Keller has now released its interim results for the year ending 2015.

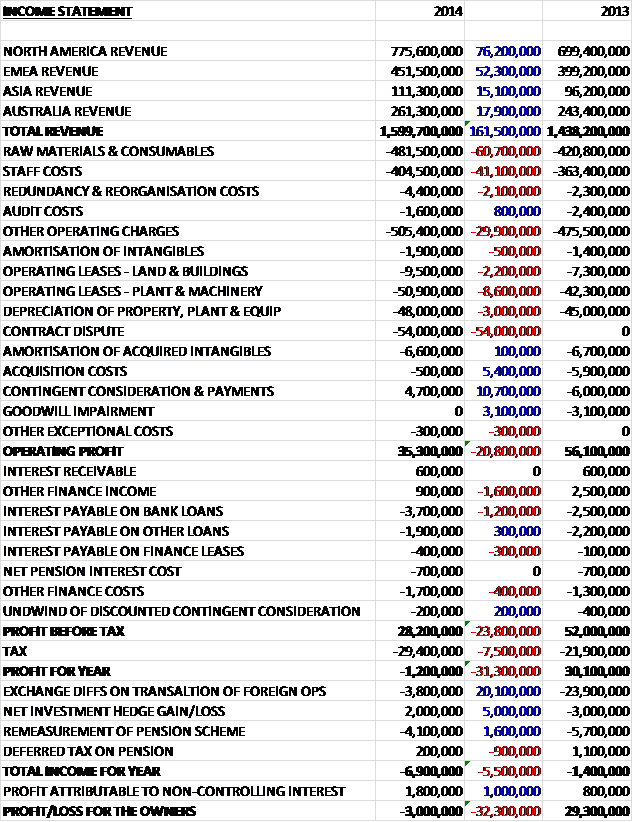

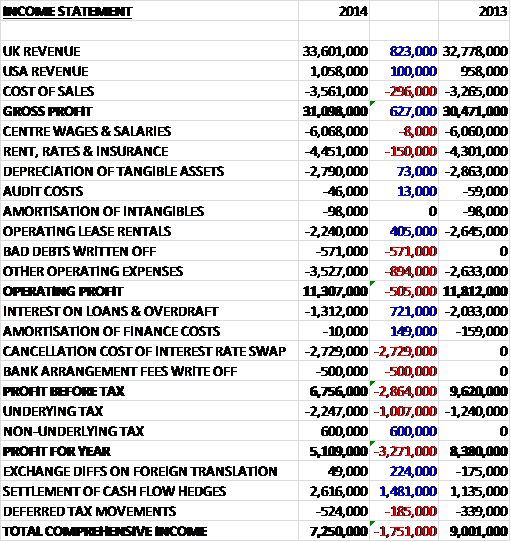

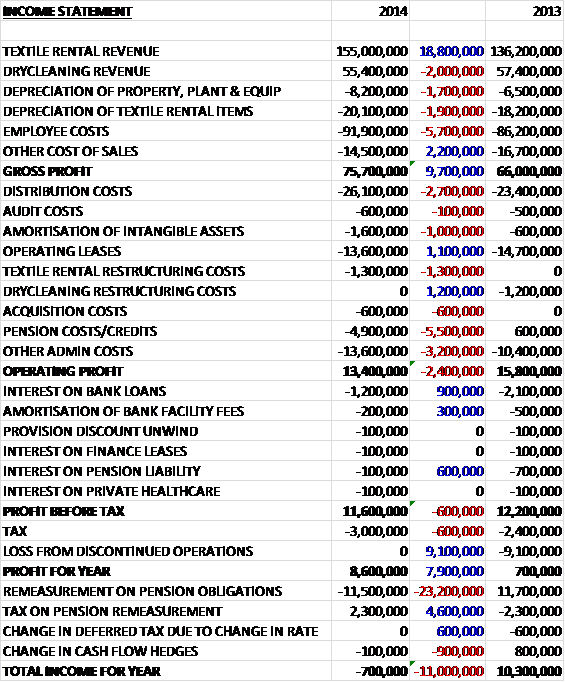

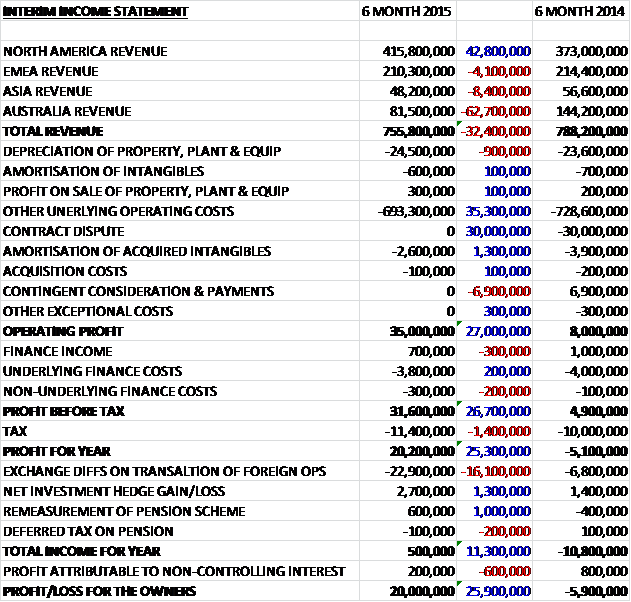

When compared to the first half of last year, total revenues fell by £32.4M as a £42.8M increase in North America revenue was more than offset by a £62.7M collapse in Australia revenue, an £8.4M fall in Asia revenue and a £4.1M decline in EMEA revenue. Underlying operating costs fell considerably, though, and the group also benefited from the lack of a £30M charge relating to the contract dispute but there was also no contingent consideration credit, which amounted to £6.9M last year relating to Keller Canada that the group no longer expects to pay. In all, operating profit was £27M ahead of the same point of last year which became an increase of £25.3M to £20.2M after finance costs and tax. It should be noted that translational exchange differences completely wiped this profit out, however.

