Serabi Gold is engaged in the evaluation and development of gold projects in Brazil. This year saw the start-up of the Palito gold mine and the start of development of its neighbouring high grade Sao Chico gold project. The projects are located in the Tapajos region in Northern Brazil which has seen alluvial and small scale surface mining operations in the past. The Palito mine has a measured and indicated resource of 206,466 ounces of gold at a grade of over 7.5g/t with inferred mineral resources of 392,817 ounces of gold. Palito is a small-scale operation using selective mining techniques with an initial production target of around 24,000 ounces per annum. The Sao Chico deposit was acquired in 2013 and is being developed as a satellite deposit to supply supplemental high grade gold ore to the Palito processing plant. Average resource grades at Sao Chico are in excess of 25g/t and whist the current resource is small (inferred resources of just 71,385 ounces of gold), management is confident it will be expanded. In addition to these two mines, the company holds exploration licenses over the surrounding 41,000 hectares and is seeking additional exploration holdings in the Tapajos region.

All revenue is derived from the sale of copper and gold concentrates along with gold bullion produced by the Palito mine. It is expected that all future production derived from the Sao Chico mine will be in the form of gold bullion. The concentrate is mined in Brazil and then routed through the UK and shipped to Hamburg. There are only two customers, one publicly quoted major copper smelter in Europe that takes the concentrate and the other that takes the bullion.

The plan for the Palito mine is to operate at levels of about 90,000 tonnes per annum and during 2015 running down stockpiles of coarse ore and floatation tailings. The plan for Sao Chico is to be in development for 2015 with limited production being generated from stoping and only in 2016 to reach full mine production rates. The annual LOM gold production is expected to be 42,000 ounces over a period of eight years. Every $100 change in the price of gold would affect value in use by $20.7M.

The shares are listed on AIM and the Toronto stock exchange and the company is 52% owned by Fratelli Investments. Serabi Gold has now released its final results for the year ended 2014.

