Easyjet has now released its interim results for the year ending 2015.

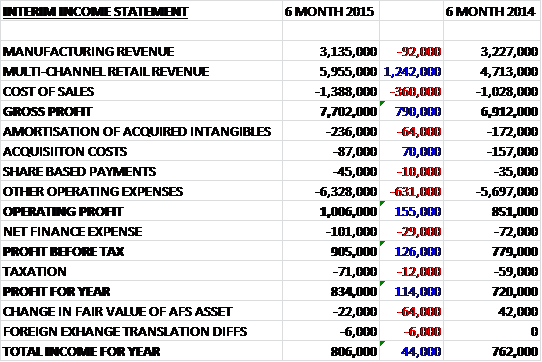

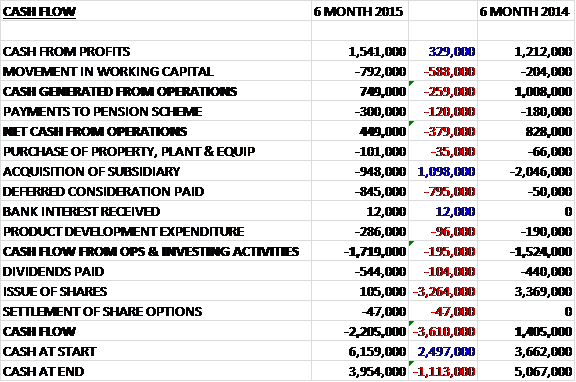

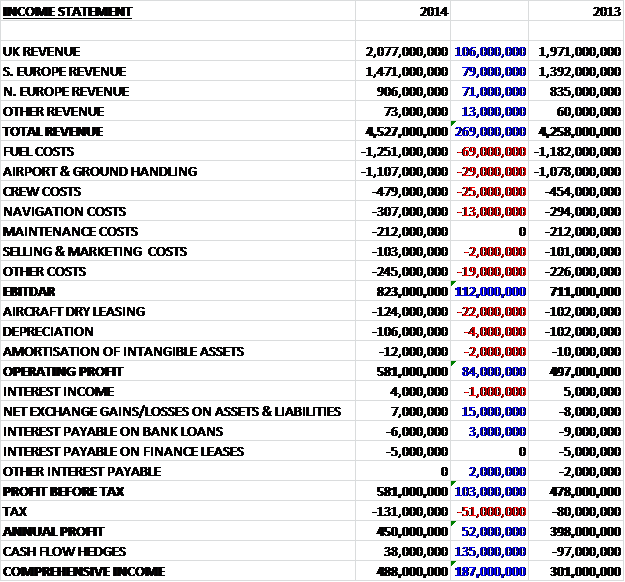

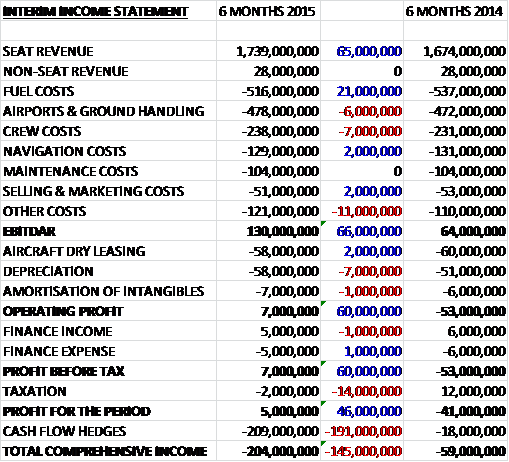

When compared to last year, seat revenue increased by £65M. Operating costs remained fairly flat year on year as an £11M increase in other costs relating to disruption costs, a £7M growth in crew costs due to pay increases and the early recruitment of crew ahead of the three new base openings, and a £6M increase in airport costs due to expected regulatory changes in Germany and Italy were offset by a £21M decline in fuel costs (although the market fuel price reductions have not been fully reflected in the cost to the group due to the hedging policy). Depreciation was then £7M higher than last year to give an operating profit of £7M, a positive swing of £60M when compared to the first half of last year. After tax this became a £46M positive swing to £5M for the half year, although we see that the hedges took a hammering due to the decline in the fuel price. It should be noted that revenues and profitability are lower in the first half and recover in the second half which covers the much busier Summer season. The performance in the first half has benefited from an exchange rate gain of £18M which is expected to more than reverse in the second half.

