Glaxo have now released their full year results for the year ending 2013.

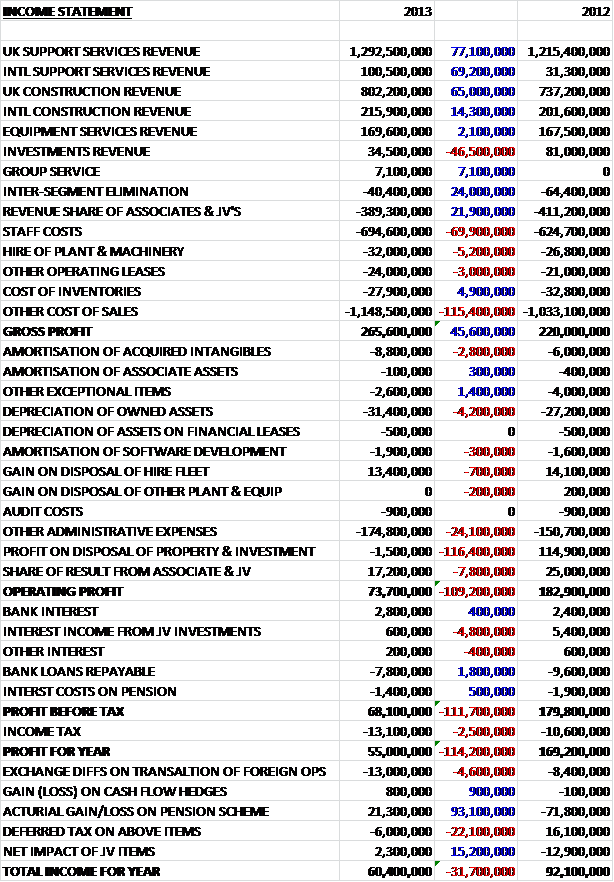

Overall, revenues were up £74M to 26.505BN. The main drivers for the increased revenue were respiratory, oncology, vaccines and immune-inflamatory products which were all up by about £100M or more. These were mitigated by falls in cardiovascular & urogenital, down £192M; central nervous system, down £187M and total wellness consumer products, down £122M. Cost of sales also increased, with a £439M hike in the cost of inventories to give a gross profit down by some £586M. Overall, Admin costs fell slightly despite a large increase in staff costs. Impairment costs increased, mainly as a result of impairments to Lovaza due to increased generic competition. We also saw a £106M decrease in R&D costs and an £81M increase in royalty income. When compared to last year there was £752M more allocated to gains on the disposal of businesses, driven by a £1.057BN gain on the sale of Lucozade and Ribena; and a £274M gain on the disposal of the anti-coagulant business, somewhat mitigated by the lack of a £349M gain on the acquisition of a joint venture and a £233M gain on the settlement of collaborations on acquisition. In total, these gave rise to an operating profit of £7.028BN, £272M less than in 2012. This was reversed, however, by a £282M profit on the disposal of an interest in an associate which, along with some other minor differences from last year, gave rise to a profit before tax just £47M higher than in 2012. A far lower tax bill, due in part to the recognition of US R&D tax credits, however, meant that the total profit for the year was up £950M to £5.628BN. A decent headline figure, but clearly not indicative of underlying trading.

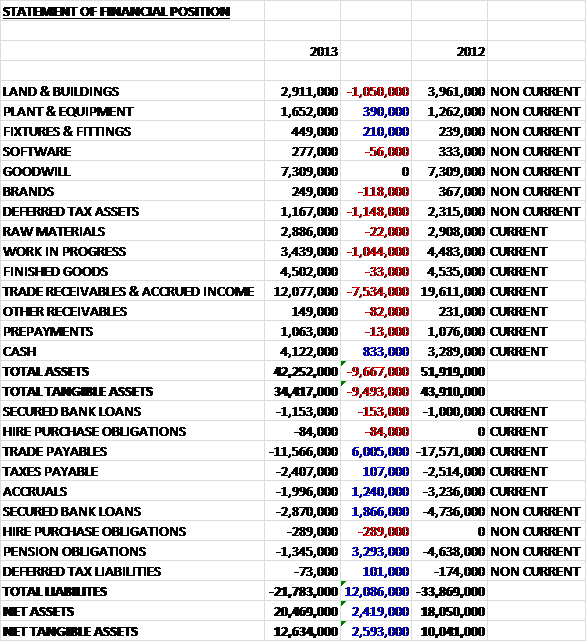

By the end of 2013, total assets increased by £605M over the figure last year. There were a number of drivers of this asset growth, the largest being a £1.35BN increase in cash levels. Other large increases included £575M more of assets under construction; £415M extra included in “other” investments, relating predominantly to an £83M further investment in Theravance Inc and a £212M increase in the fair value of current investments in the group; £349M more of other receivables which is money due in from Aspen relating to inventory and the manufacturing site; and a £206M bonus in the pension scheme surplus after a restructuring of the US post-retirement medical obligations. Not all assets increased however, and we see a £877M reduction in the value of licences and patents and a £345M fall in the value of plant and equipment due to the disposals; a £307M fall in deferred tax assets and a £256M reduction in investments in associates relating to the sale of part of their holding in Aspen.

