Vertu has now released their interim results for the year ending 2015.

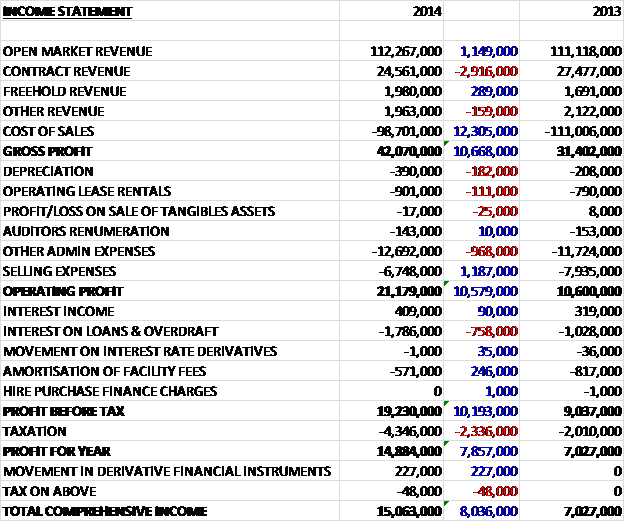

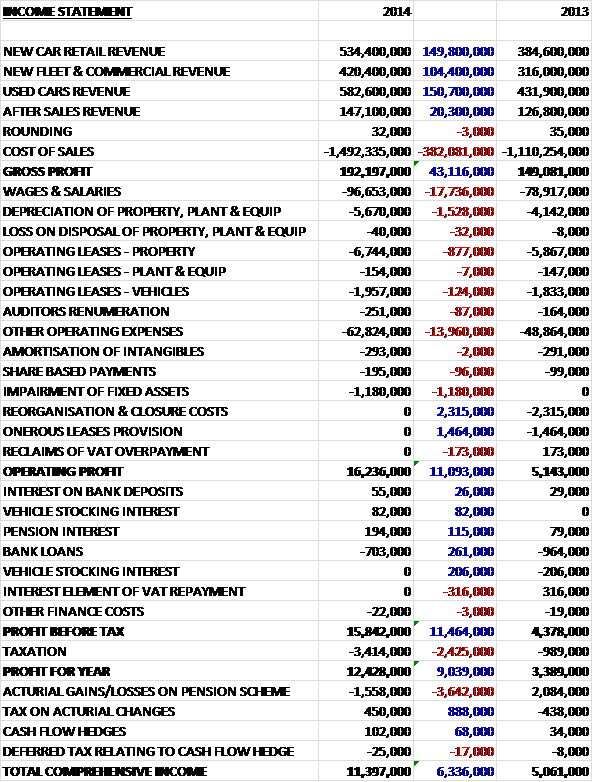

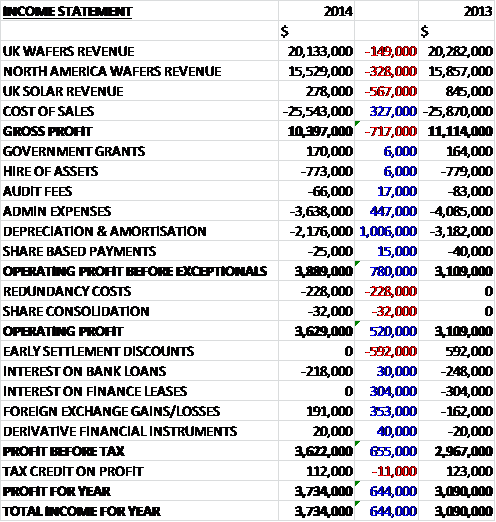

When compared to the first half of last year, revenues increased across all businesses with used vehicles up £95.5M, new car retail up £92.5M, new fleet up £48.8M and aftersales increasing by just under £10M. Cost of sales also increased to leave gross profit ahead by some £22.3M. After the increase in operating costs and share based payments, operating profit was nearly £4M higher than in the first six months of 2014. Movements in vehicle stocking interest and a reduction in loan costs were offset by a £822K increase in tax to give a profit for the period of £10.1M, an increase of £3.4M compared to last time.

