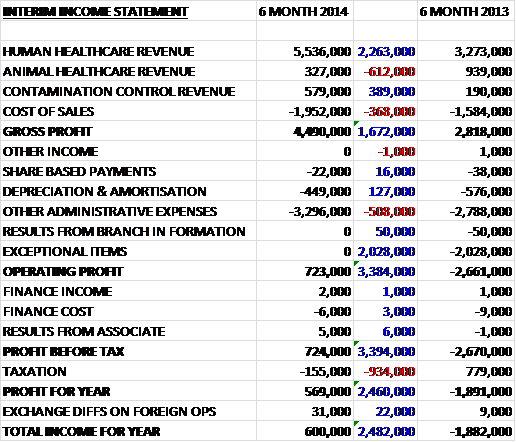

President Energy has now released its interim results for the half year to end 2013.

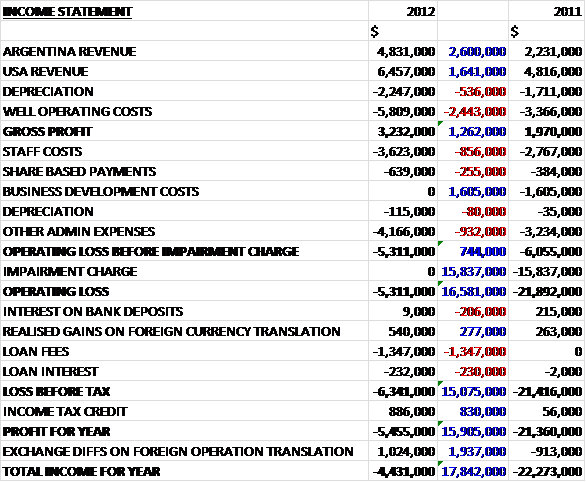

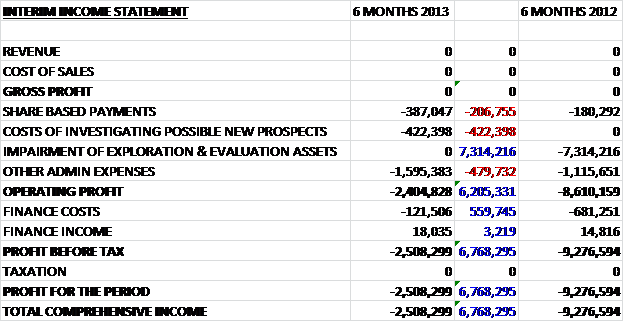

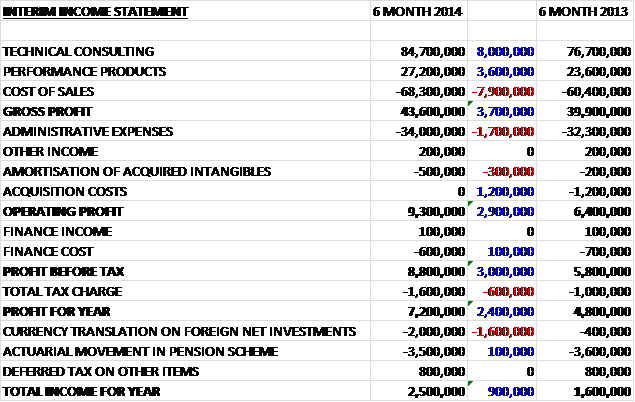

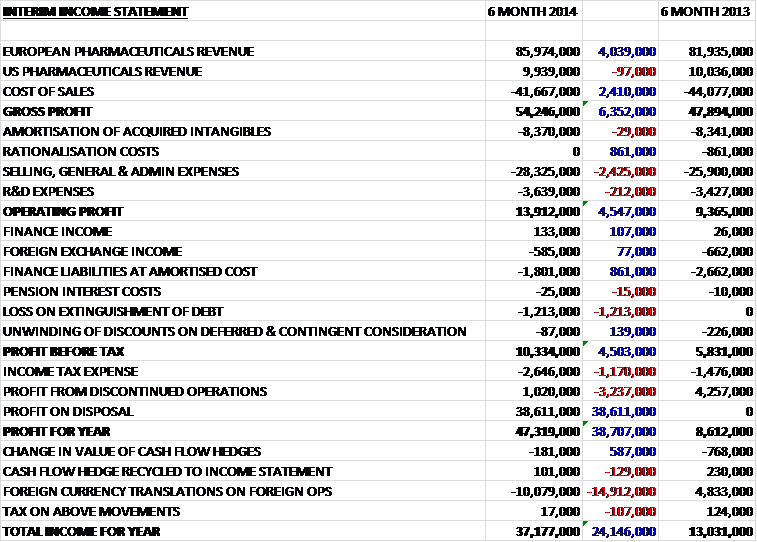

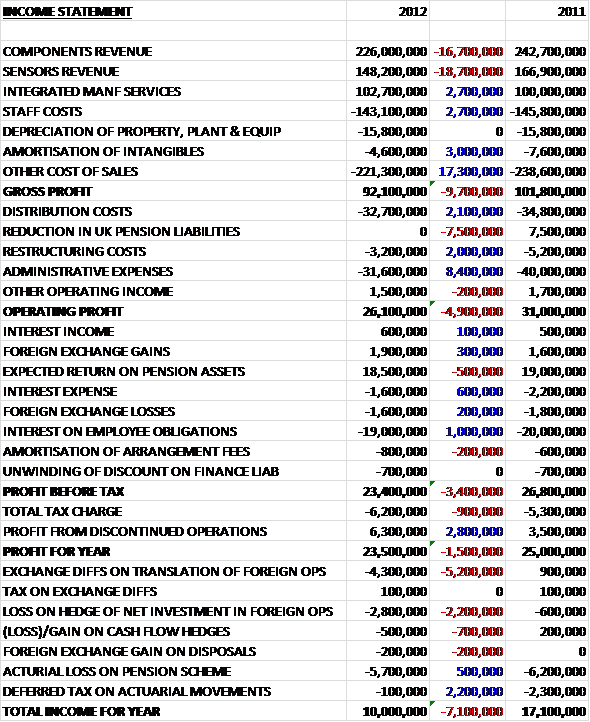

Over the first half of the year revenues were up by $692K when compared to the same period of 2012. Depreciation was slightly higher but well operating costs fell considerably by $1.1M, driven by an improved cost position in Argentina. Gross profit was therefore up by $1.6M to $1.9M. This was almost exactly the cost of the wages for the group, which at $1.9M, increased by $381K. We also saw an increase in share based payments, mitigated by a fall in other admin expenses to give an operating loss of $2.3M, $1.7M better than last year. This year, there was an impairment charge of $460K relating to the relinquishment of the PEL 132 license in Australia, compared to no impairments in the first half of 2012. As far as non-operating costs were concerned, there was a positive gain on foreign currency translation, entirely counteracted by $356K increase in loan fees and interest. Loss before tax was $2.9M, which was $1.1M better than last year. A far lower tax rebate, though, meant that the total loss for the year was actually $880K worse than in 2012 at $2.7M.

