Arbuthnot Group wholly owns private bank Arbuthnot Latham and owns just over 50% of retail bank Secure Trust Bank. Arbuthnot Latham provides a private banking and wealth management service consisting of private banking that comprises of current accounts, deposit accounts, loans, overdrafts and foreign exchange. Each client deals with a dedicated private banker who provides an individual tailored service. It also includes Wealth Planning, which is built on long-term relationships and bespoke financial strategies. The service is independent and fee, not commission based with clients receiving a service covering estate and tax planning, pensions and wealth preservation and generation. The discretionary investment management service comprises asset management, developing tailored investment strategies to ensure that each client’s specific investment objectives are met.

Secure Trust Bank is a UK retail bank and its core business is to provide banking services including a range of lending solutions and deposits. It also provides fee-based current accounts to UK customers who may not be well served by other banks. Consumer Finance offers its customers lending in the areas of motor finance, retail finance and unsecured personal lending. Business Finance provides SME’s funding for asset finance, invoice finance and real estate finance. The current account includes a prepaid card and charges a monthly fee of £12.50 with customers being able to earn rewards at participating retailers. Finally, the savings offering is a combination of instant access accounts, notice deposits and deposit bonds. The company has now released its final results for the year ending 2014.

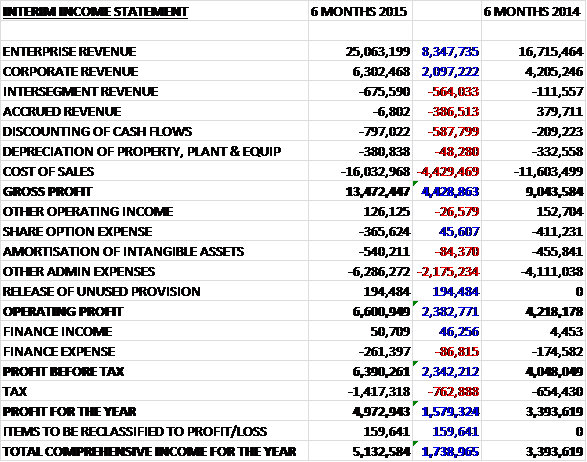

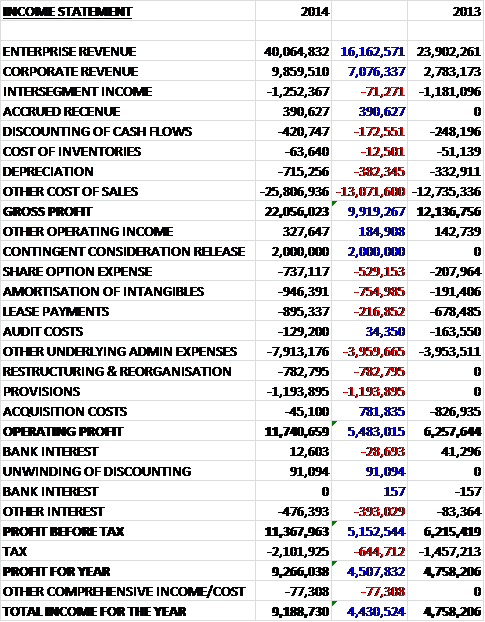

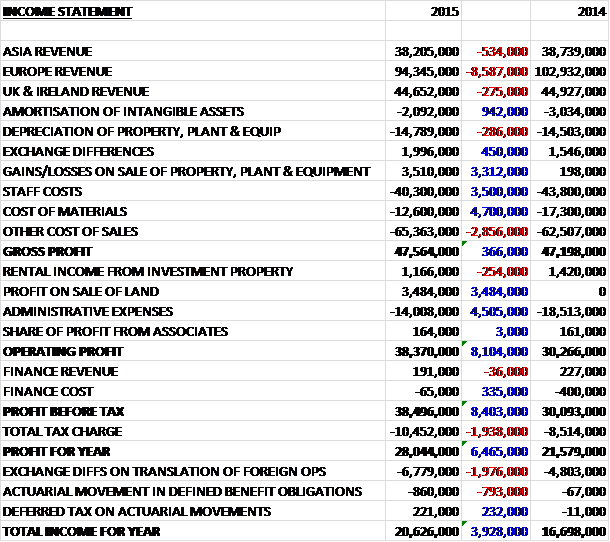

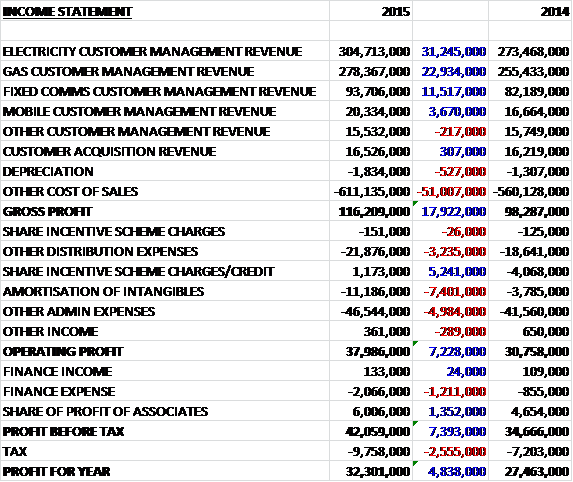

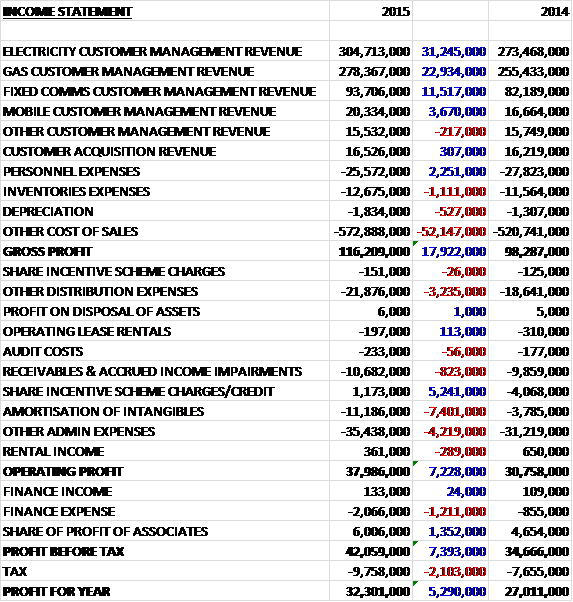

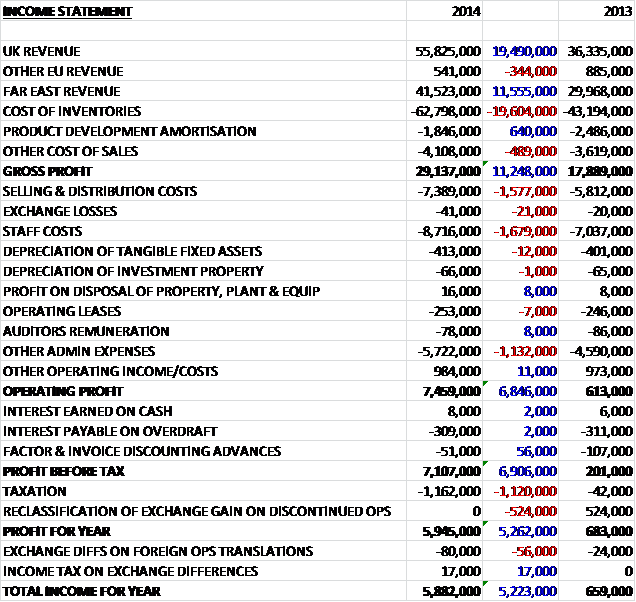

Interest income increased by some £25.2M when compared to last year, driven by a £23.8M increase in interest from loans to customers, and a £908K reduction in interest expense. Net fee income also increased, up by just £1.1M as a £2.9M fall in fee expenses and an £890K increase in trust fee income was partially offset by a £2.7M decline in PPI insurance income. Underlying admin expenses increased year on year with a an £8.7M increase in staff costs (not including share based payments) and a £3.1M growth in other admin costs but there was the lack of a number of one-off gains that occurred last year when the group got £1.2M in rental income and £6.5M from the sale of a building. . All this meant that, after a £1.3M increase in tax, the profit for the year came in at £17M, an increase of £5.5M when compared to 2013.