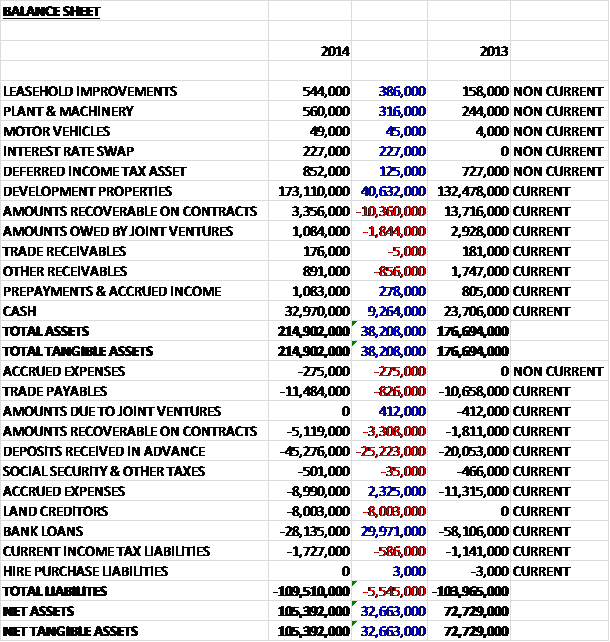

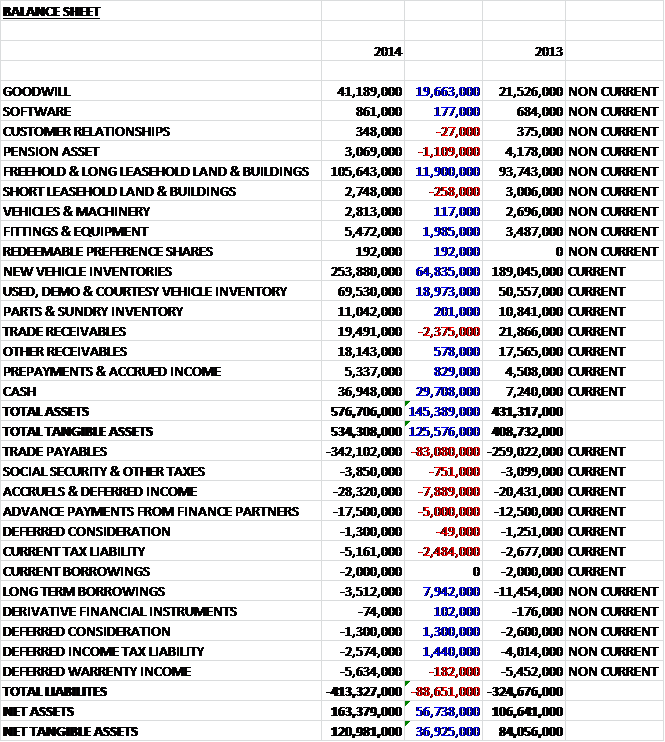

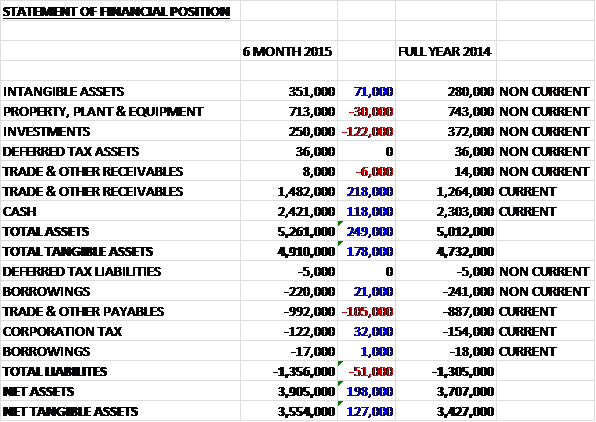

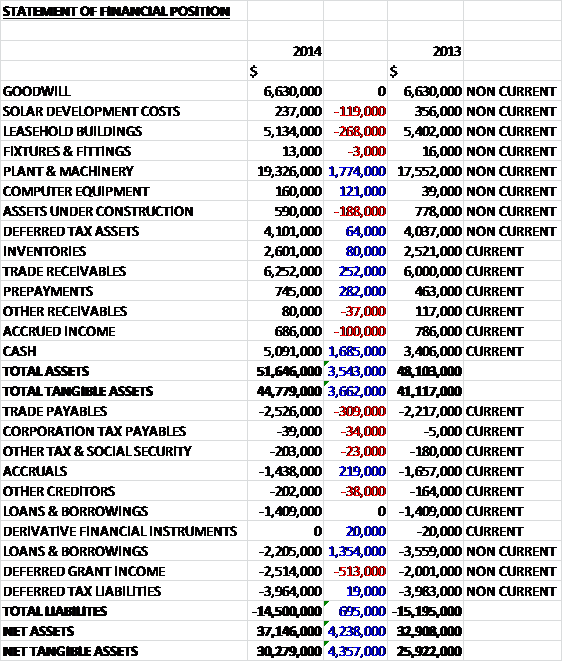

I have used the comparison with the same point of last year as opposed to the end point of the year due to the seasonality of trading. When compared to the half year point of 2014, assets are up by £105.3M due predominantly to an £81.6M increase in inventories. Other contributions came from a £7.1M growth in goodwill, a £6.8M increase in cash levels, a £4.5M growth in receivables and a £4.3M increase in property, plant and equipment with the only major decline an £810K fall in the pension asset due to a fall in corporate bond yields. Liabilities also increased during the same period, almost entirely due to a £93.7M increase in trade and other payables, somewhat mitigated by a £1.9M reduction in borrowings. Overall then, net tangible assets increased by £6.1M to £123M.