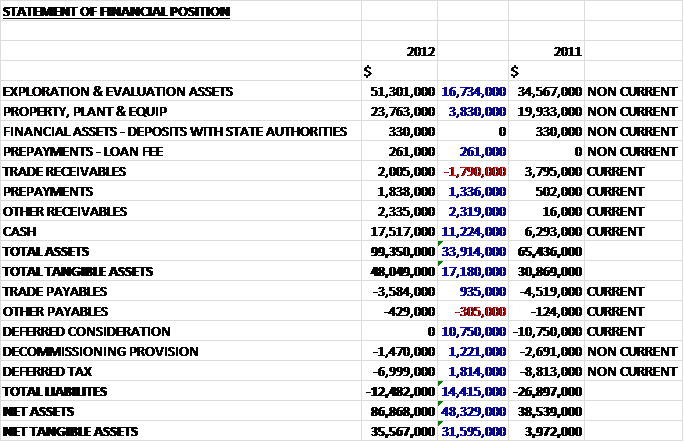

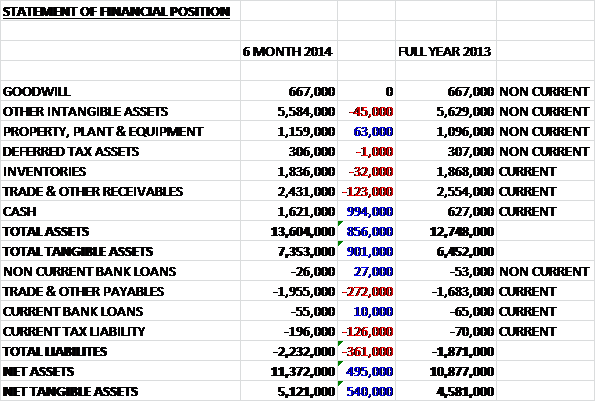

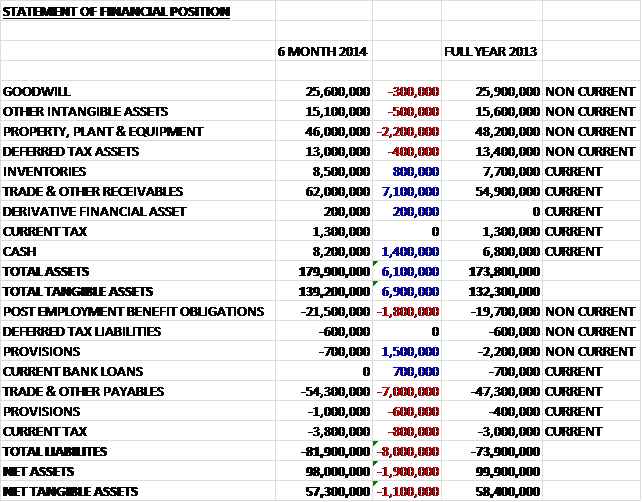

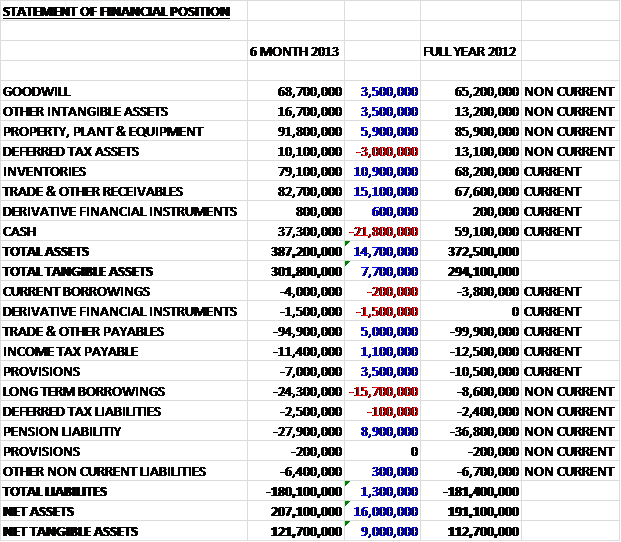

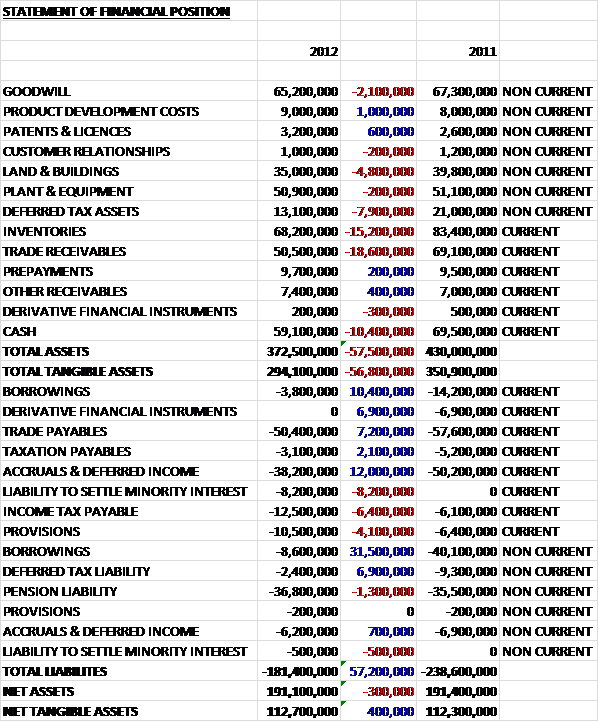

Total assets for the year were down by $8M. We can see that a reduction of $10.7M was counteracted by a $14M increase in property, plant and equipment. The driver behind the reduction, however, was the $11.2M fall in intangible exploration and evaluation assets. Apparently, following seismic reprocessing, $14.1M of exploration costs in Argentina were reclassified as property, plant and equipment. Liabilities decreased by $1.7M when compared to the end point of last year. This was driven by a $1.4M fall in payables and a $293K decrease in deferred tax liabilities. The result of this is a $6.3M fall in net assets, which now stand at $80.6M.