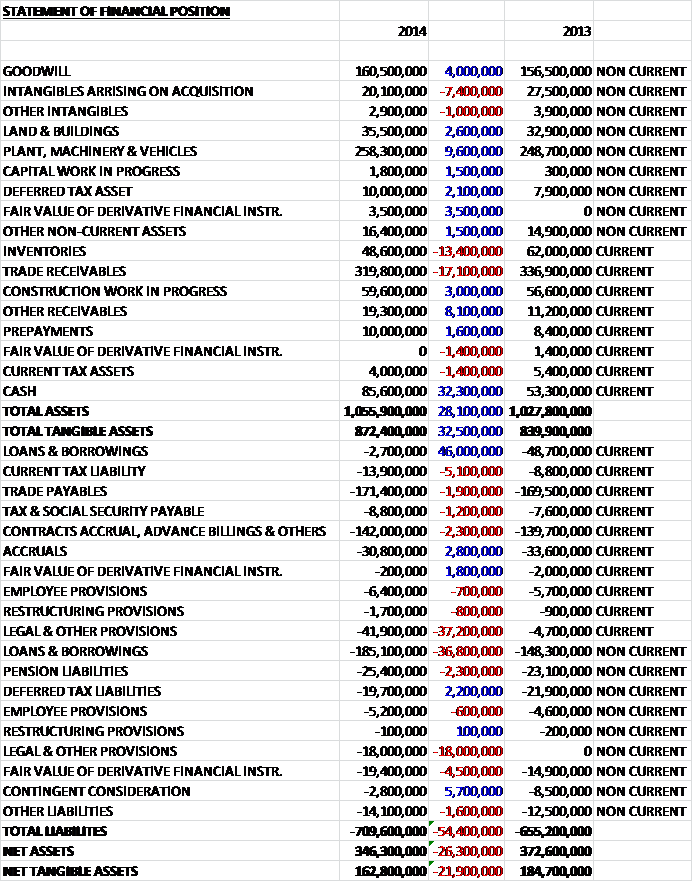

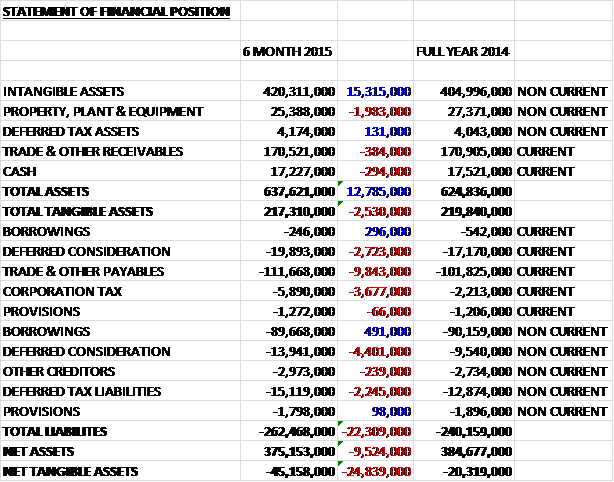

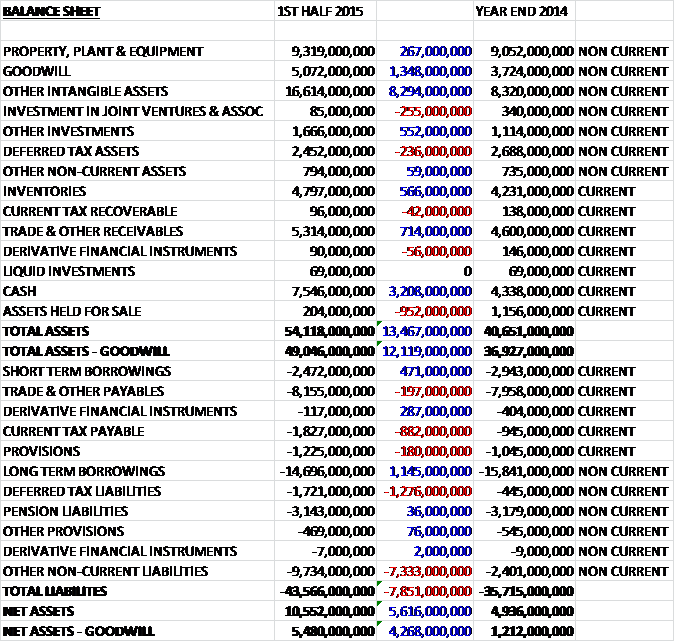

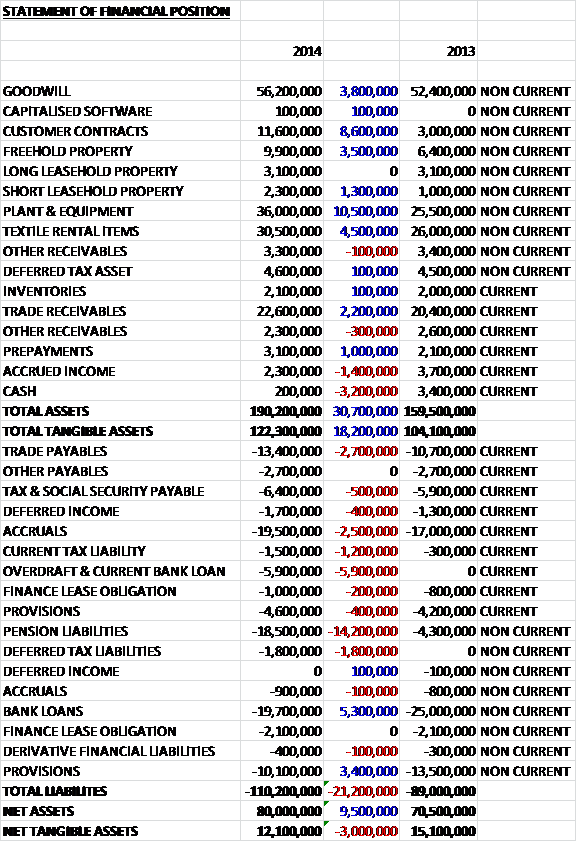

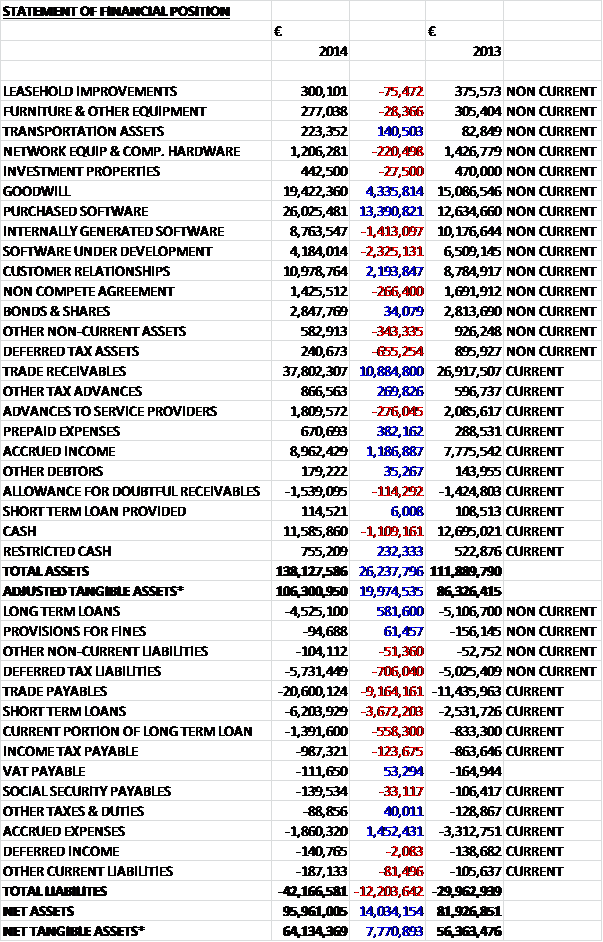

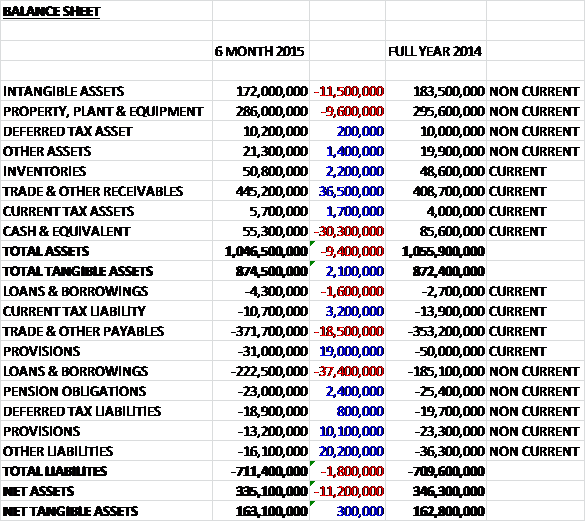

When compared to the end point of last year, total assets fell by £9.4M driven by a £30.3M fall in cash, an £11.5M decline in intangible assets and a £9.6M decrease in property plant and equipment, partially offset by a £36.5M increase in receivables. Liabilities also increased during the year as a £38M increase in borrowings and an £18.5M growth in payables was partly offset by a £20.2M fall in “other” liabilities, and a £29.1M decline in provisions relating to the payment of the litigation costs. The end result is a net tangible asset level of £163.1M, broadly flat when compared to the end of last year.

