980 Great West Road, Brentford, TW8 9GS

Glaxosmithkline is a global healthcare group which is engaged in the creation, discovery, development, manufacture and marketing of pharmaceutical products including vaccines, over the counter medicines and health related consumer products. The pharmaceuticals business develops and makes available medicines to treat a broad range of serious and chronic diseases, with respiratory illnesses making up the largest segment. The vaccines business is one of the largest in the world, producing both paediatric and adult vaccines against a range of infectious diseases. They also develop a range of consumer healthcare products in various sectors.

Much of Glaxo’s competition comes from generic producers who are able to offer the same products for much cheaper as they do not have to incur costs for R&D and other costs in bringing new medicines to market, particularly in Western markets. This effect is less pronounced for vaccines or products where patents exist on both active ingredients and the delivery device.

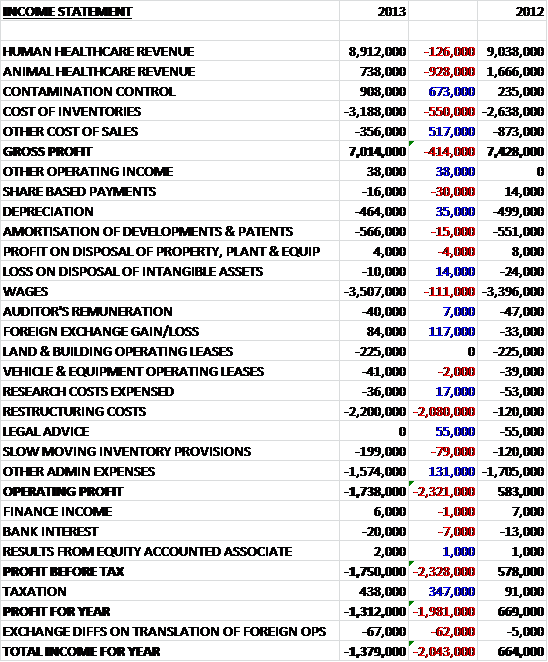

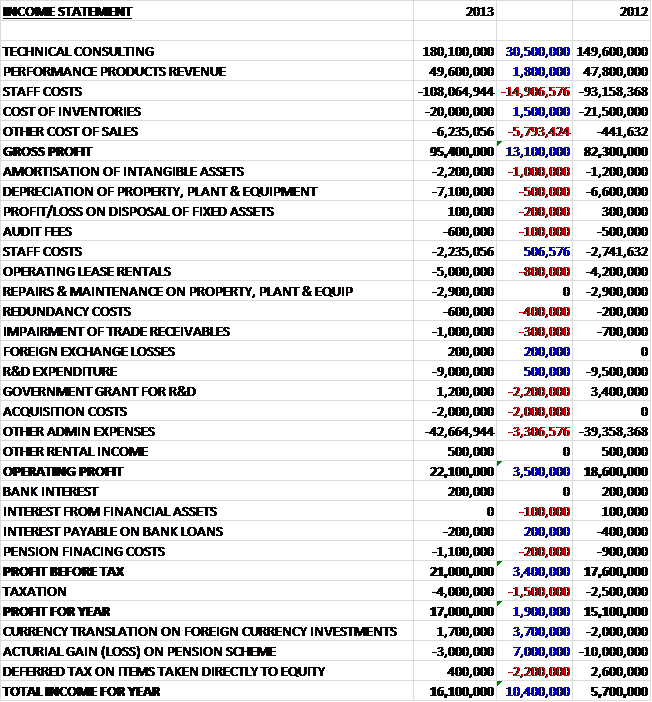

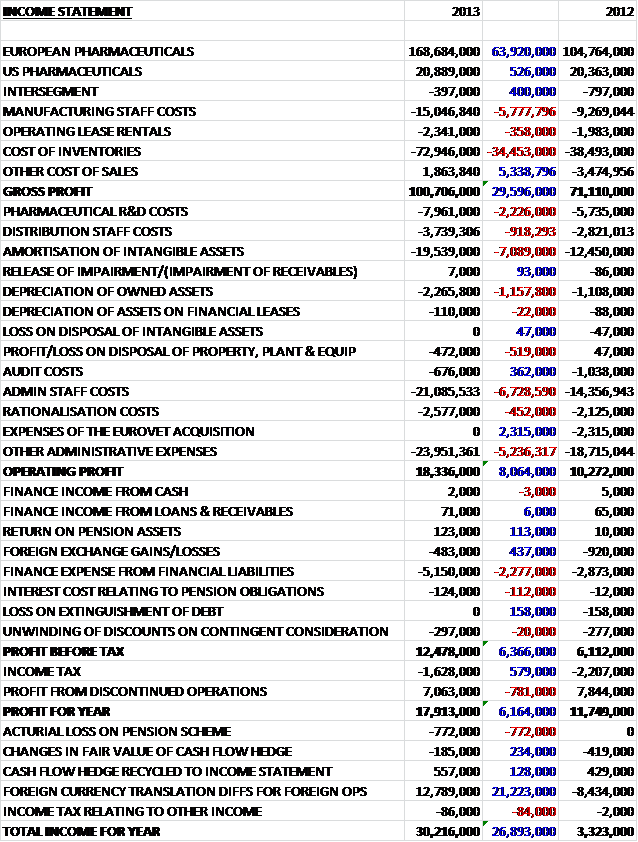

We can see that total revenues are down by nearly £1B to £26.4B. Most pharmaceutical segments suffered a decline with the exceptions being Oncology, Rare Diseases and Immuno-Inflamatory and Oral care and Nutrition in the Consumer Healthcare business. Cost of sales increased during the period, driven by higher inventory costs and write-downs to give a gross profit £1.2B lower than in 2011. Despite a £583M increase in intangible impairments, other operating costs generally fell during the period. The big differences we see during the period were a £339M increase in profit from business disposals, a £233M gain on settlement of collaborations and a £349M increase in the gain on the acquisition of a joint venture. This flattered the operating profit somewhat and that was only £415M lower than last year at £7.4B. Counteracting this, however, was the lack of £585M relating to the profit on disposal of interest in an associate before a lower tax amount gave the profit for the year £714M lower at £4.7B. This was eroded somewhat by unfavourable exchange differences and a further actuarial loss on the pension scheme and the total income for the year was £4B.