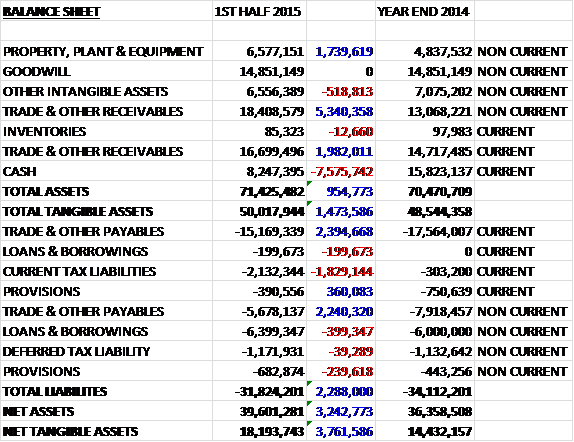

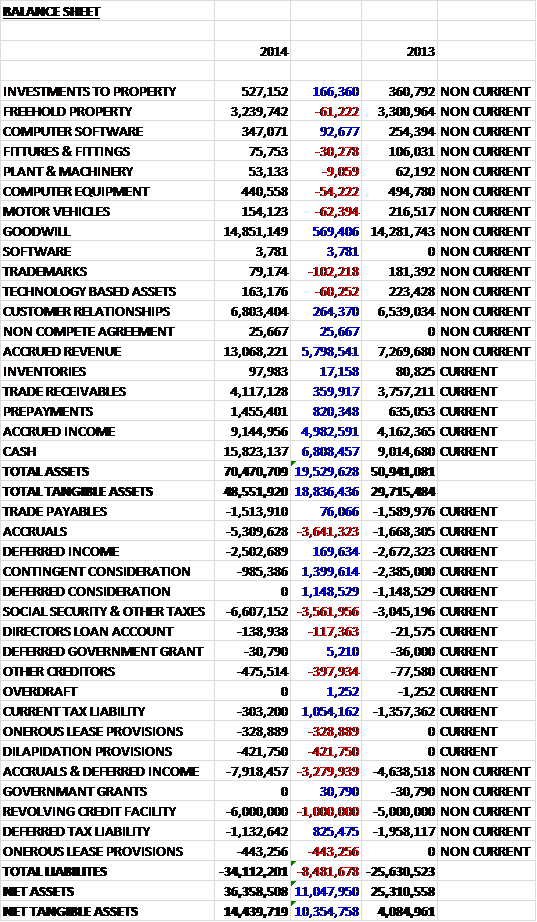

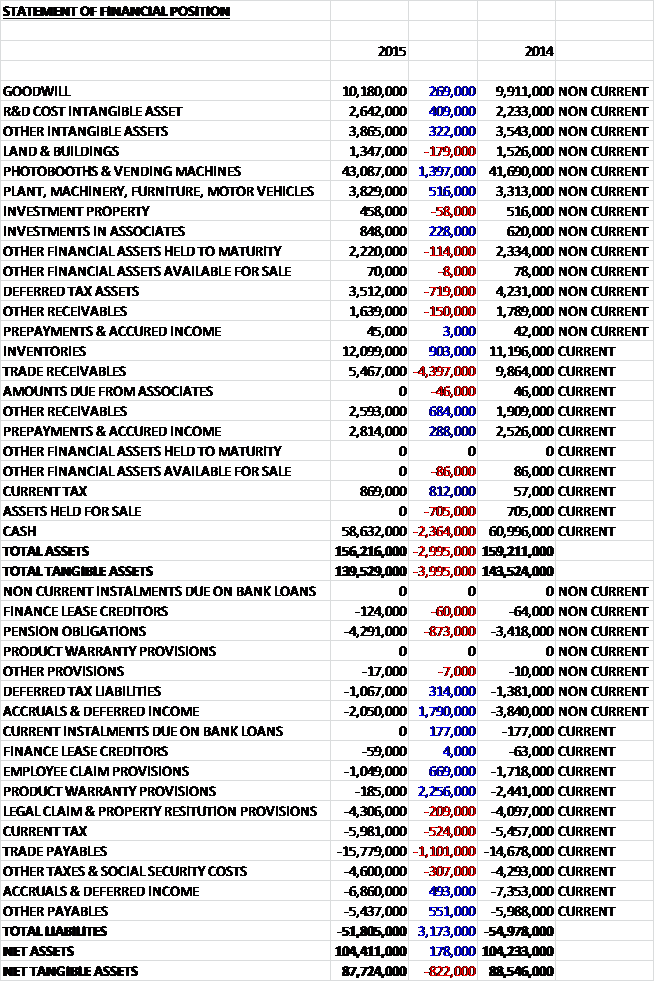

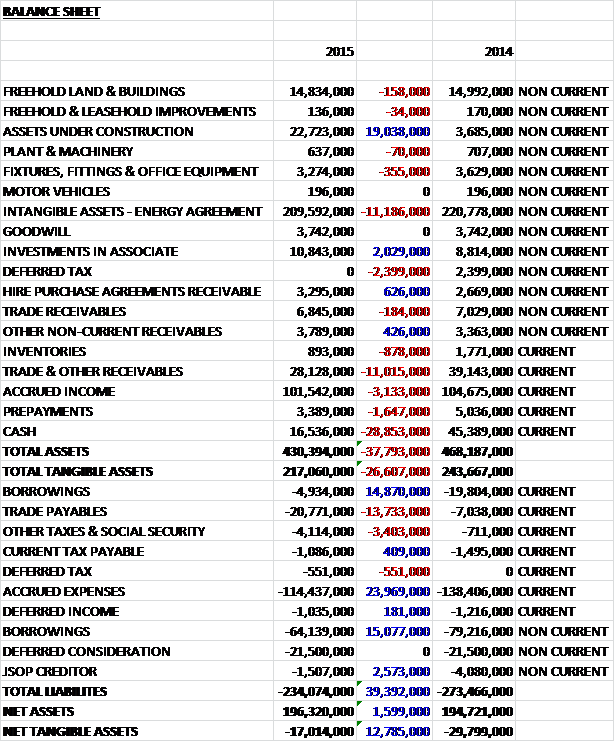

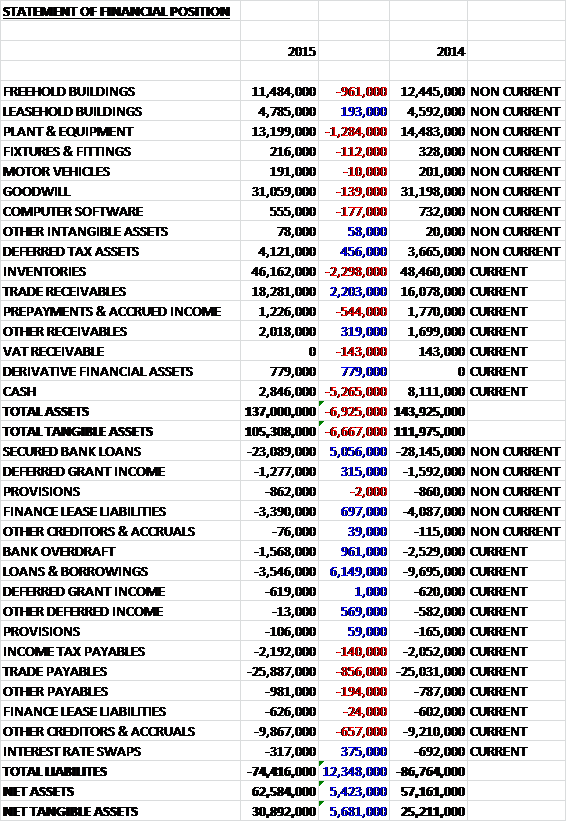

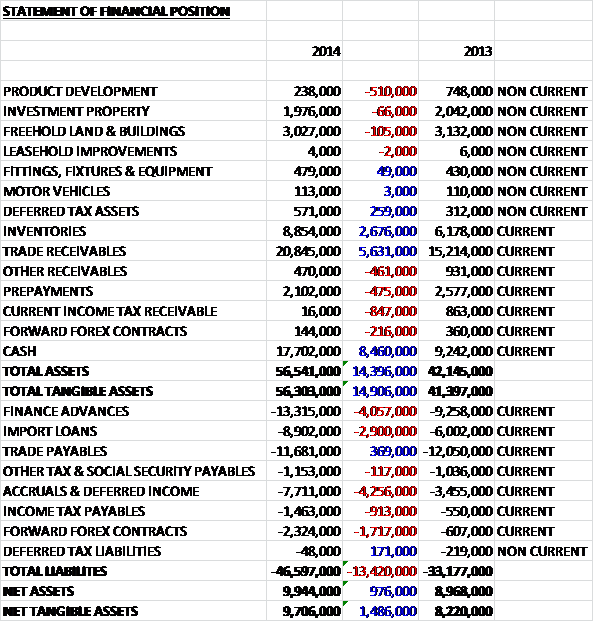

When compared to the end point of last year, total assets increased by £355.8M driven by a £197.8M increase in mortgages, a £132.5M growth in commercial loans, a £72.2M increase in debt securities held to maturity and a £51.1M growth in other loans to customers, partially offset by a £77.1M fall in cash held at central banks and a £73.2M decline in loans to banks. Liabilities also increased during the year due to a £159.5M growth in term deposits from customers, a £47.1M increase in current account deposits, a £29.9M growth in notice account customers and a £25.7M increase in deposits from banks. The end result of this is an £88.4M growth in net tangible assets to £162.3M. There are operating lease commitments of £21.4M.