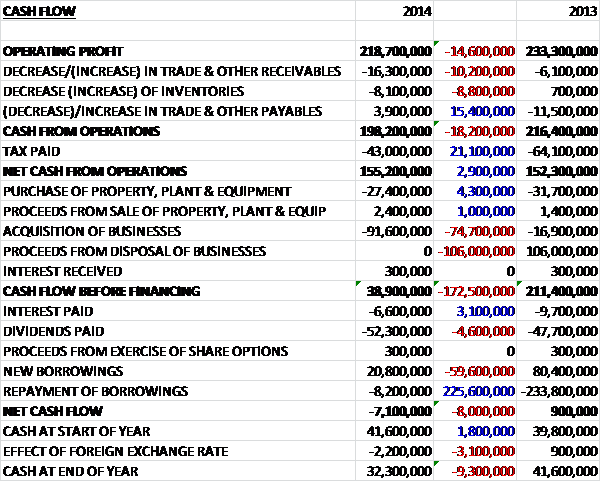

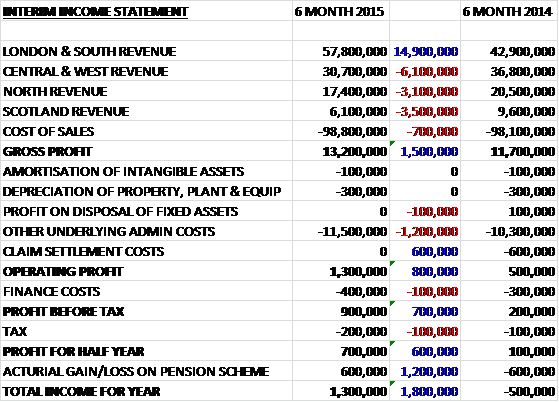

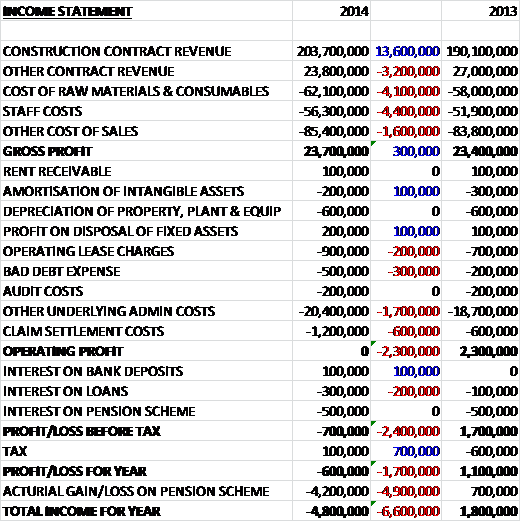

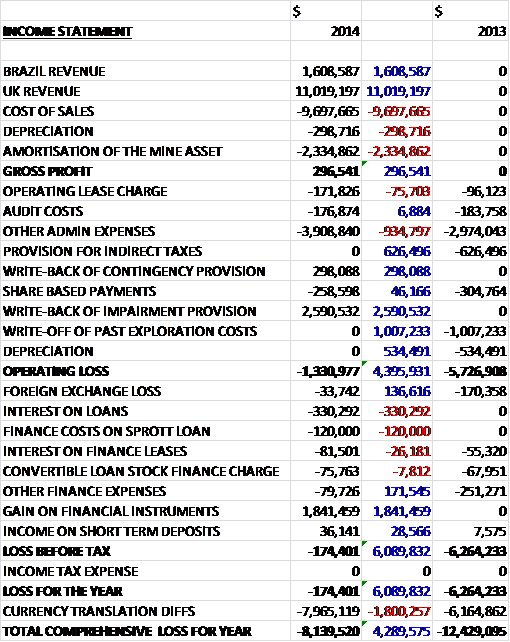

This is the first year that the group has achieved revenues and it recorded £1.6M of revenue from Brazil (relating to the gold bullion) and $11M from the UK relating to the concentrate. Cost of sales were $9.7M and after a $2.3M amortisation of the mine asset as it is now a producing mine, the maiden gross profit stood at $297K. Operating lease charges increased slightly and other admin costs were up $935K but there were various non-underlying benefits when compared to last year. There was no $626K provision for indirect taxes or a $1M write-off of past exploration costs that occurred last year relating to the Pizon project that is no longer considered a priority for the group. There was also $298K write-back of a contingency provision relating to potential labour settlements that were not required, and a $2.6M write-back of an impairment provision. All this meant that the operating loss stood at $1.3M, a decline of $4.4M year on year. With regards to finance items, there was a $330K interest on loans and a $120K finance cost related to the Sprott loan but this was more than offset by a $1.9M gain on financial instruments (partly relating to the reduction in the value of the warrants issued and the decline in value of the Sprott call option over some gold). The end result is a $174K loss for the year, an improvement of $6.1M when compared to last year but it should be noted that there was an $8M loss relating to foreign currency translation.