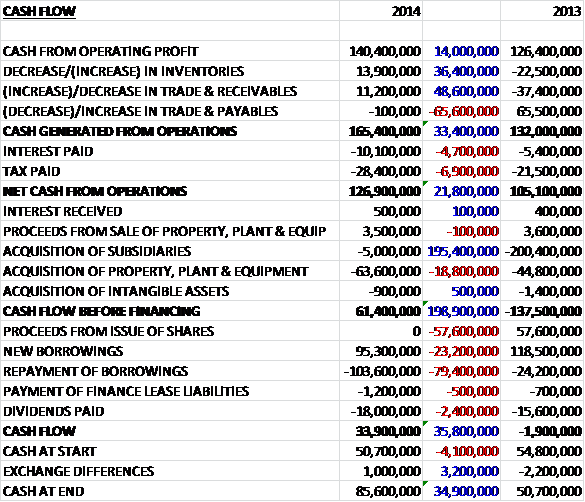

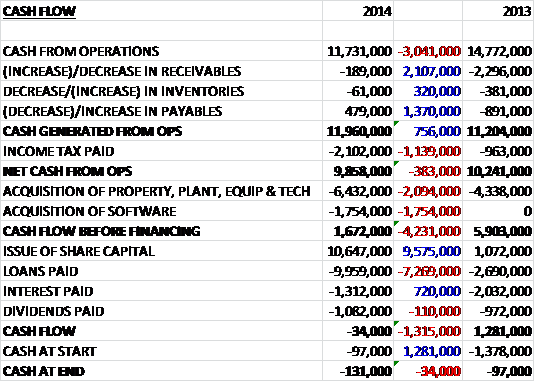

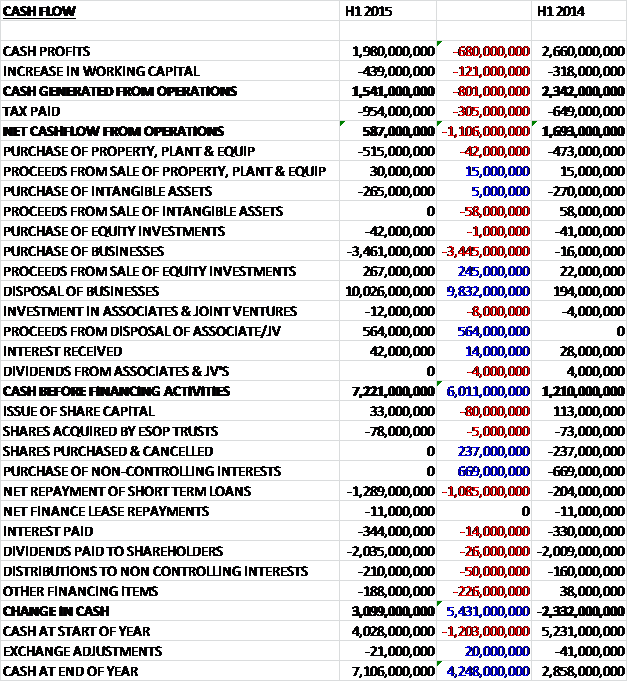

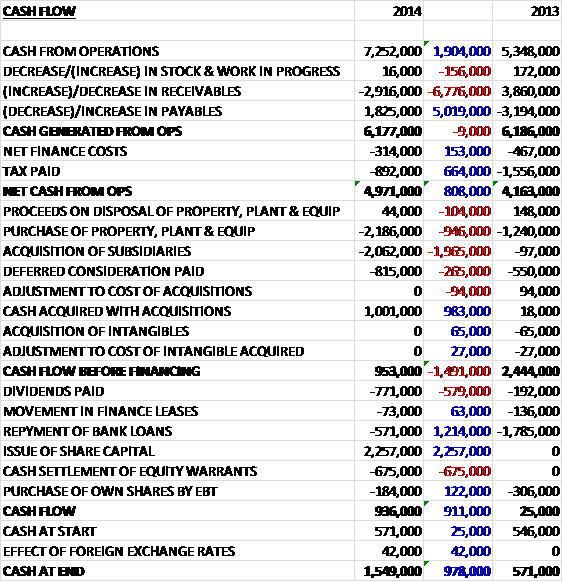

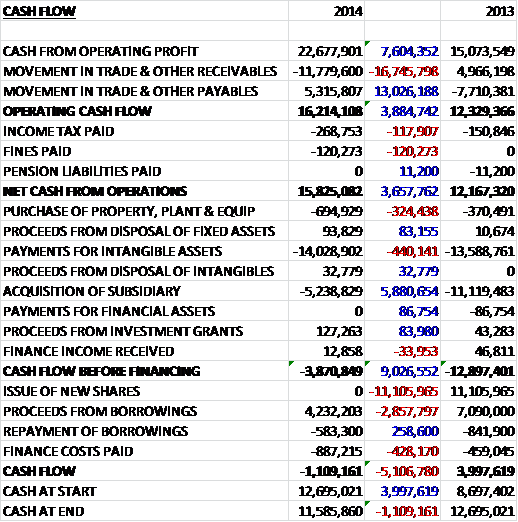

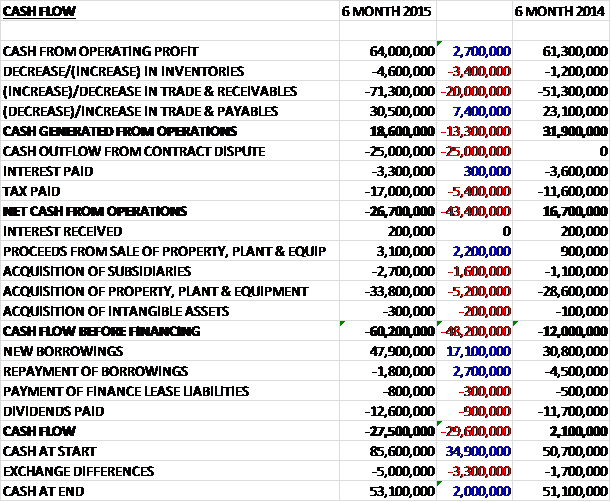

Before movements in working capital, cash profits increased by £2.7M to £64M. A huge increase in receivables, however, was not entirely offset by an increase in payables so that cash from operations fell by £13M to £18.6M. We then see the £25M payment relating to the contract litigation and a £5.4M increase in tax provide a net cash outflow at the operating level of £26.7M. The group then spent a further £33.8M on fixed assets to give a cash outflow before financing of £60.2M. The group then took out a net £46.1M of new borrowings which enabled a £12.6M payment of dividends but the cash outflow for the half year was still £27.5M to give a cash level of £53.1M at the period end, although it should be noted that the group seems to be more cash generative in the second half of the year.

Operating profit at the North America division was £28.4M, an increase of £7.7M year on year and the operating margin increased from 5.5% to 6.8%. In the US the value of total construction expenditure in the period was up 6% compared to the same period last year. Private expenditure on construction, both residential and non-residential, increased by 7% whilst public construction spend was up 3%.

The US business continued to take advantage of the improved market conditions with activity levels picking up significantly in Q2 after a slow start to the year due to adverse weather conditions. Case, in particular, performed well and bid on a record number of large projects. The Amtrak Catenary Pole Foundation work is now over halfway complete and the business secured significant work on the hydroelectric plant at Red Rock Dam on the Des Moines River in Iowa, as well as a large project on phase 1 of the $1.3BN Capitol Crossing private development in the District of Columbia.

