President has now released its interim results for 2014.

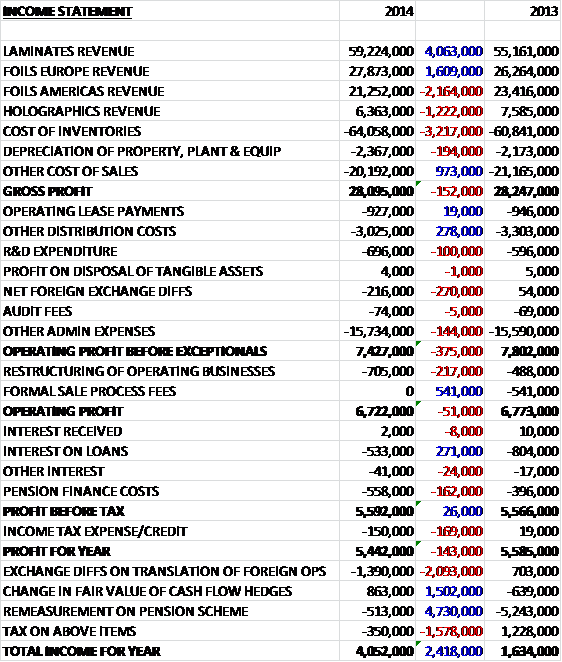

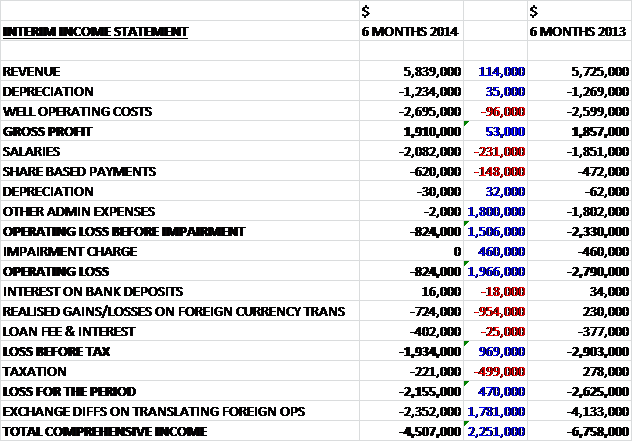

When compared to the first half of last year revenues were broadly similar, increasing by $114K as increased production was counteracted by a slight decrease in oil prices in Louisiana and whilst depreciation was slightly lower, this was offset by a $96K increase in well operating costs which gave a gross profit of just $53K more. There was a $231K increase in salaries and a $148K hike in share based payments but other admin expenses were much lower reflecting a $1.8M capitalisation of costs relating to the Paraguay drilling campaign to give an operating loss of $824K, a near $2M improvement over the first half of last year which also included a $460K impairment charge relating to the relinquishment of the PEL 132 license in Australia. Finance costs increased, though, driven by a near $1M adverse swing in realised foreign exchange transactions and taxation was half a million dollars more so that the loss for the period was $2.2M, an improvement of $470K over the first six months of 2013.