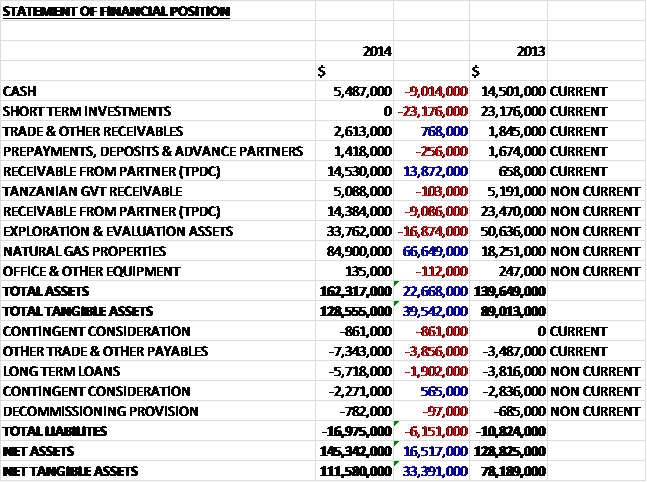

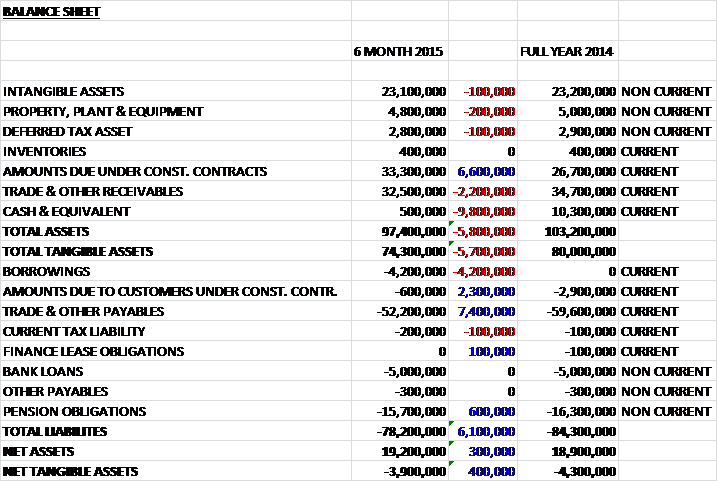

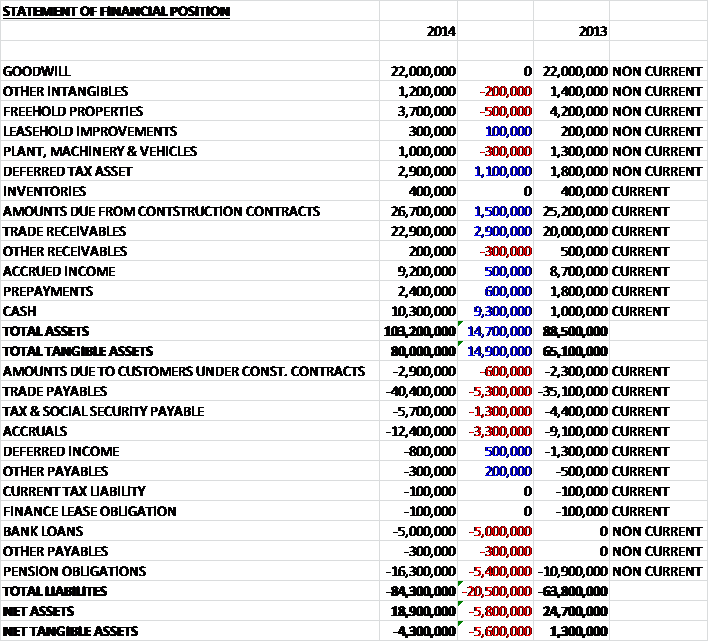

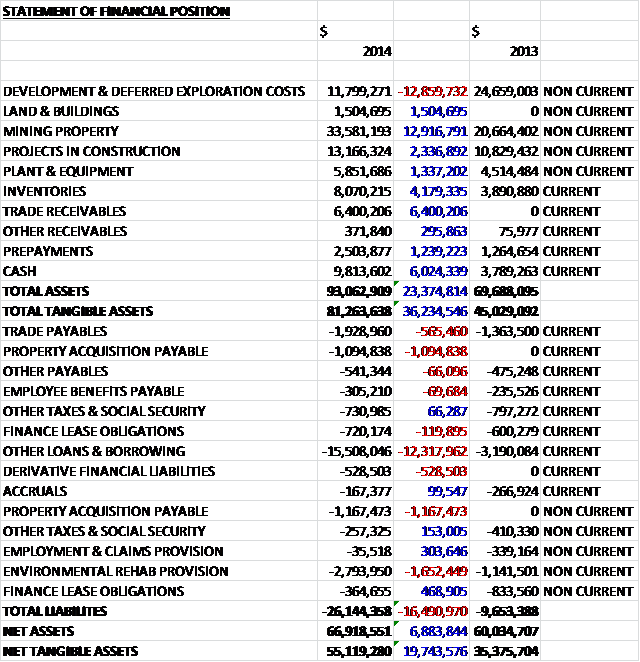

When compared to the end point of last year, total assets increased by $23.4M driven by a $12.9M increase in the value of mining properties, a $6.4M growth in trade receivables, a $6M increase in cash and a $4.2M growth in the value of inventories partially offset by a $12.9M fall in development and deferred exploration costs as a proportion of these costs were transferred to fixed assets as the mines move towards commercial production. Total liabilities also increased due to a $12.3M increase in loans and borrowings, a $1.7M growth in the environmental rehabilitation provision, and a $2.3M increase in the property acquisition payable. The end result is a $19.7M increase in net tangible assets at $55.1M.