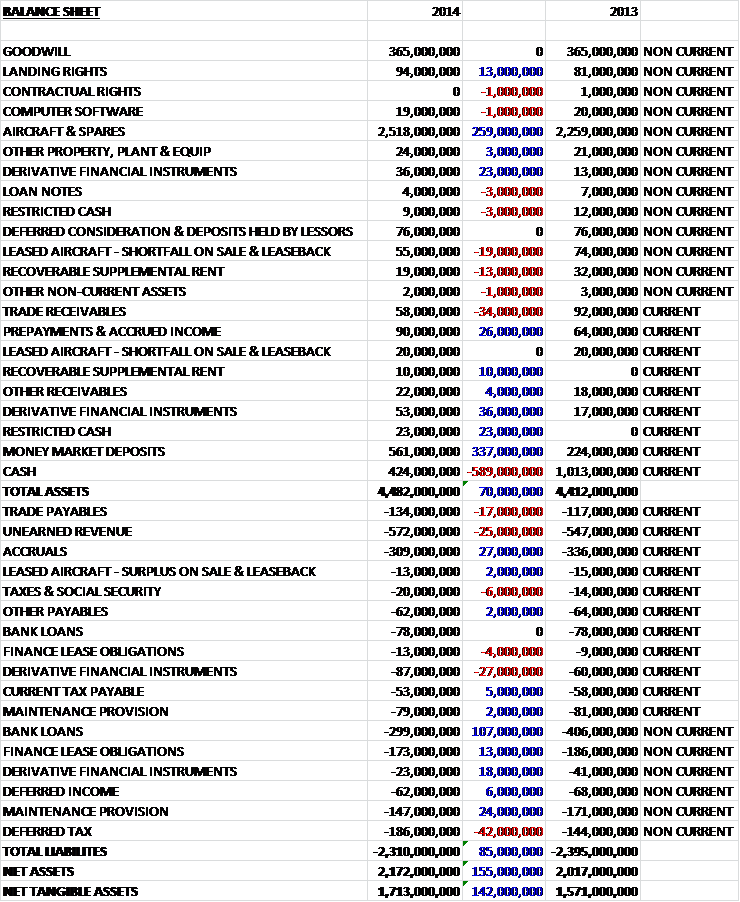

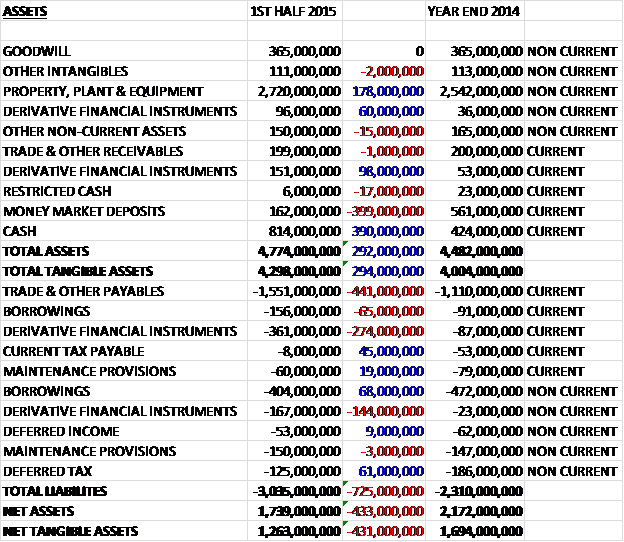

When compared to the end point of last year, total assets increased by £292M driven by a £178M increase in property, plant and equipment and a £158M growth in derivative financial instruments. We also see the £399M fall in money market deposits being offset by a £390M increase in non-restricted cash. Liabilities also increased during the six month period as a £441M increase in payables and a £418M growth in derivative financial instrument liabilities were partially offset by a £68M fall in borrowings, a £61M decline in deferred tax payable and a £45M fall in current tax payable. The end result is a £431M decline in net tangible assets to £1.263BN.

