Air Partner provides different types of aircraft for charter and related aviation services. Private jets involve the charter of smaller aircraft (under 20 seats) for groups, individuals, air ambulance service and road shows; commercial jets involve the charter of larger aircraft for governments, industrial clients, commercial clients and tour operators; freight involves the charter of cargo transport including emergency aid drops and a time critical door to door delivery service; and support services encompass fuel, emergency planning, and an in-house travel agency.

Air Partner has now released their full year results for the year ending 2012.

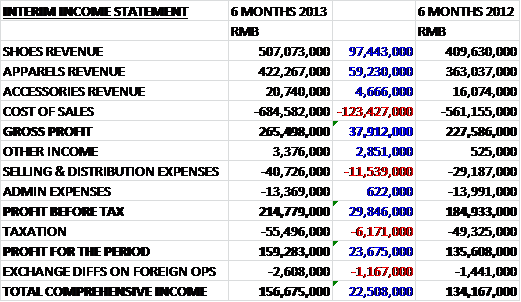

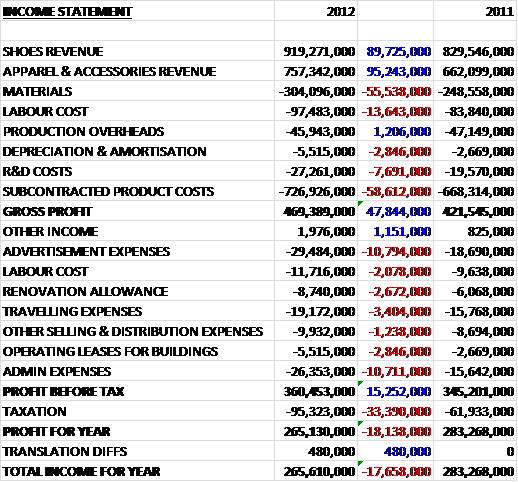

Total revenues at £227.6M were down a substantial £54.4M on last year. Commercial jet brokerage fell by £31.1M but remained the largest business segment; freight brokering fell by £15.9M, other services were down by £10.7M but private jet brokering bucked the trend with a £3.3M increase in revenue. Thankfully, cost of sales also fell considerably, which, along with a favourable £1.2M foreign exchange gain meant that gross profit was down by just £4.1M. Admin expenses fell by £1.5M and the group also benefited from a few one-off gains – there was a £1M accrual write-back, which were estimates of invoices and credit notes for revenues, and costs relating to air charter contracts that it was decided were no longer needed; and a £443K release of US excise provision, due to a lower tax bill than was provided for, somewhat mitigated by a £319K restructuring cost. This meant that tax from continuing operations before tax was down by £1.1M and a much better tax bill was counteracted by the lack of discontinued profits from last year so the annual profit for the group was £1.1M down at £3M.

