of this workover programme will be used to influence the design of the next planned drilling programme of two or three production wells.

In Tunisia, during the first half of the year the group continued to work with the Consultative Committee on Hydrocarbons and after the end of the period, they announced the renewal of the Mahdia permit. It has been extended for three years until January 2018. The extension carried with it a commitment of one exploration well, one appraisal well, and a requirement to acquire 300 square km of 3D seismic. The group currently has a 100% interest in the permit and is now looking for a farm in partner with the process now being commenced.

The offshore Mahdia permit covers an area of 3,024 km2 and contains the El Mediouni structure which was retested by the EMD-1 well in August 2014 and is a potentially large discovery. The well encountered a 133 metre column of light oil in the Ketatna carbonates. While mud losses prevented log data acquisition, the group estimates an un-risked prospective recoverable resource in excess of 70MMbo from the structure. It is located in a water depth of about 230 metres in benign Mediterranean conditions and the permit also contains a number of similar prospects which have been de-risked by the EMD-1 well.

At Ras Marmour and Beni Khalled, the group continues to evaluate its commitments in the current commodity price environment. They await final confirmation of all approvals to drill the onshore Ras Marmour well which is targeting a productive sand in the early Cretaceous Meloussi formation, which is the proven reservoir in the adjacent Robbana field. At Beni Khalled, tenders are currently being reviewed in respect of the 3D seismic with a view to future appraisal of the existing discovery.

In Oman the onshore exploration well, Shisr-1, drilled in Q1 2015 in the SW area of Block 49, was plugged and abandoned due to drilling difficulties. In light of this and coupled with the insufficient interest in the farm-in on Block 52, the group relinquished both blocks and is no longer bidding for new acreage in the country as they are exiting Oman.

During the period the group extended the convertible loan agreement with KGL Petroleum. Of the $30M loan value, $10M has been repaid – $6M during the period and $4M in July. The repayment of the remaining $20M was extended to July 2017. Also, the group drew down $12.5M of the IFC reserve based lending facility amounting to total draw-downs of $57.5M, which is a lot of debt for a company of this size in this oil price environment. Net debt stood at $64.4M compared to $23.3M at the same point last year. By August the net debt had increased further to $65.7M.

In Morocco there are a number of ongoing claims against the group. These include claims by ex-employees and claims by ex-suppliers associated with the previous country managers. The group does not believe that these claims are material or likely to succeed.

The group had estimated capital commitments amounting to $21M which are payable over the next two years. Expenditure on production and development assets is estimated to be $8.7M while expenditure on exploration and evaluation assets is estimated to be $12.3M in North Africa. This is going to be tight and the group has said they are exploring potential funding options, presumably including a potential placing.

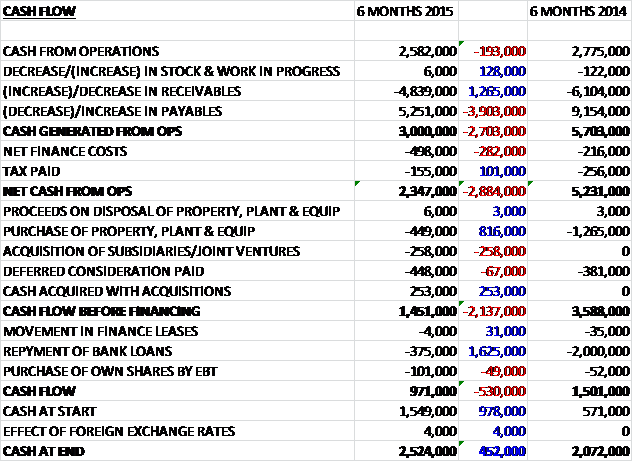

Overall then, much like many small oil and gas producers, this has been a very difficult period for the group but it has to be said that the results are probably not as bad as I was expecting. As would be expected, profits fell but the fact the group is still profitable is certainly a bonus. Net tangible assets were flat which again, is fairly good going but the real problem becomes apparent when we look at the cash flow report. Operating cash flow fell and it was not close to covering the capex of the group.

In Morocco, costs have come down and demands remain buoyant. At $8.66 per McF, the price achieved has been somewhat sheltered from the declining oil price but exploration activity has been mixed with two wells being added to production. The Egyptian acreage has very low costs, at $4.34/bbl and remain profitable even in this environment. The problem is the that this field is old and production is declining with one new well not covering the shut in AASE-21 well. There will need to be some spending in Tunisia to cover commitments there but any farm in achieved may be a catalyst for short term share price gains but with a huge amount of debt, cash levels of just $21M and some $17.1M of capital expenditure inked in over the next two years, the group really could do with an improvement in the oil price!

This chart does not look good and seems to roughly follow the oil price.