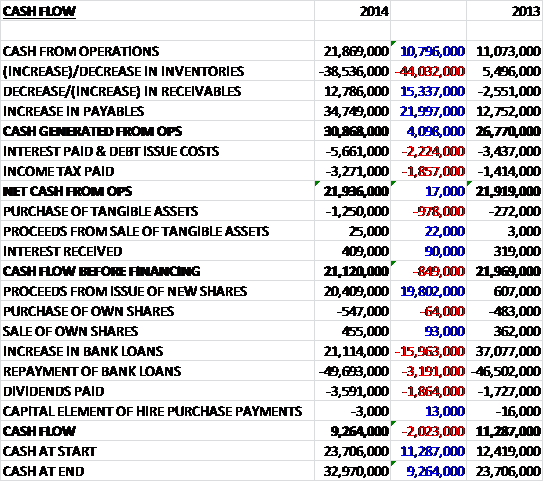

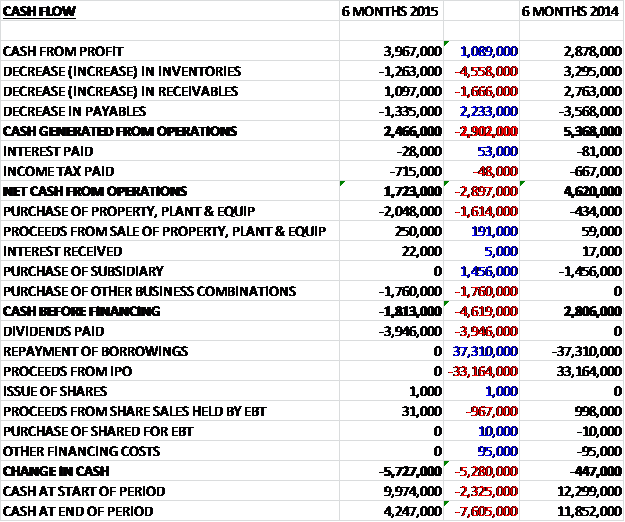

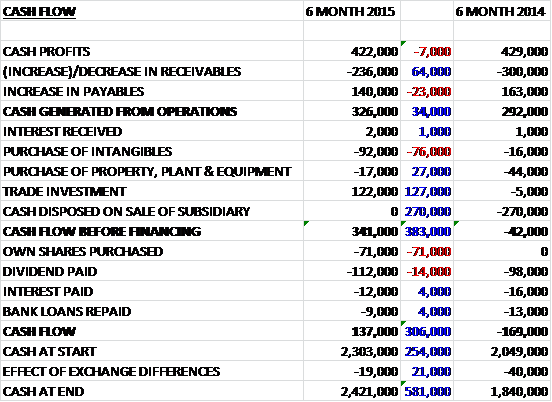

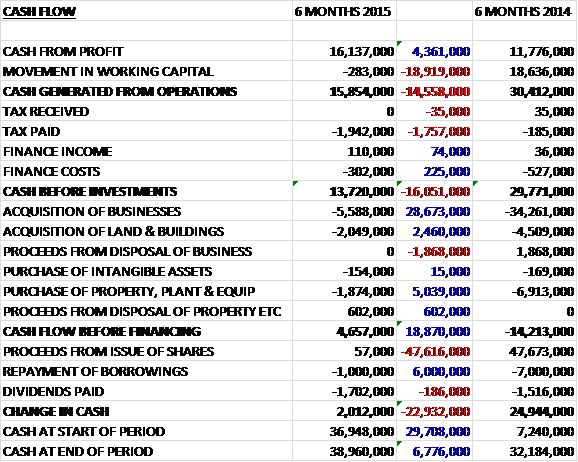

Before movements in working capital, cash inflow was £16.1M, an improvement of £4.4M when compared to last year. There was a lack of the major increase in working capital that happened last year, though, as increased inventories were offset by a decline in payables, so cash generated from operations was £15.9M, almost half that of the first six months of 2014. The tax bill this year was much higher but finance costs were slightly lower to give a net operational cash flow of £13.7M. Of this, £5.6M was paid on the acquisition of new businesses and £2M on the acquisition of land and buildings, along with another £1.9M spent on property, plant and equipment. The group did manage to receive £602K of cash on the disposal of a property (a former dealership property in Nottingham), however, to give a free cash flow of £4.7M. Of this, £1.7M was spent on dividends and £1M on loan repayments so that the resultant cash in flow during the period was a decent £2M.

Service revenues grew by 4.4% during the period reflecting growing used car sales and higher customer retention along with higher spend per customer due to a better conversion of identified and required repair work to sales with video being utilised to help customers visually understand the repair and maintenance work to be undertaken. The further roll out of this technology is expected to further increase sales conversion. In addition, the group now have 64,321 live own branded service plans compared to 39,040 this time last year and increasing service plan penetration is a key objective of the group. Elsewhere in aftersales, there was a 7% increase in accident repair revenues and a 1.9% growth in sales from parts operations with profits and margins rising across both channels, partly as a result of the better quality of remaining accident service centres after the recent closures.