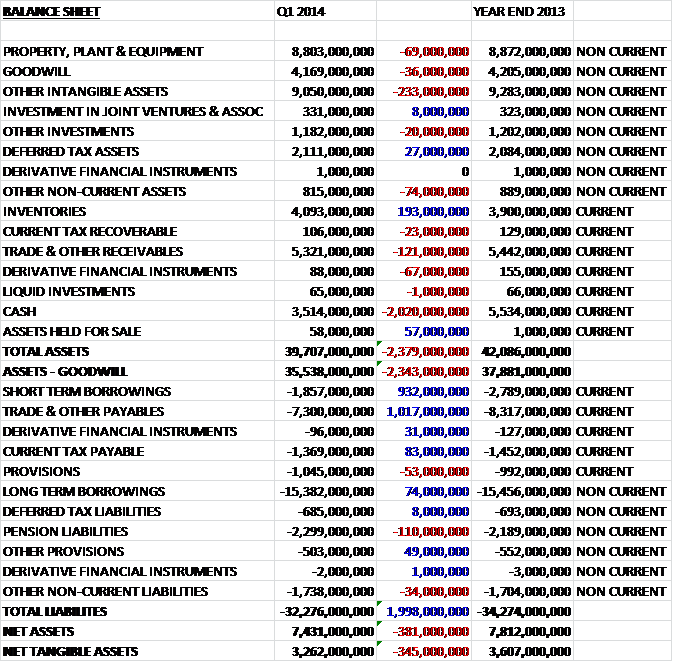

As well as assets increasing in value, we also saw liabilities falling. The main drivers for this fall were the £932M improvement in pension liabilities and a £311M fall in deferred tax liabilities. The only major increase in liabilities was a £244M hike in “other” payables, which includes £620M to be paid to shareholders in GSK Pharmaceuticals in India when they buy them out and £253M in contingent consideration relating to the purchase of the 50% share of Shinonogi ViiV Healthcare joint venture. A smaller increase in provisions due to product liability cases involving Paxil, Poligrip and a few others was also recorded. This all meant that net assets, not including goodwill movements, were higher by the tune of £1.229BN at £3.607BN.

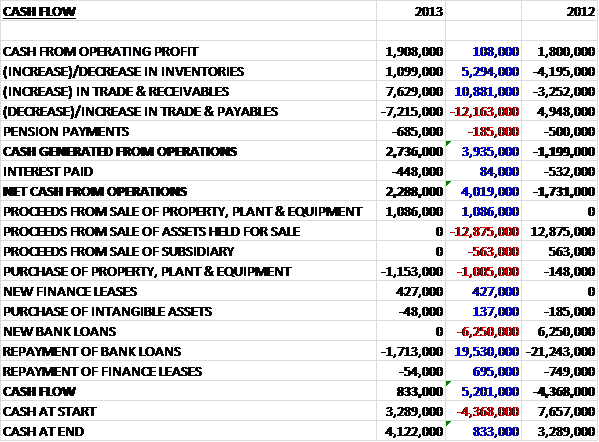

Before movements in working capital, operating cash flows were some £2.732BN higher than in 2012. An increase in receivables and inventories were counteracted by an increase in payables which meant that cash from operations was £2.451BN higher at just under £8.5BN, a pretty impressive performance. After tax, this figure came down to £7.222BN. The group spent slightly more on capital expenditure than last year and the lack of a disposal of intangible assets was counteracted by a £1.851BN cash injection from the sale of a business and the £429M proceeds from the sale of a subsidiary. An increase in loans was almost entirely mitigated by the payment of other loans but the largest cash expenses was a £919M net purchase of their own shares and £3.68BN paid out in dividends, which was slightly lower than in 2012 due to there being less shares in circulation. There was also a £749M interest bill and £588M spent on the purchase of non-controlling interests. All in all there was a cash inflow of £1.473BN compared to an outflow of £1.607BN last time. This cash flow, although pleasing, was entirely attributable to the business disposals.

The group is continuing with major restructuring, particularly after the acquisitions of Human Genome Sciences and Stiefel Labs. In total £517M of restructuring costs were included, including restructuring the European pharmaceuticals business with staff reductions in the sales force and admin; projects to simplify processes in the core business services, leading to staff reductions in support functions; the transformation of the manufacturing and vaccines business to improve productivity and costs; and the rationalisation of the consumer healthcare business. So far, the restructuring programme has made annual savings of a remarkable £3BN (in one case the group had 360 different packs of certain drug which has now been simplified). By 2016, the group expect to make a further £900M of annual savings. The integration of the Genome Sciences business has produced annual savings of £130M. The pension scheme is also getting some attention and the group has reached an agreement to make additional payments to bring the deficit down.

As usual, there were a number of acquisitions during the year. These businesses included Akairos AG, a European based biopharmaceutical company focused on the development of vaccine technology. The total purchase price was £255M, including £1M of contingent consideration and this included £53M of Goodwill paid. The group came with early stage assets for respiratory syncytial virus, hepatitis C, malaria, TB, ebola and HIV. There were also a number of disposals during the year. Lucozade and Ribena, including the manufacturing site and inventory were sold to Suntory Beverage and Food for a cash consideration of £1.352M. The Anti-coagulant business, including the IP rights of Fraxiparine and Arixtra, together with inventory and the manufacturing site was sold for £732M, of which £499M was received in cash with the rest being deferred to 2014. The group also sold 1/3 of its holding in Aspen (an associate), representing 6.2% of the share capital for £429M in cash. The group also increased its shareholding of joint ventures. The shareholding in GSK Consumer Healthcare India was increased from 43.2% to 72.5% for £588M and the holding in GSK Pharmaceuticals India was increased from 50.7% to 75% for £620M.