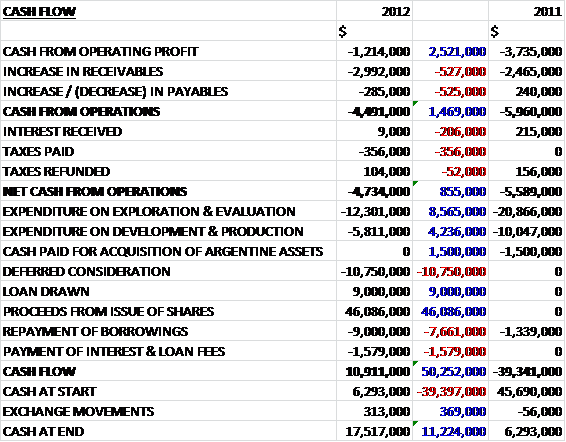

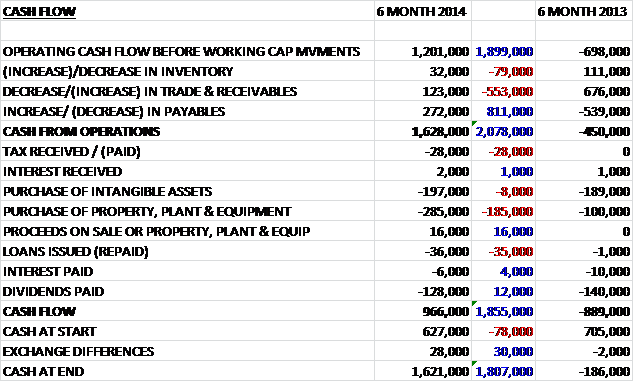

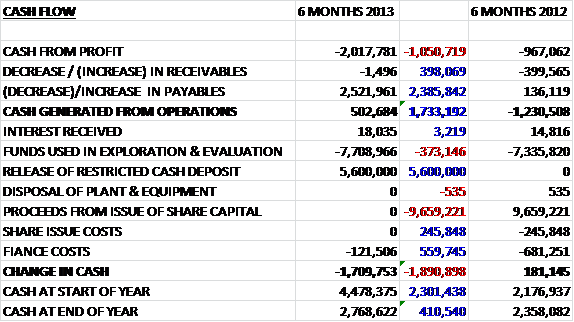

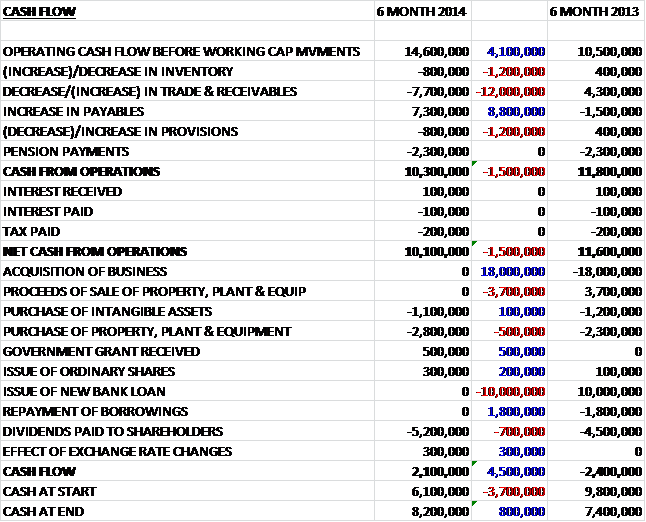

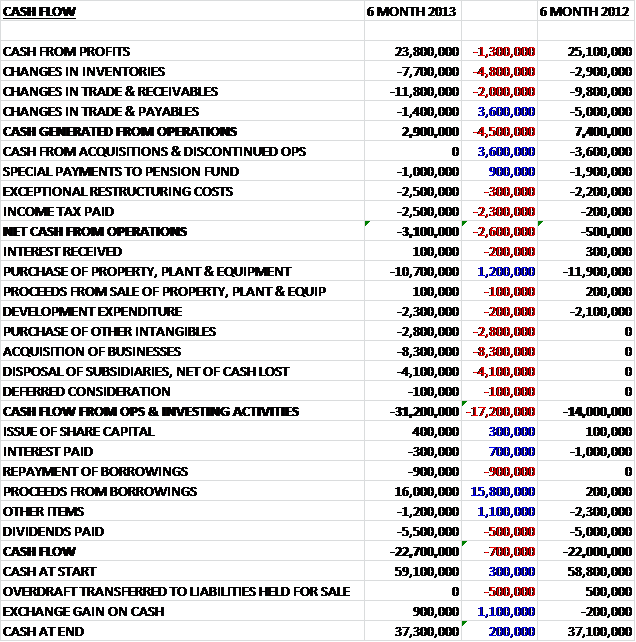

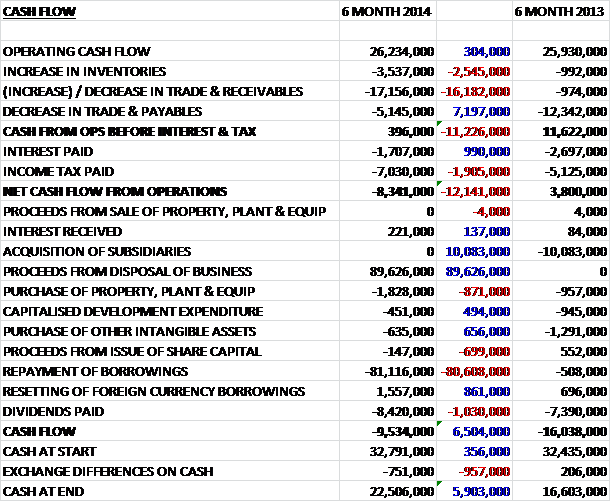

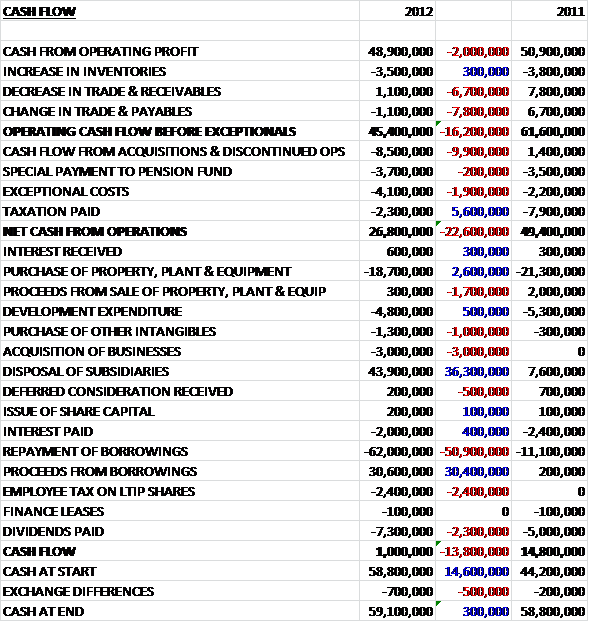

Before working capital changes, it is good to see that the group had a positive inflow of cash of $888K compared to the outflow during the same period of last year. A decrease in payables, however, meant that the cash outflow from operations was $601K, still $3.1M better than last year. The group then spent $5.5M on exploration and evaluation, $1.5M more than in 2012; and $2.5M on development and production, which was pretty much the same as the amount spent last year. This year was a lot quieter as far as cash flow was concerned as there were no acquisitions, new loans or new shares issued. So, after the payment of the loan fee, the outflow of cash was nearly $9M which leaves the group with a cash position of $6.8M at the end of the half.

In Paraguay the original seismic acquisition programme was successfully completed ahead of schedule and initial results were apparently encouraging. In addition to this original programme, the group also acquired a further 700km of 2D seismic detail on the additional follow on potential throughout the basin, which has now been 90% completed and more than 20 potential drilling targets have been identified. The high grade targets identified to date lie within the Cretaceous interval but the new seismic details suggest that there is also a large Paleozoic play system, and technical work has now begun to establish the potential. Preparations for drilling remain on course for the first well of three to be spudded in Q2 2014. In August, Paraguay had a general election where President Cortes won a clear victory and set out his determination to attract foreign investment, which bodes well.

