![]()

This is my Photo-Me international blog. Photo-Me provide a number of photographic products. Their main product is the photobooth, which provide people with passport sized photos. They also have Digital Printing Kiosks for the printing of digital photos, Mini Labs, Photobook machines, Coin Operated copiers and business card machines, and coin operated Amusement machines .

The operations division includes the operation of unattended vending equipment such as the photobooths, digital photo kiosks, amusement machines and business service equipment. The sales and servicing division comprises the development and manufacture, sale and after sale servicing of the vending equipment.

Photo-Me have now released their full year results, I will start with the income statement.

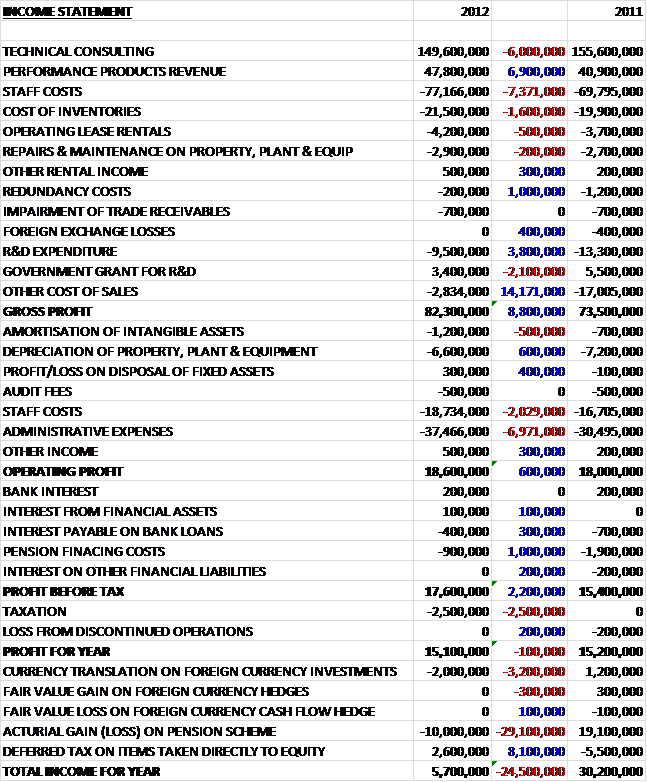

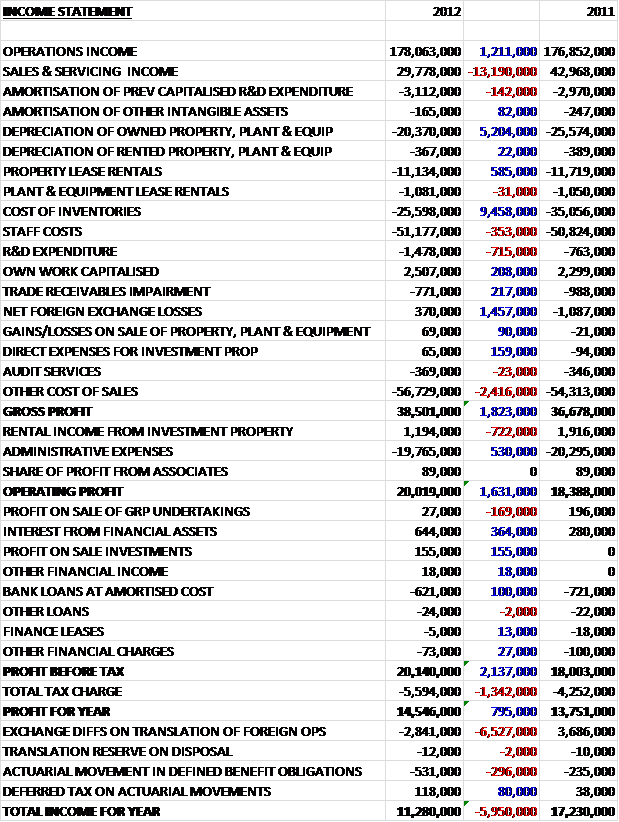

Income from the Operations division has been fairly flat, up just £1.2M to £178.1M, where increased Asian revenues counteract lower revenues from the UK and Europe businesses, but income from the Sales and Servicing division has collapsed, down £13.2M to £29.8M. Thankfully, expenses have also fallen, including nearly £10M less spent on inventories and a slight fall in property lease rents counteracted by the R&D expenditure nearly doubling. We also see a £722K fall in income from investment properties to leave the operating profit £1.6M higher at £20M. The group received operating income from the investment property of about £1M. These rights have since been sold so this will be a non-recurring income stream. That small amount of profit on the sale of group undertakings occurred due to the recycling of accumulated exchange differences through the income statement.

The group benefited from increased financial earnings, as their cash pile and investments gains some interest but a higher tax charge means that the profit for the year is only £800K higher at £14.5M.