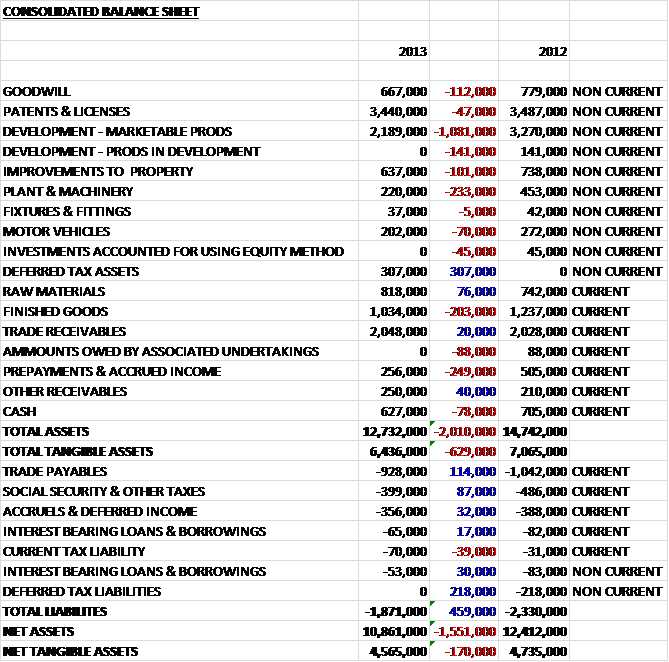

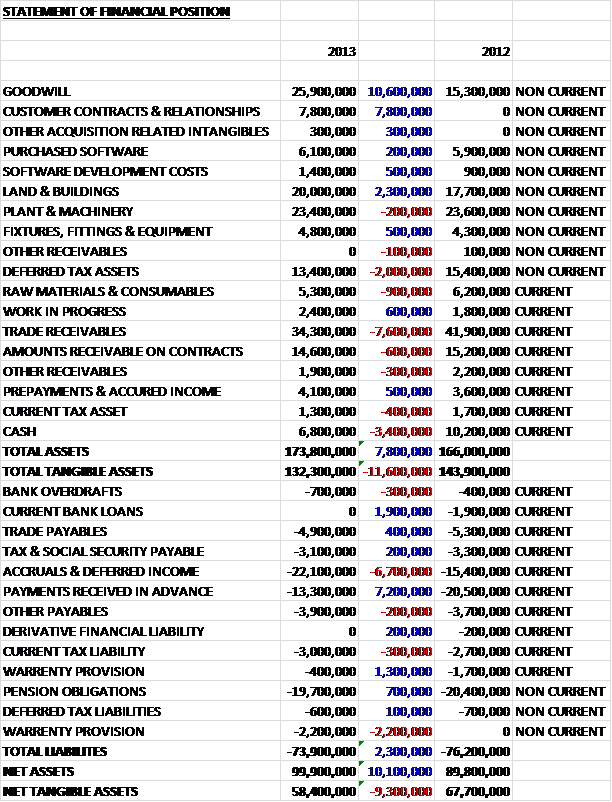

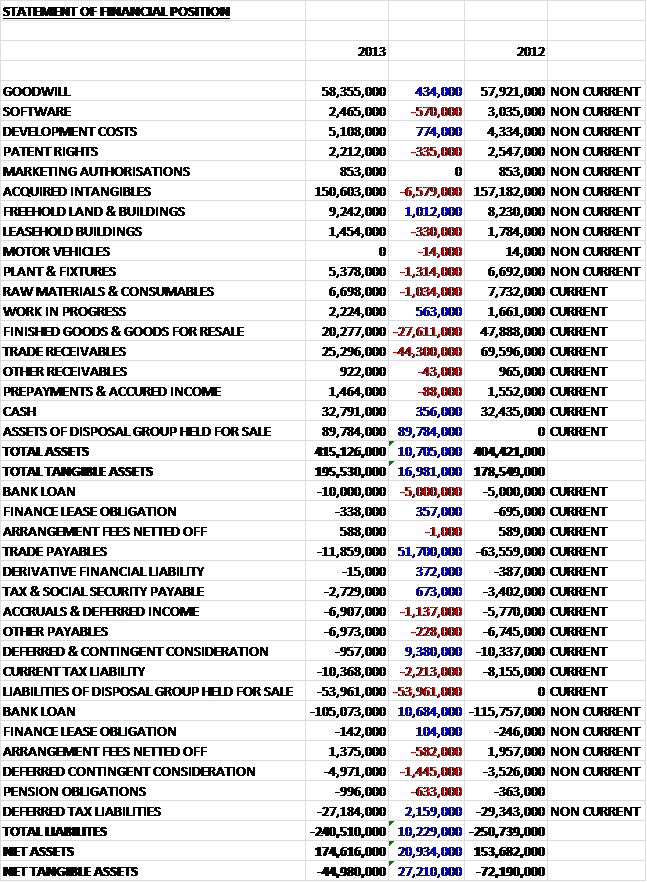

The largest increases in the value of assets were in Licences and Patents which increased by £2.3B to £7.4B due to the acquisition of Human Genome Sciences. The only other major increase in assets was Goodwill up £605M to £4.4B and land & buildings, up 226M. These increases were counteracted by decreases in cash, down £1.5B; assets held for sale, down £605M due mainly to the disposal of the OTC brands; deferred tax assets, down £464M, which relates to the centralisation of their intellectual property and product ownership into the UK, and trade receivables, down £326M, which include £257M due from state hospital authorities in Greece, Ireland, Italy, Portugal and Spain. These movements, along with some other minor changes have increased the level of assets by £395M. As the largest increases were intangible, however, the tangible asset base tumbled by £2.6B.