On the 13th October the group released an update covering the Ksiri West-A exploration well on the Sebou permit in Morocco. The well reached a TD of 1,890 metres and prospective gas shows were logged, and a completion string installed in preparation for well testing and then connection to existing production facilities. The primary main Hoot target interval was perforated from 1,818 metres to 1,826.7 metres and flowed gas at a maximum rate of 8MMScf per day on a 24/64” choke. The well will be tied back to the pipeline from Sebou to Kenitra ready for production. IT is about 680m west of KSR-11 and 1,120 metres west of the Ksiri sub-station.

The rig has now relocated to drill the Caid El Gaddari-13 (CGD-13) well, the final well in the current drilling campaign. The location lies within the Gaddari Sud exploitation concession near the SW margin of the Sebou permit. This well has a primary target of just 780 metres which consists of gas-bearing Miocene sandstones in a structurally elevated position east of the CGD-1 well and west of the CGD-9 well.

The flow rate achieved on this well is in the upper end of the range of expectations – it is nice to see some good news coming out of the company for once!

On the 28th October the group announced a discovery at the Caid El Gaddari-13 (CGD-13) exploration well on the Sebou permit. The well spudded on 8th October and reached a TD of 871m on the 17th, significantly ahead of schedule. The target consisted of gas-bearing Miocene sandstones in a structurally elevated position east of the CGD-1 well and west of the CGD-9 well. The well has encountered about 5.9m of net pay and an interval of 4.7m was perforated between 791 and 812m. Testing has been completed and the well has flowed at a rate of 4.45MMscf/d through a 28/64” choke. The well is located 320m northwest of the closest tie-in point on the 75% owned pipeline to Kenitra. The well will be brought into production and produced through the pipeline to customers in the city.

This discovery concludes the drilling campaign in Morocco. Ten wells have been drilled in total, seven in Sebou and three in Lalla Mimouna with six recorded discoveries (five at Sebou and one at Lalla Mimouna). Improving operational efficiency has been a key goal for the group and drilling costs have fallen 30% per well during the course of the campaign, as the oil price has fallen. The geological team will review and integrate the well data from the campaign when planning the next one in Morocco, initially scheduled for late 2016.

It is good to end on a high, and this well does seem to be fairly promising. For me, there is just too much debt to take the plunge, however.

On the 14th December the group released an update. There has been slower progress than expected on the negotiations with the IFC to extend the reserve based lending agreement by one year to June 2019. Trading remains very challenging due to a further weakening of global oil prices, varying production levels in NW Gemsa and the impact of macro events on payments from EGPC. Following a reduction in the value of the company’s assets, they expect the borrowing base to be reduced and as a result there will be a moderate shortfall. The group is therefore considering a number of options including an equity raise to improve the balance sheet.

For what it’s worth, in Morocco they are reviewing the well data from the recent drilling campaign and the final two successful wells have been tied back to the existing production infrastructure and started production earlier in the month. It is the intention to re-start drilling in Morocco in Q4 2016.

In Egypt, the company, its partners and the government signed a processing and treatment agreements which sets out the framework under which the participants in the NW Gemsa field will be paid for gas sales since February 2013. As at June this year, the group’s receivables stood at $25.3M, of which about $2M was attributed to gas sales. Operationally the workover campaign aimed at managing the field as it matures is nearing completion and has informed the design of the next drilling programme which started this month with the spudding of the AASE-23 well which will be first of two new producing wells with the objective of increasing production levels.

In Tunisia, the farm-out process for the Mahdia permit is ongoing with the company engaged in discussions with a number of companies despite the market for farm downs being impacted by the overall decline in the sector.

In conclusion then, the pertinent point of this update is that the debt is too high and it is very likely the company will have to undergo an equity placing to repair the balance sheet – this has been on the cards for a long time but I suppose the most recent plunge in the price of oil as brought the situation to a head.

On the 8th February the group released an operational and financial update. They have signed a memorandum of understanding with SBS Porcher, a potential new gas customer in Morocco. As part of the arrangement, a new pipeline extension would be constructed linking the existing pipeline in the northern Kenitra region to the Porcher factory in the central Kenitra area. The key terms are that Porcher will pay for and own the pipeline extension with construction estimated to start in May with first gas expected to flow in Q4 of this year; the estimated gross offtake volume would be 0.35mmcf per day with a price equivalent to $12/mcf which represents a 6% increase in production volumes compared to 2015; and the gas price would be fixed for the duration of the five year contract. All parties are expected to sign binding documentation in the coming months and when signed this will represent a gas price some 40% higher than the average price currently and will enable the group to access a potential new customer base in central Kenitra.

In Egypt the infill drilling campaign on the NW Gemsa field is continuing. The first of two production wells, AASE-23 has been drilled, completed and tied in to the production infrastructure and a couple of days ago, a well test showed the well flowed at a gross average rate of 4,081bbls per day and 2.715mmscf through a 48/64” choke. The well will be produced at a lower rate, however, in order to manage the long term field production. The second production well, AASE-24, was spudded on the 8th Feb. In Tunisia the farm out process for the Mahdia permit is continuing and apparently the company remains engaged in discussions with a number of interested parties.