New car retail sales volumes increased by 11.8% on a like for like basis compared to an 11.3% increase in UK private car registrations as manufacturers continue to target the UK over continental Europe and a combination of improved UK economic factors and enhanced fuel and tax efficiency of new cars keep demand high. Core margins fell from 7.5% to 7% during the period reflecting this focus on volume but this increase in volume meant that profits in the sector rose overall. Motability volumes returned to growth with like for like volumes up 5.7%. Although relatively low margin, it is an important market due to the positive impact on after sales demand for the three years following purchase.

New fleet car like for like volumes grew by 12.4% compared to a market growth of 9.4% and new commercial van volumes rose by 28.6% compared to 13.6% in the market as a whole but margins slipped from 2.2% to 2.1% and dealerships are increasingly employing dedicated local business specialists to provide additional after sales opportunities.

The used car market remained stable during the period and the latest data suggests that demand has increased despite the constraints on supply and highly competitive new car offers. During the period like for like volumes grew by 11.6% which is thought to be considerably ahead of the market as a whole. These gains have been driven by the marketing strategy including TV, radio, press and internet. Used car pricing has continued to increase as a result of constrained supply after reduced levels of new vehicle sales during the downturn of 2008-2010 hence the averaged used car selling price rose by 4.2% during the period, also impacted by the inclusion of higher value franchises such as Land Rover which is likely to continue going forward. Used vehicle gross profit per unit increased by 6% during the period with gross margins increasing from 11.1% and 11.4%, boosted by profits on disposal of part exchange vehicles and continued improvements in stock management and sales process.