As far as liabilities are concerned, we can see £2.4B reduction in the value of current provisions. This was predominantly due to the settling of the US legal disputes. In contrast, an increase was seen in “other payables” which were up by £1.4B during the period. Other payables included £585M related to the potential maximum amount payable to shareholders of GSK Consumer Healthcare Ltd, the Indian subsidiary after Glaxo offered to buy all the shares and a contingent consideration relating to the acquisition of the Shionogi-ViiV healthcare joint venture. Apart from the increased payables, the bulk of the increased liabilities are in the form of extra borrowings and loans which were up a very substantial £3.4B. This has helped increase liabilities by £2.5B. The upshot of this is that net assets were down by £2.1B to £6.7B but net tangible assets fared even worse, down £5B to a negative £7.8B. I do feel that for Glaxo, those brands and patents are rather valuable so I have also calculated the net asset value without the Goodwill (which I still consider to be somewhat of a distraction when trying to calculate the value of a company) which was £2.7B lower at £2.4B. Either way, it is clear that borrowings are well up and that as far as the balance sheet was concerned, the group took a bit of a battering this year.

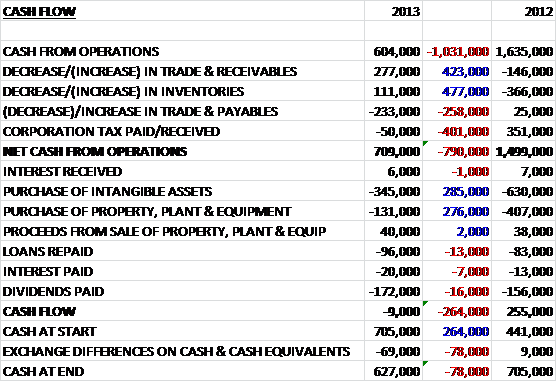

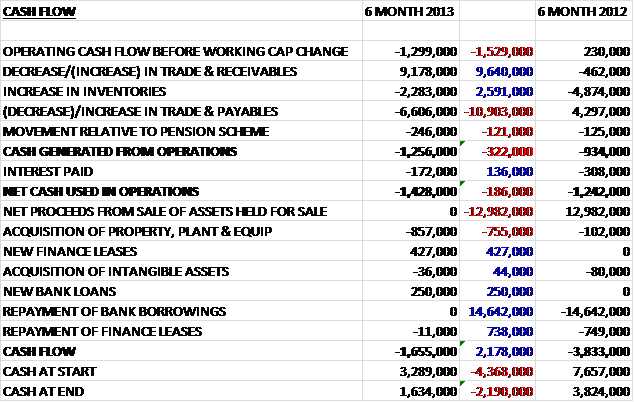

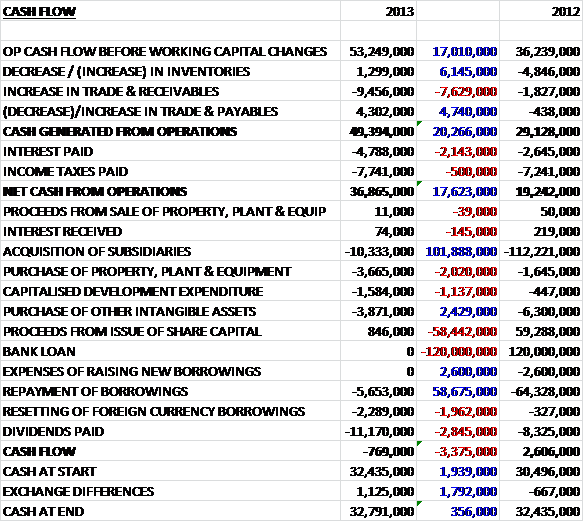

Operating cash flows for the year of £5.5B were a disappointing £1.8B down from last year. The group has been actively targeting working capital and has already reduced the capital cash conversion cycle from 202 days to 194 days and having already targeting receivables and payables, are now looking at the inventory levels (inventory levels increased somewhat due to the HGS acquisition and increased vaccine inventories). These favourable movements in working capital meant that cash from operations was £6B before tax took its toll and brought it back down to £4.4B, £1.9B lower than last year. A £1.1B receipt from the sale of intangible assets paid for the purchase of property, plant and equipment. There was a £3.6B increase in borrowings, which paid for the business purchases (£2.3B) and part of the share buy-back scheme (£2.5B). The group also had to pay £779M out in interest on the loans and £3.8B was given back to shareholders in the form of dividends. Overall this all lead to a net cash outflow of £1.6B. By taking into account the new loans, the share buy-back scheme and the new business sales, the cash flow would have been a negative £493M. Considering this included the £3.8B dividend to shareholders, this is not too bad (although it does depend on the £1B sale of intangible assets) but I would be looking for a better performance next year to sustain that dividend and prevent spiralling debts.

The US and EMAP regions were the only areas that increased profits. The result in Europe was particularly badly hit, being down by £525M. During the year a new joint venture, Japan Vaccine Co was started with Daiichi Sankyo which commenced trading in July. Most of the profit from associates is received from Aspen Pharmacare (£235M during 2012). Aspen, 19% owned by Glaxo is listed on the Johannesburg stock exchange and is Africa’s largest pharmaceutical manufacturer