As would be expected, the group is involved in a number of legal proceedings, including intellectual property proceedings; product liabilities, mainly involving Adandia, Paxil and Poligrip; sales and marketing regulation, with the ongoing Chinese investigation having a big effect on business there, the third party payer litigation in the States where a number of US healthcare insurers filed a suit against the group seeking compensation for drugs they allege were adulterated and illegally marketed and an OFT investigation relating to a potential lack of competition in the industry. The Chinese problem I think is one that has worried the group as this is a key emerging market for them. As such, they have implemented their own legal investigation of the Chinese operations to root out any issues. The legal charges this year came to £252M, a reduction from the £436M that occurred in 2012. The charges were principally related to existing product liability matters.

Five new medicines were approved during the year. Those include Breo Ellipta, that was approved in the US for the treatment of COPD and Asthma in Japan; Anoro, which was also approved to treat COPD in the US; Tafinlar, in the US and Europe and Mekinist in the US for melanoma; and Tivicay for HIV in Europe and the US. Another medicine, Albiglutide, is due for a decision in the first half of 2014. The group also launched a new flu vaccine, Flulaval in the US and Fluarix in Europe. Files were submitted in the US and Europe for Albiglutide, a treatment for type 2 diabetes; a single tablet combination of Tivicay and Kivexa for the treatment of HIV; Arzerra as a first line treatment for chronic lymphocytic leukemia; and Umeclidinium, a component of Anoro for COPD. In the US on its own, the group submitted files for Fluticasone fuorate as a monotherapy for Asthma and in Europe, files were submitted Votrient for Ovarian cancer. The group are also expecting decisions in Europe in 2014 on Anoro Ellipta, Incruse, Mekinist and Mekinist/Tafinlar.

Phase 3 data was produced for a number of medicines. Data for the new malaria vaccine showed that it almost halved the number of children who developed the disease and the group are intending to submit a file in 2014. Data for darapladib in chronic coronary heart disease and mage-a3 in melanoma showed that the primary end points were not met in both cases and the group is looking to see whether either can be useful to any sub-groups of patients. They are still waiting for the results of darapladib in acute coronary syndrome and mage-a3 in lung cancer. Rights were handed back to partner companies for four assets during the year. IPX066 for Parkinson’s was handed back to Impax due to delays in regulatory approval and launch dates; migalastat in Fabry disease was handed back to Amicus, vercirnon in Crohn’s disease to Chemocentryx and drisapersen in Duchenne muscular dystrophy to Prosensa, all for disappointing phase 3 data. The group also decided not to pursue development of Tykerb in head and neck cancer and gastric cancer after studies failed to meet primary end points. During 2014/2015 the group is expecting to receive phase 3 data for six assets and phase 3 will start in 10 more.

In consumer healthcare, the group launched NiQuitin Strips, the only oral stop smoking aid in the form of strips and is designed for light smokers. Studies showed it relieved the urge to smoke within 50 seconds and the product has already been launched in 3 markets. In the US, the group introduced Sensodyne Repair and Protect. The product builds a layer over the vulnerable areas of teeth to help protect from pain and has not been used previously because of stability issues in water, which have now been overcome. Women’s Horlicks was launched in the Indian subcontinent and is the first health drink for women in the region that provides 100% of the macronutrients recommended by the WHO.

India seems to be a country that the group is investing in heavily, having increased its stake in the subsidiary and announcing plans to build a new manufacturing facility there. The US has recently enacted legislation designed to speed up development and approval of novel medicines for high priority conditions. Also in the US, rebates that are paid by pharmaceutical companies have been increased, and it is thought this will increase access to prescribed medicines in the country. Similarly in Europe, there is a potential new legislation coming into effect in 2016 that should simplify the regulation and approval process but austerity programmes in many European governments continue to put pressure in prices. In Japan, a roadmap has been produced that tries to align their governing body more closely to other regulators around the world, which again, should simplify processes. In emerging markets the focus is on allowing greater access to medicines which will improve demand but could also impact pricing. The BRIC countries for example are all looking at managing costs through pricing controls.

Respiratory is the group’s most important segment. Overall sales grew by 4% with the US up 7%, Europe down 3%, emerging markets up 4% (9% not including China) and Japan increasing by 9%. Sales of Seretide/Advair were up 4%, largely due to the strong US performance; sales of flixotide/flovent were up 2%, Ventolin up 2% and Xyzal, with sales mostly made in Japan, up 26% to £137M. The launch of Breo Ellipta in Q4 gave sales of £5M. The hit to European turnover was due to increased competition in many of the markets with Serevent sales the worst hit, down 17%. In Japan, the growth was driven by Xyzal and Veramyst whilst Relvar Ellipta, launched in December, had revenues of £3M.

Sales of anti-virals declined by 6%, mainly due to lower sales of Zeffix and Hepsera in China. It was not a good year for CNS sales. Seroxat/Paxil revenue fell 16% due to generic competition in Europe and Japan, Requip sales fell 18% due to generic competition in Europe and the US and Lamical turnover fell by 7%. Cardiovascular sales fell by 8%, primarily due to the impact of the conclusion of the Vesicare co-promotion agreement. Discounting this, sales fell by just 1% as increased Avodart sales were counteracted by reduced Lovaza and Arixtra sales. The increase in metabolic revenue was driven by higher sales of Prolia in Europe and Emerging markets. In anti-bacterials, Augmentin revenue increased by 5% to £630M with strong growth in emerging markets partly driven by the comparison with the supply issues in 2012.

