TT Electronics has now released its interim results for the year ending 2014.

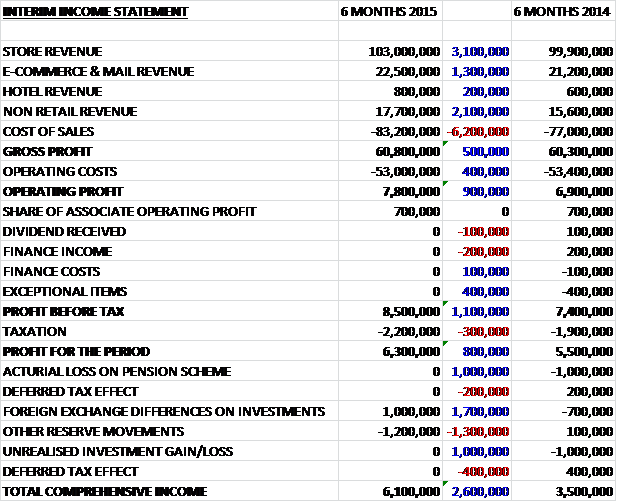

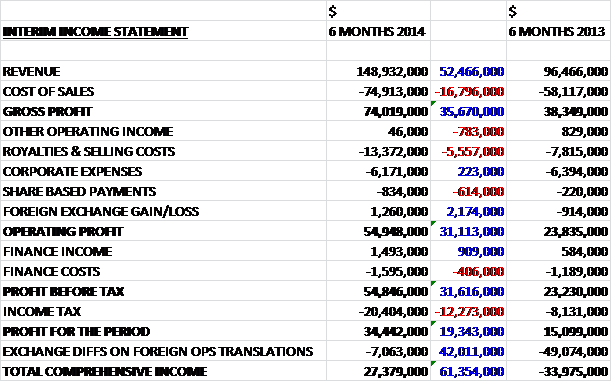

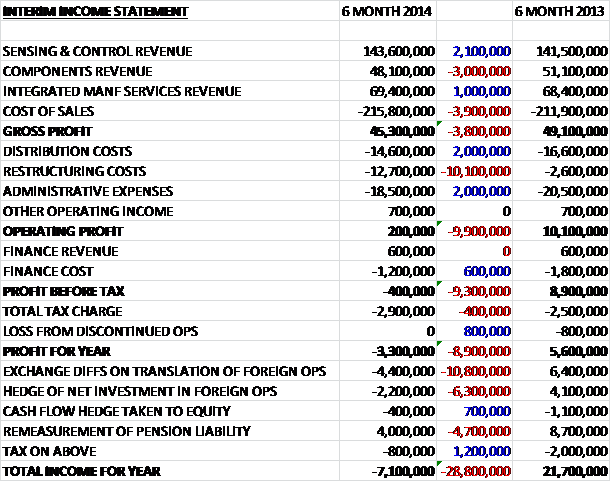

Overall revenues remained flat as small increases in Sensing & Control sales, and Integrated Manufacturing Service revenues were mitigated by a £3M reduction in Components revenues. Cost of sales increased, though, so that gross profits were £3.8M lower than during the same period of last year. A £2M reduction in both Distribution costs and Admin costs were dwarfed by a £10.1M hike in Restructuring costs so that operating profit collapsed by nearly £10M to just £200K, although it is worth noting that there would have been a slight increase in operating profit were it not for the one-off costs. Finance costs improved on the first half of last year but were still higher than finance income before a £400K increase in taxation meant that the loss from the half year period was £3.3M compared to a profit of £5.6M in the first half of 2013.