The new licenses and patents that have been acquired are also considered the most valuable, with Dolutegravir valued at £1.8B and Benlysta valued at £1.2B. These are pretty hefty valuations! As far as brands are concerned, Panadol is considered the most valuable at £413M with Sensodyne next at £256M. Glaxo is currently involved in numerous legal disputes and incurred a charge of £449M related to product liability cases involving Paxil, Poligrip and a few others.

During the year the group made a number of acquisitions, the largest being Human Genome Sciences, a US based biopharmaceutical company which is focused on the development of protein and anti-body drugs for the treatment of immuno-inflammation diseases for $2.3B of cash. The goodwill difference was £791M. Another considerable purchase was the acquisition of Shionogi’s share of the Shionogi-ViiV healthcare joint venture. There were no tangible assets gained but the main drugs under development are Dolutegravir and early stage integrase inhibitor compounds. There was no cash involved in this acquisition but there is a contingent consideration based on the future sales performance of the compounds, which has a theoretically unlimited value and a 10% stake in the subsidiary has also been offered. Glaxo obviously see potential in Shionogi-ViiV’s pipeline but the contingent consideration concerns me slightly. The group also made two other acquisitions for a consideration of £302M. During the year the group disposed of their holding in Quest Diagnostics, listed on the NY stock exchange, generating a profit of £584M. After the end date of the balance sheet, Glaxo increased their stake in their Indian subsidiary to 72.5% for £570M.

The pharmaceuticals industry seems to be keeping several lawyers in work and there are a substantial number of legal claims that Glaxo is involved in. Many of them seem to be generic drug makers challenging patents for various drugs so that they can enter the market. Perhaps more worrying are the product liability suits where people have had adverse side effects from the drugs. The most infamous current example is Avandia, where the group have settled many of the US claims but claims in Canada and Israel are still pending. Another significant product liability case is with Paxil where there have been alleged problems with birth defects when pregnant mothers take the drug, along with possible dependency issues. The group has settled the majority of the US claims relating to birth defects but a number of other claims remain unsettled, including many in Canada and in the UK. Finally, there are still some outstanding claims relating to the use of Poligrip between 2005 and 2010. It is alleged that the use of Zinc in the adhesive caused copper depletion and neurological problems. Many of these cases have been dismissed but some are still ongoing. Sales and marketing cases are also costly for Glaxo. The Avandia related marketing matters have mostly been settled, as have the “Colorado Investigation” lawsuits, but a number still remain outstanding. Litigation involving the average wholesale price of drugs sold to US state Medicare organisations has also mostly been settled with only Illinois and Wisconsin outstanding. A matter relating to the Puero Rican manufacturing site has also been settled for the substantial amount of £500M. I am not sure what the issue was but this is a substantial pay out by the group.