The increase in Oncology revenue was very strong. US sales were up 17% with a strong performance from Votrient (up 56%), Promacta and Arzerra and also benefited from the launch of Tafinlar and Mekinist for Melanoma in Q2 which contributed £21M. Revenues in Europe grew by 28% and emerging market sales increased by 18% with Votrient up by an incredible 80% to £331M as it continued to build market share in many markets and a number of others increased slightly but were somewhat counteracted by a fall in Tykerb/Tyverb sales due to increased competition. Revolade received approval in Europe for use in thrombocytopenia associated with Hepatitis C and Tafinlar was launched in Q3 in certain markets and has experienced strong up take.

Dermatology revenues fell by 8% due to US sales falling by 40% as many of the treatments there continued to suffer from generic competition and the disposal of a number of brands took effect. Emerging market sales were up 6% reflecting growth in Bactroban, Dermovate and Duac, particularly in the Middle East, Africa and Latin America. European sales increased by 5%. Rare Diseases increased by 7%, driven by hikes in the sales of Volibris (21%) and Merpon (8%). Counteracting those increases was a 16% fall in Flolan due to the biennial price reduction in Japan and continued generic competition in the US and Europe. ViiV healthcare revenues were flat year on year as an increase in US sales was counteracted by falls in Europe and emerging markets. Epzicom/Kivexa sales were up 14% to £763M and Selzentry was up 10% during the year. Tivcay recorded sales of £19M from the early stages of its launch in the US, which started in August. Tivcay was approved in Europe at the start of 2014 and launches are planned in several markets through the year. The growth in these drugs was mitigated by declines in Combivir, which was down 36%.

Although vaccine sales were only up 2%, the performance improved towards the end of the year with a significant increase in tender sales in Q4. The growth is attributable to the increased sales of Infanrix, Fluarix/Flulaval and Boostrix which were counteracted by the decline of Cervarix in Japan (down 37%), reflecting the suspension of the recommendations for the use of HPV vaccines in the country and a strong performance in 2012. Infanrix sales were up 9% to £862M, with the growth reflecting stronger tender shipments in Europe and emerging markets plus the benefit in the US of a competitor supply shortage. Boostrix also benefited from this supply shortage and increased sales by 19% to £288M. Sales of hepatitis vaccines fell 4% to £629M reflecting lower sales in the US as a result of the return of competing vaccines to the market in the second half of the year. Synflorix increased by 2% to £405M aided by strong tender sales in the Middle East, Africa and Latin America. Rotarix sales increased by 5% with strong growth in the Middle East, Africa and Europe partially offset by the impact of increased competition in Japan. Fluarix/Flulaval sales grew by 25% following the launch of the Quadrivalent formulation in the US.

In consumer healthcare, total wellness sales, excluding the disposed brands, grew by 1% as increased sales of alli in the US and Europe, along with a severe cold and flu season was partially offset by a 57% fall of Contac in China, due to new shelving requirements, and Fenbid, down 31% in advance of mandatory price reductions. The strong growth in oral care was led by Sensodyne Sensitivity and Acid erosion, up 15% and denture care brands, up 9% which was only partially counteracted by a 12% decline in Aquafresh sales. Nutrition sales grew by 7% with strong growth in emerging markets, particularly for Horlicks which was up 14% and Boost in the Indian Subcontinent. Skin health sales were up 5%, led by Abreva in the US. Geographically US sales were up 2% with strong performances by alli, Abreva and the oral health brands counteracted by declines in Gastro-intestinal products due to increased competition, and smoking control products which were impacted by supply disruptions. In Europe sales grew 3% due to a strong performance from alli and respiratory health and pain products. Rest of the world markets grew by 6% as a strong performance from India was offset by a 23% reduction of sales in China.

One interesting project that the group is involved in is work with the Biomedical Advanced Research and Development Authority to tackle the threat of bioterrorism in the US. They have supplied their inhalation anthrax treatment, raxibacumab to the Department of Health and Human Services. The contract is worth $196M over four years.

Overall this has been a pretty decent year operationally. Although profits before tax were broadly flat, eps has increased due to the share buy-back campaign. Operational cash flows were very strong and the group is building its presence in India, which seems a good move. The issues in China seem to be ongoing but other emerging markets are picking up the slack. There were a good number of new treatments developed during the year, with a smaller number still to receive approval this year. Net debt at the end of 2013 stood at £12.645BN which was an improvement of £1.392 over the end point of last year and can be explained by the receipts from the disposals. At the current share price, the P/E ratio is 14.2 but this is expected to increase slightly to 14.7 next year as analysts expect a small reduction in income. The dividend yield is now 4.8%, which is a decent income and is covered about 1.5 times by earnings. I am happy to continue holding here.

On 20th February the group announced that the European Medicines Agency issued a positive opinion regarding umecidinium (under the brand name Incruse) as a once daily maintenance treatment to relieve symptoms in adult patients with COPD. This is not a final decision from the European commission but a good step in the right direction. The EC are expected to make their final decision in Q2 2014. GSK also submitted a similar drug for consideration by the Food and Drug Administration in the US and are still waiting for a decision.

Also on the 20th February the group announced that the EMA had also issued a positive opinion recommending marketing authorisation for uneclidinium/vilanterol under the brand name Anoro, a once daily maintenance bronchodilator treatment to relieve symptoms in adult patients with COPD.