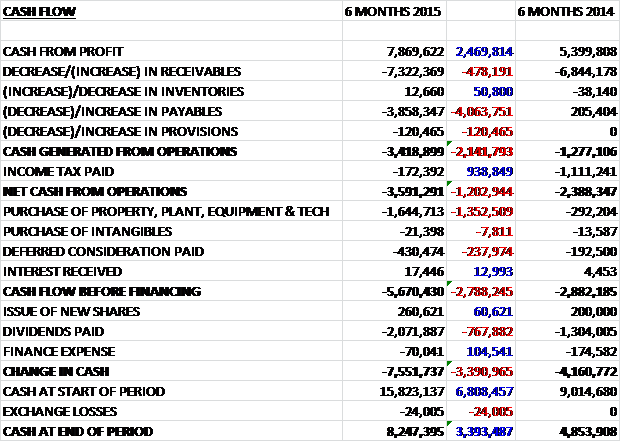

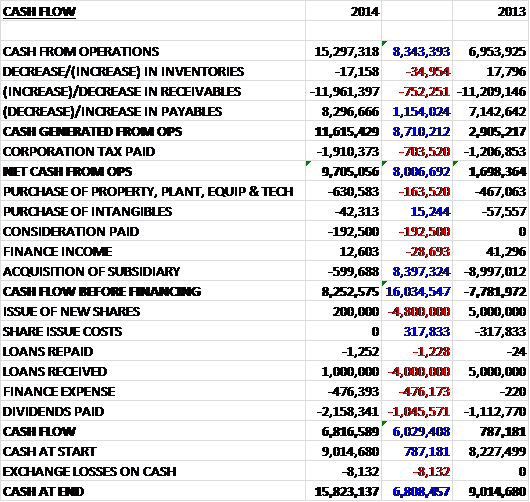

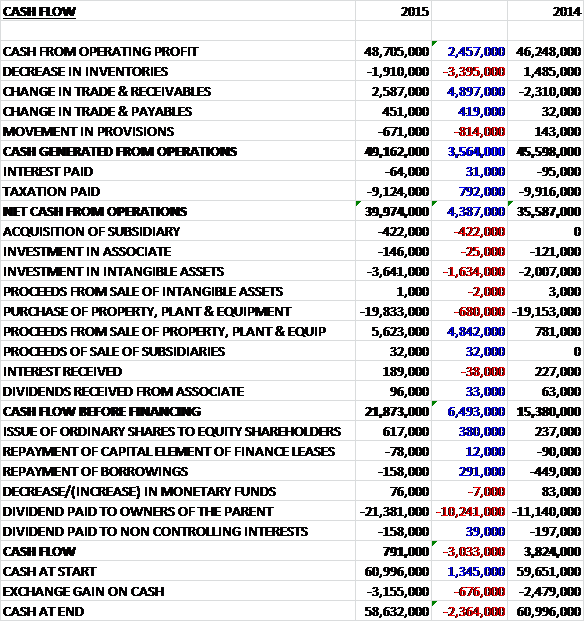

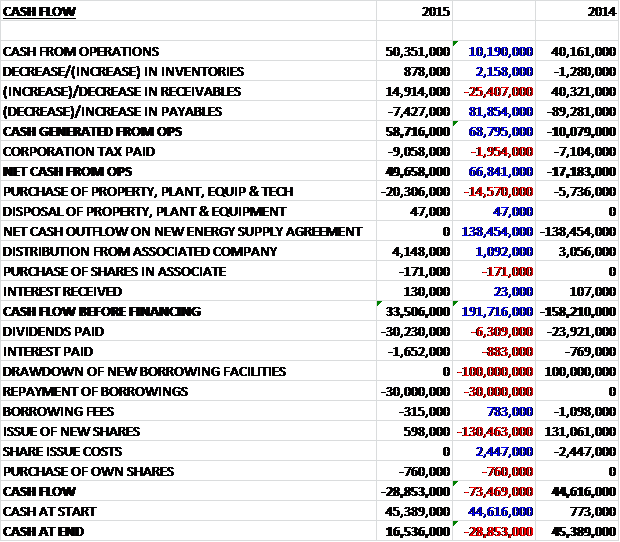

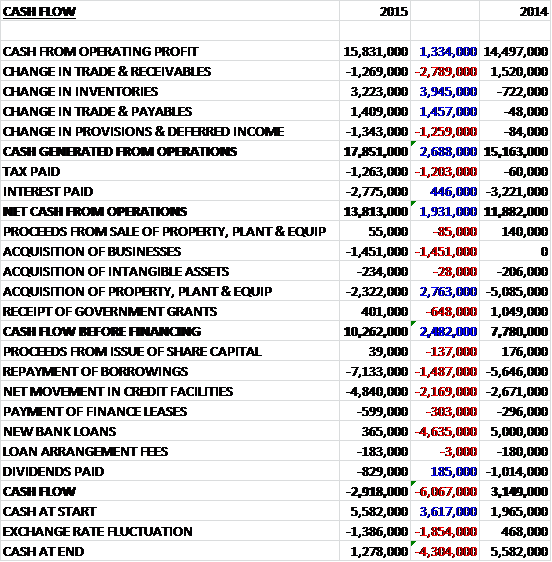

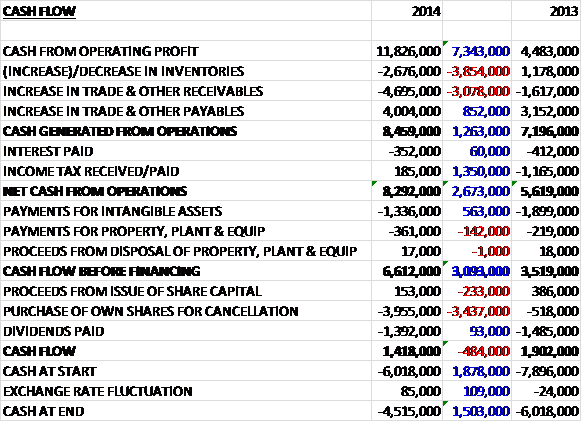

Most of the cash was gained through interest receipts with a £25.6M increase in interest received and just a £1.4M increase in fee income. We also see that there was no other income compared to the £7.7M that occurred last year (relating to the sale and leaseback of the HQ). Cash payments to employees and suppliers increased by £10.7M and tax was slightly higher to give a cash flow from profits of £31.2M, an increase of £9.9M year on year. The net cash from operations was heavily negative, however, widening by £129.5M to give an outflow of £163.8M. This was because the increase in loans to customers was not covered by the increase in amounts due to customers. We then see a further £7.8M spent on property plant and equipment and a net £72.2M being spent on debt securities to give a cash outflow of £244.8M before financing. The group then increased borrowings by £25.7M and gained £48.8M from a placing at the subsidiary, One Trust Bank along with £24.3M in proceeds from selling shares in One Trust. The end result is a cash outflow of £150.3M to give a cash level of £147.8M at the end of the year which is clearly not a sustainable situation.