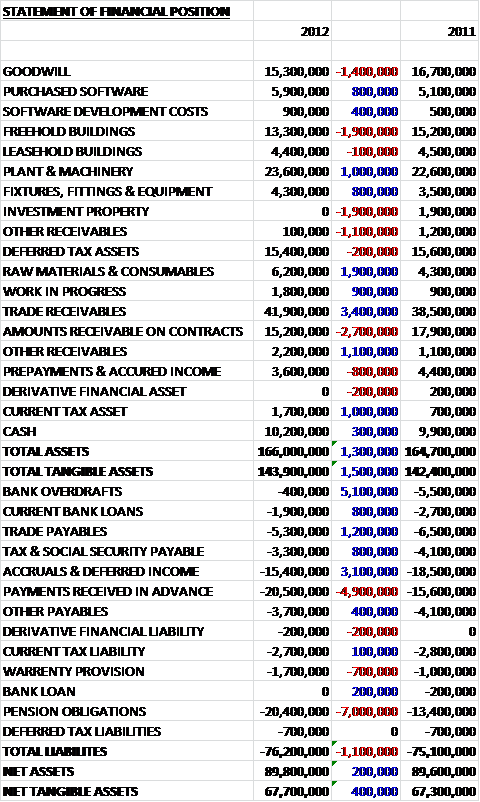

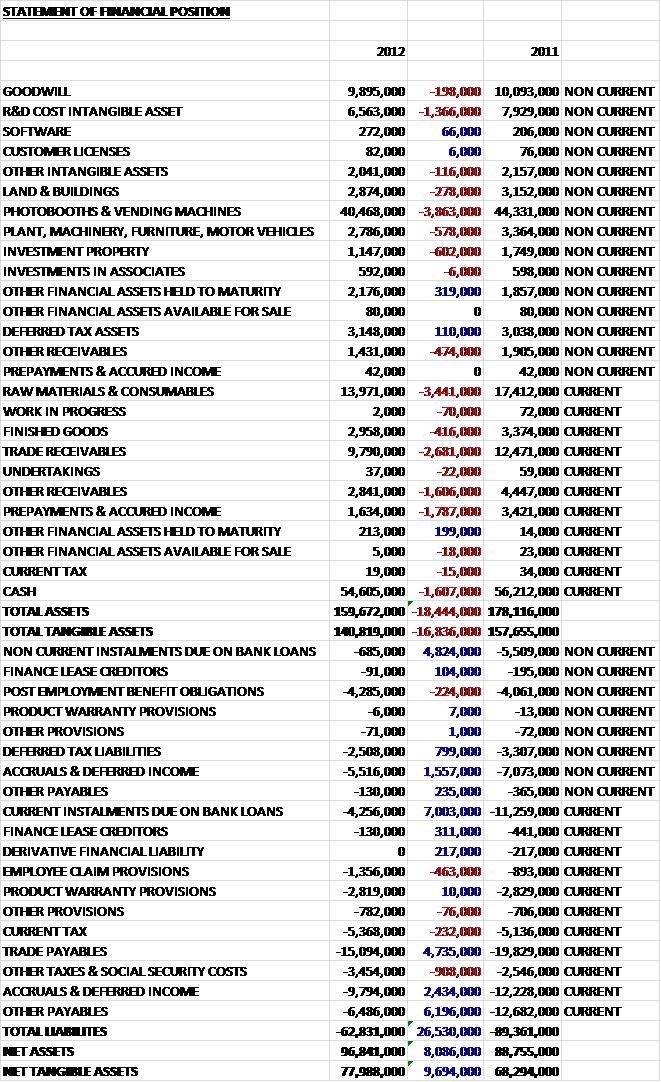

The total asset base of the group is quite a lot lower, £18.4M down at £159.7M. Almost everything has fallen in value, some of the largest falls are in Inventories, the value of the machine portolio, trade receivables (actually less than £10M, £2.7M down), £1.7M of which are overdue which seems like quite a high percentage, and a reduction in the cash level of £1.6M. This does seem a bit concerning, but I would expect the trade receivables to be low given the nature of the vending machines that the group is involved in. Those other intangible assets relate to the payments made for the right to occupy a space to site vending machines. The held to maturity financial assets are bank deposits where cash is held by the bank as security against contingent liabilities, the increase is due to agreed interest on the sale of the rental income of the Grenoble property.

Thankfully, liabilities have also fallen. They were a massive £26.5M lower at £62.8M. The largest decrease is in the instalments due on bank loans which were £11.8M lower due to the group using its positive cash flow to pay back debt – this should be reduced to zero within a year or so. We also saw a £4.7M reduction in trade payables and other payables were also down considerably. Employee related claims currently stand at £1.4M, and these have increased. They relate to claims made by former overseas employees of the group and should be met in the coming financial year. It is unclear as to the exact nature of the claims.

All the above leaves the net tangible assets nearly £10M higher at just under £78M, quite a healthy amount considering the lack of debt.