More generally, the US piling companies had an excellent first half with profit up significantly up on last year. Contract awards in the period were strong and they enter the second half of the year with a record order book. Hayward Baker reported a steady first half performance, aided by the final settlement of two large contracts. Results varied across its diverse sectors, reflecting differences in local market conditions. Progress on the Elliott Bay seawall project in Seattle, which was delayed earlier in the year, is now back on track. Suncoast, which is mainly focused on residential construction, had a solid first half and is apparently well set to benefit from the recent increase in housing starts.

Market conditions in Canada continued to be difficult, with investment in the Canadian resources markets, particularly the oil sands market, at a very low level. As a result the group have seen increased competition in commercial and infrastructure construction, adversely impacting margins in these areas. Against this challenging market backdrop, Keller Canada recorded lower profits than in the same period of last year. Costs have therefore been cut in a number of areas.

Operating profit at the EMEA division was £7M, an increase of £4.3M when compared to last year with margins increasing from 1.3% to 3.3%. Most European construction markets continued to be challenging, so far the group has not seen many signs of a market recovery and competition remains intense. Better prospects have been seen in the Middle East and African regions, however.

The group’s German subsidiary produced a good result and the business in Poland, after a quiet first half, is well set for the remainder of the year. The major rail project in Austria announced earlier in the year is now up and running, underpinning a much improved result in that country. Having completed major projects at Crossrail and Victoria station, revenues in the UK were down year on year but strong recent contract awards should lead to an improved second half to the year. The businesses in Southern Europe continued to face very difficult market conditions. The Middle East and Africa, particularly South Africa, performed well during the period and the work on Ada phase 2, a major jetty project on the coast of Ghana, progressed well. The group are now mobilising on a major project in the Caspian region after some earlier delays.