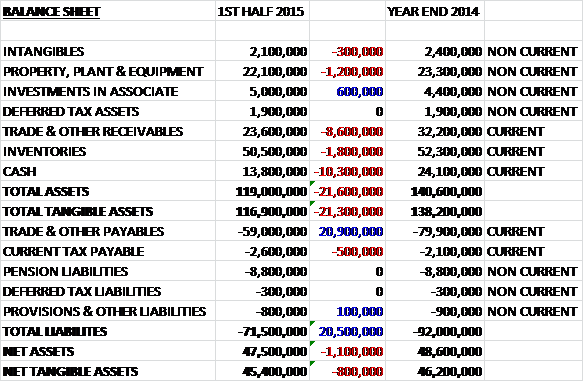

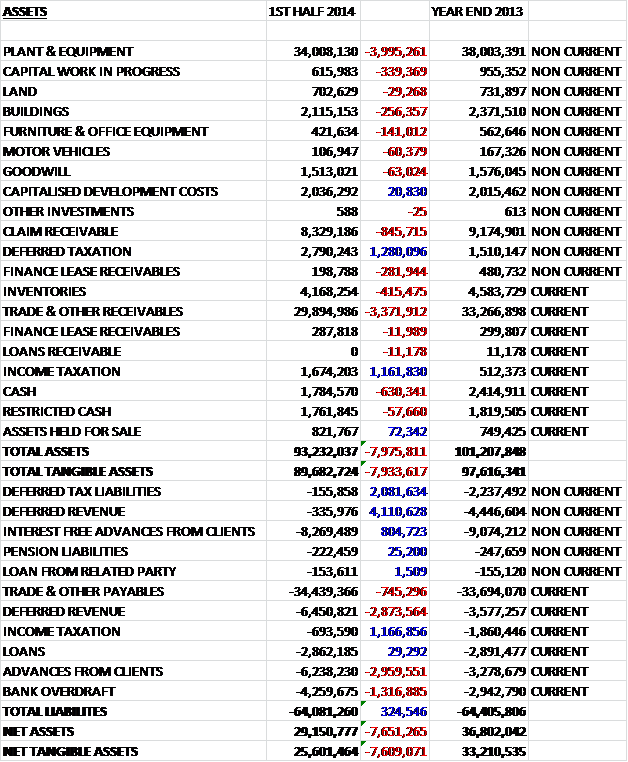

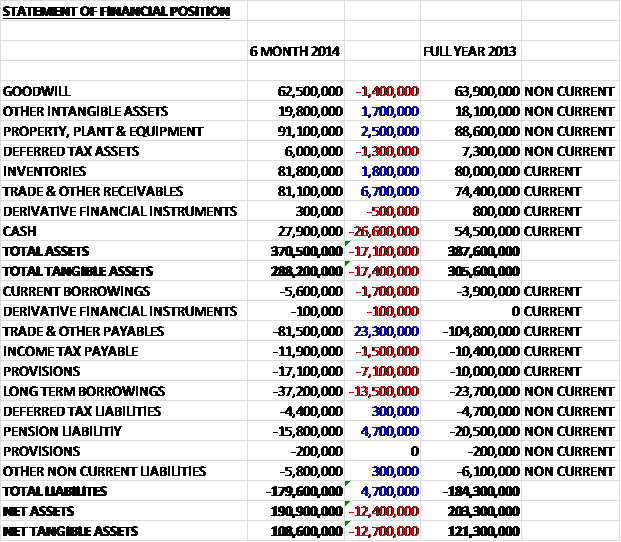

Overall assets fell by £17.1M when compared to the end point of last year. This decrease was driven by a £26.6M collapse in the cash levels, somewhat mitigated by a £6.7M increase in receivables, a £2.5M growth in the value of property, plant and equipment and smaller increases in other intangibles and inventories. Liabilities also fell, driven by a £23.3M reduction in payables and a £4.7M fall in pension liabilities, counteracted by a £15.2M increase in borrowings and a £7.1M growth in the value of provisions. Overall this still meant that net assets fell by £12.4M to £190.9M.