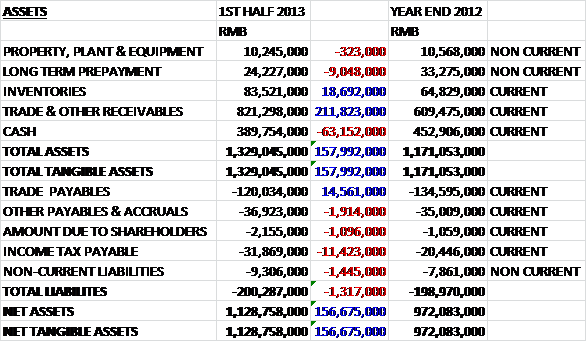

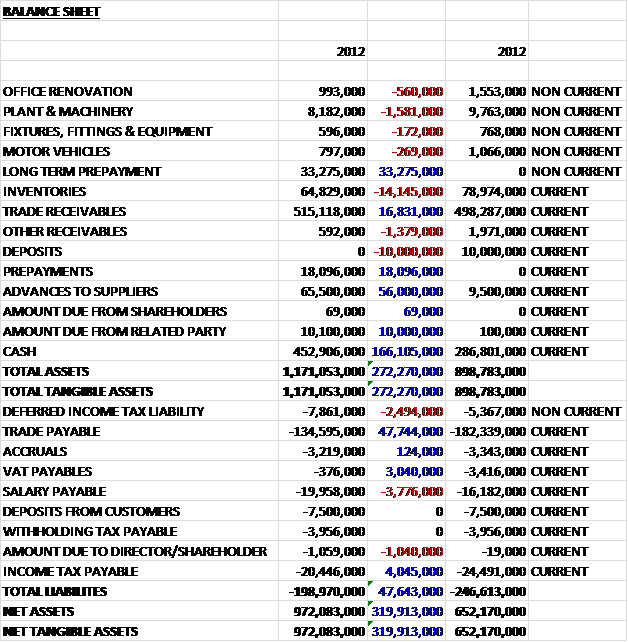

Overall assets were down by the tune of £5.7M at just under £50M. The main falls were recorded in trade receivables, down by £9M; prepayments & accrued income, falling by £4.4M and the loss of ain aircraft worth £980K, which looks as though it has been impaired somewhat and placed in assets held for sale. These falls were counteracted by an £8.6M increase in the cash levels. Thankfully, liabilities also fell. The largest improvements were in trade payables, down £6.1M; “other” liabilities, down £1.1M; the loss of the US federal excise tax provision (£1M) and the £812K reduction in accruals. These were somewhat mitigated by a £2.2M increase in deferred income which means the net tangible assets increased by £893K overall and now stand at just under £13M. The admin claims provision is held in relation to potential settlement claims following the closure of Air Partner Private Jets and the group expects all of these to be settled by the end of July 2014. The restructuring provision relates to redundancy costs due to the structural review that took place this year and the dilapidation provision was paid in full.

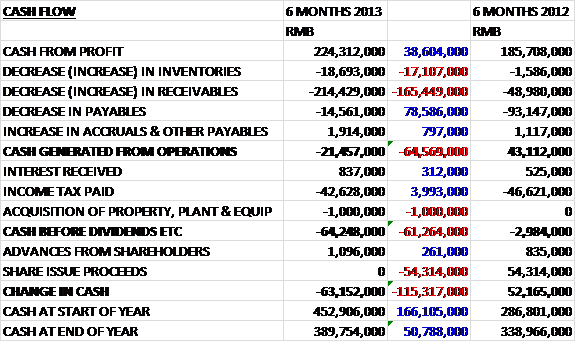

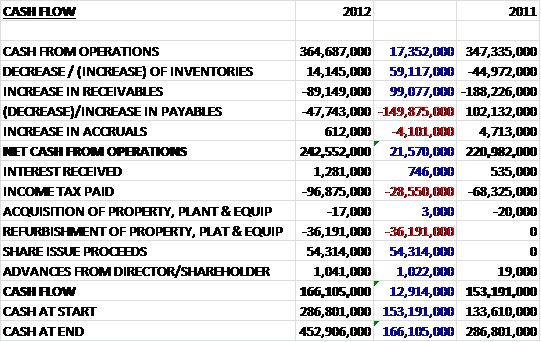

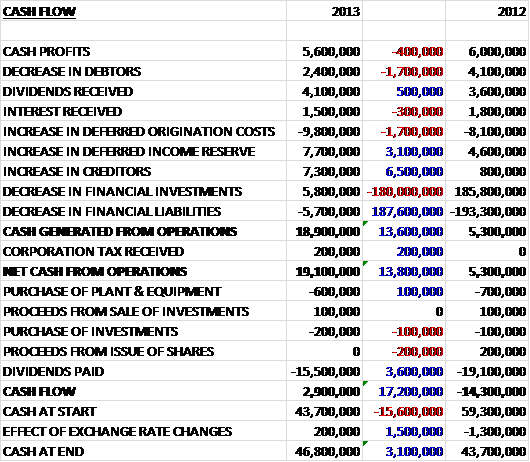

Operating cash of £4.2M was some £2.1M below than of last year but a huge decrease in trade receivables meant that the cash actually generated from receivables was £12.2M. After tax was paid and the contribution from discontinued operations was taken into account, which related to the cash received from the administrators after the closure of Air Partner Private Jets, the net cash from operations was £11.6M, £13.6M higher than last year. The group then spent a small amount of money on tangible assets and computer software to give a cash flow before finance of £11.1M. There was then £1.7M spent on dividends which left the change in cash during the year of £9.4M (£14.1M up on 2011). This does look rather good, although the positive result is almost entirely due to the payment of a large chunk of receivables.