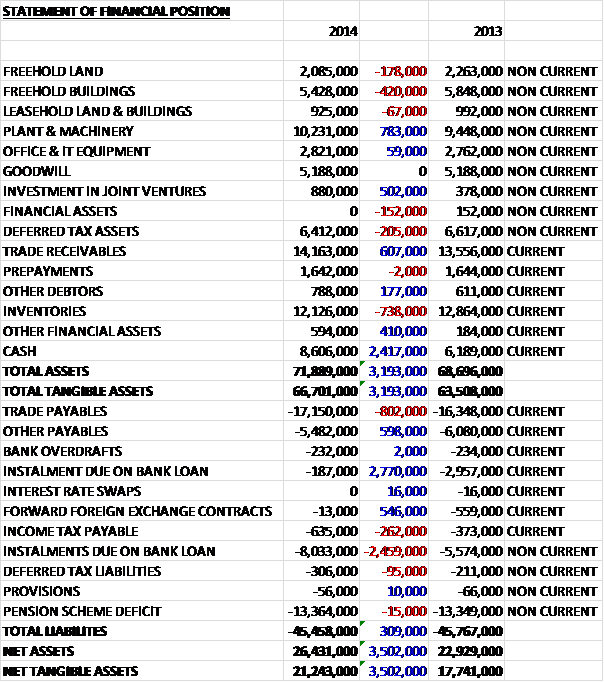

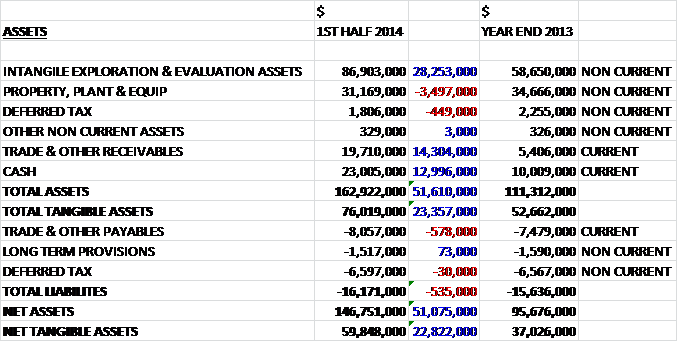

When compared to the end point of last year, total assets increased by $51.6M driven by a $28.3M increase in intangible exploration assets, a $14.3M growth in receivables relating to prepaid exploration expenditure and a $13M increase in cash levels, only partially offset by a $3.5M reduction in property, plant and equipment. Liabilities were broadly similar with the $535K increase almost entirely due to an increase in payables. This means that net assets were $51.1M higher than the end point of 2013 but until the results of the well are known, those exploration assets could be impaired.

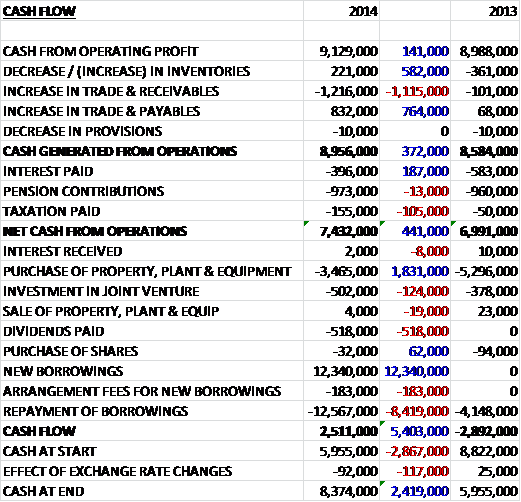

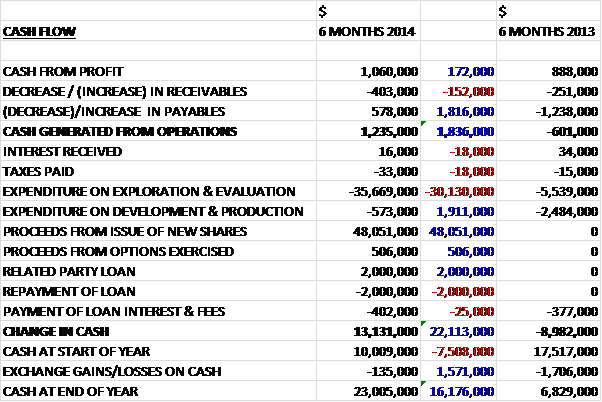

Before movements in working capital, cash profits of $1M were $172K higher than in the first half of last year. An increase in both receivables and payables, with the latter increasing by more meant that cash generated from operations was $1.2M compared to an outflow of $601K in H1 2013. The main origin of cash was the issue of new shares, however, which netted the group $48.1M. The vast bulk of this was spent on exploration and evaluation, accounting for $35.7M with just $573K being spent on development and production with a further $402K being spent on payment of interest and fees on loans. This resulted in a cash inflow of $13.1M with the cash position at the half year point being $23M.

At the moment Paraguay is the core focus for the group. The most recent seismic identified two structural play fairways each containing two petroleum systems. The first is the Cretaceous system and is an extension of the Palmar system in Argentina. The second is an underlying Palaeozoic system that was identified during the recent Jacaranda drilling that has charged the producing fields in Bolivia and Argentina. The group have entered into an 18 month contract with Schlumberger for project management and drilling services and a rig has been contracted. The results from the Jacaranda drill, although disappointing, did confirm the presence of a thick live source rock of Devonian structural leads identified across all three of the concessions. In addition, a possible unconventional source potential was identified with technically recoverable resources in the Palaeozoic areas of the Paraguayan Chaco of 67Tcf of gas and 3.2BN barrels of oil.

After the end of the period date, the group also announced that it had farmed in to the maximum 80% interest at the Hernandarias Concession and as a consequence, President now operates the entire Pirity Rift basin. It was also discovered that the Devonian shales area is estimated to hold between 20 and 28 Tcf of gas in place in shale and that this formation is expected to be present in significant thickness throughout the group’s acreage and that the formation shallows to the north and is expected to be in the oil window.