Arbuthnot Latham reported pre-tax profit of £3.6M compared to £7.7M last year, although last year’s result was dominated by the £6.5M gain generated by the sale and leaseback on the new HQ and underlying profits more than doubled. The underlying business delivered a year of growth across all key areas. The core business of private banking and wealth management benefited from the evolving market conditions and the move into the new HQ in London towards the end of the year was a sign of the development of the business and the continued expected growth going forward.

The business has been focusing on key sectors of the wealth market in the UK through the recruitment of new senior bankers and the growing disenchantment of wealthy clients with the ever increasing volume of changes has resulted in some of them moving their business to Arbuthnot. Excluding the acquired portfolio, the client loan book grew by 26% to £430M and client deposits grew by 12% to £586M. As a result of the higher number of quality private banking clients, the overall costs of deposits fell during the year. In Wealth Management, there was a 26% increase in assets under management to £666M.

The bank is developing its proposition outside London. The office in Exeter has grown, a new office in Manchester has been opened and the Dubai office completed its first year of operation. In Dubai, there has been strong business strength in a short space of time reflecting the dynamic nature of the local market and its long term potential. Towards the end of the year, the bank completed the purchase of a portfolio of residential mortgage loans. The mortgages were being sold by the administrator of the Dunfermline Building Society and they are geographically diversified. They also offer the group a stable asset to offer as collateral to participate in the Bank of England’s sterling monetary framework, gaining access to a further source of liquidity. The portfolio was purchased at a discount to face value and came onto the balance sheet at £106M. It had little impact on the results this year but will be immediately accretive in 2016.

Secure Trust Bank recorded pre-tax profits of £26.3M, an increase of 53% when compared to the previous year. The Bank’s lending portfolios achieved double digit growth with advances to customers increasing by 59% to £622.5M at the end of the year and total new volumes growing by 79% to £545.9M. Motor Finance increased by 20% to £137.9M as the business continued to service the top 100 UK car dealer groups and strengthened its relationship with specialised motor intermediaries. Retail Finance grew by 37% to £156.3M with an encouraging performance of V12, acquired in 2013. The launch of its season ticket offering was well received and the funding strength provided by the group enabled V12 to pitch to larger retailers with a new strategic relation with AO.com being a good example of this. Personal unsecured lending balances including Everyday Loans increased from £159.2M to £181.4M and these portfolios are currently being managed to maximise return rather than outright growth, although the newly launched guarantor loan offering should supplement growth rates in 2015.

The bank launched its SME division during the year and Real Estate Finance has quickly developed a portfolio of loans totalling £133.7M largely secured on residential properties and towards the end of the year the bank also began its invoice finance business via STB Commercial Services. The flow of new business on this product exceeded the initial expectations and the portfolio ended the year totalling £5M. In addition, asset finance was commenced via a partnership with Haydock Finance who provides a full business outsourcing service.

The bank has been on a good trajectory of growth and the management teams have been careful to ensure that it is well controlled. Improvements have been made to the risk and compliance teams and a new treasurer, chief internal auditor and chief technology officer have been appointed. The bank is funded by the retail deposit market and during the year customer deposits increased by 39% to £608.4M and in addition, a £50M share placement was completed which increased the capital base of the bank by 44%. During the year the bank has received several external accolades including being the only UK bank to hold the Customer Service Excellent award which replaced the kite mark and it has also received the 4 star mark by the Fair Banking Foundation. The Current Account ended the year with 20,792 accounts compared to 22,860 in 2013.

Although impairment losses increased by 3%, compared to the increase in the loan book this represents a good outcome. There were a number of reasons for this. Firstly, a significant proportion of the increase in lending was as a result of the start-up of the Real Estate Finance Division. This lending is fully secured at LTVs of around 60% so losses on this portfolio should be minimal and due the short time that it has been running, it is too early for any of its lending to have become impaired. Secondly, as a result of the market benchmarking exercise for non-performing loans, the business concluded that the provisions held against its debts in long term recovery were excessive so the provisions were released.

During the year the company sold over one million shares in its subsidiary, Secure Trust Bank that resulted in a net gain of £24.3M. In addition, Secure Trust issued over two million new shares, gaining it £48.8M. This had the effect of reducing the company’s holding from 67% to 52% which is a bit of a shame in my view.