There are also a few competition investigations, with the EU and the UK looking into agreements relating to patents and generic drug makers, to determine whether competition has been stifled by some of these payments. A couple of US anti competition and monopoly law suits where buyers alleged Glaxo conspired with other companies to delay generic competition and charge higher prices are due to be settled for $216.5M. Other litigation includes actions relating to the purchase of Steifel labs where their former employees were encouraged to sell their shares back to the company at an undervalued rate before it was sold to Glaxo – not really Glaxo’s fault but they have to pay up if the claims are successful. Additionally the group may be liable for the disposal and clean-up of hazardous waste at various US sites. The figures could be significant but the group accrues values for this as it goes along. Overall, all these actions look daunting but after the US Avandia issue seems to be mainly solved, there are not that many outstanding issues that could be hugely detrimental to the group depending on the outcome of the anti-competition investigations.

As far as individual drugs are concerned, by far the most important with £5B of sales (flat on last year) is Asthma/COPD treatment Seretide/Advain. Other drugs that earn more than £700M are Avodart for Prostatic Hyperplasia (£790M); infanrix, a vaccine for Diptheria, Tetanus, Polio and Hep B (£775M); and Flixotide, another Asthma remedy (£779M). From these figures it is clear just how important Seretide is to Glaxo and the patent expires in the EU for this drug in 2017.

As would probably be expected, emerging markets are becoming more important for Glaxo and they now account for 26% of sales and grew 10% during the year. Sales in Japan fell 6% because last year was boosted by catch-up sales of Cervarix. Sales in the US were down 2% but the group are apparently preparing to launch a few new products in the new year. The real drag on results, however, was the performance in Europe with business there weaker by the tune of 7% where government austerity measures are impacting growth. R&D progress was good during the year and there are now 6 key new products under regulatory review and phase 3 data is expected on 14 products over the next couple of years. The group have recently announced a program that aims to cut costs by about £1B by 2016 and will help simplify supply chains.

Investments in emerging markets are being made and during the year a new innovation centre was opened in China and the shareholding in the Indian subsidiary was increased. A strategic review is underway regarding the Ribena and Lucozade brands, which are popular in Western markets. Investment is also being made in the UK with a new biopharmaceutical manufacturing centre in Ulverston part of a £500M investment program.

In many countries the prices of pharmaceuticals are controlled by law. Governments can also influence prices through their control of national healthcare organisations. In Europe, governments are responding to increasing austerity pressures. Healthcare reforms in France, Spain and Germany have restricted pricing and mandated generic solutions. In Japan the government implemented its mandatory bi-annual price review in 2012. In the US there are no government price controls over private sector purchases but federal law requires pharmaceutical manufacturers to pay rebates on certain medicines to be eligible for reimbursement under several state and federal healthcare programs. Those rebates were expanded in 2011 and this year the government is finalising additional details for implementing the Affordable Care Act which includes an expansion of the government’s health insurance for low income citizens.

In the US, the healthcare market is undergoing changes due to the ongoing healthcare reforms and pharmaceutical companies are having to adapt to the changes. Overall sales during the year were down by 2% but when Avandia was taken out of the equation, sales were flat. Operating profit increased by 1% as a result of continuing efficiencies being made. In the respiratory market, sales grew by 1% after a fall last year. Advair, the largest product was up 1%, whilst Flovent sales reduced by 1%. Ventolin sales did well, increasing by 14% this year. Strong performances from Lovaza, Lamictal, Promacta, Votrient and Arxerra helped offset the loss of patent exclusivity for Ariztra and Argatroban and the loss of Avandia sales. The new treatment for lupus, Benlysta contributed sales of £65M during the year. Turnover was flat in the vaccines business as a decline in Flu vaccines were offset by increases in Pediarix and Boostrix. During the year the pipeline made progress with several products receiving FDA approval including Votrient for Sarcoma, Promacta for Hep C, MenHibrix, a vaccine for Meningitis, Raxibacumab for Anthrax inhalation and Fabior foam for dermatology. In addition, five other medicines were submitted. The year also included a settlement with the US government on long standing legal cases as mentioned earlier.