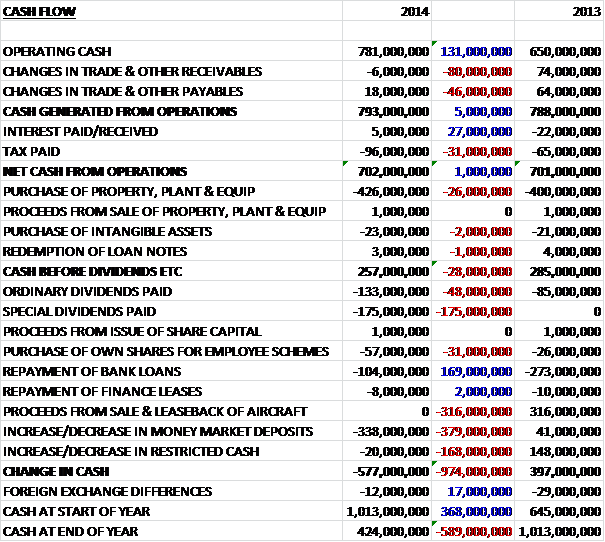

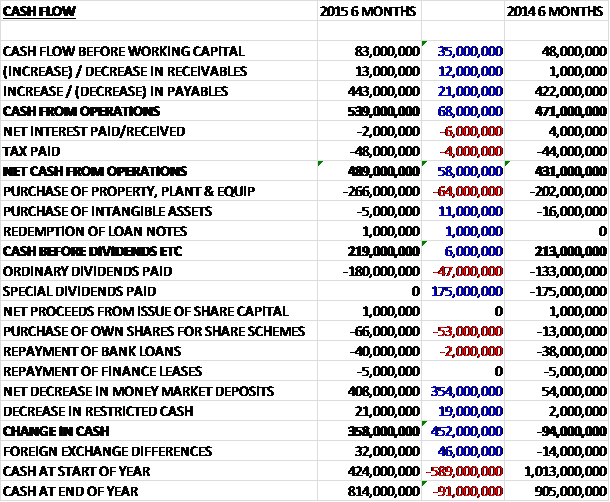

Before movements in working capital, cash profits increased by £35M to £83M. We then see a huge increase in payables partially offset by a £48M tax bill to give a net cash from operations of £489M, an increase of £58M year on year. This was easily enough to pay for the increased capital expenditure with the spend on tangibles up £64M to £266M relating to the acquisition of eight A320s, the purchase of life limited parts for use in engine restoration and deposits on aircraft acquisition made in advance of delivery, and the spend on intangibles down £11M to £5M to give a free cash flow some £6M higher at £219M. This was enough to cover the £180M dividend spend and the £40M repayment of the bank loan but it did not cover the £66M spent on the purchase of shares for employee share schemes (no doubt to cover the ridiculous exec director remuneration. We then see some £408M transferred out of money market deposits into cash to give a £358M cash flow for the half year and a cash pile of £814M at the period end.

Easyjet’s markets grew by 6.8% year on year in terms of numbers of seats but the group only increased capacity by 3.6% as their competitors took the bulk of the increase, growing by 7.7%. The growth in the European short haul market is set to continue in the second half as a result of improved economic conditions and a lower oil price.

In the UK EasyJet increased capacity by 3% and increased capacity at Gatwick by 10% due to the new slots purchased from FlyBe and by deploying larger aircraft at the airport. The group launched 12 new routes such as Edinburgh to Funchal and Gatwick to Stuttgart whilst also increasing frequencies on selected routes. In the first half of the year the group increased capacity in Switzerland by 6.3% with growth focusing on increasing capacity on existing routes and introducing new routes such as Basel to Lanzarote and Geneva to Vienna.

The group continued to increase capacity and market share in France with capacity increasing by 4.3% to give a market share of 14%. The growth was focused on increasing frequencies on existing routes and introducing new routes. The board continues to see attractive growth opportunities in the country. In Italy the group increased capacity by 5.3% and it now has a market share of 12% with growth focused on both existing routes and new routes. They now have 26 aircraft based across Milan Malpensa, Rome Fiumicino and Naples and operates from 17 different airports in the country. In Germany, the group’s capacity increased by 15% and it now has a 4.1% market share. Capacity growth was driven by increasing frequencies to business destinations including London, Amsterdam and Basel. There are now 12 aircraft based across Berlin and Hamburg and 13 new routes were launched during the period.