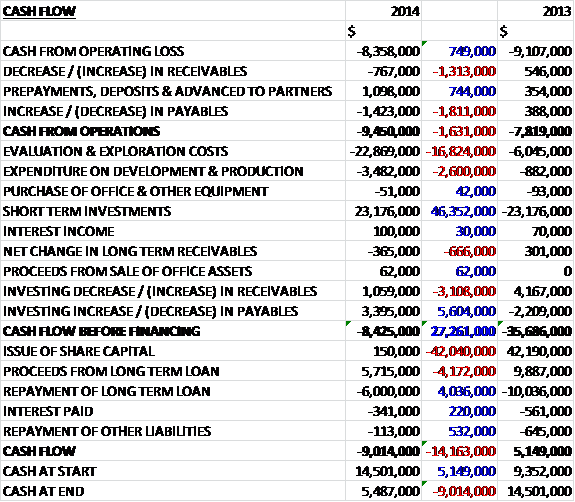

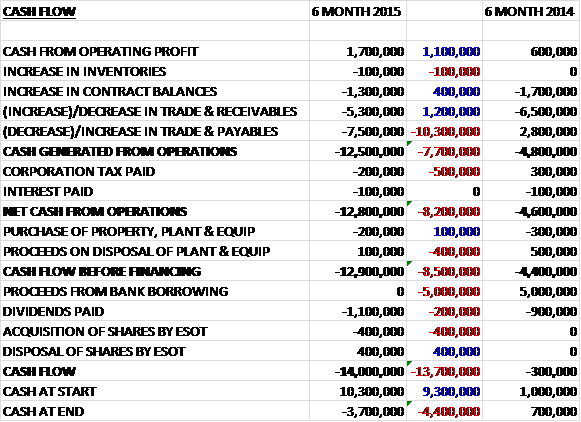

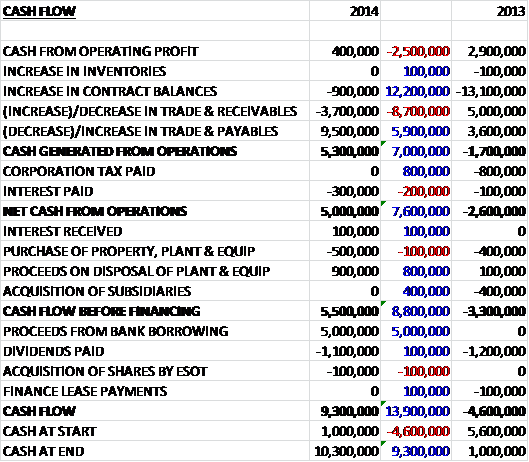

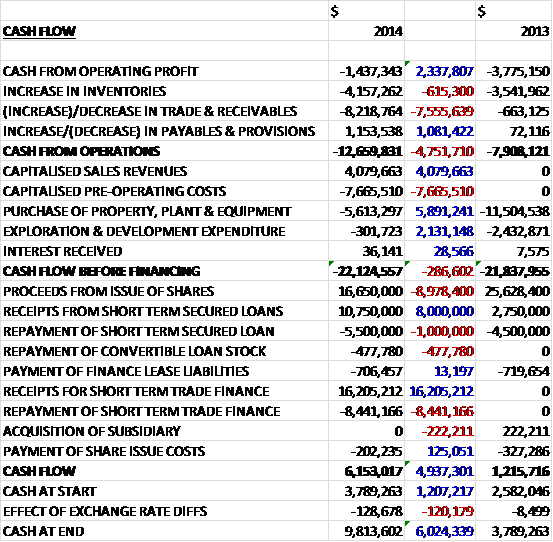

Before movements in working capital, cash losses fell by $2.3M to $1.4M. A huge movement in receivables and a fairly large increase in inventories, however, meant that the operation cash outflow stood at $12.7M, an increase of £4.8M year on year. After operating costs and the purchase of property, plant and equipment, the cash outflow before financing was $22.1M. The group then made $16.7M from new share issues, a net $5.3M from new short term secured loans and a net £7.8M from short term trade finance to give a cash inflow of $6.2M and a cash level of $9.8M at the end of the year.

The company expects to start processing ore from the Sao Chico gold project in Q2 2015 and expects to produce 35,000 ounces of gold in 2015 at an all-in sustaining cost of between $900 and $950 per ounce from both mines together, a 90% increase on the 2014 output with a further increase in 2016 once Sao Chico is in full production. The Palito mine has now reached a relatively steady state of operations and is expected to generate some 90,000 tonnes of ore at around 8.5g/t next year. The gold production from this mined ore will be supplemented by the reprocessing of stockpiled tailings accumulated during the first three quarters of 2014 and by running down surface stockpiles of ore that have been established over the last year of operations.

With much of the capital requirements for Sao Chico being incurred in the first half of 2015, the group are expecting to be producing positive cash flow which will allow them to retire their current (very expensive) debt arrangements and start to look for new growth opportunities both organically and potentially through acquisition.

At Palito, by the end of 2013 the company had established a run of mine stockpile of ore of approximately 25,000 tonnes with an average gold grade of over 8 grams per tonne. Initial commissioning of the gold process plant commenced In December 2013. For the first quarter of 2014, the operation was in a planned ramp-up phase and during the second quarter the company continued to build upon the start-up targeting a long term plant throughput rate of 7,500 tonnes per month with commercial production starting in July. Underground development mining has continued with more than 6,200 metres of horizontal development completed at the end of the year. Production activity is now in eight mining areas, three sectors in the Palito West area and five sectors in the Palito Main Zone.