In Argentina the operator at Puesto Guardian has sought to focus on cost efficiencies given the difficult political and economic situation in the country. After the period end, President took control of 100% of the concession and has become the operator which takes the Proved and Probable reserves up to 13 mmboe. The concession is now contributing $150K in cash per month to the group and a reserves audit should confirm the results of the 2013 well stimulation campaign by the end of 2014. At the other two concessions of Mattoras and El Ocultar, processing of historical data and lab studies are underway. Average net production for the period increased from 153 to 171 bopd and post-acquisition, the current net production is 300 bopd with the average realised prices increasing by $3 per barrel to $74.

In Louisiana, average production remained consistent at 218 boepd but average realised prices fell from $108 per barrel to $102. After the period end, a new discovery well drilled at East Lake Verret, the Eagle Crest well, established gross initial production in August of 492 bopd and 2,312 mcf of gas per day. The group has a 3% royalty at Eagle Crest and a 12% working interest coming into effect following well pay out, expected to be mid-2015. They also manage production handling at the well which generates additional income. Additional exploration prospects at both East Lake Verret and East White Lake are being evaluated and current production in Louisiana is averaging about 230 boepd prior to the inclusion of the new well. In Australia, the group’s PEL 82 block is continuing to be technically evaluated and is the subject of farm out discussions.

Clearly the results of the current drilling campaign in Paraguay are going to be the catalysts for the group. Management have done a good job talking up the prospect and it does seem as though the current well being drilled is the best bet for some hydrocarbons. In Argentina and Louisiana, there seems to be a decent job being done of increasing production but the recent oil price will not do the group much good. At the moment I feel it is a case of waiting for the results of the latest drill but I feel no need to invest further at this time.

On the 1st October the group announced that it had completed the first stage of drilling on the Lapacho well and has cased the well to a depth of 3,200m, approximately 1,100m above the projected start of the target reservoir. The timing of the well is on track with target depth still expected to occur on approximately the 11th November with the target reservoir not expected to be intercepted until towards the end of the drilling timetable.

On the 20th October the group announced that it had made an oil discovery in the Lapacho well. They have found two conventional oil bearing pay zones in the Devonia Icla Formation at a depth of 3,926 metres. This formation was not the original target of the well and the well is now setting casing at the base of the Icla Formation at a depth of 4,127m before drilling ahead to test the target underlying Devonian Santa Rosa Formation. Side wall cores are bleeding live oil in the type of light oil and condensate and flow testing will be conducted at the end of November when the well reaches final target depth. Given the good matrix porosity and the abundant natural fractures, hydrocarbon flow rates are expected to be commercial on a stand alone basis. The size of the discovery is still to be determined but seems to extend over at least the crest of the large underlying Santa Rosa structure. The drill remains on time and within budget with TD to be reached around the middle of November.

At the previously drilled Jacaranda well, a long interval of liquid hydrocarbon saturation has been identified in the Jacaranda structure lying within the Devonian shales of the Los Monos/Icla Formations. The liquid hydrocarbon saturation occurs between a depth of 4,150 and 4,400 metres and appears as a continuous saturation of 250 metres within the shales. This find increases the chance of success to discover liquid hydrocarbons in conventional sandstone reservoirs below 4,000 metres. Therefore, after the Lapacho well is finished, the group intends to re-enter the Jacaranda well to deepen it in order to encounter the same Icla sand liquid bearing pay zones as just discovered at Lapacho below the current TD at Jacaranda. The costs of this will be met out of the Company’s existing cash reserves and would mean that the tapir prospect will be addressed at a later date. There is clearly still a long way to go before commercial production is a reality but things finally seem to be happening for President and I am pleased to hold not the shares have returned to a break even point.

On the 17th November the group updated the market regarding progress on the Lapacho well. The well has now been drilled to a depth of 4,490m since setting casing at 4,125m. They have now drilled the upper section of the Santa Rosa Formation and considers it is drilling a series of gas or gas/condensate sands. Management are encouraged by a constant background gas ranging from 3% to over 12% in the circulated drilling mud to surface throughout the drilling of the hole. The group now plan to drill to the base of the Formation to a depth of 4,600m. Due to the extended drilling period, a further announcement will be made towards early December. This seems pretty hopeful if rather uncommittal, it is also clear that the drill is taking quite some time to complete (no reasons were put forward for this). The market did not like the update but I see it as a wait and see situation at this time.