On the 10th March the group announced that it has increased its stake in its Indian subsidiary from 51% to 75%, although it will remain publically listed. The shares were acquired for the price of £625M.

On the 12th March the group announced that a phase 3 study of Mepolizumab met its primary end point of reduction in the frequency of exacerbations in patients with severe eosinophilic asthma. This is the first potential non-inhaled treatment for severe asthma and the group will be progressing towards global filings at the end of the year. This is a new drug, not approved anywhere in the world so has some good potential.

On the 20th March the group announced that a phase 3 trial for MAGE-A3, a cancer immunotherapeutic in non-small cell lung cancer, did not meets its first or second endpoints as it did not significantly extend disease-free survival when compared to a placebo. For now, the trial will be continued I order to assess the third potential endpoint, that there may be a sub-population of patients who may benefit but the results will not be released until 2015.

On the 26th March the group announced that it has withdrawn its application to the EMA for the use of Mekinist in combination with the previously approved Tafinlar for the treatment of adults with metastatic melanoma with a specific mutation. The panel concluded that the data provided by GSK did not show a conclusive positive benefit-risk balance. The phase three study is still ongoing and the group plan to resubmit when more data is revealed. Interestingly the combination is already approved in the US and Australia, and also on its own in Canada. Mekinist as a single treatment is still under consideration by the EMA. This was quite disappointing news but does sound like just a blip rather than anything else.

On the 26th March the group announced that the European commission has granted authorisation for its once-weekly diabetes treatment Eperzan. The drug is indicated for the treatment of type 2 diabetes in adults to improve glucose control. The group expects to launch the product in several European countries in Q3 or Q4 2014 with additional launches to follow. The drug is also currently under review by the US FDA.

On the 30th March the group revealed data from a stage 3 study of darapladib in patients with coronary heart disease. The trials did not meet the specified end point but the group seem to be intent on finding patients who may benefit from treatment and more studies seem to be ongoing.

On the 2nd April the group announced its decision to stop the phase 3 trial of its MAGE-A3 cancer immunotherapeutic after it was established that there was no sub-population of patients that would benefit from the treatment. The group is continuing a phase 3 clinical study to determine whether a sub-population of melanoma patients that would benefit from the treatment, with the outcome expected in 2015. Given the failure of this particular drug in the past, I am not too hopeful.

On the 15th April the group announced that the FDA has approved Tanzeum as a once-weekly treatment for type 2 diabetes. Following the approval, GSK are planning to launch the product in the US in Q3 2014. The same drug was approved in Europe in March under the brand name Eperzan.

On the 17th April the group announced that Incruse Ellipta has received market authorisation in Canada for the long-term once-daily maintenance bronchodilator treatment of airflow obstruction in patients with COPD. This is the first market authorisation of this drug anywhere in the world and GSK are looking to push through into other markets.

On 22 April the group announced a tie up with Swiss pharma company Novartis. The crux of the deal involves a new joint venture consumer healthcare business involving the brands from both companies whereby Glaxo will retain a 63.5% stake. GSK will acquire Novartis’ vaccine business, excluding the flu vaccines for some reason, for an initial cash consideration of $5.25BN with a potential for subsequent milestone payments up to $1.8BN and ongoing royalties. GSK will sell their Oncology business to Novartis for a cash consideration of $16BN, $1.5BN of which depends on the results of the COMBI-d trial. GSK shareholders will receive $4BN capital return funded by the net cash transaction proceeds to be delivered by a B share scheme. This transaction is expected to be completed during the first half of 2015 subject to the relevant approvals.

The new joint venture will trade under the GSK Consumer Healthcare name and be active in all territories except Nigeria and India where GSK will continue to hold directly its interests in its listed subsidiaries. It should be noted that there have been issues as Novartis’ facility in Nebraska, that will be part of the assets owned by the joint venture. There have been manufacturing issues and at this time it is apparently not possible to determine when the site will resume full operation.

The acquisition of the vaccines business will benefit the group with the addition of Bexsero, a new vaccine for the prevention of Meningitis B and will also strengthen the manufacturing network and improve supply costs. Novartis has traditionally been fairly week in emerging markets, so GSK’s expertise here should open up new markets for their vaccines. There are a number of different vaccines in the pipeline, including ones for hospital infections and TB. Of the supply and chain and manufacturing sites included in the transaction are packaging facilities in Italy and Germany, along with manufacturing sites in India and China. As part of the acquisition there are a number of contingent payments relating to certain milestones. $450M is payable upon FDA regulatory approval for the MenABCWY vaccine, $450M is payable in the event that Bexsero achieves an egreed net sales threshold (not idea what that threshold might be), $450M upon an agreed milestone relating to ACIP regulatory recommendations in respect of MenABCWY or Bexsero, and $450M upon achievement of an agreed milestone relating to ACIP regulatory recommendations for the Group B Streptococcus vaccine. There are also 10% annual royalty payments on certain net sales of the above products.

The proposed transaction will fundamentally change the revenue structure and increase revenues by $1.3BN a year with 70% of revenues received from either respiratory, HIV, Vaccines or consumer healthcare. The board also expect to find £1BN of cost savings per annum by 2020 which will cost about £2BN to achieve, with only half that being cash costs. GSK’s late stage pipeline will receive four new candidate medicines from Novartis. The Consumer Healthcare combinations seems complimentary with regards to geographical presence with Novartis currently under exposed to emerging markets but strong in Central and Eastern Europe, in contrast to GSK. The board of the new group will consist of Novartis and GSK executives with Sir Andrew Witty becoming chairman.