Moving on to the cash flow

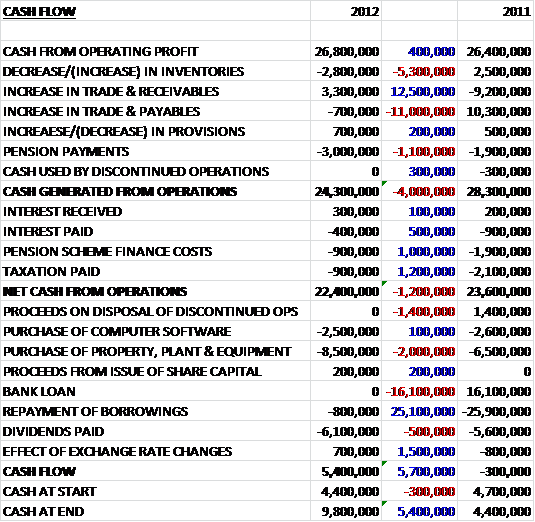

The cash obtained from the profit was a disappointing £5.7M lower, at £42M. Changes in payable/receivable management had little affect and the cash generated from operations was £42.4M. This was actually £16M less than last year due to a reduction in trade payables and the lack of the cash from the sale of the rental income which occurred in 2011. The tax bill this year was also quite a bit higher, and £3M more was paid out in tax. This meant that the net cash from operations was £36.5M, down by £18.9M.

£15.9M was spent on purchase of property, plant and equipment, which seems like a lot, but it was over £1M less than last year. The other big cash expenses were the repayment of borrowings (£11.1M) and dividends (£7.2M, an increase of £2.7M). All the above meant that the cash flow was £267K, compared to £15.1M last year. With the differences in exchange rates, the group actually lost £1.9M in cash.

When compared to last year, this performance is actually a little disappointing. However, it should be pointed out that in paying back over £11M of loans, the group still managed a small cash inflow so when this expense is taken out, that cash pile should start growing again.

The group still seem to be struggling for profitability in Sales & servicing, so further restructuring has been deemed necessary. Already, costs have been reduced by reducing stock and staff and the headcount has already been reduced by 137. Photobooth sales have been going according to plan but some other product sales have been adversely affected by the state of the economy in the group’s geographic markets.

Geographically speaking, all regions are profitable and the performance in France has been particularly good. Trading has also been good in Germany, Switzerland and Japan, where business has improved after the earthquake last year. Revenues in the UK were down due to the loss of part of the business supplying driving licence photos and a difficult economic climate. The UK operations have now been bought under control of the CEO of European activities. Progress in China has been slower than expected but the group now has operating licenses in Shanghai, Beijing and Guangzhou and this is considered a long term prospect.

The fact that photo booths are increasing is good as they are a mature, cash generative business and make up the back bone of the profits that Photo Me make. The Digital printing kiosks seem to be doing well in France and Switzerland, which is also a positive sign. The amusement rides are suffering against a poor economic outlook but the latest range of simulation type products seem to be making progress. As already mentioned, the Sale and Servicing division is having some trouble as the revenues are driven by sales to third party retailers of photographic equipment, who seem to be doing badly in the current climate and resist making big orders.

Most of the profits for the group are generated outside the UK so the group could be adversely affected by a change in exchange rates and a 10% change in exchange rates would affect profit by £974K. Most of the cash is held in Euros (21.8M) but there are also reserves held in Sterling and Yen. The group’s loan is predominantly in Euros so there is a slight natural hedge which will unravel as the group pays back more debt. Going forward, the group is somewhat susceptible to a reduction in retail site owner base that provide the base for sites for the group’s vending equipment and they could lose operations revenue streams and market for equipment in the sales and servicing activity could be reduced should any retailer go out of business. There is also a risk that governments could introduce centralised image capture for ID photos that Photo Me currently provide. Many of these risks are out of their control so it would help to me mindful of them.

The company hired a few new directors and they are now in compliance of UK Governance code with regards to independent directors (they were not last year when I reported on the results). Also, during the year, a long standing director sadly passed away. At that point he owned a lot of shares, and they are now held under the Dan David foundation, the long term intention of which I am not sure about.

Overall then, this was a fairly good set of results but not amazing. Revenues are down and the Sales and Services business seems to be faring rather badly but overall profit is up just under £1M to £14.5M. Assets are down, including trade receivables but net tangible assets are up due to the lower liabilities (mainly because the group paid back so much of the bank loan). Although not as good as last year, the cash flow is still in pretty good shape. Despite paying back £11.1M of the bank loan and an increase in dividends, there was still a small positive cash flow recorded. The photo booths are still what is keeping the group in profit and successes in other products seem to be somewhat lacking but a lot in being spent on R&D so hopefully something else will start to shine soon.

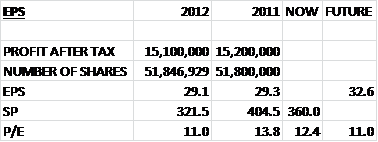

There is a lot of net cash here (nearly £50M) so at some point something will have to be done with that (maybe in the form of a shareholder reward) but a recent rally in the share price has given a P/E ratio of 17.2 so they are no longer cheap. However, with a solid net cash position and a dividend yield of 3.7% on the current share price, there are worse places to be invested. Hold