On the 1st December the group released a statement covering the Puesto Guardian transaction. Due to the seller urgently requiring cash, President will immediately pay $800K to the seller and the deferred consideration of $1.9M and a 5% overriding royalty on production will be cancelled. Therefore the total price paid for the 50% ownership of the concession is $5.8M as opposed to the contingent sum of $17.9M agreed previously. The group have also completed an intial review of the concession with supports the company’s view that there is a strong potential for significant production and reserves upside. This is all good, positive stuff on an unplanned acquisition but I am a bit concerned that last time a positive update on Argentina was followed by disappointing news in Paraguay, which is the real potential prize here.

On the 10th December the group released an update for the Paraguay drilling campaign. The Lapacho well reached TD at 4,543m in the Santa Rosa formation with 418m of the 600m target interval drilled. Hydrocarbon shows have been encountered throughout the formation thickness extending to TD with a background gas of up to 20% and trip gas of up to 48%. The full logging program was restricted due to difficult downhole conditions but from the logs obtained, the well generated 54m of clean sandstones with individual sand bed thickness up to 10m, most of which appear to be hydrocarbon bearing. Some additional 30m or so of additional sandstone is expected in the undrilled target interval section below current TD, suggesting a total thickness of more than 80m of Santa Rosa reservoir at this location.

Management value the resources at approximately $12 per boe for natural gas and $25 per barrel for liquids. The rig is now progressing to open hole well testing operations and a multi-rate test is planned to commence in the next few days to determine fluid type, flow rates, pressures and permeability. On completion of the Santa Rosa test, the separate shallow discovery in the upper Icla formation will be tested and an update with the initial results is planned in 10 days, on Christmas week. This is encouraging stuff but the real confirmation comes with the test results, so not so long to wait now.

On the 11th December the group announced a significant increase in reserves at the Puerto Guardian area. 1P Proven oil reserves increased by 333% from 2011 estimates to 9.1 MMBbls; 2P Proven and Probable oil reserves increased by 114% to 14.1 MMBbls; 3P Proven, Probable and Possible oil reserves of 17.5 MMBls were shown and Contingent resources of 3.2MMBbls, 8.9MMBbls and 16.5MMBbls respectively related to concession extensions for which application is being made. The group are looking to start development work on the concession in earnest in Q1 2015 with a view to increasing production so this update seems pretty positive.

On the 29th December the company sneaked out a statement regarding the all important information on the flow rates of the Paraguay drill. Unfortunately it seems this endeavour has been beset by problems. Hydrocarbon flow testing has been hampered by mechanical failures due to poor hole conditions but the presence of mobile gas condensate was confirmed in the Santa Rosa formation. With the Icla rest not being valid, a re-engineered well design and re-drill of the Lapacho x-1 well will be required to established sustained commercial flow rates.

At the Santa Rosa test, the well initiated flow at a rate of 107 barrels per day but the test had to be prematurely terminated after producing just 14.2 barrels of fluid due to a serious mechanical failure in the bottom of the test string that prevented inflow. After a check confirmed the blockage, a check trip was performed and elevated gas readings of greater than 20% total gas was encountered. Given the deteriorating hole conditions and high risk of hole collapse under an extended testing program it has been decided no to attempt a repeat of the test but to suspend the open hole section for later re-drilling by side tracking. Despite the problems with this test, given optimal drilling techniques, management are of the view that Santa Rosa can be commercialised.

At the Icla test, during two flow periods a total of 110 barrels of gas cut formation water with no traces of oil were obtained but the higher salinity of this water does not correspond to the characteristics of the Icla Formation, but instead indicates it came from the overlying Cretaceous Pirgua Formation above 3915m. This suggests that this is not a valid test of the Devonian hydrocarbon bearing interval previously evaluated. The cementation of the 7″ liner was executed successfully but the cement bond log shows poor quality cement over the Cretaceous Pirgua Formation which immediately overlies the Icla Formation. It is concluded that communication exists with these overlying sands annd given the cost of mobilising equipment for a squeeze job and generally low chance of success of these operations, the interval was suspended for future re-entry.