All of these deals are dependent on each other for the go-ahead and none will happen if one of them does not as things currently stand. The group expects the general meeting to discuss the deal to go ahead in Q4 2014 with the transaction being anticipated to take place in H1 2015. In all, this seems like a decent deal for GSK. The extra revenues and cost savings do look good, although the royalty payments and any other payments should some of Novartis’ drugs be successful look a little steep. The Oncology business does seem to have been struggling of late and I think it will probably be a good thing for GSK to focus on its more successful areas going forward.

On the 28th April the group announced that the European Commission has granted marketing authorisation for Incruse as a once-daily bronchodilator treatment to relieve symptoms in adults with COPD. It is now licensed across all EU states and it is expected that the first launch will take place in Europe by the end of 2014. This particular drug is also licensed in Canada and is currently under review in the US and several other countries.

On the 30th April the group announced that the US FDA has approved Ellipta as an anticholinergic for the long-term maintenance treatment of COPD. It is thought that the drug will be launched in the US during Q4 2014. So, this is now approved in the EU, the US and Canada. There are still a number of other countries still considering the drug.

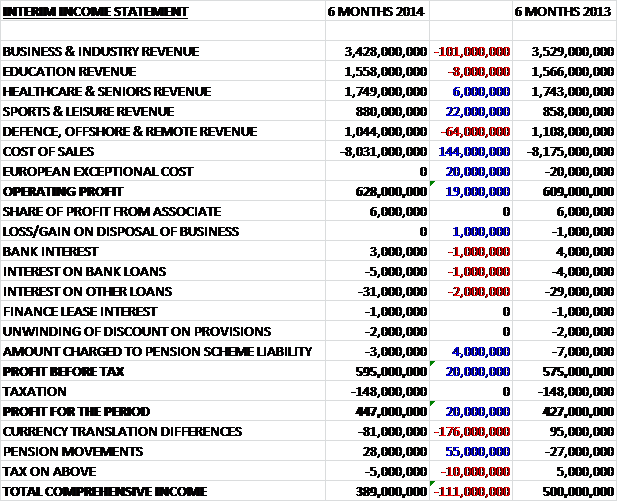

GSK have now released their results for Q1 2014.

In Q1 revenues fell pretty much across the board with European sales the only one not to show a decline. US revenues fell by £212M, consumer healthcare fell by £124M and there was the lack of £216M of discontinued revenue. Cost of sales also fell, however, and were some £233M lower. General costs were also some £109M lower and a lower R&D cost, due to the end of some large projects was counteracted by a similar fall in royalty income after the conclusion of a number of agreements. Share of profits from associates fell to just £1M due to the reduction in the shareholding in Aspen. This meant that the operating profit for the first quarter of the year was down by nearly half a billion pounds. A smaller tax bill, however, meant that profit for the period was £310M lower than in Q1 2013 at £719M.