In Portugal the group has a 12% market share and opened their second Portuguese base at Porto with two based aircraft. In the second half, six new routes will be launched from Porto to Luxembourg, Nantes, Stuttgart, Manchester, Bristol and Luton. The group has an 8% market share in Spain and continues to see opportunities to allocate capacity to routes able to generate high returns. In the Netherlands, the group increased capacity by over 13% after launching a new base in Amsterdam in March with three based aircraft and another to be sited there from October.

During the period the cost per seat, excluding fuel fell by 1.4% on a reported basis but increased by 2.9% on a constant currency basis. The increase was driven by an increase in charges at regulated airports, increased crew costs associated with new base openings along with higher levels of de-icing and disruption in Q2.

The revenue per seat grew by 0.2% on a reported basis and by 2.6% on a constant currency basis. This increase was driven by strong October trading, particularly UK beach and domestic French routes; an increase in load factor by 0.7 percentage points to 89.7%; increased allocated seating conversion rates and the yield management of bags; the timing of Easter and a good finish to the ski season; business passenger initiatives including the first business TV advert; and continued investment in digital and revenue management initiatives such as the bespoke app for the Apple watch.

The business passenger initiative made good progress during the period with growth in passengers in line with expectations. Sales of business products performed well, including a more than doubling in the sale of inclusive fares when compared to the first half of last year. Sales through Global Distribution Systems grew by 59% as the group continued to leverage its relationships with the Travel Management Companies. The board continues to see opportunities across Europe and recently strengthened its corporate focused sales team in France, Germany and the Netherlands.

The group’s on-time performance declined from 89% to 86% due to adverse weather across Europe and industrial action. The weather in Q2 was worse than the unusually benign period last year which resulted in an increase in the use of de-icing fluids. In addition there were increased diversions due to snow across Europe and strong winds. Q2 also saw an increase in industrial action in Europe including two Italian Air Traffic Control strikes, firemen strikes in Paris and two strikes by airport security staff in Germany which resulted in a total of 683 cancelled flights in the first half compared to 520 last year.

Overall the Euro rate weakened since the last half year which resulted in a loss of £35M in revenue generated in Euros and a gain of £50M on costs excluding fuel incurred in Euros. The dollar rate also weakened slightly which resulted in an exchange rate gain of £6M on the purchase of fuel. Overall the impact of exchange rate movements was a gain of £18M. Although the group has a surplus of Euro costs over revenue, revenue cash inflows generally occur several months before cost cash outflow which, with the weakening Euro against Sterling, results in a short term benefit to the income statement. It is expected that this will more than reverse during the second half giving an adverse impact for the full year.

The “lean” programme delivered £21M in sustainable savings in the period which included the benefit from longer term airport deals such as the new contract with Gatwick that gives the group certainty on passenger charges over the next seven years. It is hoped that the programme will deliver between £30M and £40M in savings over the next five years. The company is also in the process of evaluating the provision of its maintenance contracts and has selected AJW to be the primary provider of its requirement for component maintenance and the provision, storage and distribution of spare parts.

The decision has been made to increase the number of seats from 180 to 186. All new aircraft delivered from May 2016 will be fitted with 186 seats and the existing fleet will be retrofitted from winter 2016 to be completed by the summer of 2018. This action should deliver a cost per seat saving of 2% but obviously will reduce the space in the aircraft.

The group is contracted to acquire 167 A320 aircraft with a total list price of $14.3BN. Of these, 11 are due for delivery this year, 50 from 2016 to 2018 and the remaining 100 by 2023. During the first half of the year the group took delivery of eight A320 aircraft and disposed of four A319 aircraft. In the second half of the year, one aircraft will exit the fleet and a further 12 A320 deliveries are planned.

Going forward the group is planning on increasing capacity by 6.2% this summer against a forecasted competitor increase of 6.7% with lower fares being offered due to the declining price of fuel. The second half has started off with a difficult month. Due to extended French Air Traffic Control strikes in April the group has had to cancel some 600 flights which is expected to impact pre-tax profit by around £25M. Taking this into account, along with the increasingly competitive environment, it is expected that revenue per seat on a constant currency basis in the second half will fall by low single digit percentage points. In addition Q3 revenue per seat will be impacted by the movement of Easter which is likely to reduce revenue per seat by 3 percentage points which means the group is expecting Q3 revenue per seat to fall by about four percentage points.