It is thought that the Hernandarias has the two intervals at a shallower depth so the intention is to attempt drills here instead. Line clearing for seismic in Hernandarias has been completed and planning for a new round of seismic acquisition is underway. The rig will be released with a view to resume the drilling program in the summer of 2015. The company’s cash flow from Argentina and Louisiana when combined with the loan facility provides financial flexibility (whatever that means). So, this is all terribly disappointing and it seems we will have to wait until mid 2015 for any further news on Paraguay. The highlights on the RNS are not helpful in my view, so my “highlights” as I understand them are as follows:

1. Testing on the Santa Rosa formation failed due to mechanical failure on the drill –

2. Testing on the Icla formation failed due to the lack of proper cementing on the top of the formation, causing it to be contaminated by the non oil bearing sands above.

3. Hole conditions are such that it had to be capped, ready to re-enter at a later date

4. The next drill will occur at Hernandarias where these formations are nearer the surface.

5. The cash levels and financing requirements are unknown.

6. There remains a huge amount of potential for a commercial discovery in Paraguay.

Understandably the shares have tanked on this news but I still hold out hope that a commercial discovery will be made so I am not selling out at these levels.

On the 8th January the group announced that Harvison Capital Management had sold 2,360,217 shares to bring their interest down to under 4% of the issued capital, which is not a great vote of confidence.

On the 8th January the group gave an update on the Louisiana operations. For 2014, there was an estimate operating profit of $5M with an average production level of 225 boepd and a 2014 exit rate of 230 boepd. The effect of lower oil prices is being mitigated by reduced operating expenses and the continued utilisation of tax losses and new producing wells. The resilience of the operations is largely due to the present and forthcoming contributions from the two existing non-operated producing wells at East White Lake and East Lake Verret. In particular the Eagle Crest well at East Lake Verret. This is a large well, producing about 1,000 gross boepd with revenue set to increase further as a result of the farm-out terms agreed which enable President to be fully carried for all drilling expenses, receive a 3% gross royalty override, a further 12% working interest on pay out of a capped level of drilling costs and fees from an underlying Production Handling Agreement.

Currently the group benefits from the GRO and received a net contribution of $18K per month for processing facility fees. At the current production levels it is expected that President will become entitled to its further 12% working interest in mid 2015 which will increase the group’s share of production to 150 boepd (from just 30 boepd). Another benefit is that the group can continue to utilise tax losses to keep the effective tax rate at zero for the next three years or so and $200K per annum in management expenses has also been taken out. The group are likely to update on the Argentina operations next month but realised prices in the country remain robust at over $77 per barrel. Although this update doesn’t make up for the disappointments in Paraguay, cash generation in Louisiana seems to be quite robust.

On the 15th January the group announced that due to the lower oil price environment (and no doubt partly due to the disappointment in the 2014 Paraguay drilling programme) CEO John Hamilton, COO Dr. Richard Hubbard and non-executive director Dr. Michael Cochran have stepped down. As a result, Peter Levine will become CEO as well as executive chairman and Miles Biggins who is the current Commercial Director will become the new COO. As the oil price has fallen and made it less easy to justify large exploration programmes, the group is now focusing on their producing areas and as such Carlos Morales has joined as Manager of the Argentine operations. He is a senior operations geologist and petroleum engineer having been with YPF for 16 years including as the geologist on President’s Puesto guardian fields.

On the 26th February it was announced that Norges Bank sold over 3.5M shares in the company at a value of about £505K. They now own 3.21% of the company and this is not a ringing endorsement of the company if they are willing to sell so much at such a modest price.

On the 27th February it was announced that Harvison Capital Management sold nearly four million shares at a value of about £550K. they now own under 3% of the share capital of the company. I am not too sure who they are but they seem pretty keen to get rid of a fairly high number of shares at this low price and being the second large sale in as many days, the omens do not look great here.

On the 3rd March the group announced that the partner in the Pirity Concession, Petro Victory, has initiated court proceedings against the group. Management believes that the claims made (I am not sure what they are) are without foundation and that Petro Victory continues to be in default under the relevant joint operating agreement having failed to pay its contribution to the work programme amounting to $1.8M. As a consequence of this, the group has the right to require that Petro Victory transfer its interest in Pirity at a discounted value as of the 3rd March. This is all starting to get rather messy.

On the 4th March the group released an operational update on its Paraguay and Argentina assets. After last year’s focus on Paraguay, it seems that Argentina will now be the subject of the group’s attentions. It seems that only 8% of the 9 MMbbls pf proved oil reserves at the Puesto Guardian concession in Argentina are being produced which suggest there is potential for further production from the proves reserves as well as from the further 8.4 MMbbls of provable and possible oil reserves. Since acquiring a 100% interest in the concession the group has carried out further analysis and is now ready to embark on a multi aspect work programme including a combination of work-overs and new wells. In addition, the company will commence a farm-out process of a potentially significant gas prospect which was identified more than three years ago but was not targetted until President took control of the concession.