Mining operations during Q4 were slightly below plan as a result of reduced equipment availability during December with 25,308 tonnes being mined at an average grade of 9.28g/t. For the year as a whole, total mined tonnage was ahead of planned levels, however, with an aggregate of 76,500 tonnes at an average grade of 9.95g/t. As a result of the higher rates of mine production the surface stockpiles of ore have not been depleted as much as was expected and the surface stockpile of coarse ore totalled about 11,000 tonnes at the year-end. The average gold price achieved during the year was $1,230 per ounce against an all-in sustaining cost of $1,034 per ounce (expected to fall to between $900 and $950 next year).

In the plant, processing rates throughout the year have continued to improve having averaged about 9,600 tonnes per month during Q4 after recording 4,700 in Q1, 6,200 in Q2 and 8,000 in Q3. Gold production in the fourth quarter was 7,819 ounces, an increase of 42% over the previous quarter as the company began to use higher grade ore. The majority of gold production from the mine is in the form of copper/gold concentrate which is then shipped to smelters in Europe for further processing. During Q4, 493 tonnes of concentrate was produced and a total of 1,467 tonnes was produced in the year as a whole.

The commissioning of the CIP plant was completed shortly before the end of Q3, a delay of about a month compared with previous expectations. The first batch of gold loaded carbon was withdrawn from the circuit during October and the first elution and gold pour was completed at the end of the month. The introduction of the CIP plant will allow the operation to increase gold recoveries and the company expects that over the life of the mine, gold recoveries in excess of 90% will be achieved. A second ball-mill acquired in March became operational during the second half of July following a period of remediation. It was purchased in anticipation of establishing a second process line for ore from the Sao Chico operation but in the near term it is providing additional milling capacity to process some of the stockpiled material and maximise short term production.