Not including fuel, the group expects costs per seat on a constant currency basis to increase by 2% in H2. This does not include a possible additional navigation charge from Eurocontrol of up to £12M which the group is currently disputing. The increase is likely to be driven by charges at regulated airports, particularly in Germany and Italy; increased crew costs and higher navigation charges. Including fuel, however, cost per seat is expected to fall by about 1%. With jet fuel remaining between $550 per tonne to $750 per tonne, the fuel bill for the second half of the year is likely to decrease by between £60M to £85M year on year. For the full year the decrease is likely to be between £95M to £120M. Additionally, exchange rate movements are likely to have a £40M adverse impact in the second half and a £20 adverse impact for the year as a whole.

As the group enters the important summer season, forward bookings are in line with last year with passengers benefiting from a fall in fares in a more competitive environment due in part to the lower fuel costs. The group is apparently still well positioned to grow revenue and profit this year.

Easyjet only pays dividends once a year and at the current share price the shares yield 2.9%, increasing to 3.2% on 2015’s consensus forecast. Including operating leases at seven times, the adjusted net debt stood at £438M compared to £446M at the end of last year and the group signed a new five year $500M revolving credit facility.

Overall then, this seems to have been a more mixed set of results for EasyJet. Profits were up, although they were flattered by £18M of net currency gains and the inclusion of Easter in March. Operational cash flow also increased and the group remains very cash generative but net assets declined in the half year due to an increase in payables (this seems to be seasonal) and a growth in the net derivative financial instrument liabilities as the declining price of fuel affected the hedging instruments. So far in the second half the group has been hit by a £25M charge relating to the French air traffic strike and will also lose out due to the timing of Easter. In addition adverse currency movements are expected to impact the group by £40M which is offset by a £60M saving from the lower fuel price.

The shares do look decent value but the ongoing industrial action in the industry is a concern as is the fact that the group may become relatively less competitive than some of its rivals due to its fuel hedging activities. I will keep an eye on proceedings here.

On the 4th June the group released the passenger stats for May. EasyJet flew 6,490,974 passengers during the month, an increase of 7.2% compared to the same month last year. The load factor also increased, up from 89.4% to 91.6%.

On the 18th June the group announced a change in its operations in Italy with a new base opening in Venice and the closure of the Rome base. In Venice, the company will open a base starting from April 2016 with four aircraft based at the airport. The airline already flies to the city from 15 airports across Europe and is the largest airline at the airport. The opening of the base will enable the group to fly more early morning departures from Venice. Milan Malpensa is already the group’s second largest base with 18 aircraft. It is announced that three more will join from April 2016 which will strengthen their existing status as the largest airline at the airport which is located in Italy’s richest metropolitan area.

In 2014, EasyJet opened a base in Naples and is already the largest airline at the airport and there are plans to add one more aircraft to the base from April boosting the total to four. The Rome Fiumicino base is delivering lower returns than the group’s other bases. The worsening performance has been driven by high airport passenger charges, which have more than doubled since 2012 with further above inflation increases in the coming years. In addition, the airport offers a poor passenger experience which has led to low levels of punctuality and customer’s satisfaction, thereby dragging damaging the brand so it seems to make sense to redeploy these aircraft to other, more promising Italian cities. In addition, it was also announced that the group will open a new base in Barcelona from February 2016, basing three aircraft there.

On the 26th June it was announced that non-executive director John Browett will be appointed CEO at Dunelm from the start of 2016.

On the 6th July the group released their passenger stats for June. Passenger numbers increased by 7.6% to 6,559,802 and load factors increased from 92% to 92.7%, which seems rather impressive. Overall it does seem as though things are improving for the group although the threat of industrial action continues.

The share price seems to have halted its decline but I can’t say it is recovering yet.

On the 22nd July the group released a trading update covering Q3 where it was stated that after 77% of seats have now been booked for the second half of the year as a whole the group expects to grow profit before tax from £581M in 2014 to between £620M and £660M this year.

This quarter, passenger numbers increased by 6.2% to 19.1M year on year, and the load factor increased from 90.4% to 91.7% but the revenue per passenger fell by 6.8% to £64.42 to give a total revenue down 1% to £1.24BN. The capacity growth seen was focused on Amsterdam, Hamburg, Porto, Basel and Geneva.