During the last six months, the UK automotive sector has continued to experience favourable market conditions with the new car market showing further growth and the used car market maintaining stable pricing with modest growth. Servicing demand is increasing as the recent year’s growth in new car sales flow back into service departments for regular service and warranty work. In addition, increasing numbers of used car customers are being retained for servicing due to the growth in sales of service plans where customers pay for services either upfront or on a monthly basis. This September, service revenues grew by 8.6%.

The board anticipates that full year results will be in line with expectations with a strong trading performance in September of 9.3% like for like new retail volume higher than the 5.9% increase in UK private registrations along with an 8.6% September growth in service revenues. The relative strength of both the UK economy and Sterling means that European manufacturers are likely to continue to direct high volumes of vehicles to the UK as they seek to manage European factory overcapacity. This is clearly a positive trend overall but it does impact on margins to generate the volume required.

During the period the group opened a net five new outlets and as far as acquisitions are concerned, they acquired Hillendale, representing a Land Rover dealership in Nelson and a Jaguar dealership in Bolton for a total consideration of £7.9M including £2M of shares in Vertu issued at 58.64p with the remainder coming from cash. The excess over the net asset value of the acquisition is £6.9M. In August the group acquired part of the business of Addison Motors trading as Benfield Alfa Romeo, Benfield Chrysler, Benfield Jeep and Benfield Fiat Service centre in Newcastle for a total consideration of £398K funded from cash reserves. There is apparently a strong pipeline of acquisition opportunities going forward. Last year’s purchase, the Farnell Land Rover group made a substantial contribution to the growth in profit.

As well as business acquisitions, the group has also been acquiring property and land on which to expand organically. During the year they acquired a leasehold property in Newcastle which it opened in August as a Fiat Brand Centre, representing Fiat, Alfa Romeo and Jeep and it now has three dealerships in this area of the City. In addition, they acquired another leasehold property in Newcastle in which they opened their first Infiniti dealership. This outlet is located within 10 miles of the Nissan factory in Sunderland where the Infinity Q30 model range will be manufactured from next year and it is the only Infinity sales outlet in the whole of the North East of England. Conversely the group closed an accident repair centre in Birmingham to allow capacity to be increased for retail vehicle sales in the central Birmingham location, which is interesting considering the higher margins for service centres. They continue to operate 10 accident repair centres.

After the end of the period the group acquired a freehold dealership property in Leeds for £5M which will become their premier Land Rover dealership. In Birmingham the group closed its Bristol Street Motor Nation used car operation to free up the premises to be used as an additional vehicle compound for the growing Ford commercial fleet business, which is adjacent to the site. As far as board changes are concerned, Peter Jones starts as Chairman on the 1st January 2015.