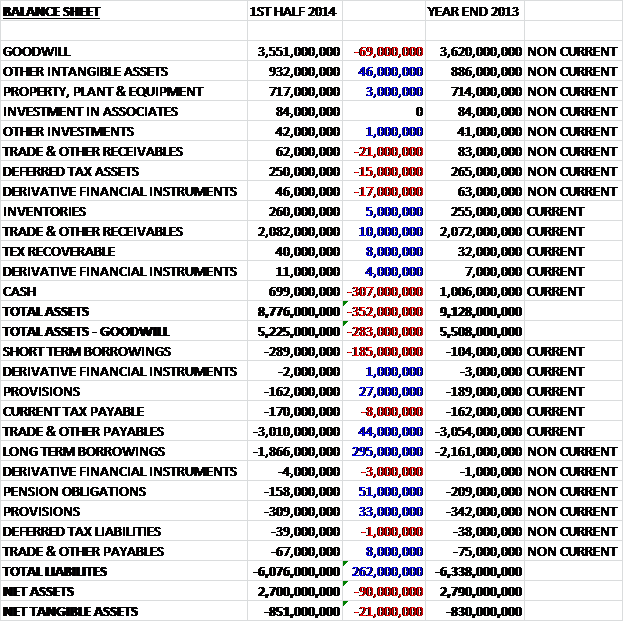

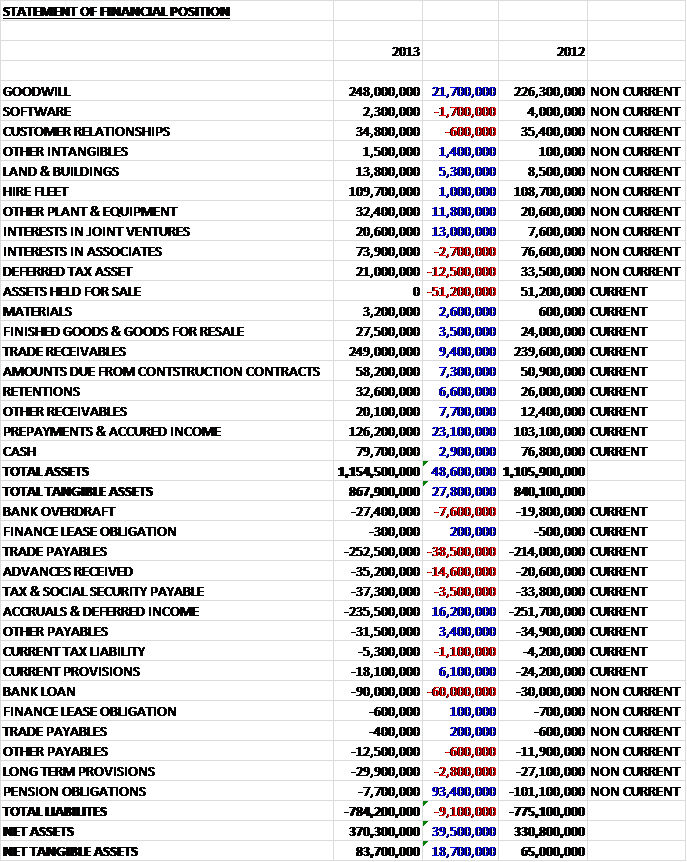

When compared to the end point of last year, assets at the end of Q1 were £2.379BN lower. This was predominantly driven by a £2.020BN reduction in the cash levels. Other reductions included intangible assets, down £233M due to the increased amortisation of Lovaza and some minor R&D write-offs; and receivables, down £121M. These were only partially mitigated by a £193M increase in inventories. Likewise, liabilities were also lower, driven by a £1BN fall in payables and a similar £1BN fall in borrowings, only partially mitigated by a £110M increase in pension liabilities due to a decrease in the rates use to discount pension liabilities. Net assets were £381M lower and once the big chunk of goodwill is taken off, net assets were lower by £345M at £3.262BN which was a little disappointing.

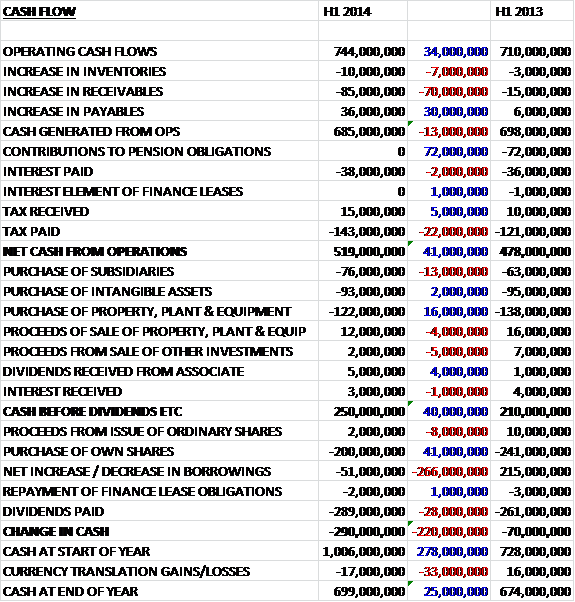

Before movements in working capital, cash profits in Q1 were £391M lower than in Q1 last year. This was predominantly put down to adverse currency movements. Working capital increased at a smaller rate than in 2013 and after tax, net cash from operations was £927M, down some £320M. The group then spent £201M on tangible assets and £148M on intangibles, up by £66M which meant that cash before financing was £593M, down by £356M. The bulk of the rest of the cash was then spent on the purchase of shares in their associate, relating to the Indian and Indonesian subsidiaries (£669M), the repayment of loans (£894M) and dividends (£910M). After all this, the group had a cash outflow of nearly £2BN, which meant that the group had £3.233BN of cash at the end of the period.

Seretide/Advair is still the most important drug, contributing just over £1BN in sales, and over a fifth of the total with the next most important a distant second – the vaccine infanrix contributed just over £200M in revenues.

The Chinese authorities are continuing to investigate the claims made previously against GSK in that country but it is not yet possible to make any estimates on the potential outcome. Legal charges as a whole increased to £108M this quarter compared to £66M in Q1 2013 due to the settlement of existing anti-trust matters and higher litigation costs.

In Q1 respiratory sales fell by 11% as Seretide was down 15%, Flixotide down 2% and a 13% decline in Xyzal sales were only slightly counteracted by a 15% increase in Ventolin revenues. In the US turnover was down 20% due to increased competition in the Advair and Breo market. Underlying sales in the country were down by 11% as a slight increase in price was counteracted by declining volumes. Breo Ellipta for COPD was launched in Q4 and sold £1M so far this year, which was lower than expected due to delays in payer coverage which has now been resolved. European respiratory sales fell by 3% due to increased competition driven by a 3% decline in seretide sales. Revlar Ellipta was approved in Europe for COPD and Asthma and recorded £2M of revenues after being launched in Q1 of this year. Respiratory sales in Emerging Markets grew by 3% despite a 12% fall in Chinese sales. Veramyst sales grew by 25% to £17M. Japanese respiratory revenues were down 3% despite a 29% increase in Adoair sales. This growth was more than offset by lower sales from the rest of the portfolio, driven by a weaker allergy season.

Oncology sales grew by an impressive 27% during the quarter. Votrient sales were up 31% and Promacta revenues were up 30% but Arzerra and Tykerb sales both fell. In the US sales grew 31% as Mekinist and Taflinar were launched in Q3 of last year. In Europe, Oncology sales were up 23% led by increased sales of Votrient. Cardiovascular revenues were up 4% as Avodart sales were up 7% and Duodart/Jalyn increased by 21%. Geographically the main drivers for growth were Japan, up 52%; Europe, up 14% and Emerging markets, increasing by 29% were somewhat mitigated by a fall in US revenue. Immuno-inflamation revenue increased by 69% with Benlystsa up 33%. Other pharmaceuticals were up 7% due to government stockpiling of Relenza in Japan, which was counteracted by a decline in Augmentin sales due to higher generic competition.