Operating profit at the Asia division was just £600K, a decline of £3M when compared to the first half of 2014 and margins collapsed from 6.4% to 1.2%. This performance was partly explained by the timing of revenues from major projects with much of the revenue for the Sengkang hospital project occurring in the first half of last year while this year has seen delays in the start of the project at Changi airport. This much reduced revenue in Singapore was combined with more difficult market conditions in other parts of the region which has been affected by lower oil and gas investment following the continued decline in the oil price.

Another issue being faced are measures by the Singaporean government to reduce foreign investment in real estate which adversely impacted investment in residential construction. Looking forward, short term prospects are more encouraging. Resource Piling has just started the foundations for another large hospital project for the Ministry of Health in Singapore whilst Ansah is beginning a number of packages of work on the RAPID petrochemical and refining complex in Southern Malaysia. Keller India had a good first half, with results ahead of expectations in a market where there are some early signs of recovery and the potential for some significant projects for the group.

Operating profit at the Australia division was £4.2M, a collapse of £6.4M when compared to the first half of last year with a margin that fell from 7.4% to 5.2%. The decline in performance in the country is largely the result of the completion last year of the work on the on-shore LNG processing plant in Wheatstone. The construction market in Australia remained challenging and major projects in the resources industries are scarce. Commercial and residential construction also remain slow and there is a lull in investment in infrastructure, not helped by the changes in state governments. The group has therefore further reduced costs in the country as whilst there is a pipeline of significant projects being tendered, their timing remains uncertain.

Waterways, the near-shore construction business remained busy, however, despite the general malaise in the market. Austral, the acquired business, provides piling and civil construction services to the infrastructure and mining industries, with a particular focus on near-shore marine work.

As can be seen, there has been a payment of £25M in cash as a result of the settlement agreement. The remainder of the costs are due to be incurred over the next year and they are substantial.

After the end of the period, the group acquired the Austral Constructions for an initial cash payment of £20.5M and a deferred payment of up to £9.8M dependent on Austral’s EBITDA earned in the three years to 2018. The acquisition complements the group’s existing expertise in near-shore marine work in Australia. It is certainly a brave move to make a large acquisition in Australia but I would hope that the amount paid would reflect this. The group also announced that it had reached a conditional agreement to acquire the net assets of the GeoConstruction group of Layne Christensen for an initial cash consideration of £25.4M with the acquisition expected to complete by the end of August.

While conditions remain challenging in many of the markets in which the group operates, the recovery in US construction remains robust and this together with a 5% increase in the order book and the benefits from the improvements management have implemented, gives the board confidence that results for the year as a whole will be in line with market expectations.

At the current share price the shares yield 2.4%, increasing to 2.6% for the year as a whole. At the end of the year, the group was in a net debt position of £171.5M compared to £102.2M at the end of last year and £161.9M at the same point of last year.