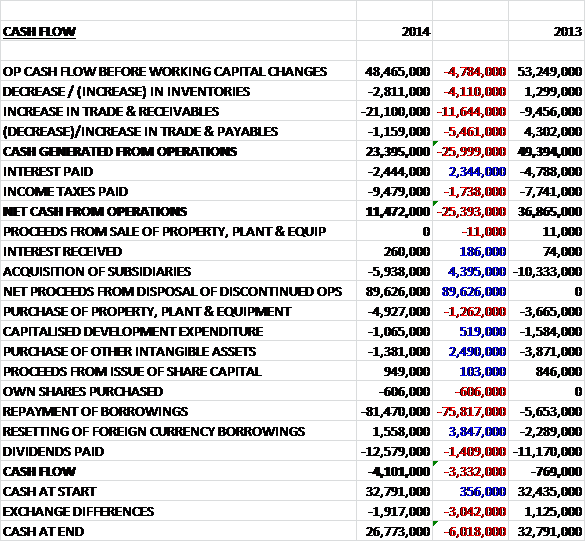

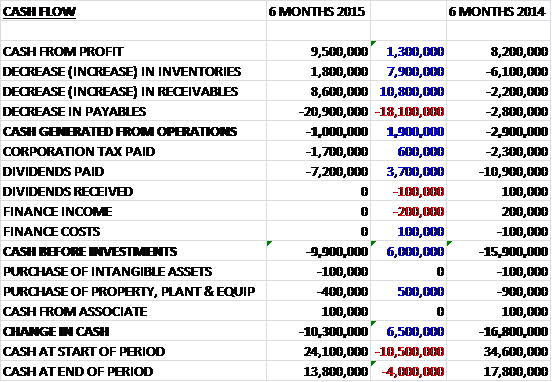

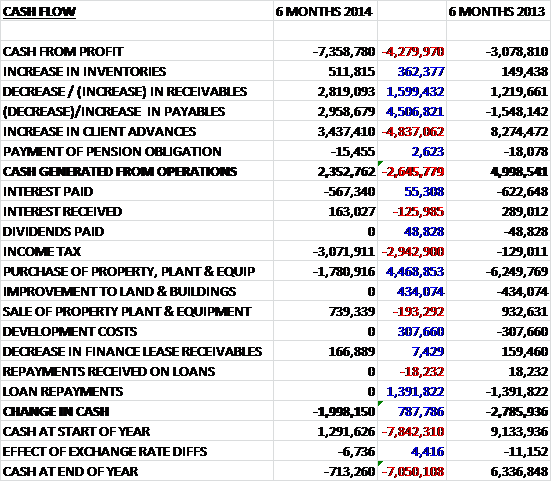

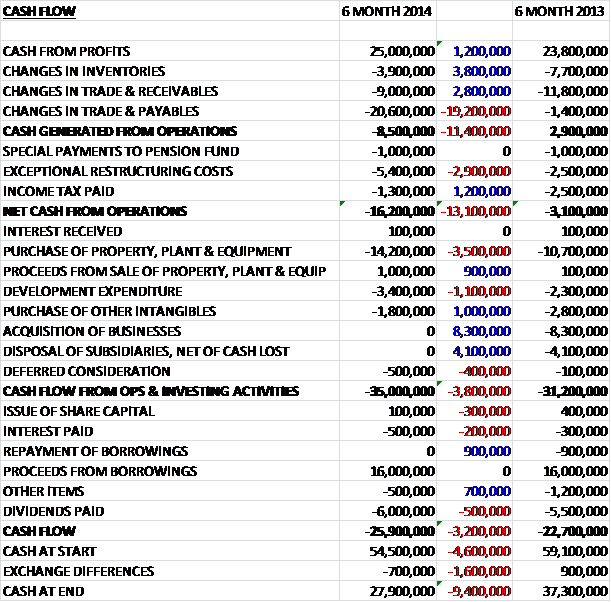

Before movements in working capital, cash profits at £25M were £1.2M higher than in the first half of last year. Unfortunately adverse working capital movements, in particular a £20.6M reduction in payables due to significant supplier payments, meant that there was an £8.5M outflow of cash from operations, £11.4M worse than in 2013. This outflow widened to a £16.2M outflow after payments to the pension fund, restructuring costs and tax. On top of this £14.2M was spent on property, plant and equipment which included a new signal conditioning product line in the Resistors business and expansion of the Romania facility, but this was broadly accounted for by a £16M increase in borrowings before a £6M spend on dividends pushed cash flow to a negative £25.9M, £3.2M worse than in the first half of 2013. Matters improved last time in the second half but this is still a disappointing result.

Under the Operational Improvement Plan a number of sales offices have been closed and line transfers from the California facility to Mexico have progressed, although the transfer of some product lines has been put on hold in order to fulfil a customer order with the transfer of those lines now expected to be made in 2015. One issue that the group have found is that the proposed transfer of manufacturing from the German factory to Romania has come up against trade union disapproval whilst the Romanian site has already been approved by some customers. Another issue is that of currency movements. During the period the strong pound reduced revenues by £10.6M and operating profit by £1.1M.

The Sensing and Control business has made some investments in new product development, increasing capabilities in R&D and establishing a team focused on Microelectromechanical Systems (MEMS). This technology enables very small, low power sensing devices and innovation in this area is likely to improve the offering of next generation pressure sensors. Operating margins in the division have fallen from 6.6% in the first half of last year to 4.6% in the first half of 2014 and operating profit declined by £1.6M due to this £2.5M R&D investment and production inefficiencies as lines are moved to new factories. Revenue growth came from a strong demand in the transportation market, including a better performance from the Austrian business. The second half of the year is expected to benefit from a significant customer order.

The market for Sensing and Control products should remain robust due to increased emissions regulation and the drive for industrial power efficiency. The group launched a new product, a next generation torque sensor, during the period which enables improved efficiency for power steering systems and in the second half of the year the group has plans to move to the commercialisation phase of their chip stacking technology for power modules. They are also planning to enhance their position sensing portfolio with the addition of a rotary sensor and expand the pressure and temperature sensor offerings into industrial applications.

The Components division enjoyed an increase in margins from 2% to 7.7% and profit increased from £1M to £3.7M due to a better overall mix of products and efficiency across the business, as well as some one-off orders received before the US factory closed. Revenues, however, declined during the period as a good performance from the Magnetics and Resistors business was offset by programme delays in other areas and a reduction in volume associated with the closure of a loss making connectors business in the US. The Connectors business launched its next generation connector product addressing the increasing deployment of integrated power and data communications systems in soldier equipment.