The phase 1 programme involves the work-over of up to 10 shut in wells with proved oil resources, expected to commence this Spring. A rig has been sources that will carry out at leas the first part of this programme with the expected uplift in production benefiting from the government’s recently announces incentive scheme of an additional $3 per barrel realisation price for each increased barrel produced over the existing production. The phase 2 programme is currently targeted to start during the latter part of 2015 and is subject to adequate finance being in place. It consists of 17 new wells to be drilled targeting proved oil reserves. The locations have already been identified and current projections are that after between $25M to $30M of development finance, the phase two programme will become self funding.

Application is being made under new legislation relating to unconventional hydrocarbons recently enacted to obtain extended license terms over the group’s concessions. It is hoped that they will be approved before the end of 2015 and if granted the end date of the Puesto Guardian concession would become 2050 and the result would likely be an increase of 16.5 MMBbls in the proved, probably and possible oil reserves that currently stand at 17.5 MMBbls.

Preparations are being made on a farm-out process, starting in March for the 100% owned deep Palaeozoic gas prospect at the Martinez Del Tineo field in the Puesto Guardian concession. It is assessed that this prospect had unrisked recoverable prospective resources of 570 Bcf of gas and 14.5 MMbbls of condensate with an NPV10 value of $1.03BN at historically low prices and initial interest has apparently been shown by “major industry players”. Realisation prices in Argentina are currently $70 and production continues to show a modest operational profit. The group is continuing to undertake studies to evaluation the prospectivity in the Palaeozoic at the wholly owned Matorras and El Ocultar concessions that are adjacent to Puesto Guardian.

In Paraguay the group commissioned a 600km 2D seismic acquisition programme on the Hernandarias concession targeted to commence in Spring with results expected two months later. The analysis of this year’s drilling results confirm that the block is very prospective. There are three leads, Boqueron, with a possible 160 km2 trap area, Labon with possible 35 km2 trap area and Tuna with a possible 40 km2 trap area and are all considered to present information to contain the Devonian and Silurian packages identified in the Jacaranda and Lapucho wells, although at shallower depths of between 2000m and 3000m. As recently announced the partner on the Pirity concession has failed to pay about $1.8M to contractors which President has covered for the time being but little more is likely to happen until the court process has been concluded. The group production for the year as a whole averaged 430 boepd with Louisiana contributing 225 boepd. There were cash levels of just $1.4M at the end of January with $10.4M drawn under the $15M IYA loan facility which leads on to the next announcement…

Also on the 4th March the group announced fundraising that involved the firm placing of over 29M shares and a proposed placing of 43M shares at 12.5p per share together with 1 warrant for every 1 new ordinary share subscribed for which have an exercise price of 18.75p per share and a three year exercise period. The proposed placing should raise $14M and will be used to fund the commissioning of the 2D seismic survey across the Hernandarias concession in Paraguay ahead of a potential farm out; the commencement of multi aspect work on the Puesto Guardian concession in Argentina and to support the working capital position of the company through to 2016. As part of the fund raising the $15M IYA loan will be extended for a further year.

Overall then a lot has happened for President over the past couple of days. The situation with Petro Victory is not ideal and a bit of a distraction but the plans for Argentina sound like a good idea. The fund raising. By my calculations the potential dilution of the fund raising will be about 18% which is not catastrophic but another potential reasons not to own the shares. I actually sold out here last week as I didn’t like the long wait for information and I felt (still do) that there is little potential here until the oil price improves despite the fact that the Argentinian price does not seem to be directly correlated to the market price. I will keep a close watching brief here for now.

On the 9th March the group announced that it had been assigned the first 40% of an up to 80% interest in the Hernandarias concession. It has $15.4M remaining to spend to earn the full farm in entitlement with the $4M allocated to the purchase of 600km of 2D seismic as a use of funds from the placing counting towards this total. Also, the company has received a certificate of good standing from the Vice Ministry of Mining and Energy of the Ministry of Public Works and Communication in relation to the Pirity concession stating that as operator of the block, President has fulfilled all of its obligations and has complied with all filings and reporting obligations and the annual work programme.

On the 8th April it was announced that Baillie Gifford, an investment manager, had sold shares to take their stake below 5%.

On the 12th May the group released a statement that the dispute between themselves and Petro Victory had reached an amicable resolution and all claims and actions have been discontinued. There is no indication of what that amicable resolution involves.