ViiV Healthcare sales increased by 4% with the US up 3%, Emerging Markets increasing by 22%, Japan up 28% and Europe falling by 2%. Epzicom/Kivexa sales increased by 12% and Tivcay was launched in the US during Q3 last year and in Europe during Q1 of this year. This growth was counteracted by a 5% fall in Selzentry sales and huge falls in Combivir and Trizivir due to generic competition. Established product turnover fell by 11% with declines across all regions led by a 17% fall in US sales. Sales of Lovaza fell by 25% due to a decline in the market and generic competition caused Seroxat to fall 15% and Malarone by 34%.

Vaccine sales were up 3% when compared to the same quarter last year. Sales in the US were up 25%, Europe turnover was up 3% and Emerging markets sales were down 8%. The increase in US sales were predominantly due to a poor Q1 2013 comparison due to CDC stockpile movements and the decrease seen in emerging markets was mainly because of the phasing of Synflorix sales. Infanrix/Perdiarix sales increased by 20% due to the US, Boostrix sales increased 41% across all markets but particularly in the US due in part to competitor supply issues. Rotarix sales were up 16% with growth driven by tender shipments in Europe and Emerging Markets. Synflorix turnover fell by 29% reflecting the phasing of tenders in Emerging Markets.

Consumer Healthcare sales were flat on Q1 last year. Sales in Europe and the US were down 4% and 10% respectively, reflecting supply issues that impacted by sales of products for smokers health and Alli. Growth in the rest of the world markets was 6% reflecting strong growth across most categories with Horlicks particularly strong in India, partly offset by a reduction in Chinese sales and a 42% fall in the sales of smoker’s health products due in part to temporary supply issues. Wellness sales were down 8% as an increase in Panadol sales was offset by the previously mentioned supply issues in smoker’s health products. Oral health sales were up 5% as strong sales in Sensodyne and denture care brands were mitigated by a decline in Aquafresh sales, partly due to more supply issues. Nutrition revenue was up 13% led by strong growth of Horlicks and Boost. Sales of Skin Care products were down 4% due to lower sales of Bactroban in China.

There are currently six new respiratory products in late stage development, including Mepoluzimab, a new treatment for severe asthma. Following positive phase 3 results the group are planning on filing the drug for approval before the end of the year. In addition, it is being investigated for use with COPD. Elsewhere, new drug Tivicay continued to show rapid prescription uptake for HIV. In vaccines, further sales growth from the new flu vaccine is expected during the second half of the year. In Oncology the newly launched MEK and BRAF mono therapies now have around a 70% combined share of prescriptions in the melanoma v600 targeted therapy in the US market. Additionally Tanzeum, a new product for type 2 diabetes is now approved in the US and Europe and it is on track to be launched in Q3 in both regions. There are also a large number of drugs due to enter phase three shortly.

The group purchased 1.7M shares during the quarter and issued a further 6.3M under employee share schemes – not sure what the point of the repurchase was in this case. Overall then, the group seemed to be struggling against a strengthening sterling during the quarter. Respiratory sales dragged down other better performing sectors and it is a bit disappointing to see that Oncology was one of the best performing sectors considering this is being sold to Novartis. It is good to see the group further pay down debt with some of the spare cash but the reduction in net assets is disappointing. Net debt at the end of the quarter stood at £13.66B which was an increase of just over £1BN when compared to the start of the year. The group declared the first interim dividend of 19p per share, an increase of 6% and at the current share price represents a decent 4.8% yield. I am happy to hold the share for income.

On the 8th May the group informed the market that they had received marketing authorisation from the EU for Anoro, a once daily treatment to relieve symptoms of COPD in adults. The first launch in Europe is expected to take place in Q2 or Q3 2014 with additional launches following afterwards. This drug has also been licensed for use in several other countries such as the US and Canada, and regulatory applications have been submitted in other countries where they are currently undergoing assessment such as Japan.

On the 13th May the group announced that in the phase 3 study with Darapladib for use with adults with acute coronary syndrome, the drug did not achieve the primary endpoint of a reduction of major coronary events verses a placibo. This is clearly disappointing that it has taken this long do discover that Darapladib is not of much use.

On the 27th May the group released a rather terse statement that it had been informed by the UK’s Serious Fraud Office that it has opened a formal criminal investigation into the group’s commercial practices. There is no further information than this, but it seems concerning.

On the 11th June the group announced positive phase 3 studies regarding the use of Incruse Ellipta or Umeclidinium in addition to Relvar/Breo Ellipta for patients with COPD and that patients had a significantly improved lung function when compared to placebo patients. This is a good bonus but is just a combination of two other drugs really.

On the 27th June the group released a statement that the CHMP issued a positive opinion recommending marketing authorisation for Triumeq for the treatment of HIV in people over 12 years old. The drug is not currently approved in any country and is the first once daily single-tablet drug for HIV.

On the 30th June, the group released a statement announcing that they have susmitted an application to the US FDA for a fixed dose combination of the inhaled corticosteroid, fluticasone furoate and the long acting beta agonist, vilanterol as a once daily treatment for asthma patients aged over 12 years under the brand name Breo Ellipta. One of the dosages has already been approved by the FDA for the long term once-daily treatment of COPD so it seems to be an application for an additional usage.