The mining fleet at Palito is relatively new and comprises three 20 tonne trucks, three underground drill rigs and four underground loaders. A fourth 20 tonne truck is deployed at Sao Chico on the preparatory works involved in the development of this deposit. The company owns various other items of mobile equipment, including three front end loaders, a bulldozer and other smaller vehicles. Whilst additional equipment purchases are planned during 2015 these will primarily be dedicated to Sao Chico and the company will transfer equipment between the two locations to supplement capacity as required.

At Sao Chico, work commenced during February on the preparatory earthworks required to expose the bedrock and establish the mine portal. It was initially thought that these works would take three months to complete but the rainy season continued longer than expected and as the ground became saturated, excavation conditions became difficult that meant it was not until Q3 that it was completed. Additional drainage and water run off areas have been constructed to ensure the stability of the cut-back and protect the roadway that is the access point to the mine. These features should ensure that a similar period and level of prolonged rainfall will not affect movement around and access to the mine.

By the end of September the first excavations to establish the mine portal were completed and Q4 saw the underground development commence with 95 metres completed before the year-end and a further 160 metres completed by the end of February 2015. Five veins were intersected in the cutback and a further three in the ramp and at the intersections all appear to be of mineable widths and grades. All eight of these previously unknown structures lie outside the current geological resource. In January 2015 the ramp development intersected the principle Main Vein which exhibited visible sulphides. The main vein ore body, which is the principle structure within the resource, has now been fully exposed by a four metre high and wide gallery that has crossed the main vein perpendicular to its strike. Sampling confirmed that the intersection had an average width of 3.6 metres with a gold grade of 42g/t. Elsewhere the zone continues to exhibit similar widths to the original intersection and grades in excess of 15g/t.

The company plans to undertake over 750 metres of ramp development and 2,700 metres of ore development at Sao Chico during the course of 2015, following the main vein as its strike extends to the East and West. With all the mining and fixed fleet required for the 2015 mine plan in place along with the initial workforce, the company expects to see continued progress at the mine. Ore transportation to Palito began in February and processing of Sao Chico ore is forecast to start in Q2 2015.

In March 2015 the company started a 5,000 metre drilling campaign which will be a combination of in-fill and step-out drilling, and the results from this will help the understanding of the ore body and facilitate the mine planning for 2016 as well as the preparation of a new resource estimation for the project. In November, the DNPM approved the final exploration report for Sao Chico which is the first process in transforming the exploration license into a mining licence. Work is now underway on the preparation of the Plano de Approveimento Economico which is the next major requirement in the conversion process. With the trial mining license already in place, however, all mining operations can continue in parallel.

As far as the other prospects are concerned, the underground development of Palito is being driven towards the Palito South area but the company has no plans during 2015 to undertake further exploration on either this or the Currutela and Piaui prospects or undertake further investigation of other anomalies. Once adequate cash flow is being generated from production operations, they intend to use some of this cash to advance these opportunities which are all relatively close to Palito.

The current gold market seems to be rather difficult. Overall supply levels have remained the same year on year as a 5% increase from mines was offset by a lower rate of recycling as a result of lower gold prices. Mine supply is expected to plateau in 2015 as mining companies cut back on capital expenditure. Consumer demand continued to be led by China and India and consumption for the jewellery market was steady throughout the year, albeit at a small reduction to 2013 levels. The strengthening of the US economy, the potential for US interest rate growth and the strengthening of the US dollar have reduced the appetite for safe haven investments but continued geopolitical events surrounding Ukraine and the Middle East can be expected to continue to have a positive effect on some demand in the near future.

There are clearly a number or risks going forward, the main one being a continued fall in gold prices which would not only reduce cash flow but also the life of the mines as some of the gold becomes uneconomic to extract – this would mean some potential impairments against some of the assets. Other risks include the fact that the exploration license for Sao Chico expired in march and whilst there is an interim license in place, there is no guarantee that a mining license will be granted. Also, the government of Brazil has been seeking to introduce a new mining code for some time and the matter continues to be an area of debate. Any new legislation could result in all current applications being cancelled and require applicants to make new ones under the terms of any new codes. The government in Brazil is losing support in general and the country is struggling economically which means the government may seek to increase taxes and royalties on the mining sector to increase state income.