The company remains in discussions with the IFC regarding its debt but given the further fall and continued volatility in oil price, discussions are unresolved and both parties are “working together to find a solution to right-size the balance sheet”. In Egypt, the dollar receipts from EGPC remain limited and unpredictable which means that the company’s cash flow and financial position remain under significant pressure.

This new contract in Morocco does sound promising but this is completely over shadowed by the fact that the company doesn’t seem to be able to get any payment in Egypt and it sounds like the IFC is going to end up owning much of the equity here and I really don’t understand why the share price has leapt in recent days. I am definitely staying out until the financial situation is sorted out.

On the 15th March the group released an operating and financial update. Discussions with the IFC have resulted in an agreement to suspend the December redetermination until 15th April with any repayments being postponed until that date. The lenders have indicated their willingness to consider further waivers as may be required in order to complete the strategic review.

The company’s cash flows and financial position remain under significant pressure, primarily due to the uncertainty and irregularity of receipts from EGPC. At the year-end, they had cash of $10M and receivables of $21.6M. Inclusive of the $20M convertible loan held by KGL, the total debt position is $77.5M and there is a further $14.1M of trade payables. Further, the company is reliant on extracting US dollars from its Moroccan operations to both satisfy its obligations to its creditors and to fund operations.

In addition, the most recently disclosed 2P reserves of 16.23mmboe are expected to have reduced due to the production of hydrocarbons and the lower oil price environment. The scope of the options being considered under the strategic review include the sale of one or more of the company’s assets, a corporate transaction such as a merger with a third party, the sale of the entire share capital of the company, and the raising of capital in the form of new share placings.

In Egypt, at the year-end, 11 wells in the Al Amir SE field (ASSE) and three wells in the Geyad field were on production, with a combined average gross production rate of 8,871 boe per day for the year. Water injection through three wells in field is providing continuing pressure support to maximise recovery efficiency and optimise production levels. The AASE-23 well was first brought on stream in February 2016 and is now being produced at around 800boe per day. Drilling continues at the ASSE-24 well which was spudded in early February.

In Morocco, the focus has been on decreasing costs and improving overall operational efficiency. Sales from Sebou for 2015 averaged 4.39mmcf per day, net to the company, utilising less than half of the pipeline capacity. Prices held up well with the average price realised during 2015 being over $8.50 per Mcf.

Overall then, there is a stay of execution but the problem remains the huge amount of debt the company has accrued. I can’t imagine this depressed environment is the best time to try and sell any of the assets so, unless the whole company can be sold at a decent price, this is not looking good for current shareholders in my view.

On the 15th April the group announced that the IFC has agreed to extend the suspension of the December redetermination and any repayments due under its reserve based lending facility until 13th May. They have also indicated their willingness to consider further waivers as may be required to continue the strategic review process. This is good news but the shares are far too risky until the review process is over.

On the 29th April the group released a reserves and resources update and to reflect the downward revisions due to the current low oil price environment, they expect to recognise an impairment charge in the 2015 results.

In Egypt, the net 2P reserves for the NW Gemsa field are 6.671MMboe compared to 12.49MMboe at the end of 2014, although 1.626MMboe has been re-categorised as P50 unrisked contingent resources and there was net field production of 1.295MMboe. In Morocco, there net reserves for the Sebou permit are 0.98MMboe compared to 3.74MMbie at the end of 2014. In addition, unrisked contingent resources are a further 1.183MMboe and the net field production was 0.276MMboe during the year.

This is certainly not good for the company – there is only about six years of production left at these levels.

On the 13th May the group announced that the IFC had agreed to extend the suspension of the debt repayment until 27th May. The group expects to receive an improved payment from EGPC for May compared to the previous months but their cash flows and financial position remain under significant pressure and a sustained improvement in payments from EGPC is required – this does not sound good.

On the 17th May the group announced that the infill drilling campaign on the NW Gemsa field has been completed. The second of the two production wells, AASE-24, has been drilled to TD, completed and tied in to the production infrastructure. A well test commenced and the well flowed at a gross average rate of 1,714bbls per day and 3.062mmscf per day of gas through a 40/64” choke. The well will be produced at a lower rate in order to best manage the long term field production.

These results will help maintain production rates and mange field production. There is no further drilling planned in 2016 although there is an ongoing workover campaign which is also expected to help maintain production levels. This all sounds fine but the operational side of this company is now a side show and the important issues are the debt repayments and receivables from EGPC.

On the 20th May the announcement came that shouldn’t have come as much of a surprise. After taking into account the company’s $77.5M outstanding debt position and based on the indicative proposals received to date, it is likely that there will be little or no value attributed to equity holders. This sounds like a total wipeout to me.

On the 27th May the group announced that the IFC had agreed to extend the suspension of the repayments due under its reserve based lending facility until 24th June. They have also considered further waivers as may be required. This is obviously good news but doesn’t change anything – there is still likely to be no value left for shareholders here.

On the 24th June he group announced that the IFC had agreed to extend the suspension of their repayments until 22nd July. The payments from EGPC have continued to be unpredictable and to date there has not been a sustained improvement.