The group seems fairly reliant on one large client which accounted for 17% of revenues during 2012. This was an improvement on the previous year, however, when that client accounted for more than a quarter of all revenues. There does seem to be some very late trade receivables and worryingly, £349K of them were overdue by more than a year. The chairman, Aubrey Adams resigned after being appointed at RBS and Richard Everitt was appointed in his place.

Private jets were the only sector to increase revenues year on year (up 8%), driven by a 67% increase in USA sales (now at £9.2M), although ad-hoc UK sales also increased and non-government contracts made up a greater proportion of the work than previously due in part to continued austerity measures put in place and an increase in jet card members. There was a slight reduction to the underlying profit for the group due to increased overhead allocation now that the division makes up a greater percentage of total revenues.

Commercial jet revenues fell by 18% on last year and suffered a 51% decrease in profits to leave underlying profits at £1.6M, due to increased competition and the oversupply of aircraft but the group did find new revenue streams in the oil and gas industry and there was growth in the niche tour operator and conference sector. Sales to tour operators in Austria, France, Italy and Germany continued to grow too. The division has now re-organised and they are now focusing sales efforts around specific industry segments where there is more potential for growth, such as in oil and gas. Some of the requests that the division dealt with included repatriating stranded cruise passengers from South East Asia; providing tour transport to music stars; supporting major sporting events; and supporting product launches. They also co-ordinated over 100 flights for a car manufacturer to launch their new model in Ibiza and Alicante, and 30 flights for the Euro football championship in Poland and Ukraine.

Freight revenues fell 38% year on year and underlying profit fell by 41% to just £300K due to the decline in global freight market, although the time critical product gained momentum. Overall, though, management don’t see a short term pick-up in this division so have lowered the cost base to reflect this. Two examples of work over the past twelve months include the urgent transport of critical components for a formula one team just before a grand prix and the transport of emergency relief aid to Turkey following a major earthquake.

Support services also saw revenues fall, this time by 36% and underlying profits were down by 54% to just £300K, again due to the market over supply of aircraft and the very competitive market within aircraft sub-leasing and fuel. The fuel contract with British Airways was renewed, however, and costs were reduced in some parts of the segment but overall management as re-aligned this part of the business to be more of a support to the rest of the group rather than a stand-alone segment in its own right.

Overall, market conditions were tough this year, with the added issue of a lack of exceptional world events such as the Arab Spring and the Japanese Tsunami which boosted revenues previously. As such, the board is cautious about the outlook next year. The strategy will be to aggressively target the US market, growing private broking in Europe (where their current market penetration is only 2%), proactively market within the oil & gas sector and to target the tour operator sector. In addition, where margins are attractive, the group will be looking to emerging markets. As part of this desire, they launched a strategic partnership with InterGlobe in New Delhi, providing a range of private aviation products in India based on a low-cost model. The group is involved in a business that by definition has a very low visibility but is also allied to the general economic outlook.

At the time of writing, the decrease in the final dividend meant that the current yield is 3.3%, which is not too bad but the current P/E is 17.3 which seems a bit lofty for a company which seems to be stuttering on growth. There were no broker forecasts to try and ascertain a forward looking P/E. Profits were down across nearly all sectors due to increased competition and a decline in the global freight market. Net assets actually improved, but would not have done were it not for the release of the provision held for the US government taxes. Cash flow was the one shining light, achieved by keeping a tight reign on receivables. There is also no debt here which is always nice to see. I do think there is a decent case for investment here but the outlook seems a little too pessimistic for the share valuation in my view. I will keep abreast of new but not yet invest.