April was a difficult month due to the movement of Easter and the French ATC strike which together reduced revenue per seat by three percentage points and adversely affected profits by £25M. In the other two months, the performance was better than expected through driven by trading in the UK and beach routes across Europe along with a number of revenue management initiatives. Business passengers grew in line with expectations and sales of inclusive fares grew by 76%.

The group launched a mobile host and new iphone app during the period. The host is now available in Gatwick and Edinburgh and provides customers with notifications at relevant points of their journey through the airport such as bag drop and gate information. In the quarter the group took delivery of nine A320 aircraft to give a total of 90 A320s and 149 A319s at the period-end. The net cash position has fallen by £182M year on year to £421M as a result of pre-delivery payments and the acquisition of aircraft.

During the period the group cancelled 1,463 flights compared to 648 in the prior year. The majority of these cancellations (773) were due to the reduced capacity caused by a fire at Fiumicino airport with the French strikes accounting for a further 591. The on-time performance was lower in the quarter, driven by issues with the ground handling supplier at Gatwick which have now been addressed.

There was a 1.1 percentage point impact on costs from the French strike and the fire at Fiumicino and airport charges increased by 0.8 percentage points in regulated airports in Italy and Germany. Cost per seat, excluding fuel therefore increased by 2.8% on a constant currency basis but because the price of fuel has fallen so heavily, the cost per seat including fuel fell by 3.3% and the fuel bill in the second half of the year is expected to fall by between £65M and £80M, offset by a £35M adverse effect from exchange rate movements. The efficiency programme delivered a further £7M of saving in the quarter driven by initiatives in airports and ground handling and the group are confident of delivering savings for the full year between £35M to £40M.

Going forward the group has hedged 83% of its fuel requirement for Q4 at $878 per tonne and 80% at $844 per tonne for next year with jet fuel currently trading between $550 and $750 per tonne. The current macro environment is uncertain with the issues in Greece and Tunisia combined with the reduction in capacity at Fiumicino and continued threats of industrial action but the group still expected to grow profit from £581M last year to between £620M to £660M this year which includes the impact from the resolution of the Eurocontrol dispute which will result in an £8M additional navigation charge in Q4.

Overall then, things seem to have improved since the last update and profits are going to increase this year, mainly as a result of the fall in the price of fuel despite the previous hedging policies adversely affecting the group.

On the 6th August the group released their passenger stats for July. In total, passenger numbers increased by 9.4% to 7,036,470 when compared to July 2014 and the load factor increased from 92.9% to 94.3%.

On the 3rd September the group released a trading update. The load factor for August was an astonishing 94.4% and passenger numbers were a record breaking 7.06M. They have also seen a stronger than expected unit revenue performance for the month and the outlook for September, supported by successful ongoing digital and revenue initiatives, looks good with capacity growth across the short haul network of around 6% and particular strength on UK beach routes.

The strong revenue performance has more than offset the significant cost headwinds that the business has faced so far this year, with greater than expected disruption across the network, the impact of the two fires at Rome Fiumicino airport and the one-off £8M settlement with Eurocontrol and costs associated with higher load factors. Fuel and currency exchange rate movements remain broadly within expected ranges. Consequently full year profit before tax is now likely to be between £675M and £700M, an increase from the previous guidance of £620M to £660M. This all looks rather good actually, especially when it is considered that the fuel costs should come down once the more expensive hedges work their way through the system.

On the 4th September it was announced that that the Haji-Ioannou family share holding had been reduced from above 34% of the total to 33.73%.

On the 9th September it was announced that CEO Carolyn McCall exercised an option to purchase 106,978 shares which were all subsequently sold, netting an astonishing £1.9M. This is quite a bonus! It is also a shame that she decided not to hold on to any of the shares.

On the 29th September the group announced that Warwick Brady, a director in the company, sold 17,500 shares at a value of £309K.

On the 5th November the group announced passenger stats for October 2015. Passengers increased by nearly 10% to 6,398,796 year on year and load factors increased from 90.9% a year ago to 93.3%. The profit guidance previously announced continued to be between £675M and £700M so all good here. Having purchased a few shares here I have almost immediately sold again as I got nervous about the fallout from the air crash at Sharm El Sheik.