In Argentina the group successfully completed the three-well stimulation campaign on wells PE7 and PE8 at Pozo Escondido, and well DP1001 at the Dos Puntitas Field. Wells PE7 and PE8 had both been closed for 20 years and the preliminary results for these two wells provide strong encouragement for the establishment of new reserves in the carbonate reservoir, and for considering the stimulation across the large portfolio of old wells in the concession. Initial production from these two wells has increased by 100% with the net production attributable to the group running at about 300 bopd and expected to further increase with the contribution from the third well.

The reprocessing and interpretation of the data on the Pozo Escondido and Dos Puntitas fields has now been completed, showing significant undrilled highs within the field areas. At Pozo Escondido, it is estimated that there is an increase in the “sock tank oil initially in place” (STOIIP) of 215% to 63 MMB. At the Dos Puntitas field, the reprocessing has validated the existing STOIIP of 15 MMB and six undrilled highs have been identified. These results point to a further development potential in these fields through fracks, sidetracks and further drilling. Average net production for the period was 153 bopd, down by 2 bopd compared to the same period of last year due to delays to the stimulation programme but current net production, including the two recently stimulated wells, is substantially higher, at 300 bopd. Average realised prices for the period were $71 per barrel and the Argentine assets are currently breaking even.

Louisiana continued to provide the group with solid production and cash flow. Average production was up 36% at 212 boepd and average realised oil prices were $108 per barrel. Realised prices for gas sales were $97 per barrel of oil equivalent. Current production in Louisiana is 275 boepd. In Australia, the PEL 82 asset is currently the subject of farm out discussions and PEL 132 was relinquished with an impairment of $460K taken.

The current cash balance is $6.8M and the group has a $15M revolving loan facility in place. The Argentine assets really seem to be stepping up production but the real prospect is Paraguay. There will probably be no re-rating, either up or down, until the first wells are drilled there but I am happy to hold until then.

On the 27th September the group announced that it had entered into an agreement with the International Finance Corporation, and arm of the World Bank, to acquire over 12% of the company’s shares. New shares would be placed in order to allow this and the proposed investment is £12.5M. This is a good vote of confidence, but does mean more dilution of the share capital.

On 4th November the group announced that it had entered into an eighteen month contract with Schlumberger for the provision of project management and integrated drilling and completion services for its Paraguay drilling programme. Early seismic results show the possibility for an expanded resource potential compared to the basin estimate of 159 mmb of risked oil published last year. At least two major structural plays have been identified and management have suggested that the total risked resource potential of greater than 500 mmb of oil is a possibility.

On 5th December the group confirmed it had signed the subscription agreement with the IFC. It was also announced that as part of the deal they have given certain covenants to the IFC, including an undertaking to adhere to IFC’s environmental, social and other performance standards in relation to its conduct in all Paraguay operations. IFC are also able to nominate a director to the board to act as their representative, which I guess is fairly standard with this size of holding. From IFC’s perspective, they are looking to help Paraguay harness its domestic resources and decrease the country’s dependence on fuel imports. There are no further details given about the covenants, but there seem to be quite a few conditions attached to this deal.

On 8th January, the group released an operational update. In Paraguay, the group procured a rig and a letter of intent has now been entered into to drill the 2014 exploration programme. The contractor is Queiroz Galvao Oleo a Gas, one of the largest service providers in Brazil. The rig is capable of drilling down to depths of 5000m, which is adequate to explore the deep Paleozoic play identified in the survey. Mobilisation from Brazil is due to commence during February and is estimated to take two months with the first well scheduled to spud during May. At the end of January, the group should have finished analysing the seismic results and an independent audit by RPS should have been completed, that will hopefully confirm the presence of about 500 mmboe of risked prospective resource.

In Argentina the frack programme on the PE-7 and DP-1001 wells has stabilised field production at 415 bopd, an increase of 40%. PE-7 is averaging 185 gross barrels of fluid a day whilst DP-1001 is averaging 110 gross barrels a day. The PE-8 well encountered some technical problems. A workover was carried out and a beam pump installed which produced 200 gross barrels of fluid a day. Subsequent to this, however, the pump performance started dropping off before failing entirely. It is thought that this is due to seal damage from some low level of sand production. The well is therefore currently shut-in awaiting a pulling operation to change the pump seals. Current realised oil prices increased to $76/bbl, an increase of 13% on a year ago. In Louisiana, production remained strong with monthly production of about 250 boepd. Oil prices remained firm at $109 per barrel and the group now intend to drill two new exploration wells in the area.