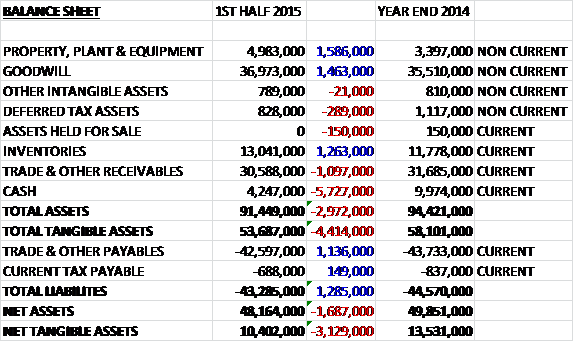

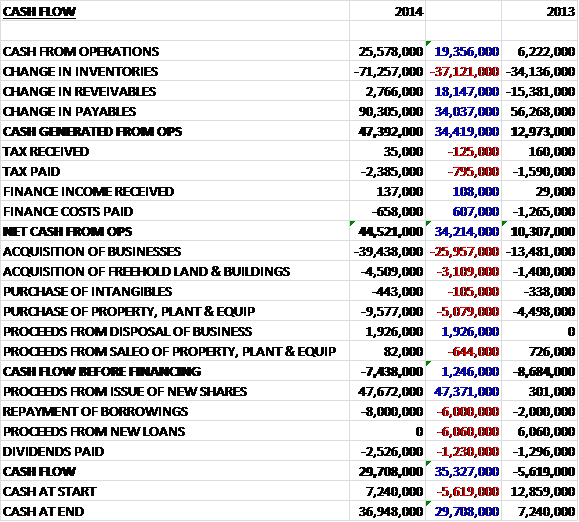

At the end of the period net cash stood at £34.4M, an improvement on both the £25.7M of net cash this time last year and the £31.4M figure at the end point of 2014. An interim dividend of 0.35p has been announced which is a 16.7% increase on last year and represents a 1.5% dividend yield for the full year at the current share price.

Overall then, this is a good set of results. Profits are up and seem to be healthy across all business sectors, net assets have increased and there is a decent free cash flow. The fortunes of the group are closely linked to those of the UK, and to some extent mainland Europe so the question has to be asked as to whether this situation is likely to continue for the foreseeable future. Despite this slight concern, though, I see Vertu as a quality outfit and I will attempt to look for an entry point.

On the 16th October it was announced that the new Chairman, Peter Jones has doubled his share holding to one million shares which equates to 0.29% of the share equity. The transaction cost him £56,810 but as he is new I guess he is probably expected to be acquiring some of the equity.

On the 5th November the group announced that it had acquired The Taxi Centre and Easy Vehicle Finance, who source vehicles for the private taxi sector. The group is based in Scotland and employs 8 people. The total consideration was £700K of which £200K is in the form of Vertu shares. Despite the acquisition coming with a leasehold office property, there is clearly a net liability as goodwill for the transaction is £1.1M. In addition to this, there is an earn-out arrangement whereby the vendor will earn 20% of the pre-tax profits of the Taxi Centre over a three year period. In the year to Dec 2013, the acquired group made EBITDA of £400K and management expect it to be earnings enhancing in its first year. This seems like a decent small, niche purchase to me.

On the 10th November the group announced that it had acquired Gordons Ltd that consists of two Ford main dealerships in Bolton and Wigan along with two satellite operations in Walkden and Horwich. The group will pay £11M in cash for the acquisition and Gordons comes with considerable assets including four freehold properties valued at £6.9M. Indeed, no Goodwill was paid on the acquisition. During 2013, Gordons generated revenues of £76.7M and an operating profit of £300K with the dealerships expected to be earnings neutral in the first full year of ownership and earnings enhancing during the year ending 2017. This transaction increases the representation to 22 Ford outlets in total and although they do not seem to be very profitable at present, the price paid seems good bearing in mind the assets gained and once Vertu has worked its magic, margins at the acquired outlets should improve.

On the 2nd January the group confirmed the appointment of Peter Jones as Chairman as Paul Williams retired after seven years as Chairman. Peter has been Commercial Director of Inchcape and CEO of Brammall and Lookers so he seems to come with some considerable pedigree.

At this point I thought I would try something different and take a look at the chart. Since the start of 2014 the trend seems to be trending between about 52p and 65p and definitely seems range bound. After a brief upturn in October, the share price definitely has downwards momentum and it will be interesting to see if there is support around 55p. If so, it could be a decent entry point.

On the 5th March the group released a pre-close trading update. In 2014 there were nearly two and a half million new car registrations in the UK which was the highest amount since 2004. The five months ending January 2015 saw a tightening of trading conditions from the recent highs and while the new car market continued to grow, in January the private retail market for new cars fell by 5.1% which was the first decline for a number of years. The high market sales volumes continued to be driven by the push of new cars by vehicle manufacturers into the UK due to the combined effects of the weakness of the Eurozone’s new car demand and the strength of Sterling against the Euro.