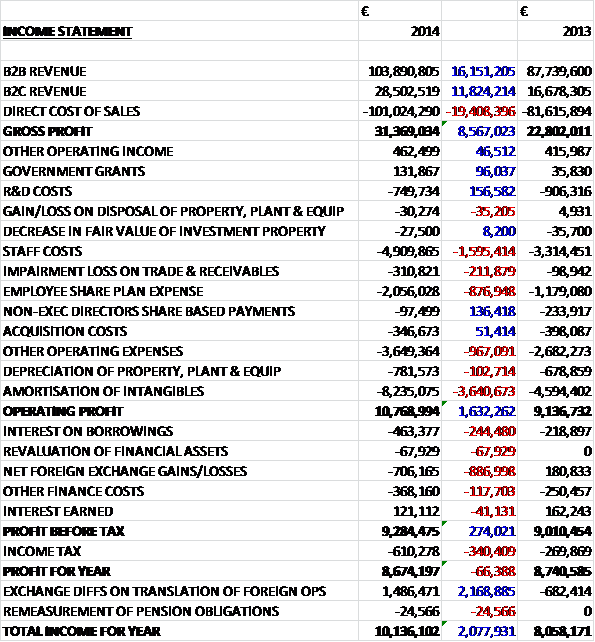

Overall then this was a robust performance I think. Profits improved, even when the contingent consideration credit and the litigation cost last year are removed and net assets remained flat. Underlying cash profits did improve slightly but the operational cash flow took a real hit, partly as a result of the first payment relating to the litigation but also partly due to a big increase in receivables which I suspect is somewhat seasonal. Operationally, things are tough in many of the group’s markets. The continued weakness in commodity prices is hitting operations in Australia and Canada, the falling oil price is affecting the Malaysian business and the Singapore business has been hit by delays on the Changi airport project and the government’s decision to restrict foreign investment in real estate.

These negative headwinds are more than made up for by the small number of markets which are improving. India seems to be starting to show signs of life and the EMEA region in general seems to be slowly easing out of the doldrums but it is the US that is really driving the increase in profits. Construction in the group’s largest market really seems to be coming alive, although whether this will continue if interest rates are increased there remains to be seen.

Overall then, this is a tricky one, if a downturn were to hit the US, the group would be in quite a bit of trouble – there is likely to be continued cash outflow form the acquisitions and the litigation payments. Despite this, I believe we have a quality outfit here though and I am tempted to buy in but can’t help feeling a better entry point may present itself (famous last words!)

The shares have certainly recovered from the dip at the end of last year and now seem to be enjoying a decent run.

On the 16th November the group released a trading update. There has been no significant change in market conditions since the interim results. In North America, the US construction market continues to grow steadily while the market in Canada remains very challenging. European construction markets as a whole remain stable but the outlook in Australia shows no sign of improvement.

Overall trading for the group during the four months has been in line with management expectations. Year to date revenue remains down on last year as a result of lower revenues from major products, primarily due to the completion of the Wheatstone project last year. Operating profit is ahead of the same time last year, supported by solid operational progress and some good final project settlements, particularly in the US. The order book at the end of October for work to be executed over the next year is around 20% higher than at the same time last year and the board’s expectations for the group’s results for the full year remains in line with market expectations.

The acquisitions of GeoConstruction for £29M and Austral Construction for £19M were both completed in the period but other than this there has been no material change in the financial position of the group since the end of June.

The ongoing improvement in the US construction market continues to contribute to good results from the US business as a whole with Suncoast continuing to benefit from the increase in housing starts. Bencor, the business they bought earlier in the year for its advanced diaphragm wall technology, is being successfully integrated and working on a number of prospects with the other Keller businesses. The Canadian business is operating in a very difficult market but ongoing cost reductions have enabled the business to record a small profit.

The EMEA division has continued to produce results ahead of last year, helped by good profitability in German, Poland and Austria and Franki Africa is performing well and seeing increased opportunities in the Middle East. The major contract in the Caspian region continued, albeit slower than original anticipated and the next $25M of work has just been confirmed.

The performance of the Asian business has improved in recent months and the division will have a much better second half. The result is underpinned by a major project in the refinery and petrochemical integrated development project in SE Johor, Malaysia where the group has just secured another contract bringing the total value of their contracted projects in the area to $46M. In October they won their first major ground improvement project in Indonesia for about $25M of vibro-compaction works at Pluit City, a newly created island located near Jakarta.

In Australia the foundations business continues to struggle in a difficult market and further cost reductions are being implemented. The group expect to reach agreement on a final settlement on Wheatstone before the end of the year which will benefit the 2015 Australia results. Waterways and Austral, the near-shore marine construction specialists, continue to perform well. The integration of Austral is proceeding to plan.

The group has recently completed a strategic review of its organisational capabilities. Changes include the strengthening of key functions, formalising product teams and rationalising structure where appropriate. The Asia and Australia divisions are set to merge from the start of 2016 and the structures within both are under review.

In summary, while conditions remain challenging in many of the markets they operate in, the US construction market remains healthy and this, together with the benefits from cost-cutting measures means that the board is confident that the results for the full year will be in line with expectations. Nothing much has changed here really, but the share price has come down quite a bit and despite the problems affecting many of the group’s markets as long as the US construction industry remains strong, they should be ok. The shares are therefore starting to look rather cheap to me.