In Europe, economic conditions remain hard with many governments undergoing austerity measures. In addition to the 7% drop in sales, there was also an 11% fall in operating profits. Pharmaceuticals were down 8% and Seretide revenues fell by 4% despite increased volume as prices were cut. Sales of Oncology products did well, however, as did sales of Duodart and Avodart which increased by 9% despite Duodart not having market access approval in France or Italy. Gaining approval to market products continued to be challenging but improvements were seen this year with Prolia, a treatment for osteoporosis and lupus treatment Benlysta being launched in most markets. Vaccine turnover fell by 4% reflecting austerity driven price cuts and the group have decided to further restructure the European operation to reduce costs.

In Emerging Markets, growth, although still strong, slowed somewhat as global economic factors, increasing price controls, funding constraints and aggressive local competition took their toll. Within the 10% overall increase, sales in Latin America were up 11%, China up 17% and India up 10%. Price constraints in Turkey and Korea counteracted these large increases though. Seretide, Avodart/Duodart and Avamys all gained market share with strong launches for Duodart in Philippines and Prolia in Brazil, Russia and Argentina. Benlysta is now approved in 10 countries across the region, including Russia and Taiwan and was launched in four. Regulatory approval was completed for Relvar in Philippines, Taiwan and Brazil. Classic brands increased sales by 5%, boosted by strong showings from Augmentin (8%), Ventolin (10%) and Zeffix (3%) including successful tenders in Saudi Arabia, Russia, Korea and Kazakhstan. Vaccines grew by 14% driven by Synflorix, Rotarix and Cervarix with Synflorix having a particularly successful launch. Operating profit grew broadly in line with sales.

Although turnover in Japan fell by 6%, this reflected the end of the Japanese HPV catch-up vaccination program. Discounting Cervarix, turnover was up by 5%. The Japanese system of reimbursement helped Glaxo as it takes into account strong innovation portfolio. Pharmaceuticals turnover grew by 3% with strong growth from the recently launched products Lamictal, Avodart and Volibris, partly offset by the impact of price cuts and increased generic competition for Paxil. The respiratory portfolio grew 6% with strong contributions from Adoair and Xyzal counteracting declines in Flixonase and Zyrtec. There were six new approvals this year including Samtirel for Pneumonia, Paxil CR for depression, ReQuip CR for Parkinson’s disease, Votrient for soft tissue sarcoma, Botox for hyperhidrosis and Malaron for malaria. New product filings were made for Relvar (Asthma/COPD) and Arzerra (Leukemia). Operating profit in the region fell by 7%, comparable to the decrease in sales.

Consumer Healthcare turnover was up by 5% (discounting the effect of the OCT brand sale) with strong growth in Oral Care, Nutrition and Total Wellness partially offset by a small decline in Skin Health. US sales grew by 2% and European sales were flat year on year reflecting the continued tough economic conditions. The rest of the world markets grew by an impressive 12% with India, the Middle East and China making strong contributions and the group increased their holdings in their Indian subsidiary. Within Total Wellness, gastro-intestinal products did well, up 11% through the launch of Tums Freshers in the US and strong performance of ENO in emerging markets. The weight loss product, Alli suffered a major interruption from the supplier which impacted sales, however. Smoking reduction products performed well in Europe and North America. The Oral Care category showed good growth, up by 8% and led by Sensodyne rollouts of Repair & Protect. The denture care business also did well, up by 12%. In Nutrition (up 8%), Horlicks continued to grow in India and the Maxinutrition brand acquired in 2011 achieved strong growth of 21% year on year. The Skin Health business registered a 1% decline during the year where strong performances of Bactrobran in China and Zovirax were offset by declines for Hinds in Latin America and Oilatum in the UK. Operating profit in the division fell 9% reflecting the disposal of the OTC brands.