Apparently retailers have been self-registering vehicles to achieve the growing volume targets set by vehicle manufacturers which has clearly created a disconnect between actual sales to private customers and official registration levels with those self-registered vehicles being sold to private customers as used vehicles which is how the group is explaining its 0.5% like for like increase in new car sales against the 5.4% official increase in private registrations recorded by SMMT. Some good news is that the like for like gross profit per unit has slightly increased.

Like for like commercial vehicle sales grew by 16.7% during the period against an 10% increase in UK commercial van registrations as a whole and the group maintained its like for like profit per unit. The UK used car market saw a more typical seasonal deprecation cycle after a period where margins had been holding up well and margin pressure increased in the period as a consequence. Against this background, like for like sales of used vehicles grew by 6.4% but gross profit per unit declined slightly during the period. The group increased like for like revenues in each of its major aftersales channels and overall they grew 1.8% in the period with margins strengthening slightly.

Since the end of last year, the number of sales outlets increased by 11 with the Gordon’s Ford dealerships acquired trading in line with plans whilst it undergoes integration into the group. One of the dealerships will relocate next month to a new purpose build freehold property and a location acquired as part of the acquisition will be sold for £700K. In December the group disposed of a Nissan dealership in Altrincham which realised cash of £700K. In January, the opened a Renault and Dacia dealership in Nottingham with a Honda motorcycles sales and service outfit being built on the same property. In addition to the new premises, the group is redeveloping and improving a large number of dealership properties which will result in an increase in capital expenditure levels in the near term.

The board believe that the results for this year will be in line with current expectations with a significant net cash level. The UK new car market seems to be stabilising at a high level after a long period of growth whilst the used vehicle market is likely to see an increase in the volume of cars entering the market which should increase sales numbers but weaken margins. March remains the most important month for the profitability of the motor retail sector and current evidence suggests that this March may be a record month for total UK new vehicle registrations with the group’s like for like order book currently running ahead of the prior year. Meanwhile the board continues to examine further acquisition properties.

Whilst a record profit for the group is clearly positive, there are some notes of caution here. Whatever the cause, the sale of new cars seems have slowed somewhat to just 0.5% and used car margins are now being squeezed. Added to this is the fact that the UK new car market seems to be levelling off, albeit at a high level and the group are going to be increasing capital expenditure next year which leads me to believe on the limited evidence we have so far, that next year may not be another record year. There is no doubt that this is a quality investment but I feel there may be some short term issued to overcome first.

Also on the 5th March it was announced that finance director, Michael Sherwin had purchased 13,141 shares at a cost of just under £7,500 to leave him with 361,326 shares. Whilst it is nice to see directors putting their money where their mouths are, this is quite a modest purchase for a man who owns more than £200,000 of the stock and earned a total of £440,000 (including bonus and benefits) last year.

Conversely, on the same day we see Schroders selling 6,717,787 shares netting them £3,822,421 which rather dwarfs the director purchase. After the sale, Schroders now own just under 3.5% of the company’s shares which is not a ringing endorsement.

On the 6th March it was announced that CEO Robert Forrester joined his finance director in buying some shares, this time 17,451 at a value of just under ten grand. Again, nice to see, but peanuts to a man who owns £3,778,930 of the company’s shares already and does not really change my opinion at the moment.

On the 1st May the group announced the acquisition of Bury Land Rover and Bradford Jaguar. Bury Land Rover was acquired from Pendragon for a total of consideration of £7M, all of which represents goodwill paid and was settled in cash from the group’s reserves. In 2014 the dealership showed revenues of £41M and EBITDA of £1.5M and the board expects the acquisition to be earnings enhancing in the current year. The group already operates the Jaguar dealership in the same territory. Bradford Jaguar is being acquired from Lancaster PLC for a total consideration of £900K, including £750K of goodwill and will be settled in cash from existing resources. In 2014 the dealership had revenues of £14.7M and made a loss of £150K. The board expects the acquisition to be earnings neutral in the current year and earnings enhancing from then on. Following these acquisitions the group now owns five Land Rover dealerships and two Jaguar outlets. The price paid for the Land Rover dealership looks quite high but this is a profitable outlook so should be good for the group going forward.