The company is controlled by founder, CEO and Chairman Henry Angest who owns nearly 54% of the total share capital. The other large holders are made up of various institutions such as Unicorn and Prudential. I have to say that the board remuneration looks very generous with the highest paid directors getting £3.7M and £3.6M during the year. This was mostly due to LTIP awards but seems overly excessive to me even though the company seems to be performing well (bankers, huh?). At least none of these were Mr. Angest which really would have sent alarm bells ringing.

The group seems to have a decent capital ratio with the core tier 1 capital ratio improving from 14.4% to 18.2%. In addition the group does not seem to have much exposure to exchange rate movements or interest rate changes Going forward, the economic outlook remains uncertain with a continued weak Eurozone economy and the central banks committed to expansionary monetary policies. Despite this, the group is making good progress and the board remains optimistic that this can continue.

At the current share price the shares are yielding 1.9% which increases to 2% on 2015’s consensus forecast which is decent rather than spectacular. At the current share price, the shares trade on a rather expensive 25.2 times earnings but this falls considerably on next year’s forecast of 13.8 which starts to look rather good value.

Overall then this looks like a great year for Arbuthnot. Profits were up considerably despite a one-off gain last year from the sale and leaseback of the HQ – something I am not actually a fan of but I suppose the group must have been desperate for the cash to expand. Net assets were also up as the group purchased a large mortgage portfolio and underlying cash profits increased, although operating cash flow was heavily negative due to the rapid expansion in lending to customers. Operationally, Arbuthnot Latham is by far the smaller contribution to profits but underling income from that bank did double during the year while Secure Trust is the main driver of earnings which had a great year, opening its SME banking operations.

The bank is funded by retail deposits and seems to take quite a conservative view on funding which is something I really like, but having said that they do seem to be displaying some short-termism in their actions with the sale and leaseback of the HQ and the sale of a portion of their Secure Trust holding. That bank is going from strength to strength and is a major source of profit so why are they selling down their holding? I don’t really understand that to be honest. Overall though, the bank is performing very well, the dividend yield is decent enough and the forward P/E doesn’t look too taxing so I am thinking of taking a position here.

On the 15th May the group and Secure Trust released trading updates for Q1. As far as the group is concerned, it has started the year well. Both banks have traded robustly and have delivered strong growth in lending volumes. Overall, customer loan balances finished Q1 over 60% higher than at the same point of last year. The board believes they are well positioned to make further progress during the year.

There is a bit more detail on the Secure Trust update. The Consumer Finance business continued to make significant progress compared to Q1 last year. New lending volumes in Retail Finance and Motor Finance have grown 121% and 22% respectively. In the SME lending market they continue to see strong demand for their products. Momentum is building in line with management expectations and lending balances now exceed £200M. The Real Estate Finance business has a significant pipeline of new opportunities and the commercial finance and asset finance businesses continue to develop as planned.

This all sounds very positive.

he share price hasn’t really made much progress this year but the recent weakness could be a bit of a buying opportunity?

On the 4th December the group announces that Secure Trust Bank has agreed on the sale of its branch based non-standard consumer lending business, Everyday Loans, to Non Standard Finance. The total consideration is for £127M and comprises £107M in cash and £20M in NSF shares and on completion, NSF will repay the £108M intercompany debt to STB with the expected profit on disposal being at least £115M. In the view of the CEO of Secure Trust, the unsolicited approach for the business presented an attractive option to accelerate the strategy of proportionately reducing their exposure to personal unsecured loans products whilst investing in the strongly growing motor retail and SME lending activities.

ELG represents about £102M of the £189M receivables of the bank’s consumer lending division and generated revenues of £40M last year with profits of £12.9M. It has net assets of just £7M. The acquisition is being funded by way of a placing and debt facilities, of which £30M has been provided by Secure Trust in the form of a three year loan.

While in the short term the disposal is expected to be earnings diluting, the board is confident that the proceeds can be invested to accelerate the bank’s growth prospects and secure new income streams. They are continuing to see strong growth in the Motor, Retail and SME lending activities and the capital generated by the disposal will support the ongoing increase in customer lending balances which now exceed £1BN. The bank has reiterated that it expects 2015 results to be in line with market expectations, after taking into account the deal costs already incurred.

Overall then, this seems like a good price for the business and hopefully the proceeds can be invested sensibly.