Turnover in the HIV division was down 10% on the previous year. This decline was anticipated as the mature product portfolio faced greater generic competition in the US. Two drugs fared well, however, with Epzicom/Kivexa (now by far the most important drug in this segment) growing sales by 10% and Selzentry/Celsentri increasing sales by 20% and the latter experienced expansion into Japan, Argentina and Australia. Due to robust cost control and a change in the mix of products sold profits in the division were flat year on year. The submission of Dolutegravir in Europe, US and Canada was completed during the year to try and mitigate the ageing drug portfolio in this sector. Glaxo offers HIV drugs to many low income countries on a not for profit basis.

The upcoming pipeline does look rather strong across the board at the moment with new vaccines for flu, meningitis and meningitis-Hib gaining approval along with two significant new indications for existing medicines treating cancer and hepatitis. Six new products were also submitted to regulators during the period covering treatments for respiratory disease, cancer, HIV and diabetes. Additionally, phase 3 data (the final tests before a decision is made on submission) is expected to be received for a further 14 assets in the next two years.

The two new indications for new medicines were for Promacta for thrombocytopenia associated with hep c and Votrient for the treatment of soft tissue sarcoma. The six new submissions were respiratory medicines Relvar/Brevo and Anoro; oncology medicines Dabrafenib and Trametinib; Dolutegravir for HIV and Albiglutide for diabetes. Two new chemical entities moved into phase three development whilst none in phase three were terminated so all in all a fairly positive outlook for the pharmaceutical segment. The three new vaccines that gained approval were Nimenrix for meningitis, MenHibrix for meningitis hib and a flu vaccine with four other vaccines in late stage development. The development of new vaccines is a complex process that takes about 10 to 12 years and traditionally vaccines have been used to prevent illness but one interesting area for study is for vaccines to help the body’s immune system fight current illnesses such as a variety of tumours.

Some new consumer healthcare products launches during the year were Tums Freshers, a combination of heartburn relief and breath freshener; Abreva Conceal, a patch that conceals cold sores whilst still letting air in; and Horlicks Growth +, a nutritional product for children.

There were £165M of restructuring charges related to the acquisition of HGS during the year due to restructuring and reducing costs. Over the past five years the manufacturing organisation has also undergone rationalisation and savings of £930M per annum have been achieved. There is also a program to standardise packaging and to phase out small volume packs to further improve efficiencies.

This was a mixed year for Glaxo, revenues were down and profits overall were down by £415M on last year as impairments were counteracted by gains on disposals of assets. Net assets (not including Goodwill) more than halved during the year as an increase in the value of patents was more than counteracted by a reduction in cash and increases in borrowings and payables. The cash flow on the surface was rather disappointing with a £1.6B outflow of cash. During the year, however, the group spent £2.3B on acquisitions, £3.8B on dividends and £2.5B on share buy-backs and the group are targeting £1B to £2B of share buy backs next year. It is also notable that loans increased by £3.6B and there was £1B received from the sale of the OCT brands. Net Debt at the end of the year was £14B, £5B more than last year. This is quite a hike in debt levels but was affected by the £1.9B to settle the most significant ongoing US government investigation and £2B of cash paid out to purchase Human Genome Sciences and the aforementioned share buy back scheme.

As with most companies around the world, Glaxo is finding Europe very tough going with increases of sales coming from emerging markets. The settlement of most of the US claims is welcome but the anti-competitive issues could still be a problem. The pipeline of new drugs is encouraging but it should be noted that Glaxo is very dependent on one drug at the moment (Seretide) and if this fails there could be trouble. At the current share price, the P/E ratio is a rather pricey 17 but this falls to 14 for 2013 estimates. The P/E for this year does drop to 12.4 when the non-core items such as amortisation and legal fees are taken into account (whether legal fees are a non-core cost is another argument altogether, though). The current yield is a healthy 4.6% and that encourages me to rate these as a hold.