On 10th January, the group announced a proposed farm-in for the Chaco region of Paraguay. It as been offered an option of up to 80% participation interest in the Hernandarias block in the Chaco region. The group will fund the first $17M of a work programme including one well drilled to test the Devonian at any time within the three year exploration phase of the concession contract. The block covers an area of 18,500km2 and is located immediately North of the existing Pirity and Demattei concessions. President will retain the entire block of 18,500km2 for one year, reducing to 8000km thereafter. The block is of interest because it contains the same Paleozoic play that has delivered significant reserves in numerous giant field in the Andean mountain front of adjacent Argentina and Bolivia. The Andean front structures die out before the basin reaches Paraguay but the Paleozoic play system becomes highly structured into numerous large rotated fault blocks in the Hernandarias system, which is unique to the Paraguay concession (in this area). The group hope to commence acquisition of seismic data with a view to drilling the first Paleozoic structural test within the three year work programme period.

On the 24th January the group released a statement covering the new independent audit of the Paraguay resources. The audit covers the three drilling prospects that are being targeted in 2014. In total, there are 647 mmboe of unrisked prospective resources attributable to President and 130 mmboe risked resources. The success rate outcomes attributed to President are $11.7BN unrisked and $2.4NB risked. There are also over 20 prospects yet to be evaluated. The three drilling targets are the Jacaranda prospect, the Tapir prospect and the Yacare prospect with the Jacaranda containing the largest total quantities, followed by Tapir and with Yacare having quite modest potential.

Within Jacaranda the large structural prospect is developed within the tilted fault block domain along with the North West flank of the Pirity rift basin and contains two petroleum systems with several play types. Prospective resources have been attributed to four independent sandstone reservoirs that can be tested with one vertical well (both Cretaceous and Paleozoic sections are found there). In the Cretaceous zone the targets are likely to be oil in the Lecho sand and a wet gas in the underlying Pirgua sand. In the Paleozoic, prospective sandstone reservoir targets are developed within the Carboniferous and Devonian and are most likely to contain wet gas.

The Jurumi complex comprises five four way dip prospects in the Cretaceous Lecho reservoir. The audit covered the Cretaceous reservoir in only three prospects and for the Paleozoic section only in the Tapir drilling location within the complex. As in the Jacaranda prospect, the Paleozoic targets are considered to be most likely wet gas. The group believes that upon completion of seismic studies, further significant prospective resources within the Jurumi complex will be identified. The Yacare prospect is a four way dip closure with prospective resources contained in the Cretaceous Lecho sand and is expected to be oil. Seismic depth migration is still ongoing and the prospect size here cannot be reliably estimated until the work is complete.

On the 6th February, the group announced a placing of shares to institutional and other shareholders. In total, $50M was raised in the placing to institutional shareholders and the new shares represent just under 29% of the share capital before the placing. There was also an open offer to the group’s existing shareholders to raise a further $6.7M.

On the 24th February the results of the placing and open offer were revealed. Only 11.9% of the open offer shares were taken up but, along with the placing, the exercise raised $50.8M. Some of the shares were taken up by the IFC and they now control 13.5% of the capital.

On the 26th February, Chairman Peter Levine purchased over 390,000 shares to take his holding in the company to 19.32%. A few other board members also made some smaller purchases. I do like to see long standing board members dipping into their own pockets for shares in their company.

On the 24th March the group announced that it the mobilisation of the rig contracted from Brazil had taken place. The first well will be drilled on the Jacaranda prospect, and will target multiple horizons – it is scheduled to spud by the end of May.

On the 30th April the group released a statement covering their acreage in Australia. They have recently comissioned comprehensive seismic data and and re-interpreted some existing 3D data on the PEL82 license. It has been ascertained that in addition to the conventional play, a previously unidentified new unconventional play exists in PEL82 with gross prospective resources on a best case basis of 904 Bcf. This report has re-energised ongoing discussions to find industry participation for further activity. In order to do this, the license has been extended to September 2015. This is an interesting development. Paraguay is clearly the focus but if the group can get some real value from these new resources in Australia then it would be a bonus.