The company seems to have rather a complicated share structure. There are ordinary shares of 0.5p each, deferred shares of 4.5p and deferred shares of 9.5p. The deferred shares carry no voting or dividend rights or any rights to participate in the profits or assets of the company and all the deferred shares may be purchased by the company at any time for no consideration. In the event of a return of capital, after the holders of the ordinary shares have received the aggregate amount paid up thereon plus £100 per ordinary share, they are then eligible to receive payment. I have to say I don’t really understand what this is all about and why anyone would want a deferred share.

On the 3rd March the group completed a share placing raising £10M which provided additional working capital during the start-up phase of production at Palito and also to fund the initial development and further evaluation of the Sao Chico project. The placing involved the issue of 200,000,000 units at a subscription price of 5p whereby each unit comprises one new ordinary share and one half of one new warrant. Each warrant entitles the holder to subscribe to one new ordinary share at a price of 6p before March 2016.

In September they entered into an $8M secured loan facility for the period to the end of 2015 with the Sprott Resource Lending Partnership providing additional working and development capital which carries a massive 10% interest rate per annum. The first tranche of $3M was drawn down in September with the facility being completely drawn down by the end of the year. The group also makes use of a borrowing facility of $7.5M with Auramet Trading to provide advance payment on sales of gold and copper concentrate for the period between shipments leaving Brazil and settlement from the refinery, which extends to the end of 2015. It is also worth noting that there are property acquisition payments due to a past owner of the Sao Chico property valued at $2.3M which will be paid in instalments with the first due in 2015. Of this amount, $1.1M is due within one year. In addition to the loan, the group have granted Sprott a call option over 4,812 ounces of gold at a strike price of $1,285 which can be exercised any time before the end of 2015.

The group expects to have sufficient cash flow from its forecast production to finance its ongoing operational requirements and, in part, to fund exploration and development activity on its other gold properties. The forecasted cash flow projections for the next year, however, include a significant contribution from the Sao Chico development where commercial production has not yet been declared.

After the year-end, the Brazilian Real has reduced in value in comparison to the US Dollar by approximately 20%. The value of the company’s net assets and liabilities will have been significantly impacted by this devaluation. The company sources the majority of its operational consumables in Reals and salaries of its Brazilian employees are paid in Reals so the operating costs are also affected by the change which mitigates against this issue somewhat. It seems likely that the Real will remain weak in the medium term.

The group made a loss this year so there is no PE ratio but on next year’s consensus forecast, the shares are trading hands at a PE of just 4.5 which seems cheap.

Overall then, this seems like another interesting gold miner just about to ramp up production. The deposits are small buy high grade with some 42K ounces expected to be produced over eight years. The company is loss making still but earned its maiden revenues this year. Net assets did increase, but this would be expected due the placing undertaken this year. The company burnt through some $22.1M in cash before financing considerations which seems like a lot but within this there was a $9.8M working capital outflow, and the ramp-up to commercial production at Palito so next year should see an improvement.

There are clearly some potential risks going forward, not least the gold price which is showing continued weakness, I suppose mostly due to the strength of the US economy. In addition, the new mining code and the lack of a mining production license at Sao Chico is of some concern, as is the possibility of the beleaguered Brazilian government adding on short sighted royalty penalties for miners. Next year, the company is expected to produce 35K ounces of gold at all-in costs of between $900 and $950, which does remain below the current gold price. From 2016, there should be additional contribution from the Sao Chico mine. Year-end cash levels of $9.8M should be enough to see the company through the foreseeable despite the $1.1M due next year to the previous owner of land at Sao Chico.

All in all, this seems like an interesting prospect but I am worried about continued gold price weakness so I might keep a watching brief here for now.