Margins in the IMS division deteriorated from 4.1% to 3.7% during the half year and operating profit fell by £200L to £2.6M as UK sites were consolidated and some production was moved to Romania and the group suffered from adverse currency movements. During the year the business won new work from Shanghai Avionics supporting production of airborne avionics systems used on the C919, China’s first domestically produced airline. The group also established a design facility in North Carolina to support defence and aerospace customers with specialised technical expertise and product support. During the period a facility was closed in Wales and manufacturing was moved to Romania.

In all the group spent £10.2M on the improvement plan which included the moving of production from California to Mexico and costs relating to the proposed transfer of manufacturing from Germany to Romania. Other restructuring costs of £2.5M arose from the consolidation in the UK and the establishment of a Romania facility for the IMS division. Last year a triennial valuation of the UK pension scheme found that there was a £19.1M deficit, which was an improvement from the £39.4M deficit identified in 2010. An agreement was made that contributions of £4.1M, £4.3M and £4.5M will be made over the next three years to reduce the deficit. Additionally the company set aside £3M over the last three years to be used in reducing the long term liabilities of the scheme.

After the end of the balance sheet date the group announced the acquisition of Roxspur, a UK supplier of temperature, flow, pressure and level sensors together with calibration services in segments such as oil and gas, power generation, water management and materials processing. There was an initial consideration of £7.5M in cash with further £2.5M payable in cash in 2016. The acquisition will be immediately earnings enhancing.

At the end of the period, net debt stood at just under £15M compared to a net cash position of nearly £27M at the end of the year due to the working capital outflow and capital investment. The board have increased the interim dividend by 6.2% to 1.7p per share which I suppose they have to do but I would have maybe kept it the same to conserve cash. The restructuring seems to be really affecting the business at the moment, and it is sometimes hard to see how it is doing without all the noise. Both the IMS and Sensor and control divisions have seen margins eroded due to the changes and the Components division seems to have had its results flattered by one off orders. The decline in net assets is disappointing but the underlying reason for this seems to be cash outflow due to the big chunk of supplier invoices paid during the period so might be temporary. The pension deficit also seems to be a bit of a drain on cash in the short term. In the medium term, these could well end up being a good investment but I feel there is just too much short term uncertainty to take the plunge at this time.

On the 21st August, director Sean Watson purchased 216,000 shares at 171p a share which seems like quite a vote of confidence.

On the 4th November the group released an interim management statement covering the first 10 months of the year. The group has now made a final agreement with the unions in Germany and under this agreement certain lines will be moved from Werne to Romania but some manufacturing will remain in Germany for service and specific highly automated production. The overall heacount at Werne after the completion of the programme will reduce by about 45% to approximately 300-325 compared to the original target of 220. The site will continue to be used as a centre of excellence for engineering and product development as originally intended. Taking this into account, the cost of the European programme will reduce by £1M to £25M but significantly the annual cost saving going forward will be just £3.5M as opposed to the previous estimate of £6M. There have also been a number of costs this year relating to this disruption and these inefficiencies are expected to continue in 2015 with the first benefits of the programme now expected in 2016.

The closure of sales offices in Japan, France and Italy was completed on schedule by June and benefits of £1.3M per annum are being delivered in the second half. The transfer of manufacturing from Fullerton in the US to Mexico is also progressing but as previously announced some production line transfers have been put on hold in order to fulfil a significant customer order with the transfers being made in 2015. The expense for R&D in Sensors and Controls has increased by £2.3M year on year and the group are conducting an in-depth review of historical R&D spend and amounts carried on the balance sheet so it looks as though there may be some impairments imminently. There has also been a move to lower margin products in the division which have been offset this year by a significant one-off order from an existing US customer. As a consequence of these points, it is anticipated that performance will be materially lower in 2015.

The group is carrying a net debt of £30.7M but the board still expect an improvement in working capital before the end of the year and this year, underlying revenue growth over the same period of last year has been 3% but the performance for 2014 as a whole will be towards the lower end of current expectations. It seems to me that this restructuring is more complex than management originally expected and it is difficult to think about investing here before the bulk of these changes have been successfully implemented.

On the 18th November the group announced that Finance Director Shatish Dasani has stepped down after six years of service. Until something changes here I don’t see much point in investing so this will be my last update of this company for a while.

On the 13th February it was announced that Aberforth Partners had sold 92,000 shares at a cost of about £109,000 to brink their interest down to 15,862,203 shares, just under 10% of the total equity.